Empowering and Revitalizing Traditional Pathology Testing: Digital-Intelligent Pathology Drives Industry Takeoff with Business Doubling

The pathology industry is currently at a historical window of development.

On one hand, digital intelligent pathology helps address industry pain points; on the other hand, it brings new momentum to the traditional pathology testing market. Meanwhile, the development of personalized medicine is driving the advent of the next generation of pathology.

At the current stage, domestic digital pathology products have largely achieved import substitution, capturing over 70% of the market share; the pathology informatics market remains fragmented but is witnessing rapid enterprise growth; the first Class III medical device registration for pathology AI has been approved, with pathology AI software for cervical cytology widely deployed across China, while AI solutions for other pathological conditions are gradually maturing… Meanwhile, the active integration of digital smart pathology with conventional pathological testing is progressively shaping a new industrial ecosystem.

At this juncture, what remaining breakthroughs are needed in digital pathology? Has intelligent pathology entered the deep waters of commercialization, and what potential application scenarios remain to be explored? What synergies will emerge from the convergence of the AI-driven digital pathology market and the traditional pathological testing market? As the next generation of pathology arrives, which emerging technologies warrant close attention? What opportunities remain untapped within the industry, and what is the future trajectory of the sector?

Following the previous release"White Paper on China's Smart Pathology Industry"“White Paper on the Construction of Digital Smart Pathology Departments”Subsequently, VCBeat Institute continued to delve into the industry to seek answers to the aforementioned questions. We collaborated with more than ten pathology experts, leading entrepreneurial companies in the field, and industry investors to conduct in-depth discussions, resulting in the following content.

Core Viewpoints of the Report:

1. The competitive landscape in the field of pathology informatics is relatively fragmented, with no dominant players capturing a significant market share, leaving substantial growth potential for specialized enterprises. Digital pathology products have largely achieved domestic substitution, with some products matching or even surpassing imported counterparts in performance; Chinese-made scanners now hold over 70% of the market share. Currently available pathology AI software basically covers the major diseases screened in pathology departments. Beyond cervical cytology screening, pathology AI solutions for gastrointestinal and breast diseases are also becoming increasingly mature. In the future, the first pan-cancer pathology AI software is likely to achieve its initial breakthrough in lymph node analysis.

2. As hospitals’ enthusiasm for establishing pathology departments increases and related products become more refined and mature, their willingness to purchase has risen rapidly. From informatization and digitalization to intelligent transformation, companies’ businesses have generally doubled or achieved substantial growth.

3. The first Class III medical device certification for pathology AI has been granted, further promoting standardized market development and expanding market potential. While the Class III certification serves as a market entry barrier, product competitiveness remains paramount. Some pathology AI products have adopted per-case pricing or one-time software purchase models, but many still rely on premium-priced integrated pathology solutions to implement implicit charging. The industry’s breakthrough lies in achieving true product maturity and gaining broad clinical acceptance. In the future, integrated pathology AI platforms may emerge, with potential development paths including: pathology informatics vendors building open ecosystems compatible with pathology AI software from different brands, and collaboration and product integration among pathology AI developers.

4. The pathology testing market is undergoing domestic substitution. Although the era of digital and smart pathology has arrived, the overall level of “four modernizations” in pathology departments remains relatively low, and no industry giants have yet emerged. Through mutual cross-promotion, digital and smart pathology are actively integrating with the traditional pathology sector to create a new industrial ecosystem. Smart pathology products are revitalizing the traditional pathology testing market while empowering the rapid development of the digital pathology market. The pathology industry is experiencing unprecedented vitality and rapid growth, leaving ample room for imagination regarding its future landscape.

5. Large models are entering the field of pathology, accelerating the R&D of AI-driven pathology products, bridging knowledge gaps, and tackling critical challenges in cancer treatment. With broad application scenarios and significant growth potential, these technologies address the pathological diagnostic needs of primary healthcare institutions. Meanwhile, pathology departments in leading regional hospitals and third-party pathology diagnostic centers can leverage their concentrated resource advantages to achieve rapid development. Scan speed and image compression have become key breakthroughs in digitalization efforts, while the application scenarios for smart pathology products remain to be further expanded.

6. Precision medicine, new drug development, and digital intelligent pathology are exploring increasingly deep and broad application scenarios, demonstrating significant market potential. The current focus of oncology diagnostic pathology is shifting from targeted therapy to the study of the tumor immune microenvironment. Given the limitations of existing clinical technical methods, there is an urgent need for advanced technologies to decipher the complex interactions between tumor cells and components of the tumor immune microenvironment. Next-generation pathology (NGP) technologies, represented by multiplex fluorescence immunohistochemistry, warrant close attention. Additionally, AI-based modeling of pathological data to achieve gene-level predictions for patients represents a new direction eagerly anticipated for clinical implementation.

The Pathology Industry Is Entering an Era of Major Transformation

In the Era of Precision Medicine, the Clinical Role and Significance of Pathological Diagnosis Are Prominent, and the Industry Is Welcoming a Historic Window of Development

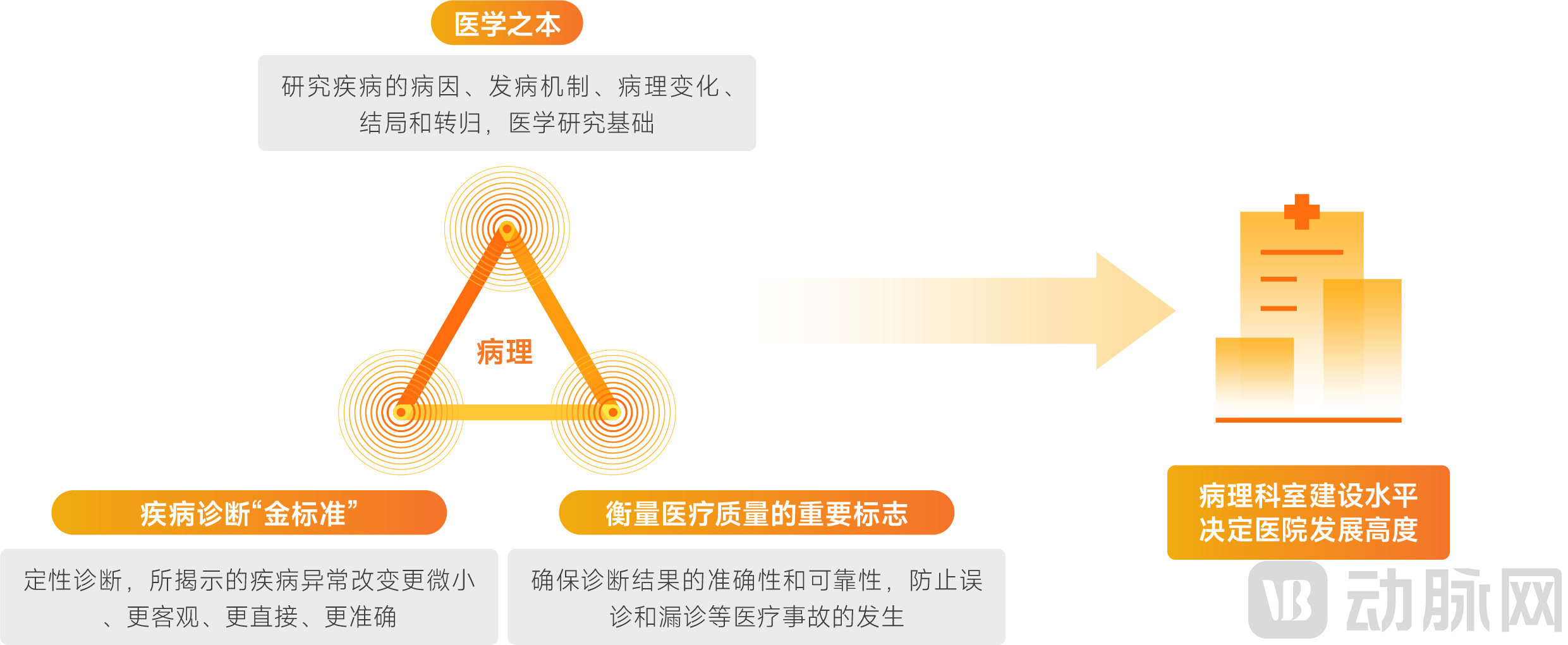

To date, pathological diagnosis remains the most reliable method for disease diagnosis and is hailed as the “gold standard.” Academician Zhong Nanshan once inscribed for the Chinese Journal of Pathology: “The level of clinical pathology is an important indicator of a nation’s healthcare quality.”

The Level of Pathology Department Development Determines the Height of Hospital Growth

Data source: Public information; chart by VCBeat

The Department of Pathology manages and controls the pathological diagnosis process to ensure the accuracy and reliability of diagnostic results, thereby preventing medical incidents such as misdiagnosis and missed diagnosis. The accuracy, reliability, and comprehensiveness of pathological diagnosis results directly impact patient treatment outcomes and satisfaction, which in turn affect the hospital’s medical quality and reputation.

