WuXi XDC Completes Hong Kong's Largest Biotech IPO Since 2022, Becomes Sole ADC-Focused CRDMO Listed on HKEX and NASDAQ

WuXi XDC

End-to-End CDMO Service Provider for Biologics Conjugation Drugs

Today, the Hong Kong Stock Exchange witnessed its largest biopharmaceutical IPO since 2022: WuXi XDC successfully listed just four months after filing its application. In yesterday’s grey market trading, shares closed up more than 20%, valuing the company at approximately HK$30 billion.

Founded in 2020, WuXi XDC is the fifth listed company in the WuXi AppTec ecosystem. Its IPO has been both star-studded and highly anticipated:Cornerstone investors—including Invesco, General Atlantic, the Qatar Investment Authority, UBS Asset Management, Sequoia China, the Novo Nordisk Foundation, and Qingchi Capital—are all trillion-dollar equity funds, sovereign wealth funds, or specialized biopharmaceutical investment institutions, accounting for 66% of the allocation. Operating in the high-profile XDC sector, the company has seen its revenue grow nearly tenfold and its net profit increase eightfold over the past three years, driving the most enthusiastic retail subscription in the Hong Kong stock market this year. The listing of WuXi XDC not only further energizes the gradually recovering IPO market in Hong Kong but also brings a touch of spring to the biopharmaceutical sector, which has endured a prolonged winter.

Can the Highly Anticipated WuXi XDC Become the Next Legendary Stock on the Hong Kong Exchange?

The Only ADC CXO Company in Hong Kong and U.S. Stocks: WuXi Affiliate’s Bold Bet Pays Off

“Market Leader” is the most popular concept in the secondary market. Among listed companies in Hong Kong and the U.S., WuXi XDC is unequivocally the “first” and “only” CRDMO for antibody-drug conjugates (ADCs) and other bioconjugate drugs.

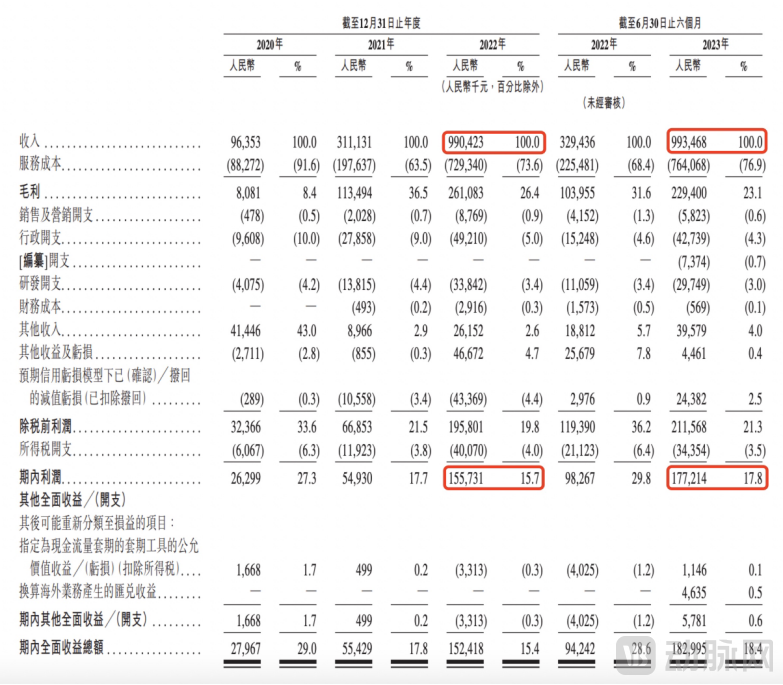

Based on 2022 revenue, WuXi XDC ranked second globally among CRDMOs for antibody-drug conjugates (ADCs) and other bioconjugate therapeutics, trailing only Lonza, which is listed in Switzerland.WuXi XDC disclosed its full financial results for the first half of 2023 in the updated prospectus following the hearing, showing that revenue and net profit for the six months ended June 30, 2023, reached RMB 994 million and RMB 177 million, respectively, both exceeding the full-year figures of RMB 990 million and RMB 156 million recorded in 2022.

WuXi XDC’s rapid development is inseparable from the strong support and investment of the WuXi AppTec ecosystem.WuXi Biologics entered the ADC business in 2013, and WuXi XDC was established by integrating the ADC operations of WuXi AppTec and WuXi Biologics.

To boost revenue, the WuXi group established direct transactions with it. The prospectus reveals that from 2020 to 2022, the amounts of non-exempt continuing connected transactions between WuXi XDC and the remaining entities of WuXi Biologics were RMB 51.5 million, RMB 253 million, and RMB 795 million, respectively. During the same period, the amounts of non-exempt continuing connected transactions between WuXi XDC and WuXi AppTec were RMB 0, RMB 23.3 million, and RMB 138 million, respectively, indicating a rapid surge in related-party transaction volumes.

