Can Autoimmune Diseases Become China's Second-Largest Therapeutic Market? Insights from Recent IPO Filings

As GLP-1 products continue to break data records this year, the domestic market has new expectations for blockbusters and mega-blockbusters: with advances in drug research, along with improved living standards and greater disease awareness, there are more blue-ocean opportunities beyond oncology.

Attention has increasingly shifted to the field of autoimmune diseases. Globally, autoimmune diseases represent the second-largest therapeutic market; however, innovative autoimmune drugs have yet to gain significant traction in China. In 2022, the global market size for autoimmune disease medications was approximately $131.7 billion, whereas the Chinese market stood at only about $3.6 billion—less than the annual global sales of secukinumab alone.

Humira, the “king of drugs,” entered the Chinese market in 2010, but its domestic sales only just reached the RMB 1 billion mark as the product approached the twilight of its patent period.The Journey of Humira in China: A Microcosm of the Development of the Domestic Autoimmune Field:For a long period, the clinical penetration rate of autoimmune disease medications remained low, with few patients able to afford the high treatment costs. After being included in the National Reimbursement Drug List, Humira faced further market compression from domestically produced alternatives offered by local companies at more competitive prices.The journey of innovative drugs for autoimmune diseases—from inception to market entry, from imports to domestically produced alternatives, and from high costs to affordable pricing—is unfolding rapidly.

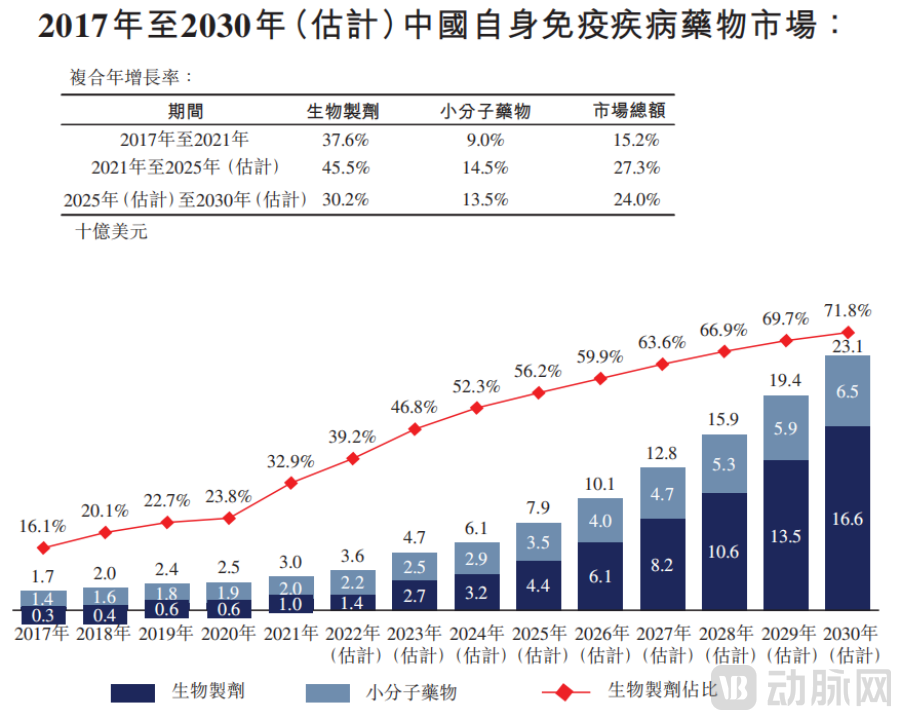

The clinical efficacy of innovative drugs for autoimmune diseases is undeniable. Given that patients are predominantly young and middle-aged adults, with a high proportion of females, and require long-term treatment, there is a substantial unmet medical need. According to Frost & Sullivan, the market size of autoimmune disease drugs in China is projected to reach approximately $23 billion by 2030.However, considering the supply of innovative autoimmune drugs, market education, and drug accessibility in China, it will take time for the autoimmune disease sector to grow into the second-largest therapeutic market. Moreover, global sales trends for autoimmune medications cannot be directly extrapolated to the Chinese market.