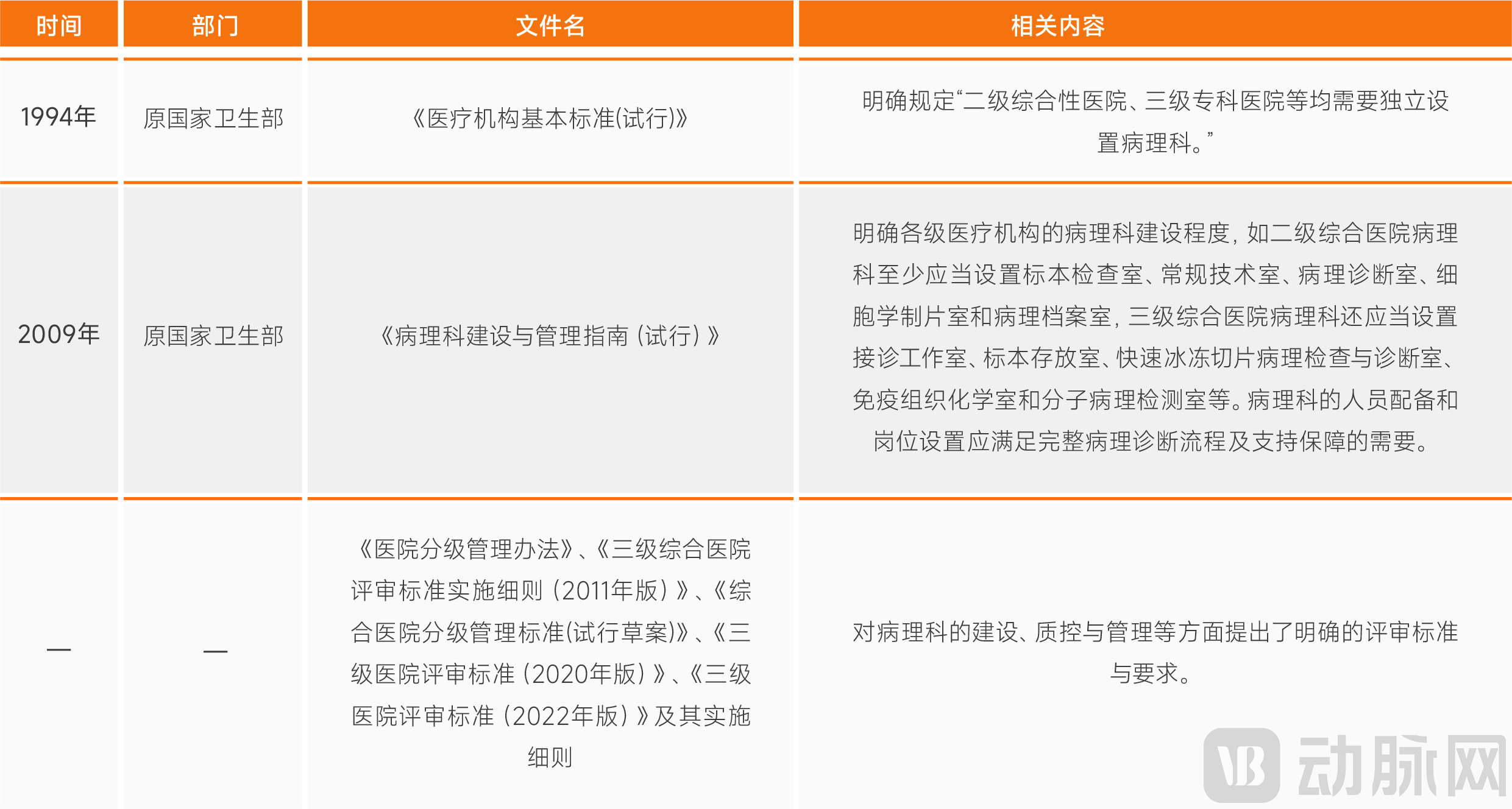

Therefore,The level of pathology department development determines the height of a hospital's growth, and the extent of its construction is also linked to the hospital's classification.

The Level of Pathology Department Development Is Linked to Hospital Classification

Data source: Public information; chart by VCBeat

In the era of precision medicine, the role and significance of pathological diagnosis in clinical practice are becoming increasingly prominent. The rapid development of multidisciplinary treatment has further highlighted the importance of pathology departments. The swift advancement of science and technology, coupled with the emergence and development of internet, cloud computing, bioinformatics analysis, big data, 5G, and AI—products of the information age—have provided a broad platform for the development of pathological diagnosis. Traditional diagnostic pathology is ushering in unprecedented historical opportunities while advancing toward next-generation diagnostic pathology.

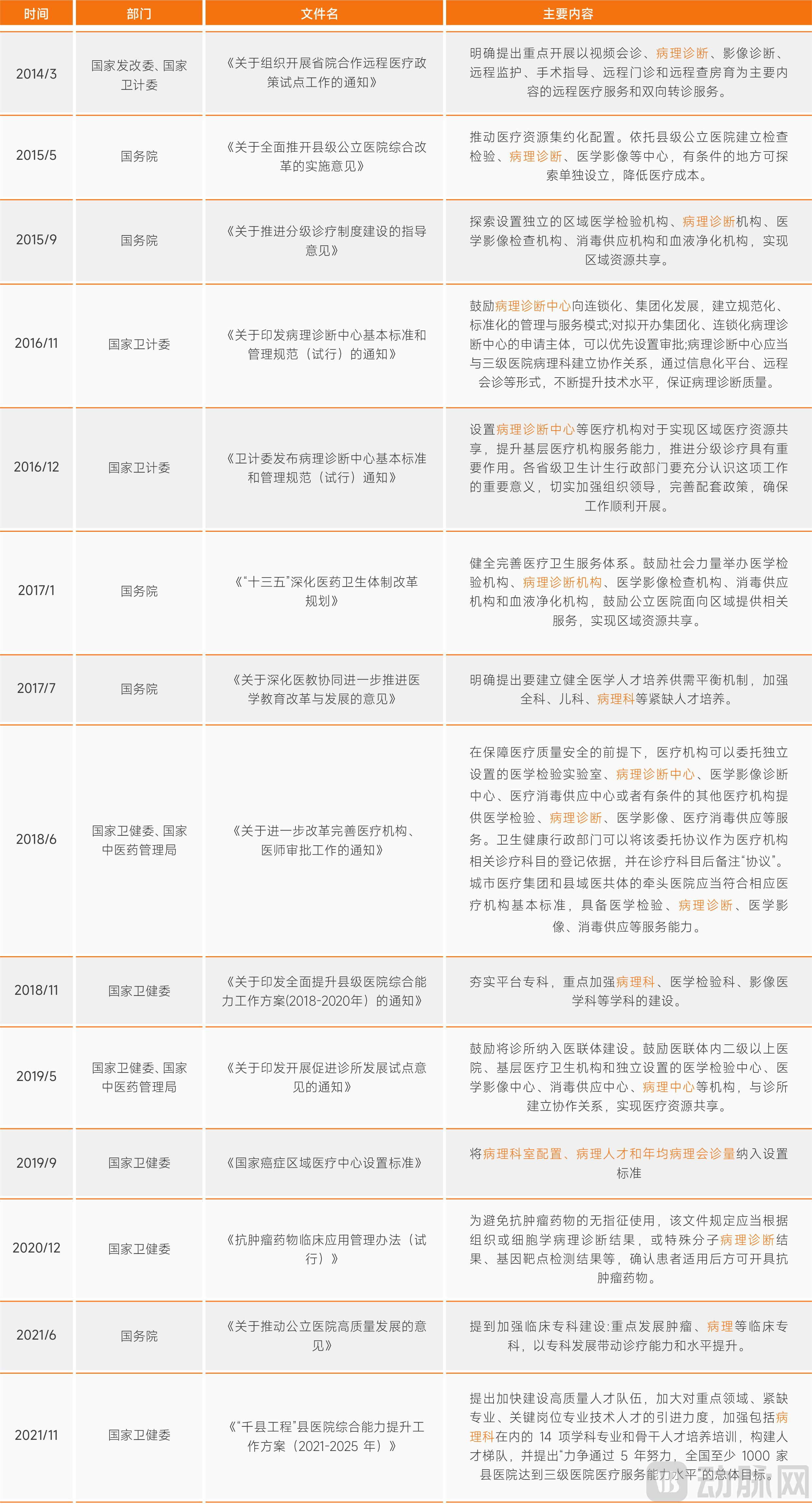

To accelerate the positive and forward development of the pathology industry, the state has successively introduced policies to encourage and support the accelerated development and construction of pathology departments.

National Policies Promoting the Construction of Pathology Departments and Pathology Centers Over the Past Decade

Data source: Compiled from public information; Chart by VCBeat.

Favorable policies and the significant cost reduction and efficiency gains achieved by digital and smart pathology solutions, both domestically and internationally, have prompted leading hospitals to prioritize the development of their pathology departments.

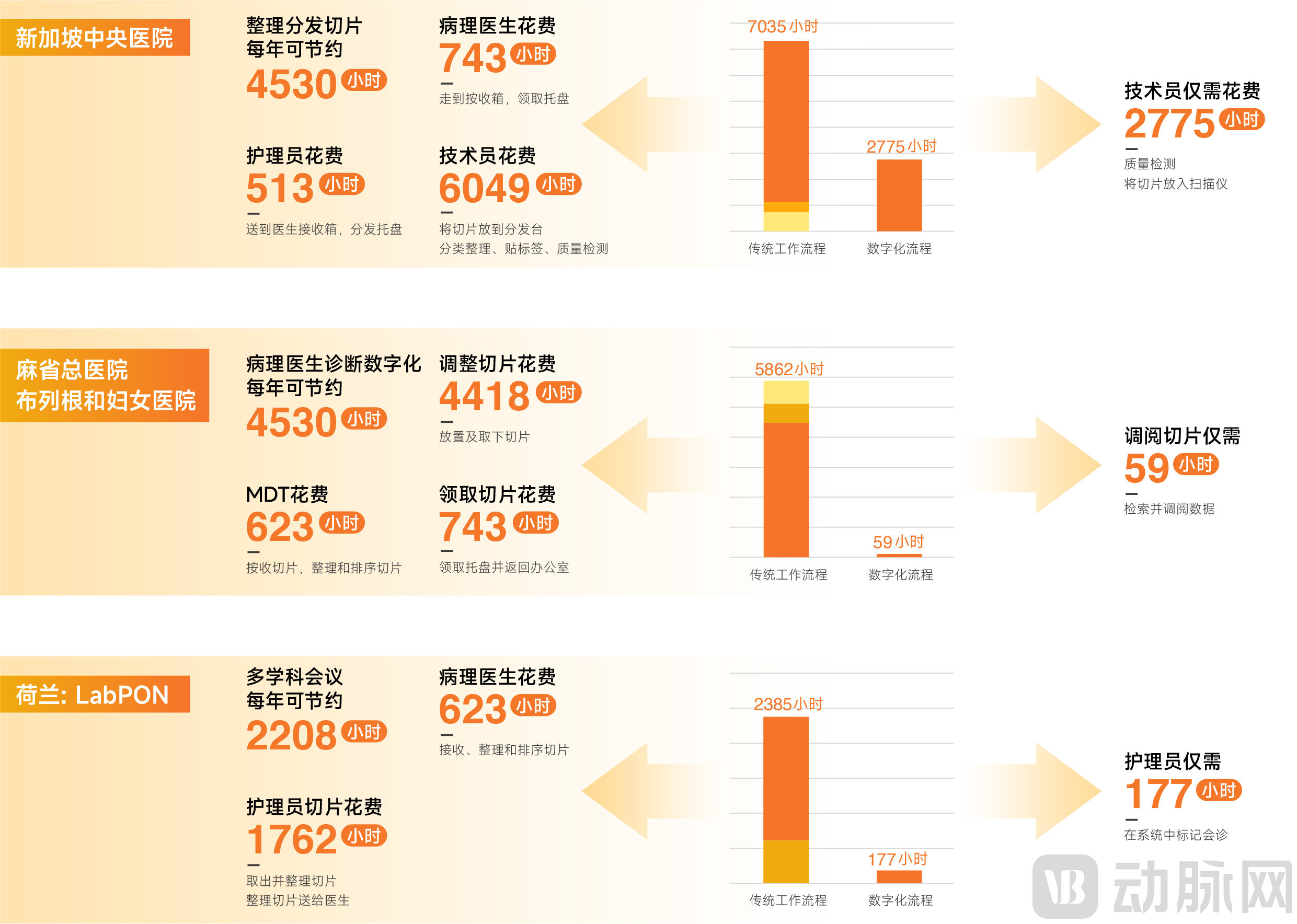

Hospitals in developed countries have achieved rapid and comprehensive digitalization of their pathology departments, with digital smart pathology demonstrating significant cost reduction and efficiency gains. Take LabPON in the Netherlands as an example. In 2015, LabPON became the world’s first 100% digital pathology laboratory. After full digitalization of its pathology department, LabPON found that it could save 19 hours per day, equivalent to saving 2.63 full-time equivalents (FTEs). Three years after the implementation of the first FDA-approved digital pathology system at LabPON in the Netherlands, clinical studies confirmed a 15% increase in hospital productivity.

