26 Biopharma Companies Collapsed in Clinical Stages in 2023: Internal Failures, Not Capital Winter, Were to Blame

Reata Pharmaceuticals

Biopharmaceutical Company

Novavax

Innovative Vaccine Developer

Throughout the history of business development, bankruptcy and closure have been the fate of the vast majority of startups. However, it is unusual for listed companies, unicorns, and star companies that have secured multiple rounds of substantial financing to announce bankruptcy in quick succession.

According to statistics from foreign media outlet Fierce Biotech, as of October 30, 22 biotechnology companies have either shut down or announced plans to do so this year.three times that of last yearMoreover, in November alone, another biopharmaceutical company announced its closure, and more biopharmaceutical firms may yet be added to this year’s “death list” in the coming two months.

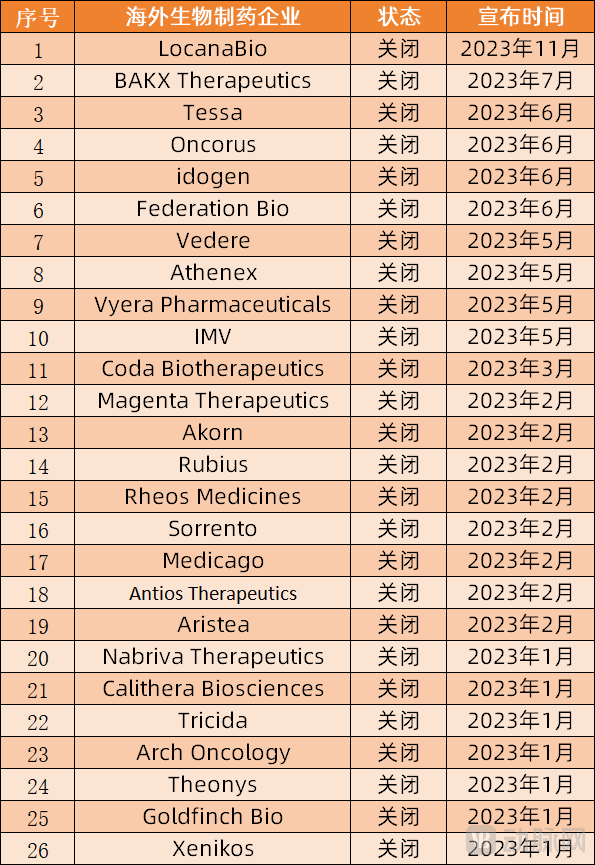

(Partial List of Biopharmaceutical Companies Announcing Closure in 2023, Based on Public Reports)

In fact, the biopharmaceutical sector has been sending strong signals of pessimism since the beginning of the year. In January, seven biopharmaceutical companies announced their closures in quick succession, dousing investors and entrepreneurs who had just stepped into the new year with cold water and casting a shadow over the industry. The situation showed no signs of improvement in February; indeed, it worsened, with nine biopharmaceutical companies announcing either closure or bankruptcy liquidation one after another.

In their shutdown announcements, most companies attributed the closures to “the current challenging financing environment, which makes it difficult to secure the time and capital necessary to sustain corporate development.” However, a deeper investigation reveals that the reasons are not so simple.

Although the global capital market has entered a winter period, making fundraising more difficult for biopharmaceutical companies than in previous years, the deteriorating financing environment is not the primary reason for these companies' failures. Financing issues likely account for less than 10% of all factors contributing to such closures. A detailed analysis reveals that the vast majority of these defunct biopharmaceutical companies shut down due to internal factors.

First, clinical trial failures were the primary factor driving these companies to declare bankruptcy.Among the more than 30 companies surveyed, approximately 50% opted for bankruptcy liquidation due to the failure of clinical trials for their core pipelines.

For example, biopharmaceutical company Tricida announced in October 2022 that its core pipeline candidate, veverimer, failed to meet the primary endpoint in its Phase III clinical trial, and subsequently filed for bankruptcy liquidation in January 2023. Dutch biotechnology firm Xenikos announced in January 2023 that its Phase III clinical trial of an antibody combination therapy with Incyte’s JAK inhibitor Jakafi was terminated due to reaching the prespecified 60-day mortality stopping boundary, and the company planned to shut down operations.

Additionally,Many biopharmaceutical companies that once attracted significant attention from the capital market have also shut down due to clinical trial failures.Aristea, which had secured over $100 million in investments from renowned companies such as Novo Nordisk and Pfizer, announced in February 2023 that it had halted the development of RIST4721 due to safety findings from ongoing Phase II clinical trials. With the termination of this project, Aristea also rapidly ceased operations.