WuXi XDC also sources the majority of its raw materials, such as various liquid containers and mixing bags, tubing, filters, and chemicals, through WuXi Biologics’ centralized procurement system. This approach leverages the resources of the WuXi Group while upholding its consistent standards for cost control and operational efficiency.

Furthermore, WuXi XDC has been receiving cash flows from the WuXi AppTec group. In 2021, 2022, and the first half of 2023, WuXi XDC obtained new related-party loans amounting to RMB 22.3 million, RMB 137 million, and RMB 28.5 million, respectively.

However, blood transfusions are not sustainable. In particular, WuXi Biologics has been affected this year by a revenue gap resulting from the end of the pandemic, leading to a 10.81% year-on-year decline in its net profit. At the Investor Open Day, WuXi Biologics disclosed that it had added 25 new CDMO projects in the first half of 2023 (before June 20), compared with 120 new CDMO projects added throughout the entire previous year.

Fortunately, WuXi XDC has leveraged its strong backing to become a leading flagbearer in the ADC CXO sector. In 2022, WuXi XDC captured 9.8% of the global market share for CRDMO services related to antibody-drug conjugates (ADCs) and other bioconjugate therapeutics. According to its prospectus, the company’s revenue dependence on WuXi Biologics has significantly decreased: in 2020, 2021, 2022, and the first half of 2023, its top five direct customers accounted for 98.0%, 91.1%, 61.2%, and 53.3% of WuXi XDC’s total revenue, respectively, while WuXi Biologics’ share of total revenue declined to 84.1%, 81.1%, 37.9%, and 13.8%, respectively.

This is attributable to WuXi XDC’s substantial accumulation of external clients: the number of clients was 49, 115, 167, and 169 at the end of 2020, 2021, and 2022, and in the first half of 2023, respectively. WuXi XDC has secured ADC development contracts for all ADC candidates in China that have filed Investigational New Drug (IND) applications and/or Biologics License Applications (BLA) in both China and the United States. Furthermore, since 2022, eight of the ten Chinese companies that have out-licensed their ADC pipelines overseas have been clients of WuXi XDC.

As of the first half of 2023, 10 Chinese companies with 14 ADC pipelines had licensed their overseas ADC pipelines to external partners.

After a decade of dedication to ADCs and three years of substantial investment, the WuXi AppTec group’s “bold bet” has undoubtedly proven successful. Following the global offering, WuXi Biologics holds a 50.91% stake. With the listing of WuXi XDC, WuXi Biologics’ “mission” has come to a close, marking the official launch of WuXi XDC.

Can Revenue Increase Tenfold Again?

WuXi XDC’s performance growth rate is already eye-catching, but from the perspectives of the XDC drug development pipeline, the momentum of domestic XDC companies, and the further advancement of conjugate drugs, the company still has significant room for growth potential.

First, the number of ADC drugs currently marketed globally remains limited, and the overall market is at an inflection point poised for explosive growth.Based on sales data from the first half of this year, several new antibody-drug conjugate (ADC) therapies have demonstrated encouraging performance. For instance, AstraZeneca reported global sales of Enhertu (DS-8201) at $1.169 billion in the first half of the year, representing a substantial 168% increase compared to $436 million in the same period last year. Meanwhile, Polivy, Roche’s second commercially launched ADC, achieved global sales of $513 million in the first half and is poised to surpass the $1 billion mark.

It is widely believed in the industry that after PD-1, ADC assets will become the "standard offering" for MNCs. However, current exploration of ADC applications remains in its early stages, with a relatively low efficacy ceiling. To advance toward first-line therapy, further improvement in efficacy may require combination therapies.

In other words, the discovery and clinical research of ADC-related projects will continue to advance and improve, with service contract values increasing as projects progress through later clinical stages.

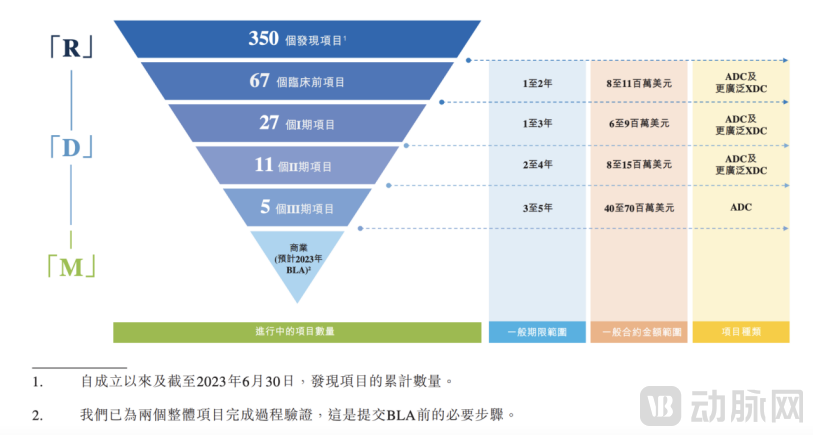

According to WuXi XDC’s prospectus, as of the first half of 2023, the company had 350 discovery projects, 67 pre-IND projects, 27 Phase I clinical trials, 11 Phase II clinical trials, and 5 Phase III clinical trials. The contract value of Phase III clinical projects is more than five times that of pre-IND projects.