Source: Frost & Sullivan Report

Is the 100-Billion Market Real?

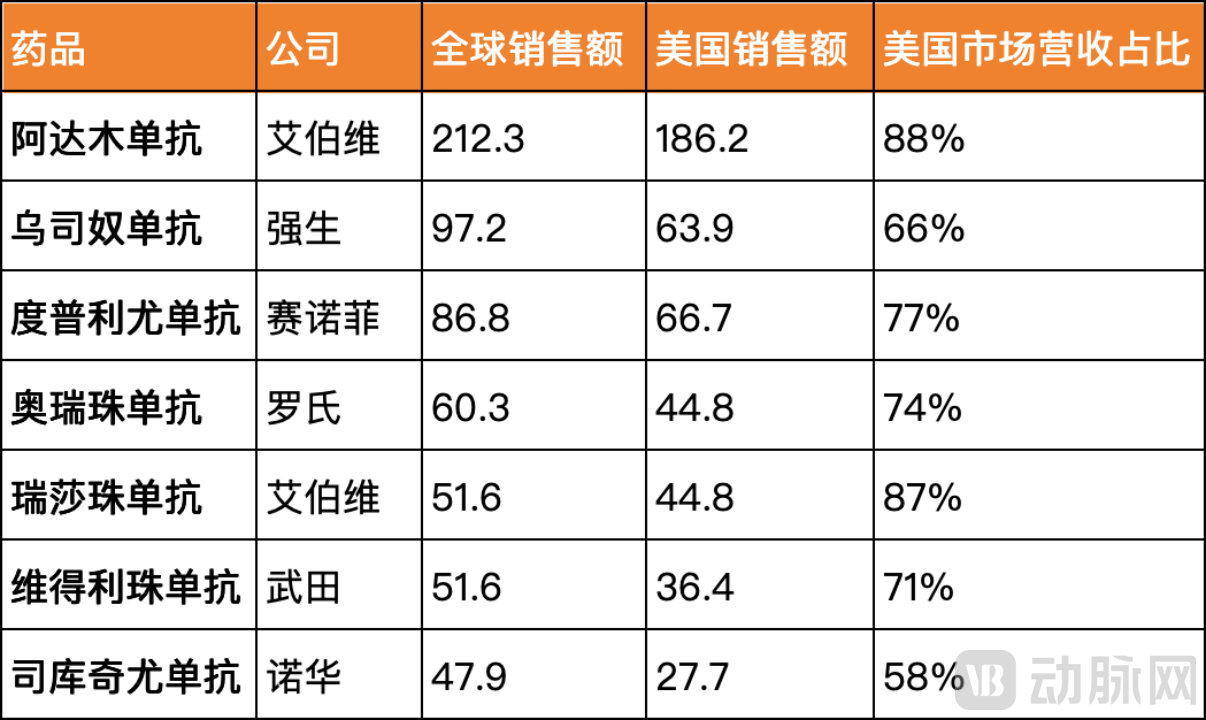

Blockbuster Drugs Emerge in the Autoimmune Field: A Global Market PerspectiveIn 2022, among the top 100 global pharmaceutical products by sales, there were 22 autoimmune drugs, which collectively generated $97.4 billion in sales, with an average of $4.4 billion per drug.

However, from the perspective of regional sales composition, the U.S. market is the key to creating blockbuster drugs. Based on 2022 sales figures, the U.S. market accounted for more than 50% of the revenue for each of the seven top-selling autoimmune drugs globally, with Humira (adalimumab), dupilumab, and risankizumab deriving over 75% of their revenue from the U.S. market.

Global Top 7 Autoimmune Disease Drug Sales in 2022 (Unit: $100 Million)

U.S. sales figures are based on the number of autoimmune disease patients in the United States. According to updated 2022 data from the National Institute of Environmental Health Sciences, autoimmune diseases affect more than 24 million people in the U.S. Meanwhile, the American Autoimmune Related Diseases Association (AARDA) estimates that the number of autoimmune patients nationwide is as high as 50 million. In other words, 10%–20% of Americans suffer from autoimmune diseases.