Second, slow project progress and difficulties in corporate financing are another contributing factor.For example, Rubius Therapeutics, the pioneer of red blood cell therapy (RCT) founded in 2013, has now initiated liquidation and dissolution proceedings. Previously, Rubius had raised over $700 million in financing within seven years. From 2013 to 2017, Rubius was almost entirely focused on building its RCT platform. It was not until 2018, when Rubius completed its Series C financing, that the funds were designated to accelerate the development of its first wave of RCT products.

(Rubius' Financing History)

Leveraging its RCT technology platform, Rubius pioneered the development of PTX-134, primarily targeting phenylketonuria. However, RTX-134 failed in Phase I clinical trials for phenylketonuria. Subsequently, Rubius announced the discontinuation of clinical trials of its red blood cell therapies for phenylketonuria and other rare diseases, shifting its focus to oncology and autoimmune diseases.

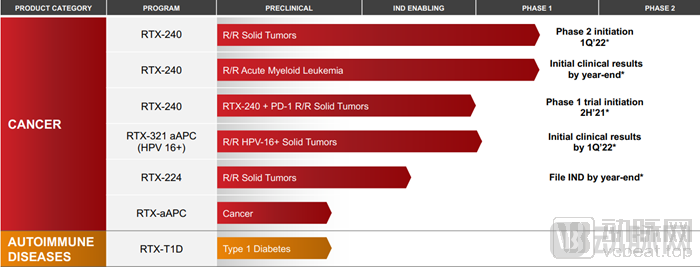

In the field of oncology, Rubius Therapeutics developed a pipeline targeting solid tumors, including RTX-224 and RTX-240, advancing them to Phase I clinical trials. However, in 2022, Rubius decided to discontinue these two programs, which were already in clinical development, concluding that neither therapy offered sufficient prospects for further investment. Shortly after streamlining its R&D pipeline, Rubius decided to seek a sale or merger.

(Rubius’s Previously Developed Pipeline and Progress)

In stark contrast to the fate of Rubius, emerging players in red blood cell-based therapies, such as Anokion, have progressed smoothly. It is reported that in May 2022, Anokion announced positive Phase I clinical data for its lead candidate, KAN-101, for the treatment of celiac disease. Subsequently, in October 2022, Anokion secured a $35 million equity investment from Pfizer. Meanwhile, Anokion reached an agreement with Pfizer to leverage the latter’s development expertise and capabilities to support the ongoing clinical development of KAN-101.

The stark contrast in fortunes between the pioneer of red blood cell therapy and its emerging rivals is enough to make one marvel at the capriciousness of fate. It should be noted that Rubius’s closure was not caused by a single factor, but rather by a combination of pipeline failures, slow progress, and insufficient funding.

In addition to the aforementioned reasons, factors such as commercialization challenges, litigation, regulatory oversight by drug administration authorities, and disagreements among investors have also forced some companies to shut down.。

Among them, Goldfinch Bio’s core product, GFB-887, has advanced to Phase II clinical trials; however,Due to commercialization issues, the company suspended clinical trials of the product and declared bankruptcy in early January this year. Additionally, the Canadian company Medicago launched Covifenz, a plant-derived recombinant COVID-19 vaccine, but also shut down due to commercialization challenges.

Vyera Pharmaceuticals, meanwhile, faced legal litigation.In January 2020, the U.S. Federal Trade Commission filed a lawsuit against Vyera, alleging that it engaged in price gouging (with an overnight price increase of 55-fold) to maintain its monopoly on Daraprim, a medication for toxoplasmosis. In December 2021, the lawsuit was settled, with the settlement agreement requiring Vyera to provide $40 million in consumer relief over ten years and to supply Daraprim to generic competitors at cost. In May 2023, Vyera filed for bankruptcy, attributing the move to declining profits, competition from generic drugs, and ongoing litigation related to Daraprim.

Regulatory oversight by drug administration authorities has also driven some companies into bankruptcy., such as Antios Therapeutics and Athenex. Taking Athenex as an example, although its core product, oral paclitaxel, completed Phase III clinical trials, the FDA issued a complete response letter rejecting its approval. The FDA determined that oral paclitaxel posed greater safety risks to patients compared with intravenous paclitaxel and expressed concerns about the uncertainty of its efficacy. Subsequently, Athenex shifted its focus to cell therapy; however, in March 2022, the FDA urgently placed a clinical hold on its neuroblastoma cell therapy following a patient death during Phase I clinical trials. The company subsequently declared bankruptcy in May 2023.