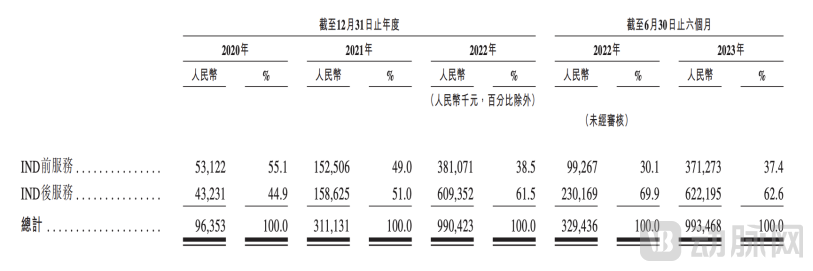

As WuXi XDC’s early-stage clients progressively advance to later-stage and commercialization phases, the company will benefit from more robust revenue streams. As evidenced in its prospectus, the proportion of revenue derived from post-IND services has been steadily increasing; from 2020 to the first half of 2023, the share of revenue from post-IND services rose from 44.9% to 62.6%.

Another growth driver stems from the R&D potential of Chinese companies in antibody-drug conjugates (ADCs) and other bioconjugate therapeutics.

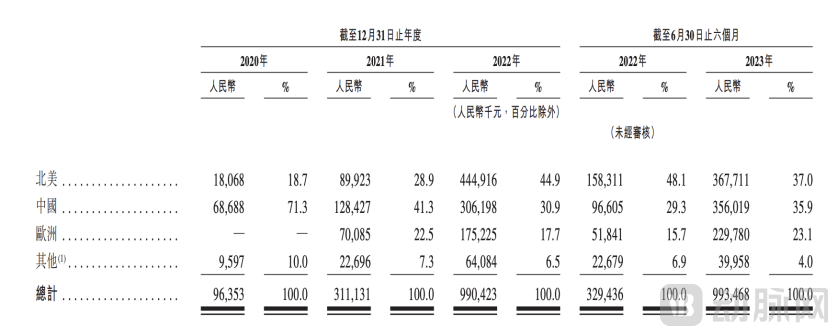

According to WuXi XDC’s prospectus, although the company’s revenue is primarily derived from overseas markets, the proportion contributed by the Chinese market has rebounded over the past year, rising from 29.3% in June 2022 to 35.9% in June 2023. This trend is attributable to the increasing investment by domestic pharmaceutical companies in the antibody-drug conjugate (ADC) field, particularly their more proactive efforts in pursuing differentiated designs.

The manufacturing of antibody-drug conjugates (ADCs) involves multiple stages, placing high demands on pharmaceutical companies’ capabilities in process development and quality control systems. Companies must possess substantial experience with both large-molecule and small-molecule therapeutics, as well as deep expertise in linker technology. While the underlying principle of ADCs is clear, it is also nuanced; the three components—antibody, payload, and linker—require iterative experimentation to achieve an optimal balance, tailored to different tumor types and tissue combinations. Domestic enterprises have developed strengths and extensive experience in technological platforms, clinical data generation, and the patience and know-how required for manufacturing.

Domestic ADCs entered a phase of explosive growth in 2021, with initial achievements becoming evident from the second half of 2022: several outbound licensing deals for Chinese ADC assets with potential total values exceeding USD 1 billion were closed within the past year. The licensors included both listed companies such as Kelun-Biotech and Keymed Biosciences, as well as strong biotech firms like Duality Biologics and Elix Biotherapeutics.

Many domestic companies candidly admit that the global expansion of their drug pipelines relies heavily on the critical support of CXOs, underscoring how WuXi XDC’s strong presence in the Chinese market can serve as a distinct competitive advantage.

Finally, the broad prospects of “connecting everything.”The XDC industry is expanding rapidly. The two components linked in these conjugates are not limited to monoclonal antibodies and small-molecule toxins; they can also include bispecific antibodies, peptides, synthetic polymers, radionuclides, enzymes, and other moieties.

According to the prospectus, the services offered by WuXi XDC include: Radionuclide Drug Conjugates (RDCs), Peptide-Drug Conjugates (PDCs), Antibody-Chelator Conjugates (ACCs), PEGylated proteins or peptides (PEG), Antibody-PROTAC Conjugates, Antibody-Oligonucleotide Conjugates (AOCs), and Fatty Acid Conjugates.

