VCs May Be Struggling More Than Biotechs in the Downturn, Warns Atlas Venture

Atlas Venture

Early-Stage Venture Capital Firms

This year has been a bumper year for multinational corporations (MNCs): record-breaking market capitalizations, the emergence of new blockbuster drugs, surging product sales, continued expansion of indications, and promising sales prospects... As of October 2023, 15 MNCs held available cash reserves exceeding $20 billion, with Roche, Merck, Novo Nordisk, and Novartis each boasting available funds in excess of $60 billion.

However, boom years for financing and M&A rarely coincide; the resurgence of the M&A and BD markets signals a downturn in the financing and IPO sectors.Atlas Venture Recently Released Its Latest Annual Report, with Data Indicating That While MNCs Are Enjoying the Thrill of Bottom-Fishing, U.S. Biopharma VCs Are Facing Tough Times.

MNCs Have a Voracious Appetite

MNCs Hold Significant Capital, Fueling a Surge in Global M&A Activity: 18 Publicly Disclosed Deals Exceeding $1 Billion Have Been Completed, Marking the Highest Level Since 2019.

According to estimates by Atlas Venture, a prominent U.S. venture capital firm in the biopharmaceutical sector, the total value of biopharmaceutical M&A transactions this year is projected to range from $15 billion to $20 billion. Given the substantial cash reserves held by multinational corporations (MNCs), the M&A boom is expected to continue into next year.

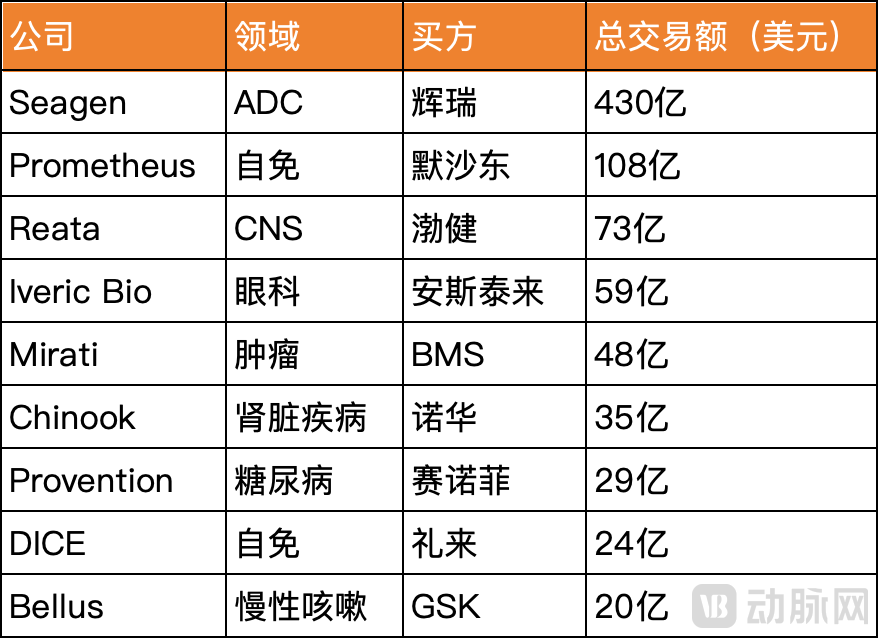

Nine Major M&A Deals in the Public Market in 2023 (as of November 2023)

M&A activity involving non-listed companies has also drawn significant attention this year. For instance, Roche acquired Telavant, a subsidiary jointly established by Pfizer and Roivant, for $7.1 billion to strengthen its position in inflammatory bowel disease. Takeda reached a $6 billion deal with Nimbus to acquire a potential best-in-class TYK2 inhibitor, a drug developed using Schrödinger’s physics-based computational platform, reflecting the trend of large pharmaceutical companies “following the science.” Additionally, Eli Lilly spent over $1.9 billion to acquire Versanis Bio, an innovative company focused on cardiometabolic diseases, further bolstering its weight-loss drug portfolio.

These transactions and their underlying motivations point the way for the future development of the biopharmaceutical industry.M&A activities help facilitate more efficient allocation of scarce resources across the industry:It enables promising projects from startups to reach the broadest global patient population in the shortest possible time, thereby unlocking significant capital that can be recycled back into the biopharmaceutical ecosystem, while also expanding the scale and overall liquidity of the talent market.

