Aesthetic Giants Heavily Invest in Photonic Beauty: Who's Quietly Taking the Lead?

IMEIK

Developer of Biomedical Soft Tissue Repair Materials

Jeisys Medical

Medical Device R&D and Manufacturer

Recently, domestic medical aesthetics giants have once again become “restless.”

November 8,ImeikWith the leading laser medical device company in South Korea’s photonics market shareJeisysSigned a distribution agreement to become the exclusive distributor in mainland China for two of Jeisys’ photoelectric anti-aging devices, covering promotion, distribution, sales, and related services.

However, this is not an isolated case; prior to this, includingHaohai Biological, Huadong MedicineMajor medical aesthetics giants, among others, have also entered the fray to bet on manufacturers of energy-based medical aesthetics devices. It can be said that a frenzied phase of acquisitions by these industry leaders targeting such device manufacturers is now underway.

But the buzz in the photoelectric medical aesthetics sector doesn’t end there. Recently, the official website of the Beijing Stock Exchange showed that a comprehensive supplier of photoelectric medical aesthetic devicesChiqi Laserits IPO application has been accepted, marking the formal commencement of its listing efforts. In the primary market,Weimai MedicalandThemis MedicalTwo startups in the field of optoelectronic medical aesthetics have also successfully completed financing recently, with their investors being no less than prominent figures: Botanee Group, a domestic beauty giant, and Shenzhen Capital Group, the "ceiling" of state-owned capital.

In fact, this scene is all too familiar in the medical aesthetics industry. The botulinum toxin and collagen sectors, which have now successfully emerged as leading markets, similarly experienced their moment in the spotlight a few years ago when they were propelled to the forefront of the industry by giants and capital. Does this mean that a new high-potential sector is quietly brewing within the field of medical aesthetics? And amidst this, who has already started to “jump the gun”?

What Is the Motive Behind Medical Aesthetics Giants Entering the Fray?

Amid the market’s winter chill, any move within the industry often carries multifaceted implications; this holds true for the collective bet by medical aesthetics giants on photoelectric medical aesthetic devices.

Starting with the global market,The trend of mergers and acquisitions in the upstream medical aesthetics industry persists, as evidenced by large-scale companies continuously integrating distinctive medical aesthetic products.。

In this regard, Dr. Wang Xinliang, Partner at Mingfeng Capital, explained the underlying logic to VCBeat, stating, “Medical aesthetic devices often target one or a few indications, making them well-suited for integration. AndFor upstream manufacturers in the medical aesthetics industry, integration can enrich their product pipelines, enhance overall business synergy, and create a more comprehensive portfolio of offerings, thereby increasing business scale.。”

From the perspective of the current overall trends in the medical aesthetics industry, and further focusing on the domestic market, what special factors lie behind the collective entry of major medical aesthetics players?

First and foremost, it is based on the pursuit of new business growth drivers.However, this issue must be viewed from two perspectives. On one hand, as the hyaluronic acid sector has become increasingly crowded in recent years, prices have been declining year by year across the entire value chain, from raw materials to end products. This has led to business bottlenecks for many upstream manufacturers in the medical aesthetics industry. Taking Bloomage Biotech as an example, its net profit in the first half of this year amounted to RMB 425 million, representing a year-on-year decline of 10.27%. This marks the first time since its listing in 2019 that Bloomage Biotech has experienced a decline in net profit.

Therefore, upstream medical aesthetics manufacturers have been eager to expand into new business segments in recent years. Among these options, energy-based device (EBD) treatments, which boast significant market potential and are still in an early stage of development, clearly represent a promising choice.

On the other hand, it is based on the exploration of the lower-tier medical aesthetics market.. It is reported that the current approximately 20 million consumers of medical aesthetics in China are mainly concentrated in super-first-tier and first-tier cities, where the penetration rate is already relatively high at this stage, making significant large-scale growth difficult in the future.The true future growth in the medical aesthetics market will come from lower-tier markets., and on this basis, compared with surgical and injectable procedures that demand high technical expertise from physicians, energy-based medical aesthetic treatments are more equipment-dependent and easier to standardize, thus carrying lower risks. Coupled with their advantages of low unit price and high repurchase rate, they readily drive the penetration of medical aesthetic services into lower-tier markets.

In addition to the demand for business growth,Another critical factor is the proactive adjustments made by upstream manufacturers in response to changes in the broader industry landscape.. Of course, this must also be viewed from two perspectives.