As of the first half of 2023, the Company had 67 non-ADC discovery projects and 12 non-ADC integrated projects, including four RDC projects, four PEGylation projects, three antiviral conjugate (AVC) projects, and one other project.

The market for bioconjugate drugs, such as ADCs, is projected to grow from $7.9 billion in 2022 to $64.7 billion by 2030.It can be said that as long as tumor therapy has not reached its limits, the potential for XDCs to conjugate with various targets remains virtually boundless, not to mention that their innovative designs have already expanded into fields such as autoimmune diseases.Given the vast market size and WuXi XDC’s exceptionally high outsourcing rate, its future performance looks promising.

Can It Take the Top Spot in the Industry?

WuXi XDC, a rising star, has climbed to the number two spot globally in just three years, but overtaking Lonza, the traditional industry leader and current global number one, remains a significant challenge.

According to Frost & Sullivan’s analysis and company annual report statistics, Lonza holds a 21.4% market share in the CRDMO sector for antibody-drug conjugates (ADCs) and other bioconjugated drugs, significantly surpassing WuXi XDC’s 9.8%.

Lonza entered the ADC market in 2006, becoming one of the first CDMOs globally to achieve commercial-scale conjugation manufacturing. By 2021, while WuXi XDC was still in its early stages, Lonza had already secured the majority of commercial-stage ADC projects worldwide. Recently, Lonza has not only continued to expand its production capacity but also directly joined the ranks of ADC developers and acquirers by acquiring the ADC company Synaffix.

One of the primary factors constraining the release of WuXi XDC’s business potential is production capacity,Even due to the rapid growth of business, insufficient production capacity and outsourcing of raw material production projects have led to a decline in the company's profits.

Therefore, it can be seen thatThe primary use of the funds raised in this IPO is to build new production capacity:51% of the funds raised will be used to construct facilities at the Singapore base, including four production lines with an estimated floor area of 18,500 square meters, commencing GMP-compliant operations by 2026; 16% of the funds raised will be allocated to further expanding domestic production capacity, including the construction of a kilogram-scale linker and payload production line.

The facilities in China will provide the necessary linkers and payloads for the operations of the Singapore base, and the global dual-site strategy will help WuXi XDC better serve global customers.

Furthermore, in terms of the number of projects, WuXi XDC currently ranks first globally in ADC and other bioconjugate drug projects, with a portfolio more than twice the size of that held by the second-ranked company. According to earlier disclosures by WuXi XDC:The company has completed over 100 projects, gaining exposure to all major platforms and technologies within the industry. This extensive technical accumulation is now reaching a tipping point, enabling us to meet any future client project requirements.

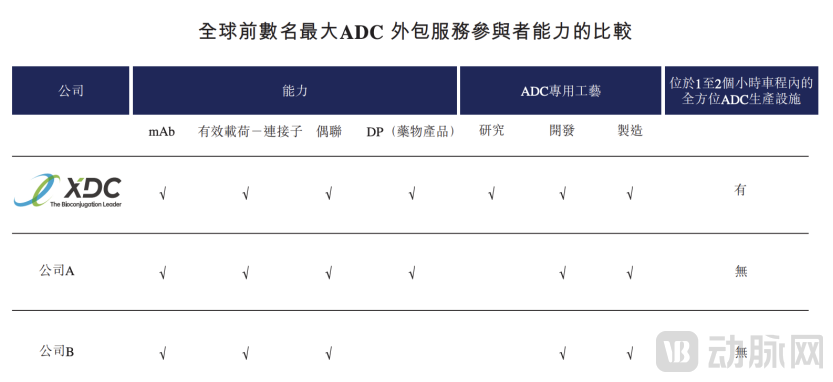

What WuXi XDC takes the most pride in is its comprehensive capabilities,The company claims to be the only one offering comprehensive capabilities across the entire discovery, development, and manufacturing process of ADCs.

Excerpt from the prospectus of WuXi XDC. According to the information in the prospectus, Company A is Lonza, and Company B is Sigma-Aldrich.

Even Lonza lags behind WuXi XDC in the research phase. As previously mentioned, WuXi XDC’s 350 discovery projects represent the robust “R” component of its CRDMO model, which will continue to drive the company’s growth. The players ranking third to fifth in market share are small and medium-sized European CRDMOs, including Sigma-Aldrich (a subsidiary of Germany’s Merck), whose service offerings and corporate capabilities are less comprehensive than those of WuXi XDC.

With rising production capacity, customer growth, and further business expansion, WuXi XDC—bolstered by core competitive advantages such as cross-disciplinary expertise, integrated supply chain manufacturing, and the “engineer dividend”—may have the potential to strive for the position of “global number one.”