There are also enterprises that have shut down due to disagreements among investors., such as the tRNA drug development company Theonys. Professor Peter Dedon, co-founder of the company, stated, “As a scientific founder, I am deeply disheartened by the situation at Theonys. The science and technology underpinning Theonys are robust, and the founders along with the majority of its team members are pioneers in the field of tRNA epitranscriptomics. Therefore, the company’s closure due to investor missteps is, to say the least, regrettable.”

Overall, the collapse of these biopharmaceutical companies is largely attributable to internal factors; the capital winter and the current financing environment should not be blamed for their failures. Only by confronting these internal issues and avoiding such pitfalls can entrepreneurs achieve greater long-term success.

Faced with a bankruptcy crisis, corporate decision-makers will naturally attempt various self-rescue measures.

Some companies pin their hopes on layoffs and selling off assets. For instance, after encountering a crisis, Athenex swiftly initiated layoffs and sequentially sold its manufacturing plant in Dunkirk and its API (Active Pharmaceutical Ingredient) facility in China. Ultimately, however, Athenex still exited the market through bankruptcy.

Rubius, the pioneer of red blood cell therapies that secured $700 million in financing over seven years, attempted to save itself through multiple rounds of layoffs and pipeline reductions after setbacks in its core programs, but these efforts proved futile. Just two months after announcing a strategic pivot to develop a next-generation red blood cell platform, the company hastily announced it was seeking a sale or merger.

Although most of these companies in crisis have shut down, a small number have merged with other firms to pool resources and extend their cash runway.For example, Adaptimmune, a company in the TCR-T field, finally merged strategically with TCR² Therapeutics after cutting its product pipeline and laying off employees, extending its cash runway to more than three years; Aileron, after acquiring Lung Therapeutics, will have sufficient private placement proceeds and post-acquisition cash to meet its operating and capital expenditure needs through the fourth quarter of 2024.

In addition, as a large number of listed companies collapsed, some biopharmaceutical firms seized the opportunity to go public through reverse mergers.For example, Angion Biomedica completed its merger with Elicio in January 2023 following a series of clinical trial failures. The combined company operates under the name Elicio, with its stock ticker symbol changing from “ANGN” to “ELTX.” Magenta completed its merger with Dianthus in September 2023 after suspending clinical studies; the merged entity operates under the name Dianthus and is traded on the Nasdaq under the ticker symbol “DNTH.”

Similarly, Cyclo Therapeutics went public on the Nasdaq under the ticker symbol “CYTH” through a reverse merger with ATM; DMK Pharmaceuticals began trading on the Nasdaq Capital Market under the ticker symbol “DMK” by acquiring Adamis’s shell company; and Tourmaline started trading on the Nasdaq under the ticker symbol “TRML” by merging with Talaris’s shell company.

For biopharmaceutical companies with strong clinical data but insufficient funding, the market typically facilitates a dignified exit through acquisitions or mergers and acquisitions (M&A), allowing their pipelines to be further advanced.For example, Surface Oncology, a company specializing in immunotherapy, announced positive clinical results for its antibody SRF388 as a monotherapy in patients with non-small cell lung cancer (NSCLC) in November 2022, prior to its acquisition. Based on these positive results, Surface initiated a Phase II clinical trial evaluating the combination of SRF388 with the anti-PD-1 antibody Keytruda.

In April 2023, Surface announced new preclinical data for SRF114. The results demonstrated that combination therapy with anti-CCR8 and anti-PD-1 antibodies increased tumor immune cell infiltration and cytokine production, and improved overall survival in checkpoint inhibitor-resistant melanoma models.

Perhaps based on the clinical data disclosed by Surface, Coherus acquired Surface for $65 million in June 2023. Following the acquisition, Coherus added four assets at different clinical stages to its portfolio: Toripalimab, Casdozokitug (SRF388), CHS-114 (SRF114), and CHS-006.

For another example, Apexigen, a tumor immunotherapy company that announced a strategic restructuring in February 2023, was acquired by Pyxis Oncology for $16 million in May 2023, thereby gaining access to its antibody discovery platform. Prior to the acquisition, Pyxis Oncology had high expectations for Apexigen’s core pipeline asset, sotigalimab. Lara S. Sullivan, President and Chief Executive Officer of Pyxis Oncology, stated, “Today marks an important milestone for the company as we add sotigalimab, a potential best-in-class CD40 agonist with anticancer activity in patients previously treated with PD-(L)1 inhibitors, which also enhances our ADC capabilities.”

Apexigen also lived up to expectations. Just one month later, Apexigen announced new data evaluating sotigalimab in combination with doxorubicin for the treatment of patients with advanced soft tissue sarcoma. The data showed that sotigalimab combined with doxorubicin was safe and well tolerated, and significantly improved overall survival in patients. Among all evaluated patients with advanced soft tissue sarcoma, the median overall survival was 35.6 months, which is higher than the 12.8–20 months observed with doxorubicin monotherapy.