Annual Work Hours Saved by Overseas Hospitals’ Pathology Departments After Digital Transformation

Data source: Journal of Clinical Pathology; graphic by VCBeat

In December 2022, Paige.AI published key research findings in a prestigious journal: with the assistance of Paige Prostate (the first FDA-approved AI pathology product, approved in September 2021), pathologists’ sensitivity for cancer diagnosis increased from88.7%Increased to96.6%, diagnostic specificity from97.3%Increase to98%. The dataset for this study includes slides from more than 150 medical institutions.

The benefits of China's digital and intelligent infrastructure development are already beginning to emerge.

Implementing remote diagnostics can improve the diagnostic accuracy of primary care pathology departments and alleviate the social issue of uneven distribution of pathology resources. Huayinkang, a domestic remote diagnostics platform, officially established its remote pathology platform in 2012. To date, it has built a medical laboratory network covering 27 provinces and regions, providing remote digital diagnostic services to more than 650 hospitals across China. It has cumulatively completed over 3 million remote pathology diagnoses and more than 100,000 remote intraoperative frozen section examinations.

In the field of smart pathology, clinical trial results for China’s first Class III-certified AI software for cervical cytology (developed by 91360) demonstrated that, under a human-AI collaborative reading model, the software achieved a sensitivity of 100% and a specificity of 96.29%, with a statistically significant 80.77% increase in diagnostic efficiency. Leveraging its digital and intelligent infrastructure, Xuzhou Maternal and Child Health Care Hospital has completed screening for over 25,000 cases in Peixian County, Xuzhou City. The detection rate of positive cases increased from 2–3% to over 5%, with an overall accuracy of 95% and a negative exclusion rate of 70%.

Where conditions permit, upgrading and expanding pathology departments has gradually become a consensus among hospitals.Currently, most tertiary hospitals and some secondary hospitals in China have completed their initial digital transformation. Nearly 10 large Grade A tertiary hospitals, including Taipei Veterans General Hospital and Shenzhen People’s Hospital, have achieved comprehensive digitalization and intelligent development of their pathology departments.

Recognizing the Importance of Pathology Departments, Leading Regional Hospitals Are Accelerating Their Development

Source: Survey interviews; chart by VCBeat.

The Many Challenges Behind the Trillion-Yuan Market Harbor Huge Development Opportunities: The Industry’s “Four Modernizations” Underway

According to a report from the 2020 World Congress of Pathology, the global pathology market size is projected to reach $44.4 billion by 2024, up from $30.3 billion in 2019, representing a compound annual growth rate (CAGR) of 6.1%. Data from Grand View Research indicates that the global digital pathology market was valued at $767.6 million in 2019 and is expected to grow at a CAGR of 11.8% through 2027. According to MarketsandMarkets, the global AI pathology market was valued at approximately $736 million in 2021 and is projected to reach $1.371 billion by 2026, with a CAGR of 13.2%.

According to relevant data, the potential market size for pathology testing in China exceeds RMB 40 billion. The digital pathology market in China surpassed RMB 1 billion in 2022, with the compound annual growth rate (CAGR) projected to exceed 10% over the next five years.Due toChina’s strong support for grassroots cervical and breast cancer screening has driven robust demand for pathological diagnosis, further expanding the scale of the pathology industry.

The pathology testing market is currently undergoing domestic substitution, presenting significant development opportunities for Chinese manufacturers. Although the era of digital and intelligent pathology has arrived, the overall level of “four modernizations” (automation, digitization, informatization, and intelligence) in pathology departments remains low.As no dominant players have yet emerged in the relevant industries, the introduction of new forms of AI-powered pathology products and their bundled sales with various other offerings are revitalizing the traditional pathology testing market while simultaneously driving rapid growth in the digital pathology market.

Current Status of Digital Intelligent Pathology Development: Modest Achievements, but a Long Road Ahead

Mature underlying hardware and software technologies, coupled with a diverse array of products across various scenarios and stages, are empowering hospitals to advance their digital and intelligent infrastructure.

The underlying hardware and software technologies are essentially mature, meeting the requirements for digital intelligence development.Currently, foundational technologies, including whole slide imaging (WSI), are advancing rapidly and have already met the requirements for building digital pathology departments. The rapid development of data storage and compression technologies has further reduced the costs associated with digital pathology infrastructure. Meanwhile, advancements in gigabit optical networks and 5G technology have significantly improved the efficiency and quality of remote pathological diagnosis.

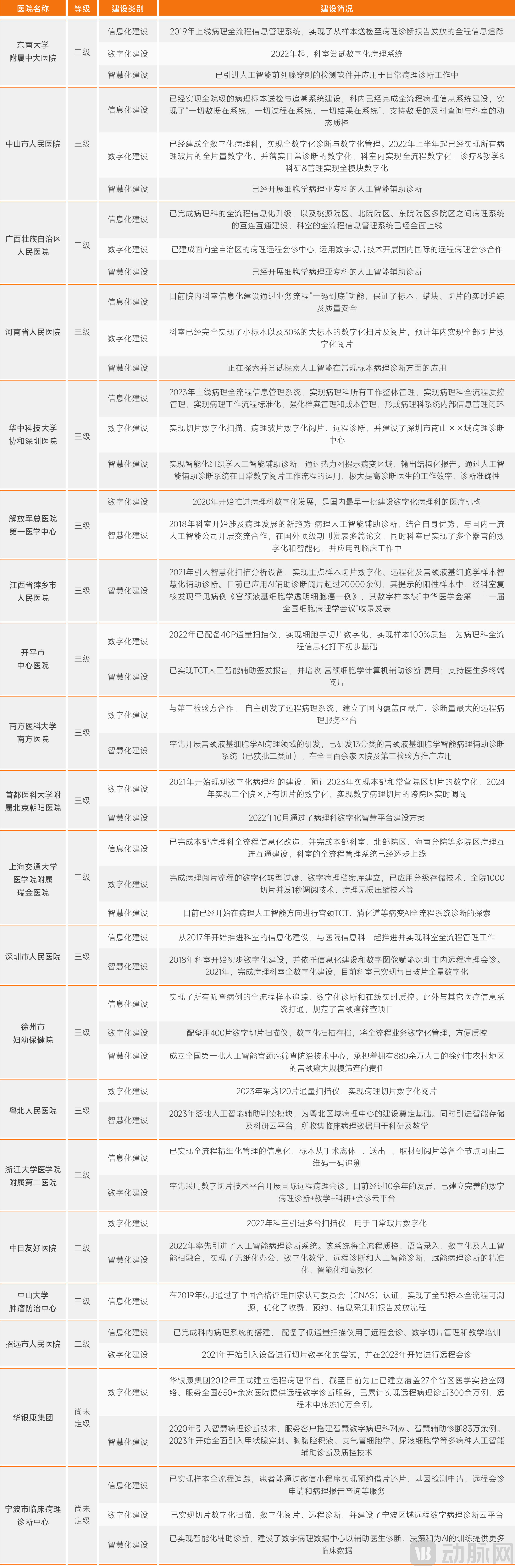

From automation and digitization to informatization and intelligence, a diverse array of products for various stages of pathological diagnosis is flourishing, gradually covering the entire workflow of pathological diagnosis.

1Automation

A wide range of automated products have been developed for various steps, including tissue processing, embedding, sectioning, staining, and mounting. Examples include the fully automated stainers from SinoTest and Kuoran Bio, as well as Kedee’s fully automated microtomes and tissue processors.

Several Fully Automated Pathology Pre-Analytical Processing Systems on the Market

Data Source: Public Information

2Digitalization

Digitalization primarily encompasses the digitization of slide content, diagnostic processes, and educational training.

Schematic Diagram of Traditional Pathology to Digital Pathology Workflow

Data source: Public information; chart by VCBeat

In the field of remote diagnosis, the China Digital Pathology Remote Diagnosis and Quality Control Platform, established by the National Health Commission, and the Remote Pathology Platform built by Huayinkang Group are currently the two largest remote diagnosis platforms in China. The former now covers more than 2,500 medical institutions nationwide and is the world’s largest remote pathology consultation support platform, while Huayinkang has to date provided remote digital diagnostic services to over 650 hospitals across China.

In the field of pathology education and training systems, companies such as Shengqiang Technology, Fangxin, and Zhijian Life have all launched related products.

In the field of digital slide scanners, digital pathology vendors have developed various types of digital slide scanners to address the diverse needs (low, medium, and high throughput) of hospitals across different scenarios (research, frozen section, routine diagnosis, etc.).

With technological advancements and product iterations, the market share of domestically produced digital slide scanners in China has now exceeded 70%, essentially achieving domestic substitution for digital pathology products.Currently, in ChinaDigital Slide Scanner MarketThe market is primarily dominated by domestic and international manufacturers such as Jiangfeng Bio, Shengqiang Technology, 3DHISTECH, Leica, and Motic. While the high-end segment remains occupied by imported digital pathology equipment providers like 3DHISTECH, a larger share of the hospital market is captured by Chinese-made digital pathology equipment manufacturers represented by Jiangfeng Bio and Shengqiang Technology.

Specifically, in terms of scanning speed and throughput, some domestic scanners have long matched or even surpassed imported counterparts. Moreover, Chinese manufacturers excel in promptly responding to user needs and developing personalized features based on user habits. For instance, between 2019 and 2022, Shengqiang Technology pioneered the global launch of multiple high-throughput (510P/600P/1200P) high-resolution (up to 0.090 μm/pixel) digital slide scanners. The company also developed proprietary extreme compression technology capable of reducing image file sizes by more than 80%, thereby providing comprehensive department-wide digitization services to pilot hospitals such as Shenzhen People’s Hospital, among the first in China to implement full-scale digital pathology.

3Informatization

Over the past two to three decades, China has made significant progress in the informatization of pathology, evolving from standalone workstations for pathological image and text reporting, to hospital-wide management and quality control of pathological information across the entire workflow, and further to regional telepathology consultation platforms.