The U.S. autoimmune diagnostics market also ranks first globally. According to a 2016 report by Kalaroma Information, the North American market accounted for 42% of the global autoimmune diagnostics market, the European market accounted for approximately 37%, while the Chinese market represented only 3%.

The domestic autoimmune diagnostics market in China is still in its nascent stage. According to the prospectus of HybriMed, an in vitro diagnostics company specializing in allergy and autoimmune testing, the size of China’s autoimmune diagnostics market was only RMB 1.1 billion in 2018. Industry experts estimate that, based on a conservative assumption of a 5% positivity rate for autoantibodies among individuals undergoing health check-ups, the total addressable market for autoimmune disease diagnostics in China should be approximately RMB 7 billion.

Delving deeper into the underlying causes, there is a general lack of attention paid to autoimmune diseases in China, particularly among primary healthcare institutions. Since symptoms in patients with autoimmune diseases are often not critical, healthcare providers may overlook them, while patients have ample time to seek care at higher-level hospitals. Most secondary hospitals and those below lack the capacity to diagnose autoimmune diseases. Meanwhile, low diagnostic capabilities have led to low confirmation rates for these conditions. Patients with autoimmune diseases are frequently referred to departments such as nephrology, hepatology, hematology, and endocrinology for treatment, resulting in a large pool of undiagnosed potential patients in China.

According to incomplete statistics, there are approximately 50 million patients with autoimmune diseases in China.However, if “autoimmune diseases” is replaced with “rheumatic diseases,” the vastness of the domestic market becomes even more apparent.Common diseases such as rheumatoid arthritis, gouty arthritis, and allergic asthma are all included in the Department of Rheumatology and Immunology.

In 2019, the National Health Commission issued a document requiring and encouraging hospitals to establish departments of rheumatology and immunology. All tertiary hospitals across China were mandated to set up such departments with at least 10 beds, and to have an independent clinical laboratory capable of supporting routine testing for rheumatic and immune-mediated diseases.

Although rheumatology is a key department for autoimmune diseases in China, Hu Chaojun, an expert from the Department of Rheumatology and Immunology at Peking Union Medical College Hospital, stated that in 2021, only about 770 of the 2,427 tertiary hospitals nationwide had independent rheumatology departments. This means that 1,657 tertiary hospitals still need to establish independent departments of rheumatology and immunology.

Drawing on the development trajectory of oncology hospitals in China, during the rapid growth phase from 2000 to 2009, the number of oncology hospitals expanded swiftly, quickly surpassing 100, and the market size for oncology medical services increased accordingly.

Whether compared horizontally with mature markets or viewed longitudinally within the oncology sector, the autoimmune disease field boasts broad development prospects, and its pharmaceutical market indeed holds potential worth hundreds of billions. However, due to China’s overall weak foundation, volume growth will remain relatively slow.

Drug Supply: Can Domestic Companies Keep Up?

In a sense, the development trends of autoimmune drugs and consumable medical devices are remarkably similar.From the perspective of meeting the demand gap, the pressure to increase penetration rates is very clear:According to the “Research Report on the Disease Burden of Psoriasis and Quality of Life of Patients in China” and the “Survey Report on the Living Conditions of Patients with Atopic Dermatitis in China,” more than 62% of patients in China are dissatisfied with the treatment outcomes for psoriasis, and over 75% of physicians are dissatisfied with the existing treatment regimens for atopic dermatitis;From the supply side, autoimmune disease therapeutics remain a high-quality area for innovative entry:Conventional therapies, including nonsteroidal anti-inflammatory drugs (NSAIDs), conventional disease-modifying antirheumatic drugs (DMARDs), and glucocorticoids, remain the mainstream in China; approved biologic agents for autoimmune diseases are predominantly from multinational corporations (MNCs).