As can be seen, the market continues to support companies with robust clinical data in advancing their projects through various means. In contrast, companies whose core pipelines suffer clinical trial failures often face bankruptcy and closure. However, among these bankrupt entities, some publicly listed companies will sell off their only remaining asset of value—their public listing status.

Overall, most biopharmaceutical companies that have gone bankrupt may truly deserve their fate.

Since the beginning of this year, approximately 30 biopharmaceutical companies worldwide have announced their closure. Amid this wave of bankruptcies, survival has become a critical consideration for all biopharmaceutical firms.

Perhaps companies that have achieved self-rescue from dire straits can offer us some insights.

Among biopharmaceutical companies that have gone bankrupt, clinical trial failures of core pipelines are the primary factor. Reata Pharmaceuticals, founded in 2002, also experienced a Phase III clinical trial failure, but it was later acquired by Biogen at a 59% premium for $7.3 billion.

It is reported that Reata previously developed bardoxolone, a novel small-molecule Nrf2 activator, for the treatment of chronic kidney disease (CKD) caused by Alport syndrome. Given the promising prospects of bardoxolone, Abbott acquired the rights to market the drug outside the United States in 2010 for $450 million. Unfortunately, after completing Phase III clinical trials and submitting its marketing application, the drug was rejected by the U.S. Food and Drug Administration (FDA) on the grounds that the clinical data failed to demonstrate efficacy. In May 2023, Reata ultimately announced the discontinuation of its bardoxolone pipeline.

Meanwhile, Omaveloxolone (brand name: Skyclarys), another drug developed by Reata based on an Nrf2 agonist, finally received FDA approval this year as a “First in class” therapy after nine years of development, for the treatment of Friedreich’s ataxia (a rare disease).

Currently, Omaveloxolone has no competitors in the market. Perhaps for this reason, Biogen announced on July 25 that it would acquire Reata Pharmaceuticals at a 59% premium for $7.3 billion to strengthen its neurology and rare disease business.

Notably, Nrf2 agonists can improve mitochondrial function in cells, making them potentially suitable for treating neurological disorders such as Alzheimer’s disease. The approval of omaveloxolone, an Nrf2 agonist-based drug launched by Reata Pharmaceuticals, has demonstrated the company’s capabilities, and more Nrf2 agonist-based drugs are likely to be developed in the future.

Vaccine developer Novavax is another representative case. After 34 years in operation, it still has no approved products on the market, and its RSV F vaccine targeting respiratory syncytial virus in older adults failed to meet the primary endpoint in Phase III clinical trials, ending in failure.

Subsequently, Novavax’s other vaccine candidate, ResVax, also failed to meet its primary clinical endpoints in Phase III trials. At that point, Novavax was insolvent and on the brink of bankruptcy.

However, the turning point came in 2020. With the outbreak of the COVID-19 pandemic and Novavax’s accumulated expertise in vaccine technology, the company rapidly secured funding from multiple sources and developed a COVID-19 vaccine. According to reports, the vaccine demonstrated an overall efficacy of 90.4% against SARS-CoV-2 infection and 100% efficacy against severe disease. Meanwhile, its recombinant protein-based vaccine offered advantages in storage and transportation compared to mRNA vaccines. Against this backdrop, Novavax rose from the brink of bankruptcy to become a company with a market capitalization of $26 billion in 2021.

In August 2023, Novavax’s financial report revealed that its second-quarter revenue reached $424 million, exceeding analysts’ expectations of $240 million. In October, Novavax announced that its adjuvanted COVID-19 vaccine (NVX-CoV2601) had received Emergency Use Authorization from the U.S. Food and Drug Administration (FDA) for active immunization to prevent COVID-19 in individuals aged 12 years and older. The vaccine also received a recommendation from the U.S. Centers for Disease Control and Prevention (CDC).

Looking at the case of Novavax, possessing technology alone can still lead to bankruptcy. For instance, Theonys, whose founders and most team members were pioneers in the field of tRNA epitranscriptomics and boasted strong technical capabilities, ultimately ceased operations. Therefore, the selection of application scenarios and products is commercially critical. Targeting appropriate scenarios and developing corresponding new products based on a robust technology platform can yield twice the results with half the effort.

As for the oft-repeated clichés about cost-cutting and efficiency improvement, this article will not dwell on them. We trust that founders of biopharmaceutical companies will possess more acute perception, deeper insight, and more scientific decision-making capabilities.