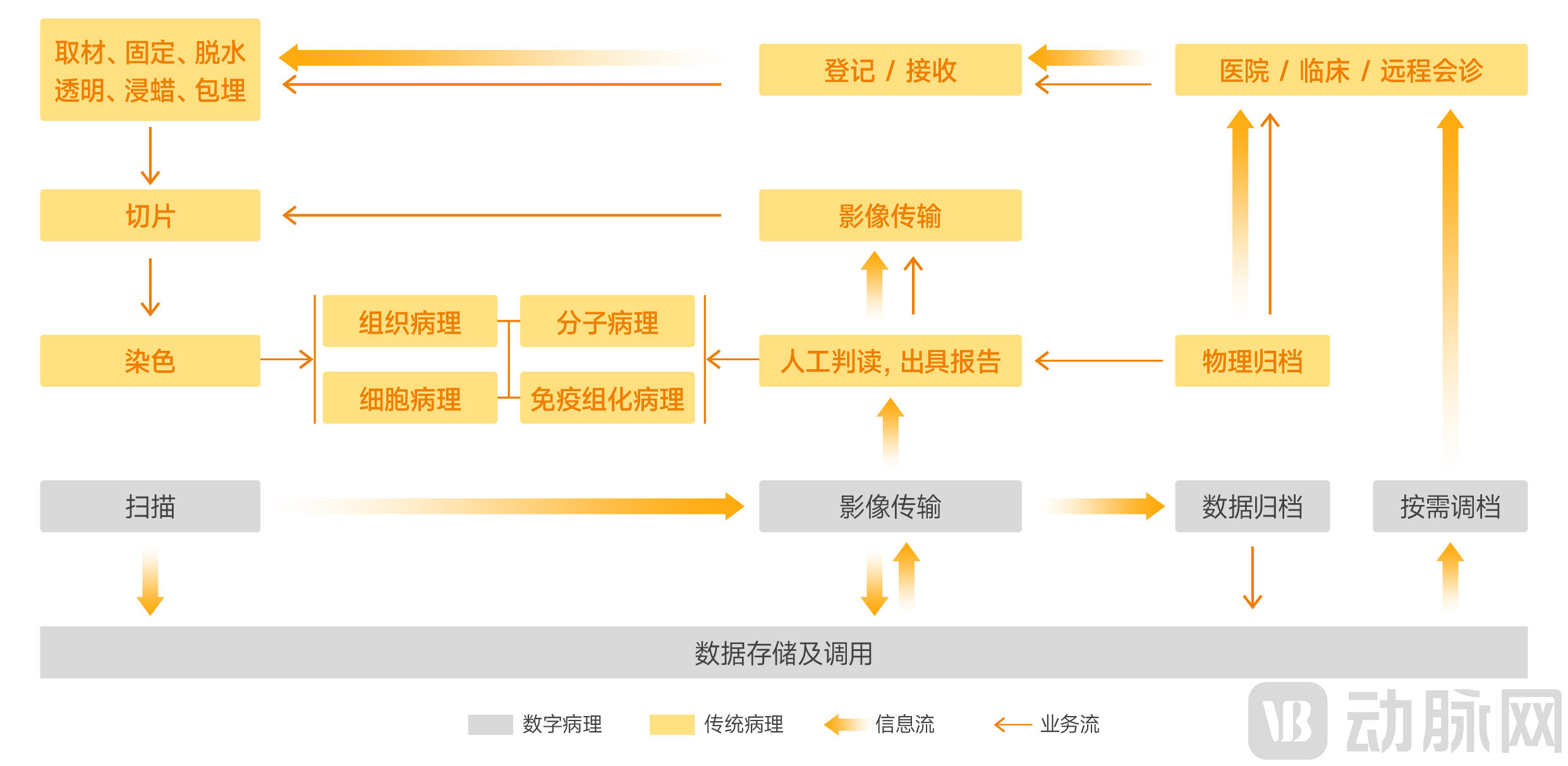

Pathology Full-Process Quality Control and Information Management System

Source: Public information; chart by VCBeat

Currently, companies deeply engaged in pathology information systems, such as Fangxin, Langjia, and Medix, are experiencing rapid growth. Meanwhile, pathology AI and digital pathology enterprises, including 91360, Shengqiang Technology, and Jiangfeng Bio, have also made significant inroads into the pathology informatics sector.

However, overall,Currently, the competitive landscape in the field of pathology informatics is relatively fragmented, with no dominant players holding a significant market share.Some companies, such as Fangxin, are rapidly capturing market share by leveraging highly differentiated business features, including end-to-end coverage and quality control of the pathology workflow, continuous system updates and iterations based on users’ personalized needs, and the assignment of dedicated engineers to each hospital.

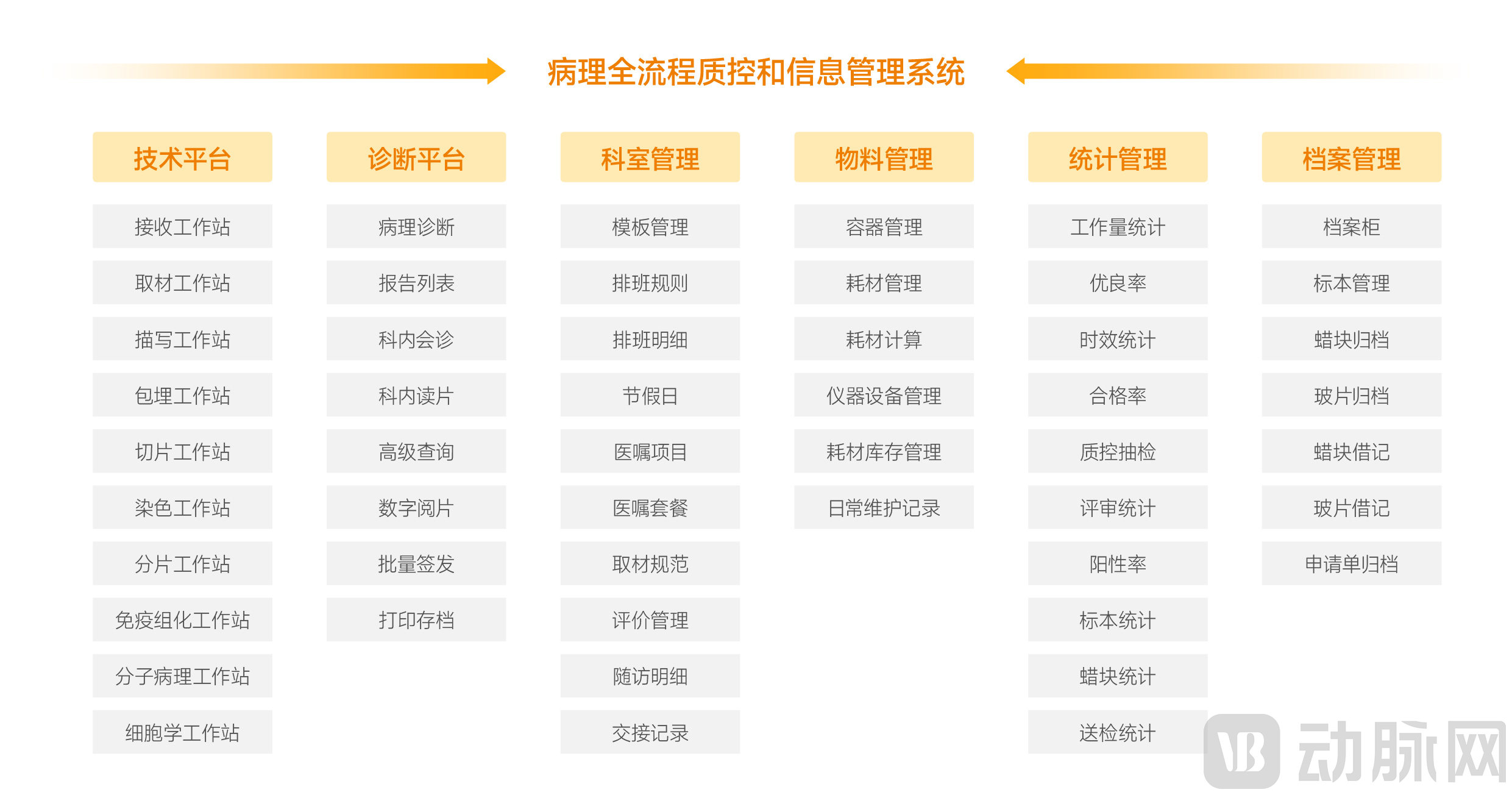

4Smartification

Chu Bing, a pathology expert at Zhongshan People's Hospital, pointed out, “Currently, the disease categories that account for the largest workload among pathologists in the pathology department are gastrointestinal cancers, cervical cancer, breast cancer, and urological cancers. Specimens related to these conditions collectively constitute approximately 80% of all pathological specimens.”

Currently,The software developed by domestic pathology AI companies basically covers most types of specimens in the pathology department (cervix, breast, digestive tract, etc.).Among these, AI-powered pathology software for cervical cytology screening is the most mature and widely adopted, with products already approved as Class III medical devices.More than 20 provinces, including Shandong, Hubei, Jilin, and Jiangsu, have currently included computer-assisted analysis of cervical liquid-based cytology in their price charge catalogs.

Schematic Diagram of the Business Process: Traditional Pathology – Digital Pathology – Smart Digital Pathology

Source: Public information; chart by VCBeat.

Pathology AI software for gastrointestinal tract, breast diseases, and other indications is also becoming increasingly mature.VBInsight’s core product, Thorough Insights®The sensitivity for identifying gastrointestinal malignancies approaches 100%, with specificity exceeding 80%. Currently, the company’s products have been adopted by more than 30 large hospitals, and its customer base is growing rapidly.

In the field of breast cancer, current practice primarily relies on immunohistochemistry results to determine molecular subtypes, guide treatment decisions, and provide prognostic insights. Currently, more than ten companies in China, including Dyingjia, Touche Future, Kunyuan Fangqing, Huaxi Precision, Savisen, and Zhijian Life, have developed related software, with their products rapidly maturing and improving.

Pathology AI companies in China generally prioritize focusing on 1–2 core disease types based on their respective circumstances. Currently, no company in the market has demonstrated the capability to cover more than three disease types while ensuring high-accuracy auxiliary diagnosis for each. Chen Jie, an expert in pathology artificial intelligence algorithms at the Institute of Clinical Pathology, West China Hospital, Sichuan University, pointed out thatThe first pan-cancer pathology AI software is likely to achieve its initial breakthrough in lymph node analysis.

“Lymph node metastasis in cancer is primarily categorized into macrometastasis, micrometastasis, and isolated tumor cell (ITC) metastasis based on the size of the metastatic foci. For pathologists, macrometastases are readily identified and distinguished; however, micrometastases and ITCs are often difficult to detect due to their minute and occult nature, leading to a high risk of missed diagnoses and underestimation of the tumor’s TNM stage. If pathology AI software could identify and distinguish these subtle, occult metastatic lesions, thereby assisting pathologists in the diagnostic evaluation of cancer, it would undoubtedly provide substantial support to their work.”