The pathogenesis of autoimmune diseases is complex, posing significant challenges in evaluating the efficacy and toxic side effects of drugs targeting novel mechanisms, thereby creating substantial barriers to research and development. Furthermore, therapeutic approaches and commercialization models differ markedly from those in oncology. According to statistics from VCBeat, among the numerous companies in China engaged in the development of autoimmune disease products, only a few are deeply committed to this field. Of the nearly 80 “active players” in new drug development listed on the A-share and H-share markets, 43 have entered the autoimmune disease sector. However, 28 of these companies (65%) have fewer than two pipeline products in this area, and only five companies (12%) have more than three products under investigation.

However, some domestic pharmaceutical companies have achieved preliminary R&D results in disease areas such as atopic dermatitis, psoriasis, rheumatoid arthritis, and systemic lupus erythematosus. In the field of psoriasis, several drugs have reached the Phase III clinical stage or filed for marketing approval. Leading companies in terms of R&D progress include Hengrui Medicine, Akeso, Quanxin Biotech, and 3SBio.

Domestic Psoriasis Pipeline

The autoimmune disease sector in China started relatively late, so it is still at a stage where low-hanging fruit can be picked. Many autoimmune targets, like PD-1, are broad-spectrum. Although PD-1 has long become synonymous with intense competition, the manufacturers that ranked among the top three or four in the PD-1 race have all transformed into Biopharma companies by leveraging this opportunity.IL-17, IL-5, and IL-4 are all well-established blockbuster targets. If clinical development in China ranks among the forefront, there is a significant opportunity to develop me-better products, continuously expand market potential through differentiated design, and capture the domestic market still dominated by multinational corporations (MNCs).

This also means that commercial competition between domestic companies and industry giants will gradually intensify. For example, Humira (adalimumab), which was among the first products to face intense market competition, now has seven biosimilars approved in China. Although Humira is included in the National Reimbursement Drug List, its first-year cost and annual maintenance cost still exceed RMB 30,000. In contrast, Chinese-made adalimumab biosimilars, such as Glairy, Handayuan, and Sulixin, require only around RMB 15,000 for the first year and annual maintenance, thanks to patient assistance programs and other measures.

In August this year, the first domestically produced ustekinumab biosimilar also filed for marketing approval. This biosimilar, QX001S, was jointly developed by Quanxin Biopharma and Zhongmei Huadong, and is indicated for the treatment of moderate-to-severe plaque psoriasis in adults.