From the perspective of the medical device industry's development trajectory, import substitution for aesthetic medicine equipment has reached a critical juncture.In this regard, Dr. Wang Xinliang, Partner at Mingfeng Capital, shared his deep insights, stating, “Drawing on the development trajectories of domestically produced ultrasound, CT, and MRI systems, the medical aesthetics equipment industry has already undergone market cultivation by importers. Domestic manufacturers are now following suit, engaging in imitation and technological catch-up.”"At present, there is a certain level of innovation capability."

This is indeed the case. It is reported that in recent years, although the overall market share of imported manufacturers in China's compliant medical aesthetics equipment market has declined slightly,but still as high as over 80%, especially in the segment of high-end equipment, where the proportion is even higher. Therefore, domestic substitution has become an urgent priority in China.

On the other hand, from the perspective of treatment methods,The combination of pharmaceuticals and medical devices has become an inevitable trend in the field of medical aesthetics.In this regard, a company executive specializing in the medical aesthetics sector told VCBeat, “In the field of non-surgical medical aesthetics, combination therapy has become the most commonly used approach. Specifically, in consumer-facing scenarios, physicians generally recommend that patients undergo injectable filler treatments first, followed by energy-based device procedures approximately one month later. This strategy not only meets customers’ segmented and personalized needs but also enables post-treatment outcomes to achieve a synergistic effect greater than the sum of its parts (1+1>2). Therefore, these two modalities are not substitutes but rather complementary approaches that jointly enhance clinical acceptance.”

In retrospect, the collective entry of leading medical aesthetics companies into the energy-based device sector is driven both by their internal imperative to diversify product pipelines and seek new growth engines, and by broader industry trends: the inflection point in the domestic substitution of medical aesthetic devices in China, and a fundamental transformation in overall diagnostic and treatment modalities.

Half Seawater, Half Flame: How to Seek Balance?

In the field of photoelectric medical aesthetics, it is not only the industry giants that are making significant moves; investors are also stepping up to the plate.

According to incomplete statistics from the VCBeat database,From 2021 to the present, more than 30 companies in the upstream supply chain of the photoelectric medical aesthetics industry, including Fumilei, Nanjing Baifu, Yaguang Medical, and Weimai Medical, have successively secured financing, raising a total of over RMB 2.5 billion. Multiple leading investment firms, such as Shenzhen Capital Group, Northern Light Venture Capital, YuanSheng Capital, Yuanyi Capital, Shenzhen High-Tech Investment Group, and Mingfeng Capital, have all made investments in this sector.。

Figure 1. Representative companies in the photoelectric medical aesthetics sector (Source: VCBeat)

Figure 1. Representative companies in the photoelectric medical aesthetics sector (Source: VCBeat)

Among this batch of startups,FumileiandWeimai MedicalAttracting significant attention from the capital market, with a relatively rapid development pace.FumileiTake, for example, a company established in 2021 that has completed three rounds of financing over the past two years. Reportedly, it specializes in the field of high-end medical aesthetic optoelectronic devices and currently possesses a portfolio of core products. Among these, its ForeShine mesotherapy device received official approval in February this year and has successfully commenced commercialization. Its picosecond laser treatment system has completed registration testing, with measured performance parameters fully comparable to those of imported counterparts, and is poised to initiate clinical trials. Additionally, its cold air therapy device is expected to receive approval and launch on the market in the near future.

Another representative company isWeimai Medical, which was also founded in 2021, has rapidly completed six rounds of financing to date. As a medical device company centered on energy-based ablation therapy systems and providing comprehensive minimally invasive and non-invasive energy medicine solutions, its currently self-developed product portfolio includes high-end medical devices such as peripheral interventional radiofrequency ablation systems and aesthetic radiofrequency treatment devices.

So, back to the beginning: why has the photoelectric medical aesthetics sector started to attract widespread attention from the capital market in the past one to two years?

The answer is undoubtedly multi-dimensional, such as the aforementioned exploration of the lower-tier medical aesthetics market, the rise of industry innovation, and the inflection point in the domestic substitution of medical aesthetic devices. In addition,Another key factor is the shift in demand for aesthetic medicine driven by the rising proportion of mature consumers.。

In this regard, Dr. Wang Xinliang, Partner at Mingfeng Capital, told VCBeat, “As both of China’s two population peaks have now surpassed the age of 30,China’s mainstream medical aesthetics consumer base has gradually shifted from the 20–25 age group to the “young mature” and “early aging” demographics, with increasingly clear demand for anti-aging treatments., while various medical aesthetic light- and energy-based treatments are precisely one of the means capable of meeting their needs.”