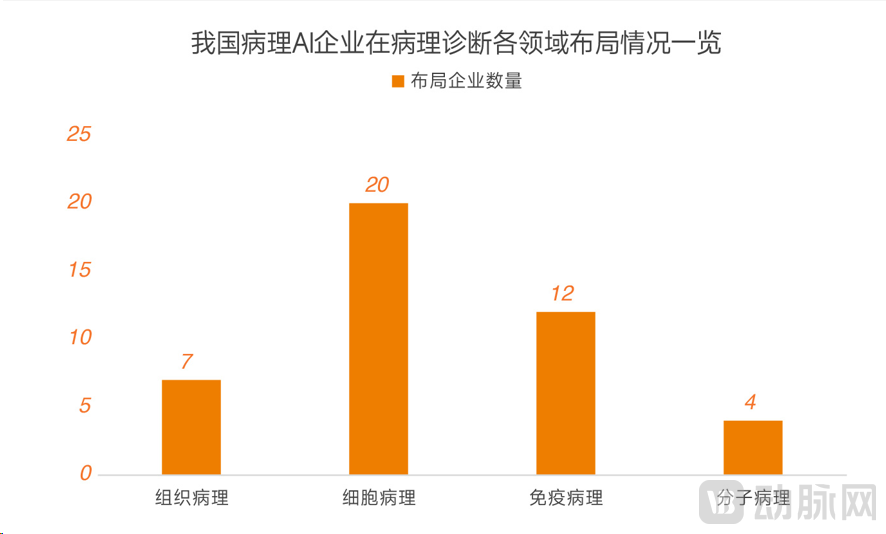

In terms of fields, cytopathology currently exhibits the highest level of intelligence, followed by immunohistochemistry. Histopathology has a relatively lower level of intelligence, while molecular pathology has the lowest.

Overview of the Layout of Chinese Pathology AI Companies in Various Fields of Pathological Diagnosis

Data Source: VBInsight; Chart by VCBeat

Pathology AI Commercialization Enters Deep Waters: First Class III Medical Device Certificate Approved, Included in Pricing Catalogs of Over 20 Provinces, and Diverse Business Models Emerge

The First Class III Medical Device Certificate for Pathology AI Is Issued, Marking a Milestone Breakthrough in China’s Pathology AI Industry. In March 2023, the Computer-Aided Analysis Software for Digital Pathology Images in Cervical Cytology, developed by 91360, officially received approval from the National Medical Products Administration (NMPA). This marks the first Class III medical device certificate for AI in the field of cervical cytology in China, signifying that the application of AI in cervical cytology has entered a phase of substantive implementation.

Industry insiders pointed out:On the one hand, the first Class III medical device certification for pathology AI will further standardize the pathology AI software market; on the other hand, pathology AI software products approved with Class III certification will further expand market opportunities.

Successful Submission of the First Class III Medical Device Application for Pathology AI: Proactive Communication with Regulatory Authorities Is Key. Drawing on 91360’s experience in securing the first Class III medical device approval for pathology AI, this report summarizes key insights to serve as a reference for the industry.

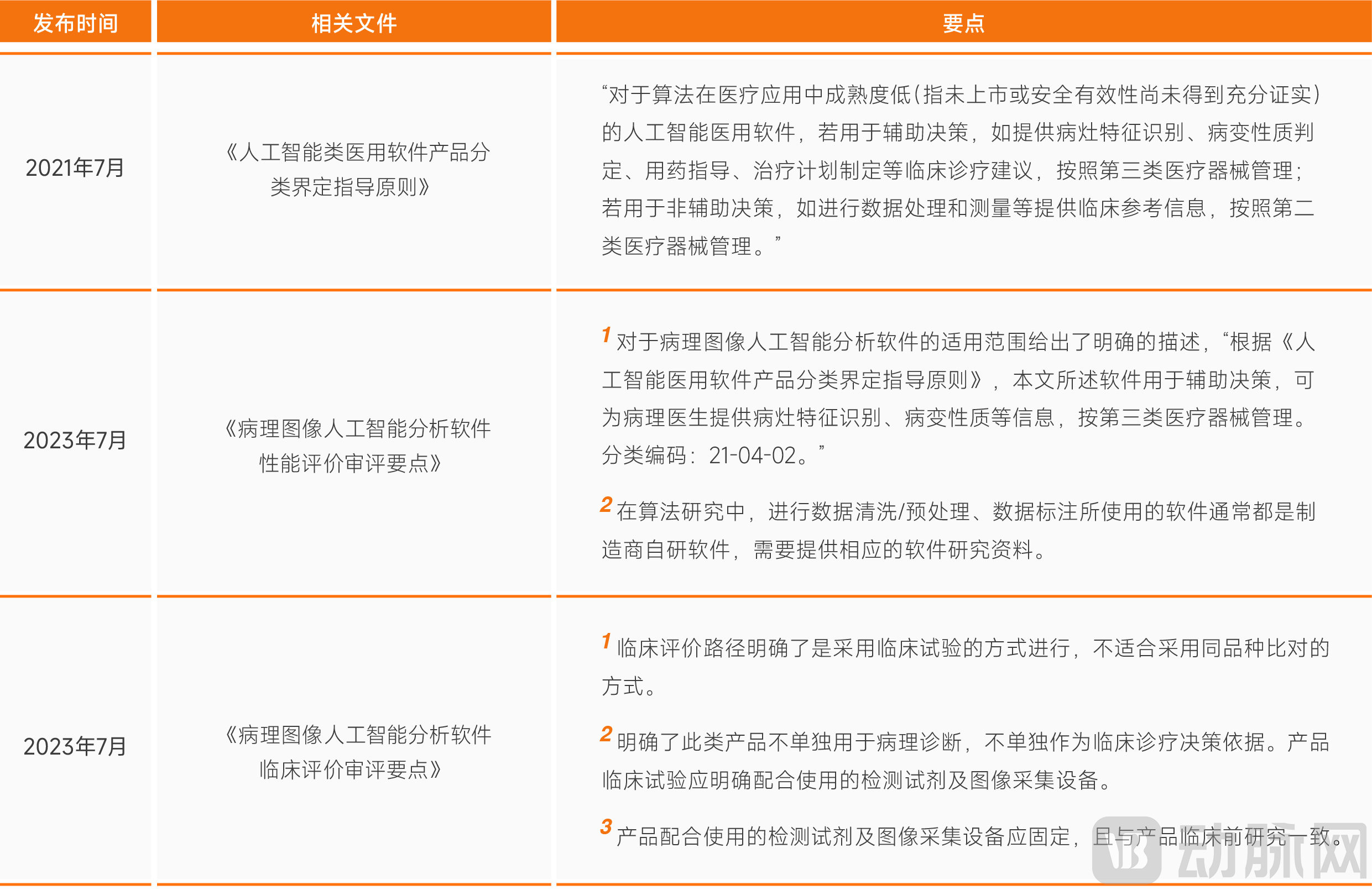

In July 2023, the guidelines for the approval of pathology AI software were implemented, further promoting standardized market development. Meanwhile, with clear principles for evaluation and approval, more companies are expected to obtain Class III medical device certificates for pathology AI in the next 1–2 years.

The Review and Approval Pathway for Pathology AI Software in China Is Becoming Increasingly Clear

Data source: Research interviews, public information, charted by VCBeat

Obtaining Class III certification is the entry threshold, but product competitiveness remains paramount; companies should advance according to their own development pace.

Given the national regulatory clarification that AI-assisted pathological diagnosis software shall be regulated as Class III medical devices, any enterprise with the requisite conditions, capabilities, and ambition to expand its market presence in the field of AI-assisted pathology should prioritize obtaining Class III certification for its AI software. However, each company must adjust the pace of its certification applications in accordance with its own development status.

Applying for a Class III medical device registration certificate is a high-investment, long-cycle endeavor.According to research by VCBeat Institute, 91360 spent approximately6–7 yearsandTens of millions of yuanR&D Investment.

“While similar products enjoy a strong reputation in the industry, some companies have not yet devoted significant efforts to obtaining Class III medical device certification. They explain that securing such certification requires multi-center validation, which involves signing agreements with numerous hospitals to conduct large-scale clinical trials. The cost of collaborating with each hospital for these trials can range from hundreds of thousands to over one million yuan. Coupled with the substantial capital required for product R&D, the financial pressure is immense.”

Moreover, since pathological data are continuously and rapidly updated, even after obtaining Class III medical device certification, AI software for pathology must undergo continuous updates and iterations, as software approved in earlier stages may not be applicable to the current realities of the pathology industry.

Therefore, for companies with limited human and financial resources, prioritizing the application for Class III medical device certification is not the optimal choice at present.

The market performance of AI-based pathology products depends on their inherent competitiveness, but obtaining Class III medical device certification is an indispensable prerequisite.Dr. Cheng Hao, Partner at Shengshan Capital, believes that while the Class III medical device certification serves as a barrier to entry in the industry, a product’s ultimate market performance still depends on its inherent competitiveness: namely, whether it meets genuine clinical needs, truly addresses the current pain points of pathologists, offers superior performance, and provides high cost-effectiveness.

The pace of obtaining certification requires enterprises to make comprehensive assessments and decisions based on their own development rhythms and predictions of the evolution of the competitive market landscape. Nevertheless, it is undeniable that obtaining Class III medical device registration is an indispensable pathway for formal AI-assisted pathological diagnostic products.

Multiple provinces have initiated pricing and fee structures for cytopathology services, and histopathology is also expected to be included in the official price catalog, thereby driving incremental growth in the pathology AI market.