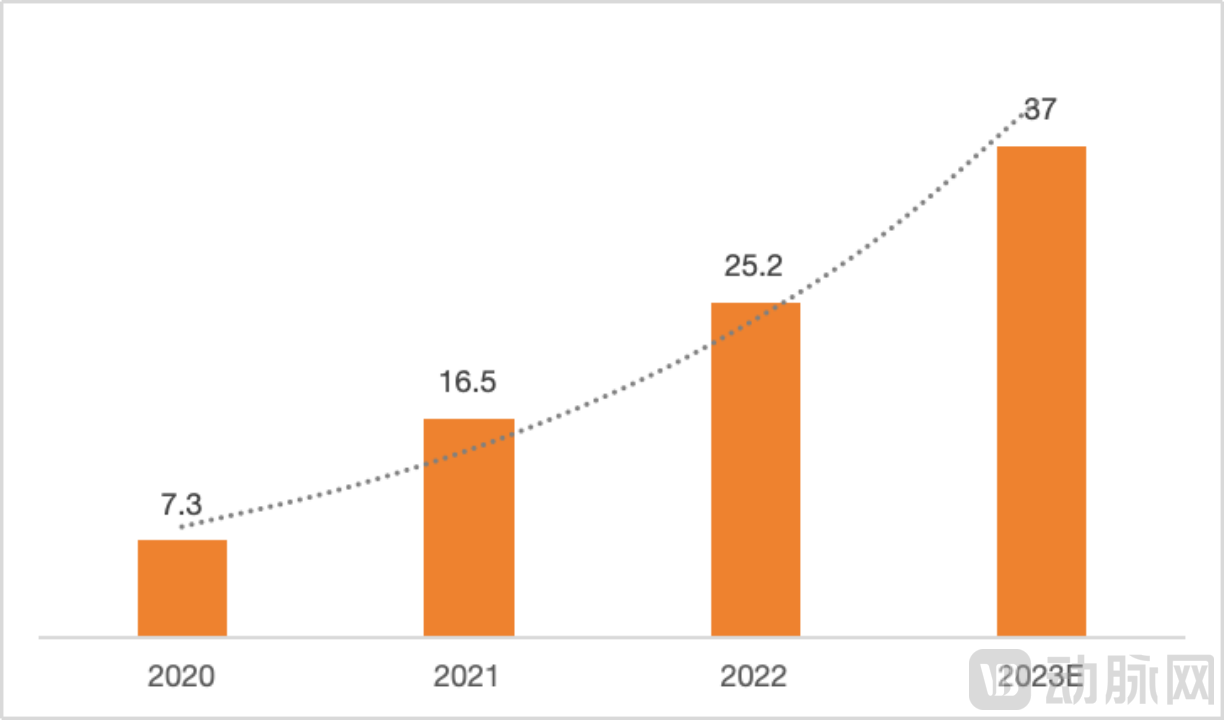

It is worth noting that, due to the relatively short development history of the autoimmune disease field in China, targeted small-molecule immunosuppressants have only recently emerged and demonstrated their ability to compete on par with biologics.The main characteristics of small-molecule immunosuppressants, particularly JAK inhibitors, are their high efficacy and rapid onset of action. Upadacitinib, a representative second-generation JAK inhibitor, was launched in the United States in 2019 and in China in 2022. Its global sales exceeded $1.6 billion in the first half of 2023 alone, with $1.1 billion in sales recorded in the third quarter of 2023, representing a growth rate of approximately 60%.

Global Sales Data of Upadacitinib (Unit: USD 100 Million)

“Upadacitinib’s rapid sales growth reflects a very high level of market acceptance. A survey in Europe assessing satisfaction with JAK inhibitors and biologics for the treatment of rheumatoid arthritis found that both patients and physicians reported significantly higher satisfaction with JAK inhibitor therapy than with biologics. Furthermore, a real-world data study conducted among Australian patients revealed an upward trend in the proportion of rheumatoid arthritis patients receiving JAK inhibitors as initial therapy, as well as an increasing rate of JAK inhibitors being selected as first-line treatment,” stated Dr. Wan Zhaokui, founder of LinkMed Pharmaceuticals. LinkMed is an innovative autoimmune disease drug developer focused on the development of second-generation highly selective JAK inhibitors and third-generation tissue-specific JAK inhibitors. The company has advanced multiple products into clinical trials and successfully completed its Series C financing round this year.

“Compared with biologics, small-molecule inhibitors are more convenient to manufacture, transport, and store; the regulatory framework is relatively mature; and they offer a pronounced price advantage. As they are administered orally, patient adherence is high. Publicly available data indicate that newly launched small-molecule JAK inhibitors have demonstrated superior clinical efficacy and a faster onset of action compared with biologics.”Based on market feedback, domestic patients and physicians in China have a higher acceptance of small-molecule immunosuppressants compared to their overseas counterparts; beyond efficacy and speed of onset, price is also a significant factor.It can be said that the promotion of small-molecule immunotherapeutic agents in China is far faster than overseas.”

According to public data, the number of JAK inhibitors led by domestic companies in research and development has exceeded 20.

Industry insiders have stated that an increasing number of domestically developed innovative drugs for autoimmune diseases will be submitted for market approval, which is good news for patients and beneficial for overall market development. However, domestic autoimmune drugs still need to overcome barriers, address safety concerns, and cope with potential “new involution,” so as to provide the market with products that offer higher efficacy, greater safety, and better cost-effectiveness and convenience.