User data further corroborates this market trend. According to the “2022 Report on Consumption Trends in the Energy-Based Aesthetic Medicine Industry” released by SoYoung Data Yanjiuyuan, the share of transaction volume on non-surgical aesthetic medicine platforms in China rose from 49.2% in 2021 to 84% in 2022. Among these, “energy-based aesthetic procedures” accounted for the highest proportion of gross merchandise value (GMV) at 43.63%, making them the most revenue-generating segment in non-surgical aesthetic medicine. Furthermore, among the aesthetic treatments most favored or most desired by consumers in 2022, 47.34% of surveyed users selected energy-based procedures. This preference is attributed to their relatively affordable pricing, lower barriers to access, reduced risks, and inherent inclusivity.

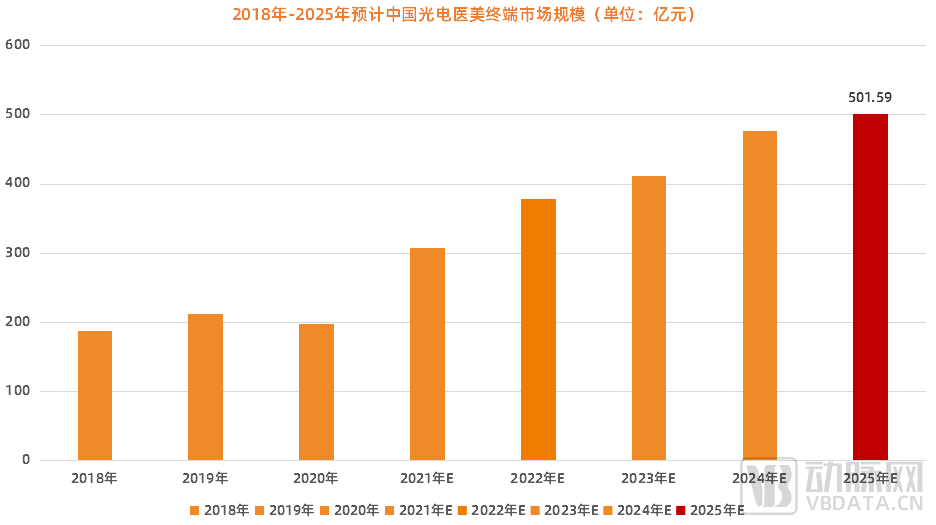

Figure 2. Projected Market Size of China’s Photoelectric Medical Aesthetics End-Market, 2018–2025 (Data Source: LeadLeo Research Institute, Shengang Securities Research Institute)

It is precisely for this reason that the market size of photoelectric medical aesthetics has grown rapidly in recent years. According to data from LeadLeo Research Institute,The market size of photoelectric medical aesthetics is projected to reach RMB 50.159 billion in 2025, with a CAGR of 13.43% from 2021 to 2025, making it the fastest-growing segment within the medical aesthetics industry.

However, everything has two sides; while photoelectric medical aesthetics continue to explore market potential, they are currently facing some limitations.

For instance, significant obstacles remain in terms of regulatory compliance at the current stage,The prevalence of unlicensed products has led to a mixed bag of domestically manufactured medical devices.. According to industry insiders,Currently, many companies have no plan to obtain regulatory approval after developing their products, but instead quickly launch them on the market.

Of course, this is merely one aspect of the industry’s chaotic practices, stemming from inadequate regulatory oversight.False advertising is also common in the field of photoelectric medical aesthetics., primarily manifested in issues such as exaggerating efficacy to consumers and making guaranteed promises regarding treatment outcomes. According to monitoring data from the Beijing Sunshine Consumer Big Data Research Institute, a total of 90,769 public opinion entries related to consumer rights protection in medical aesthetics were monitored from January to May 2023, mainly involving three categories: marketing and promotion, medical qualifications, and medical quality.

Another major pain point lies in innovation.Domestic medical aesthetic devices are still predominantly based on imitation, lacking original innovation, and may rapidly fall into price competition in the future.。

Currently, domestic medical aesthetic devices are predominantly imported brands. Particularly in the high-end segment, Chinese companies started later and face a shortage of core talent, resulting in significantly insufficient original innovation capacity in the field of photoelectric medical aesthetics. Consequently, domestically produced devices are mostly concentrated in the mid-to-low-end market. Over time, this has led to low technological value-added and increasingly severe product homogenization, heralding the imminent arrival of an era characterized by cutthroat price competition.