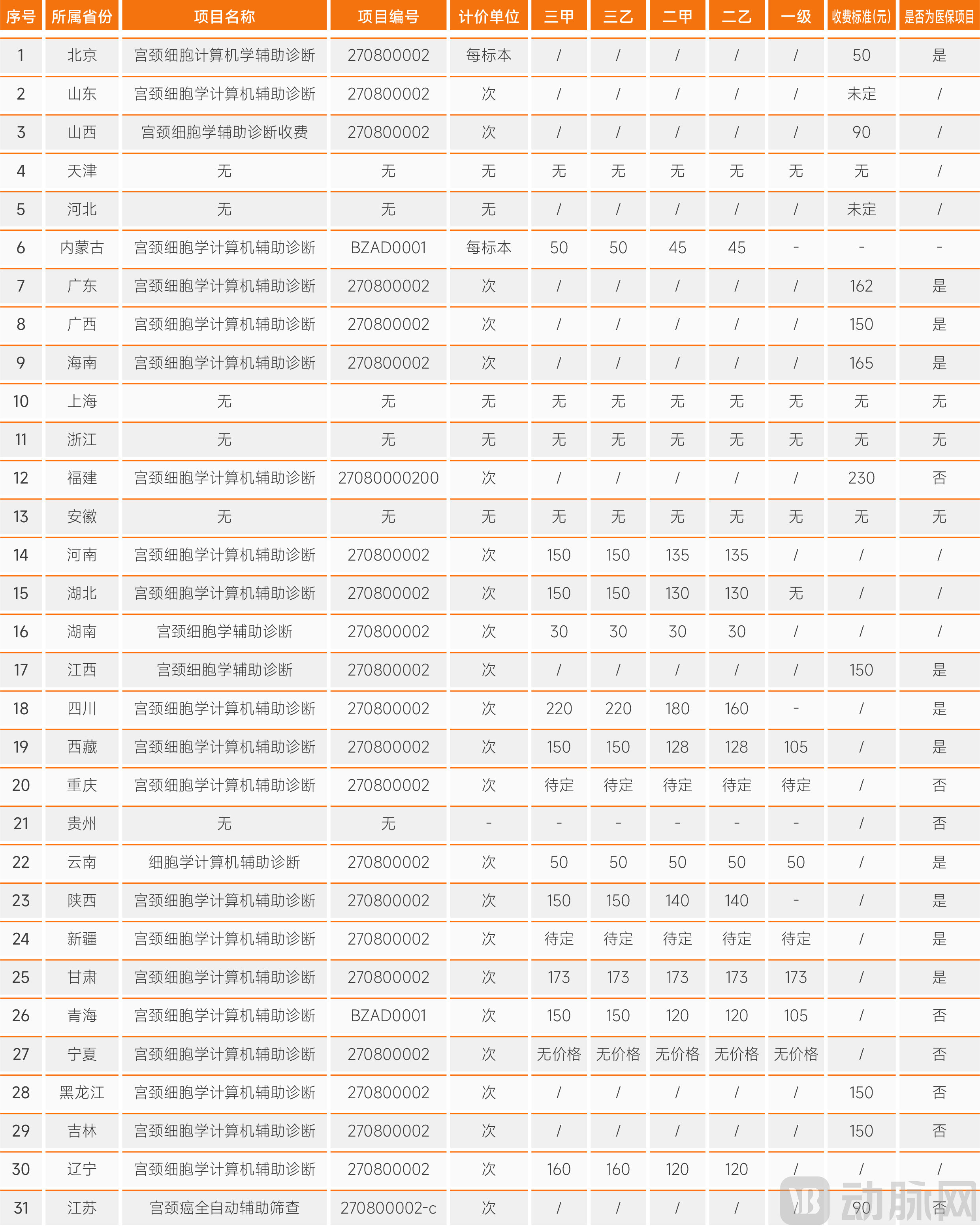

To promote cervical cancer screening, more than 20 provinces across China have already included computer-aided analysis of liquid-based cervical cytology in their official price lists for medical services. Some provinces and municipalities, including Beijing, Guangdong, and Guangxi, have even incorporated it into their medical insurance reimbursement catalogs, with fees ranging from RMB 30 to RMB 230 per specimen. Industry experts point out that,Inclusion in the price charge catalog is a key factor influencing hospital decision-making.

Statistics on Fees for AI-Assisted Cervical Cytology Diagnosis in Selected Provinces and Cities in China

Data Source: Interviews, Public Information, Chart by VCBeat

Furthermore, in September 2023, the “Technical Specifications for Medical Service Items (2023 Edition)” was released, incorporating computer-aided diagnosis of cervical cytology. This inclusion facilitates a more standardized, regulated, and widespread adoption of computer-aided diagnosis for cervical cytology, thereby further expanding the market.

"Technical Specifications for Medical Service Items (2023 Edition)" includes computer-assisted diagnosis of cervical cytology.

Data Source: "Technical Specifications for Medical Service Items (2023 Edition)"

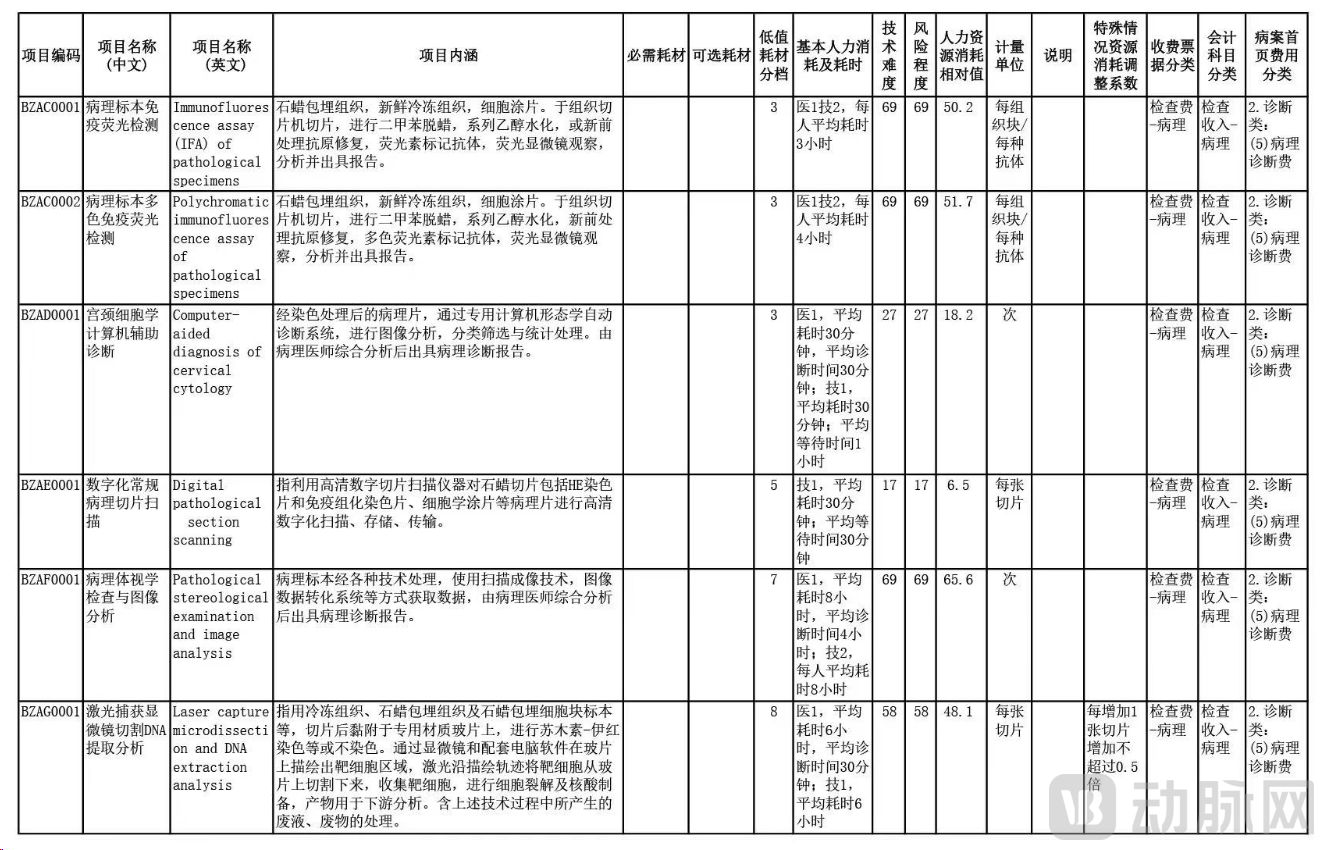

Industry insiders pointed out,AI-assisted diagnostic services for histopathological subtypes may also become eligible for regulated pricing in the future, representing a potential incremental market.In a public report, Professor Liang Zhiyong, Director of the Department of Pathology at Peking Union Medical College Hospital and Chairman of the Pathology Branch of the Chinese Medical Association, stated that the association is currently communicating with relevant national authorities on specific implementation details and actively promoting the addition of new pricing items for AI-assisted histopathological diagnosis.

Enthusiasm for the development of hospital pathology departments across China has increased, industry products have become more refined and mature, and hospitals’ willingness to purchase has risen rapidly.According to research, in 2023, the attention paid by senior hospital leaders, such as deans, to the development of pathology departments rose rapidly. They began proactively reaching out to companies to discuss collaborations, leading to a swift increase in hospitals’ willingness to purchase. This trend was evident across the spectrum from informatization and digitalization to intelligent transformation.

Fangxin, a domestic provider of pathology informatics solutions, pointed out that with the accumulation of real-world cases and increased enthusiasm among hospitals for building up their pathology departments, the company’s business opportunities have grown year by year. From last year to this year, the annual year-on-year growth in the volume of business orders has exceeded 50%. In the digitalization sector, a certain domestic digital pathology vendor revealed, “The company’s annual revenue was around RMB 60 million last year. With hospitals’ growing enthusiasm for establishing pathology departments and an increasing number of hospitals embarking on comprehensive digital transformation, the company has continued to achieve significant business growth this year.” In the field of pathology AI, a leading domestic pathology AI company disclosed, “Last year, the company’s annual revenue was still in the tens of millions of RMB range; this year, it has multiplied several times over.”

Diverse commercialization models are in play; while some pathology AI products have adopted per-case pricing or outright software purchase options, the majority of pathology AI products on the market rely on premium-priced integrated pathology solutions to implement “hidden charges.”This phenomenon is attributable not only to the immaturity of pathological AI products—such as their failure to comprehensively cover major diagnostic disease categories across key departments while ensuring high diagnostic accuracy for each, coupled with inconsistent product performance—but also to the absence of a established culture in the Chinese market of paying separately for software.

Multiple industry insiders predict,This practice of embedding hidden software fees within premium integrated pathology solutions is likely to persist for an extended period. The key breakthrough for the industry lies in achieving true product maturity and securing broad clinical acceptance.

Precision medicine, new drug development, and digital intelligent pathology are seeing increasingly deep and broad explorations of application scenarios, demonstrating significant market potential.

The rapid advancement of science has enabled humanity to gain a deeper understanding of the mechanisms governing the onset, progression, and evolution of diseases. Analytical research based on pathological data demonstrates significant potential for development in the fields of precision medicine and new drug discovery.

In terms of precision diagnosis and treatment,Analysis based on pathological data enables precise screening of patients likely to benefit from immunotherapy. For instance, quantitative analysis of multiple biomarkers in immunohistochemistry results can directly guide medication selection and prognostic assessment for cancer patients. In contrast, traditional manual interpretation of tissue biomarkers is time-consuming, labor-intensive, and subjective, significantly increasing the diagnostic burden in oncology while posing substantial challenges to pathologists.

Building on the digitization of pathological slides, AI-powered quantitative pathology software can translate pathologists’ localized interpretive expertise into objective algorithms, extending quantitative analysis to the entire slide and presenting the results intuitively through visualized charts. Such AI analysis software is characterized by automation, high efficiency, and strong reproducibility, thereby enhancing the objectivity and precision of tumor companion diagnostics. At any given threshold (e.g., 1% or 5% positivity rate), AI-based pathology software often identifies more PD-L1–positive patients than human reviewers.