Can “Accessibility” and “Blockbuster Drugs” Coexist?

In addition to insufficient supply, low drug accessibility has long been a major factor hindering the development of the autoimmune disease sector in China. In the United States, high drug prices and continuous price increases have been key drivers behind the emergence of blockbuster autoimmune drugs. Between 2009 and 2019, AbbVie raised the price of Humira by 18-fold, and in 2021, the price of Humira increased by another 7.4%.

However, in China, drugs seeking market access can hardly bypass the “price-for-volume” strategy.

Novartis was among the first multinational corporations (MNCs) to recognize this. According to Novartis’ statistics from April this year, more than 300,000 patients in China have used secukinumab (Cosentyx) since its market launch in 2019, accounting for 30% of the global patient population. This achievement is closely tied to Novartis’ pricing strategy in China. Secukinumab was initially priced at RMB 2,998 per injection upon entering the Chinese market, a stark contrast to the $7,301 price tag in the United States without insurance coverage. The drug was included in China’s National Reimbursement Drug List in 2022, reducing its price to RMB 1,188, and it was further reduced to RMB 870 this year.

Data shows that secukinumab is the most widely adopted new drug approved in the past five years, having entered the largest number of tertiary hospitals in Beijing, with more than half of these hospitals offering the treatment. Beyond first-tier cities, Novartis has made significant efforts to penetrate lower-tier markets; for instance, secukinumab is available in Tonghua County, Henan Province, where patients pay only RMB 130.5 out-of-pocket after 85% reimbursement through medical insurance.

While secukinumab has become the most familiar drug among psoriasis patients in China, its growth rate has stagnated due to price reductions.

Zhong Chongming, a health insurance research expert, stated, “Autoimmune drugs in China will not generate tens of billions of dollars in revenue as they do abroad, particularly when covered by national health insurance. Similarly, semaglutide would not achieve high sales volumes if it were simultaneously covered by national health insurance.”

Prices of Certain Autoimmune Disease Medications Before and After Inclusion in the National Reimbursement Drug List; Note: Prices may vary due to differences in local reimbursement policies and fluctuations in drug discounts.

Zhong Chongming believes that autoimmune drugs are strongly tied to medical insurance due to their characteristics. “The indications for autoimmune drugs cover people of all age groups and require long-term medication, making it unavoidable for medical insurance to bear the payment responsibility. Once included in medical insurance, it may lead to ‘welfare rigidity.’ For pharmaceutical companies, having autoimmune drugs covered by medical insurance co-payment opens up new user markets downward in the income-based pyramid population, and the lower you go, the larger the cross-section of the population becomes.”

Furthermore, the rapid iteration of autoimmune disease drugs means that prioritizing national reimbursement negotiations can reduce long-term uncertainty, but it will also test pharmaceutical companies’ short-term strategies and operations.

The autoimmune disease landscape encompasses a wide variety of conditions and features a complex market. Given China’s economic development and payment capacity, it may be inappropriate to extrapolate or envision its prospects based on the notion of a “hundred-billion-yuan market” or “ten-billion-yuan blockbuster drugs.” What is certain, however, is thatInnovative autoimmune disease pharmaceutical companies have positioned themselves at the forefront of national medical insurance policies that support innovative drugs and domestic substitution. If these companies can successfully expand their presence in the autoimmune market and leverage medical insurance funds to sustain innovation, Chinese Biopharma and Biotech firms will secure another major growth pillar beyond oncology, significantly boosting their revenue and brand value.

References

Market Size Reaches RMB 3 Billion: The Breakout Dilemma Facing Followers of the “Autoimmune Miracle” - Amino Finance, https://mp.weixin.qq.com/s/mtsTRCwBQNYzp0-S_yVCnw

Innovative Drugs: Could Autoimmune Diseases Be the Oncology of a Decade Ago? - Pharma Investment Tribe, https://mp.weixin.qq.com/s/GiDNFzMuFZOSup4EEL4Q_A