Finally, these challenges are reflected in the technical dimension. Due to the high energy density of photoelectric energy-based devices, they can easily cause damage to the epidermis, leading to side effects such as hyperpigmentation, erythema, bruising, and crusting. This is particularly true for sensitive skin, which is more susceptible to external light exposure and thermal stimulation; patients may experience immediate redness, swelling, or burning sensations, with a higher likelihood of subsequent impairment of the skin barrier. Furthermore, as the visualization systems for energy-based devices remain immature, truly personalized treatment has yet to be achieved. Variations in individual skin types can easily lead to adverse effects from improper operation, such as subcutaneous scarring and nerve injury, often necessitating post-procedural repair treatments for some patients.

Therefore, from the current perspective, beneath the enormous market potential of photoelectric medical aesthetics lie certain hidden risks.

How to Break Through: Pursuing Differentiated Innovation

According to Dr. Wang Xinliang, Partner at Mingfeng Capital, there are currently two logics for investing in photoelectric medical aesthetics,One approach is to invest in foundational product categories., including intense pulsed light (IPL) and laser-based devices, with a primary focus on domestic substitution and penetration into lower-tier markets; whereasThe other is to invest in differentiated and specialized product categories., such as anti-aging products driven by the current shifts in consumer demographics, or focusing on entirely new application scenarios, such as the use of plasma energy sources to improve hyperpigmentation in certain body areas.

Along these two investment logics, the profile of companies poised to break through in the optoelectronic medical aesthetics sector is gradually becoming clear.

First, it is essential to fully understand market demand and the logic of industry development, prioritizing major niche segments with clear growth potential for focused development.. For instance, following the logic of import substitution, corresponding products must be both high-quality and affordable, which necessitates rigorous control over production costs; alternatively, adhering to the logic of differentiation through specialized projects, the primary step is to accurately identify user needs, maintain firm confidence, demonstrate product value through clinical evidence, and ensure comprehensive regulatory compliance.

Second, establish differentiated positioning and continuously strengthen product competitiveness.Ultimately, the market must return to focusing on product efficacy, especially in the field of medical aesthetics. Users’ pursuit of better outcomes is becoming increasingly strong, and in this regard, the effective integration of intelligence with treatment scenarios may serve as a breakthrough.

In this regard,Dr. Wang Xinliang, Partner at Mingfeng Capital, distilled three dimensions:The first is more precise intelligent feedback., enabling rapid measurement and control of immediate therapeutic effects or patient-perceived sensations, such as more precise temperature control to achieve an optimal balance between experience and efficacy;The second is to intelligently set device parameters by leveraging user big data., and facilitate the development of a treatment plan;The third aspect involves integrating multidimensional information to intelligently design and implement treatment plans, thereby achieving automation and eliminating manual labor.。

However, there have been no significant developments in this field to date, with most stakeholders adopting a wait-and-see approach. The challenges lie in the substantial capital investment required and the need to overcome certain technical hurdles. Nevertheless, the immense application potential of artificial intelligence in the field of photoelectric medical aesthetics is undeniable.

Finally, ensure effective market promotion to convey the right message to consumers.. To many, a major pain point of photoelectric medical aesthetics is its overly simplistic commercialization model; coupled with industry chaos stemming from inadequate regulation, this significantly hinders market promotion.

However, this is not without solutions. On one hand, companies should strengthen academic promotion targeting physicians; on the other, they should convey more accurate and objective information about their products to consumers. For instance, Dr. Wang Xinliang has noted that due to ethnic limitations, individuals with yellow skin tones are not suitable for high-energy, high-frequency photoelectric stimulation. Yet, during the sales process, unrealistic expectations may be created for consumers, and if physicians fail to exercise restraint, adverse effects may result. Therefore, enterprises should provide proper guidance to consumers and avoid excessive marketing.

In April this year, the Center for Medical Device Evaluation of the National Medical Products Administration required that radiofrequency treatment devices (including those for home use) be uniformly regulated as Class III medical devices. Starting from April 1 next year, such products that have not legally obtained a medical device registration certificate shall not be manufactured, imported, or sold, undoubtedly raising the market entry threshold once again. From the perspective of development trends,Amidst tightening regulations and stricter policies, the medical aesthetics industry will gradually align more closely with serious medical practice, and the entire patient care process will become increasingly standardized.。

High technical and regulatory barriers will also make optoelectronic products increasingly scarce, but this also means that,Companies that have established an early presence and secured first-mover advantages can leverage superior products and brands to build stable customer relationships and rapidly capture market share, thereby possessing greater potential to stand out in the future.。

1. “Aesthetic Medicine Giants Enter the ‘Photoelectric Beauty’ Arena” – Jianzhi Research Pro;

2. “VCs Enter the Fray, Photoelectric Aesthetic Medicine Takes Center Stage” – Lieyunwang;

3. “The Strong Rise of Photoelectric Medical Aesthetics: Two Major Trends Emerge” — VCBeat.