In terms of new drug development,Analysis based on pathological data also has numerous application scenarios. Currently, analysis based on pathological data is mainly applied in two major areas:First, to guide patient enrollment in clinical trials and develop companion diagnostic products for drugs; second, to support scientific research and guide the development of new drugs.

Companion diagnostic tools developed based on pathological data enable pharmaceutical companies to meticulously classify patients by disease type and pathological stage, facilitate appropriate patient enrollment, and predict potential treatment responses according to histomorphological features, thereby tailoring optimal clinical decisions for each individual. For instance, Bristol Myers Squibb (BMS) has partnered with PathAI to leverage pathological AI models for better identification of patient populations, reducing therapeutic development risks in their drug pipeline. Furthermore, patient stratification in clinical trials across multiple disease indications is being conducted based on analyses from these pathological AI models.

As pathological images contain rich data, many morphological features or biomarker signals are associated with drug efficacy.Digital intelligent pathology systems can analyze and mine large volumes of pathological data to uncover the patterns and mechanisms underlying disease onset, progression, and prognosis, thereby providing data support and scientific evidence for drug development and accelerating the drug discovery process.Pharmaceutical companies, including BMS, are leveraging insights generated by pathology-based AI models to inform the early stages of their pipelines, thereby accelerating clinical drug development.

Domestic companies, including LBP Medicine and Kuoran Biology, recognized the market potential of leveraging pathology data analysis to guide new drug development and began exploring related business areas at an early stage. For instance, as early as 2021, Kuoran Biology established a comprehensive multiplex fluorescent immunohistochemistry technology platform in its Shanghai laboratory to launch central pathology laboratory CRO services, focusing on pharmaceutical R&D and immunohistochemistry-based companion diagnostics.withOpen Platform Strategy: Opening the technology platform to third-party medical testing laboratories, research institutions, pharmaceutical companies, and other partners.。

In the future, with advancements in AI technology and a deeper understanding of pathological morphology, we can anticipate that AI will explore tumorigenesis and tumor evolution through pathological data. By leveraging computer programs to visualize and quantify tumor heterogeneity and the tumor microenvironment, and even to identify abnormal genes and signaling pathways driving tumor cell proliferation and migration, AI will facilitate precision diagnosis and treatment as well as new drug development.

Future Opportunities and Development Trends in the Industry

Large Models Accelerate R&D of Pathology AI Products, Address Knowledge Gaps, and Tackle Challenges in Cancer Treatment

In September 2023, Paige.AI announced a partnership with Microsoft to build the world’s largest image-based AI model for digital pathology and oncology. Trained on data derived from 4 million digitized pathology slides and configured with billions of parameters, the model aims to identify both common and rare cancers that are extremely difficult to diagnose, thereby assisting physicians in delivering improved cancer care with AI support and further advancing the fields of pathology and oncology. In the same month, China-based Thorough Future released its large pathology model, Thorough Brain.

By modeling large datasets, large language models may uncover previously unknown patterns, thereby addressing gaps in existing knowledge.Including the identification and diagnosis of some rare diseases, and even establishing a “universal organ recognition and diagnostic model.”With such a technological foundation, the pace of pathological AI product development will also be significantly accelerated.Large pathology models will exert broad influence across various fields in the future, including pathological diagnosis, scientific research, and education and training.

The Pathology AI Integration Platform May Be Established: Digital Smart Pathology and Traditional Pathology Actively Converge to Form a New Industrial Ecosystem

Multiple pathologists have pointed out that the AI-assisted pathological diagnosis software favored in clinical practice is a system capable of covering major disease types within the department (such as cervical, breast, gastrointestinal, and lung diseases) while ensuring high diagnostic accuracy for each condition, achieving performance comparable to over 80% of the proficiency level of pathologists.

However, due to the inherent complexity of pathology and the diversity of pathological tissues, different companies may emerge as leaders in developing high-quality AI-based pathology products for various disease types. It is difficult for a single AI pathology company to meet all hospital needs.

In the near future, it is likely that individual departments will utilize pathological AI software from multiple vendors. Amidst a fragmented and competitive market, the industry is expected to gradually evolve toward integrated pathological AI platforms, thereby enhancing operational efficiency across the industrial chain.

We believePathways to Establishing an Integrated Pathology AI Platform in the FutureMay include:Pathology informatics vendors are building open ecosystems to ensure compatibility with pathology AI software from different brands, fostering collaboration and product integration among pathology AI product developers.

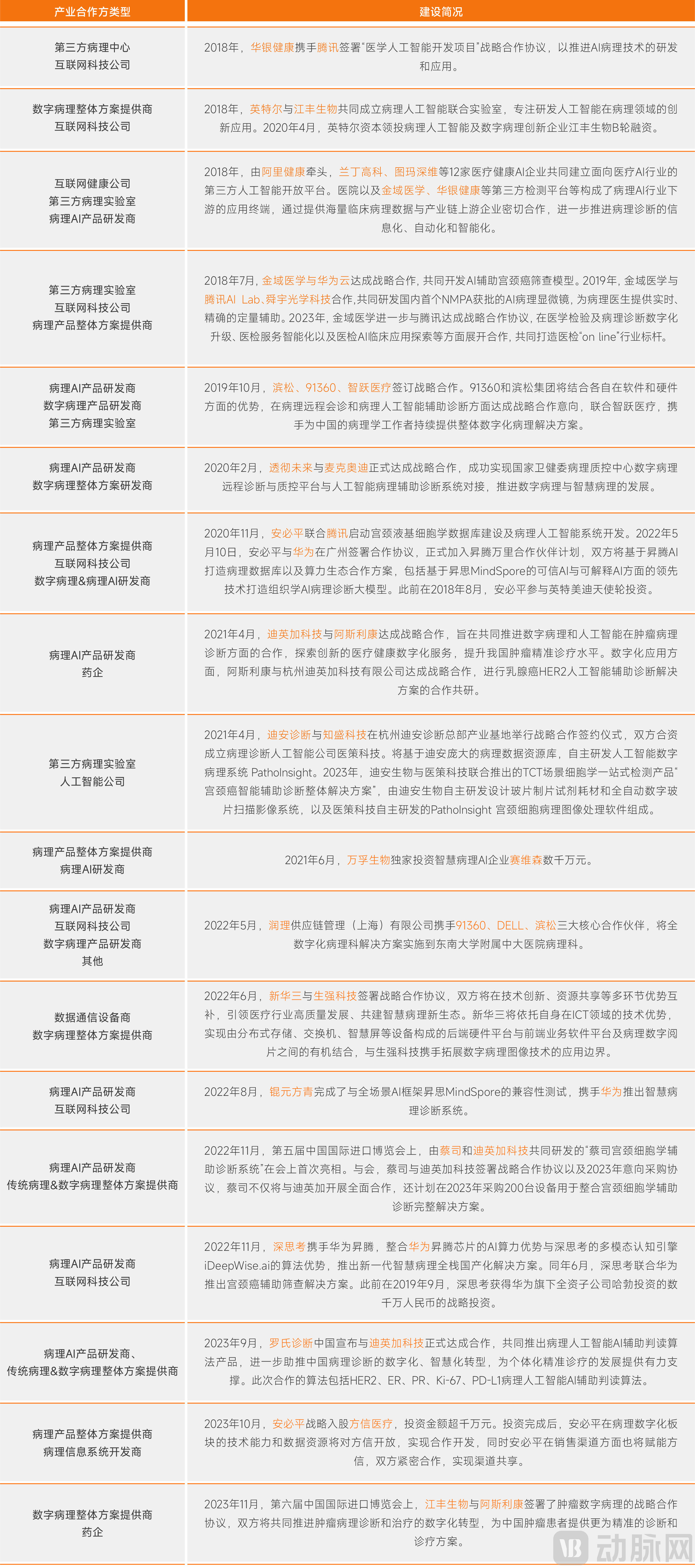

Mutual promotion: The active integration of digital intelligent pathology with the traditional pathology industry is fostering a new industrial ecosystem, with more industrial collaborations underway.

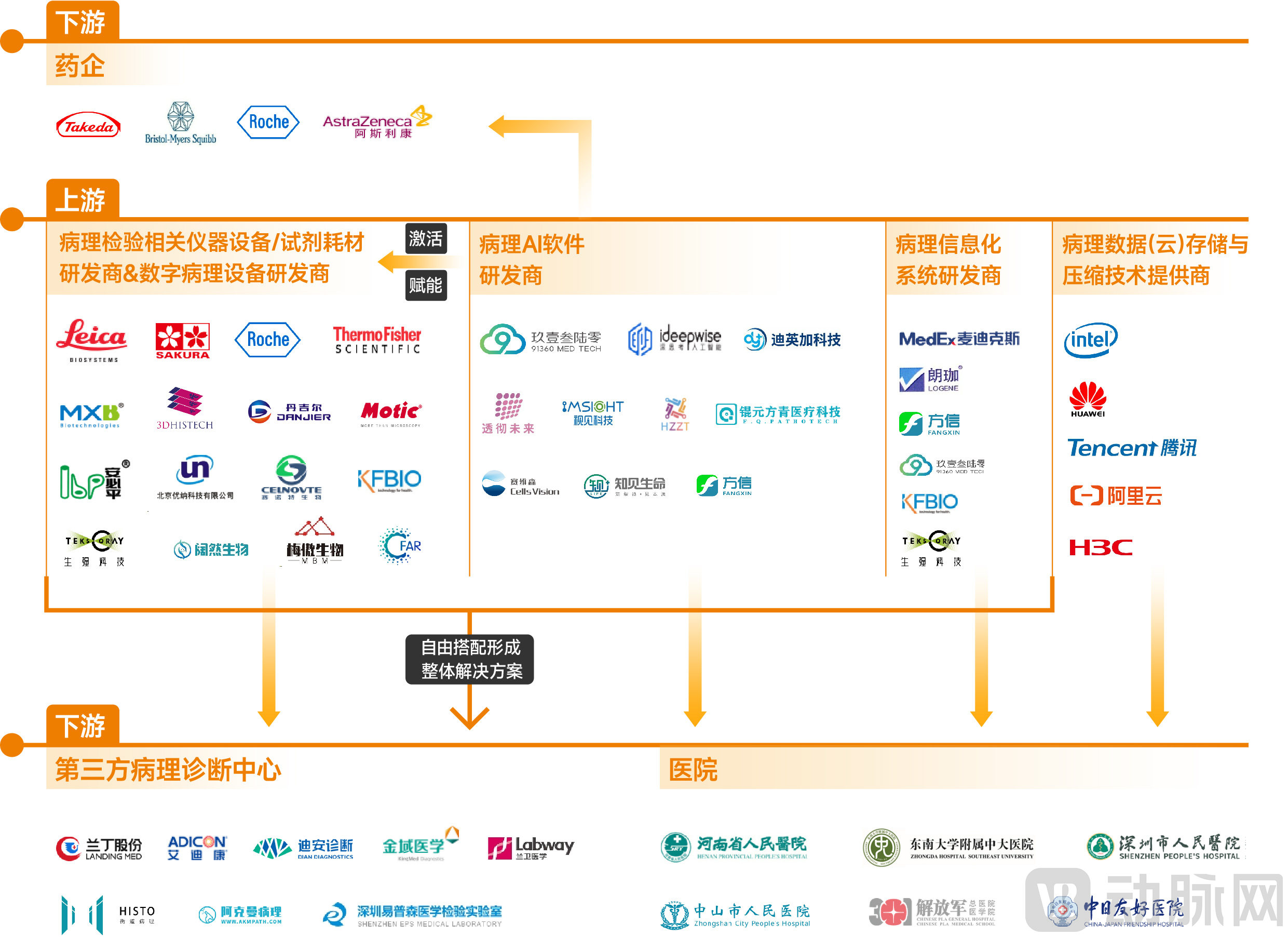

Behind the immature development of China’s pathology industry lie substantial growth opportunities. On one hand, traditional pathology products—such as diagnostic instruments and equipment, reagents, and consumables—remain partially dominated by imports, while domestic substitution is underway in other segments. On the other hand, with the accelerated advancement of the “four modernizations” in the pathology sector, digital and intelligent pathology is rapidly evolving. In both the traditional pathology testing market and the emerging digital intelligent pathology market, no dominant players have yet emerged, leaving ample room for future growth and innovation.

In recent years, collaborations across the pathology industry have emerged in abundance—whether among developers of pathological diagnostic equipment, manufacturers of reagents and consumables, providers of pathology information systems, developers of AI-powered pathology software, third-party laboratories, or internet technology companies offering cloud ecosystems and computing power. This wave of fervent collaboration is expected to continue in the future.

Digital Smart Pathology and Traditional Pathology Industries Actively Integrate to Form a New Ecosystem, with Various Industrial Collaborations in Full Swing

Data source: Public information; chart by VCBeat

On one hand, smart pathology products are revitalizing the traditional pathology testing product market., enhancing the competitive advantage of related products; on the other hand, smart pathology productsEmpowering the Digital Pathology Market,Enhance the motivation of pathologists to perform pathological diagnoses based on digital pathology slide fields of view, and expand additional product channels for them.

For smart pathology vendors, leveraging the product and market channel advantages of traditional pathology test product developers or digital pathology brands with strong market competitiveness will undoubtedly open up broader market access.

Mutual Promotion: The Active Integration of Digital Intelligent Pathology and Traditional Pathology Forms a New Industrial Ecosystem

Data sources: Research interviews, official company websites; Chart by VCBeat.

With capabilities complementing each other and driving mutual growth, the pathology industry is advancing with unprecedented vitality, leaving ample room for imagination regarding its future competitive landscape.

Addressing the Scarcity of Pathology Resources in Primary Healthcare Institutions: Stakeholders in the Pathology Industry Seize Development Opportunities

According to research, establishing a comprehensive digital smart pathology system requires a cumulative investment of approximately RMB 10 million and takes about 1–2 years to complete, extending to over three years in special circumstances. For primary healthcare institutions with low patient volumes and limited financial and human resources, building a full-scale digital smart pathology system entails substantial investment with minimal returns.

Some pathology experts have pointed out that hospitals with an annual caseload of fewer than 1,000 to 2,000 specimens do not even need to establish their own pathology departments; instead, they can send their pathology specimens to county-level pathology centers, primarily established by county people’s hospitals, or rely on third-party providers for pathological diagnosis.

Leading regional hospitals’ pathology departments and third-party pathology diagnostic centers can fully leverage the advantages of resource concentration, ushering in opportunities for rapid development.On one hand, the development of regional pathology centers is gaining momentum. Third-party remote pathology diagnostic providers, digital pathology companies, and pathology AI enterprises have established various forms of collaboration with certain regional pathology centers, seizing opportunities for growth. On the other hand, in regions where pathological resources are scarce and there is a lack of government-led initiatives to promote regional pathology centers, these centers face significant organizational challenges, thereby creating more opportunities for third-party pathology diagnostic centers.

Scanning Speed and Image Compression Emerge as Breakthroughs in Digitalization, While Smart Pathology Product Scenarios Await Expansion

Industry insiders have pointed out that large hospitals handle a massive volume of samples daily,There is still significant room for improvement in the scanning speed of digital slide scanners.In addition to actively seeking improvements in single-unit scanning speed, exploring technical directions such as breaking through parallel scanning, achieving non-stop loading and unloading of slides, and ensuring that slide changes do not affect the scanning rhythm are effective measures to address the current limitations in scanning speed. Currently, the industry is leveragingParallel multi-stage design and multifunctional, high-precision motion control design enable automated scanning modes.We are gradually making headway in addressing such issues.

Furthermore, most scanners on the market suffer from image defocusing during rapid scanning. However, overcoming the technical challenges associated with real-time autofocus is difficult; currently, only a few companies, such as Leica and Shengqiang Technology, have successfully mastered this technology. There is an urgent need for more digital pathology enterprises to either conquer this technological hurdle or provide alternative solutions.

Data Storage and CompressionAs one of the core barriers to building digital pathology systems, it is directly linked to the progress of digital and intelligent pathology construction in medical institutions, offering immense market space and potential. Currently, cost reductions achieved through secondary compression algorithms and tiered storage are far from meeting clinical demands. The industry must further advance image compression technologies to reduce storage footprint while ensuring image quality, thereby lowering the capital and operational costs associated with hospitals’ digital pathology infrastructure.With advancements in technology and product design philosophy, reducing equipment costs, lowering instrument maintenance requirements, and improving cost-effectiveness are more likely to gain widespread recognition among hospitals.

In terms of intelligence, the functions of current pathology AI software are still mainly focused on the recognition and assisted diagnosis of pathological images, but there are many other application scenarios yet to be explored: for exampleInformation Integration, Data Analysis, Knowledge Think Tank, Speech Recognition, Search Error Correction, Gross Specimen Assisted AnalysisandIntelligent Specimen Collection and Slide Preparation Quality Controletc.

NGP: The Next Growth Driver After NGS

Growing research evidence attributes the variability in immunotherapy outcomes to the heterogeneity of the tumor microenvironment, and the current focus of diagnostic pathology in oncology is shifting from targeted therapy to the study of the tumor immune microenvironment.Current clinical technical approaches have limitations, and there is an urgent need for more novel technologies to decipher the complex interactions between tumor cells and components of the tumor immune microenvironment.

Next-generation pathology (NGP) technologies, represented by multiplex fluorescent immunohistochemistry, warrant attention.Unlike the qualitative analysis of conventional immunohistochemistry, the emerging multiplex fluorescence immunohistochemistry technology has achieved technical innovations in multi-label staining, spectral imaging, and intelligent analysis. It overcomes the limitations of single-label and qualitative analysis in traditional pathology, as well as the inability of gene expression profiling and flow cytometry to obtain in situ spatial information of proteins and cells, demonstrating significant application advantages in analyzing the tumor immune microenvironment.

Multiplex fluorescence immunohistochemistry enables the acquisition of multichannel data on cellular composition and spatial architecture, facilitating high-dimensional analysis of the tumor microenvironment. This approach deepens our understanding of tumorigenesis, predicts therapeutic responses, and precisely identifies patients likely to benefit from immunotherapy. From a commercial perspective, this technology offers controllable throughput without startup volume constraints and benefits from established reimbursement models, positioning it for rapid adoption in pathology departments.

AI-based modeling of pathological data to enable patient-level genomic predictions is also a new direction that the clinical community eagerly anticipates will be implemented in practice.Sun Shijun, Director of the Department of Pathology at Zhongshan People’s Hospital, pointed out that establishing AI algorithm models based on pathological slide data to directly predict genetic-level information would not only significantly shorten clinical diagnosis and treatment time and effectively enhance the level of precision medicine, but also substantially reduce patients’ diagnostic and therapeutic costs.

The above is an excerpt from the main content of the report. To obtain the full report, please scan the QR code to add our assistant and initiate a conversation upon connection.

Special Acknowledgments (in order of research interviews):

Cheng Hao, Partner at Shengshan Capital; Di Feng, Chairman and CEO of 91360; Luo Zhaohui, Director and COO of 91360; Wang Shuhao, CTO of Touche Future; Professor Ding Yanqing, Chairman and Founder of Kunyuan Fangqing; Wang Jianguo, Founder of Fangxin; Sun Shijun, Director of the Department of Pathology and Chief Physician at Zhongshan People's Hospital; Chu Bing, Medical Expert and Chief Physician at Zhongshan People's Hospital; Bu Lingbin, Chairman of Kuoran Biology; Chen Jie, Pathology AI Algorithm Expert at the Institute of Clinical Pathology, West China Hospital, Sichuan University; Wang Zihan, COO of Shengqiang Technology; and other unnamed industry professionals.

References:

1. VCBeat and VBInsight: “White Paper on China’s Smart Pathology Industry”

2. Department of Pathology, Ruijin Hospital, Shanghai Jiao Tong University School of Medicine. VCBeat “White Paper on the Construction of Digital Smart Pathology Departments”

3. Shanghai Digital Medicine Innovation Center. “White Paper on the Development of China’s Smart Digital Pathology Industry in 2022”

4. Yao Jianguo. Current Status and Future Prospects of Clinical Applications of Digital Pathology[J]. Journal of Sichuan University (Medical Sciences), 2021, 52(2): 156-161.

5. Liu Honghong, Shi Yujun, Bu Hong. Investigation and Reflections on the Current Status of Pathology Departments in 3,831 Hospitals Across 31 Provinces (Autonomous Regions, and Municipalities) [J]. Chinese Journal of Pathology, 2020, 49(12): 1217-1220.

6. Pathology Quality Control Center, National Health and Family Planning Commission. "2015 National Report on Medical Quality in Pathology Departments"

7. 91360 Official Account. “After Much Anticipation, It Finally Emerges” — A Study of the Review Points for Artificial Intelligence-Based Pathology Image Analysis Software

8. Bian Xiuwu, Zhang Peipei, Ping Yifang, Yao Xiaohong. Next-generation diagnostic pathology. Chinese Journal of Pathology, 2022, 51(1): 3-6.

9、Cell 2018;175(2):313-326

10、Nature Cancer 2021; 2: 794-802

11、Pallua J D, Brunner A, Zelger B, et al. The future of pathology is digital[J]. Pathology-Research and Practice, 2020, 216(9): 153040.

12、Metter D M, Colgan T J, Leung S T, et al. Trends in the US and Canadian pathologist workforces from 2007 to 2017[J]. JAMA network open, 2019, 2(5): e194337-e194337.

13、Campanella G, Hanna M G, Geneslaw L, et al. Clinical-grade computational pathology using weakly supervised deep learning on whole slide images[J]. Nature medicine, 2019, 25(8): 1301- 1309.