Biopharma VC May Face a Survival Crisis Akin to That of 20 Years Ago

Unlike the M&A market, the theme for the biotech financing market this year may well have been “waiting for recovery,” yet neither the primary nor the secondary market delivered satisfactory performance by year-end.

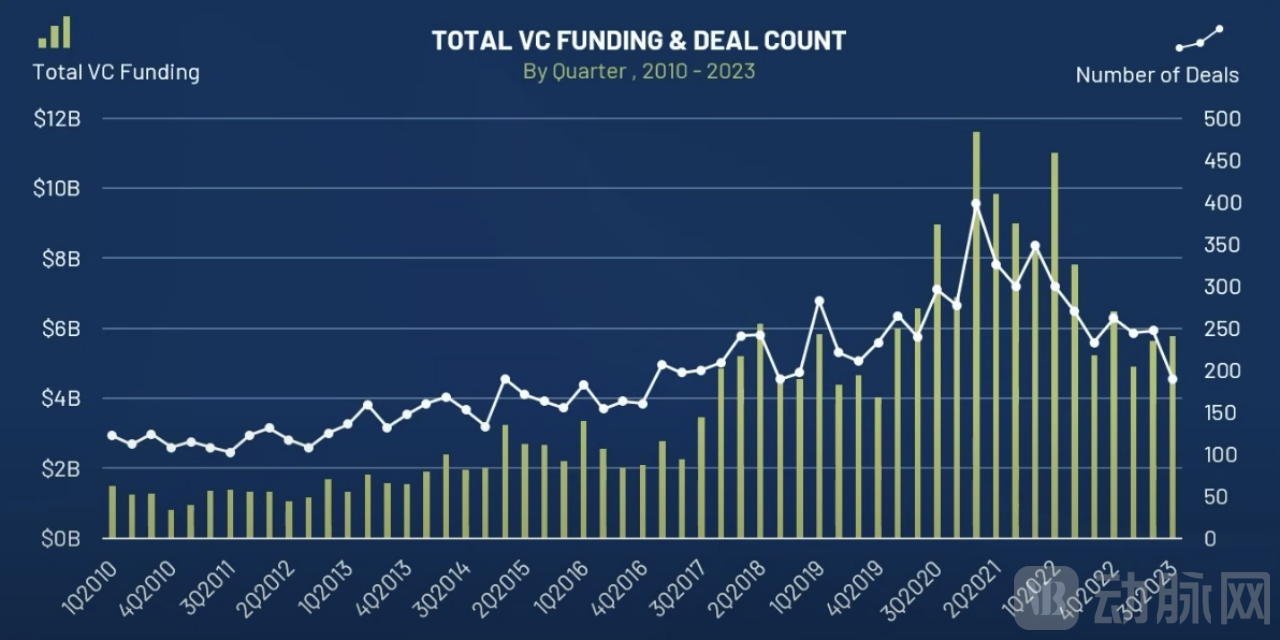

Atlas Venture believes that, from the venture capital (VC) perspective, this represents a “mean reversion.” Although VC funding in the U.S. biopharmaceutical market has declined significantly compared to 2021, it has stabilized at approximately $6 billion overall, a level comparable to pre-pandemic figures. This indicates that venture capital for the biopharmaceutical sector remains abundant.

Changes in U.S. Biopharma VC Funding Amount and Deal Count from 2020 to Q3 2023, Source: Atlas Venture

Atlas Venture stated, “Core biopharma VCs remain highly active; it is the generalist VCs spanning multiple sectors that are exiting. Although the number of biotech companies securing their first round of financing has dropped significantly, large-scale funding deals exceeding $100 million have remained stable at 15 to 20 per quarter.”

Major financing deals this year have been concentrated primarily in cell and gene therapy (CGT) and AI/computer-aided drug discovery, demonstrating a distinct frontier orientation compared to M&A transactions involving multinational corporations (MNCs). Venture capital continues to play its intended role.

Major Financing Rounds Exceeding $200 Million in the U.S. Biopharmaceutical Sector in 2023 (as of October 2023)

However, the exit landscape for venture capital firms in the biopharmaceutical sector remains bleak. Year-to-date, only 11 biotech companies have successfully completed initial public offerings (IPOs) on U.S. stock exchanges (excluding reverse mergers), compared with 74 and 85 in 2020 and 2021, respectively.

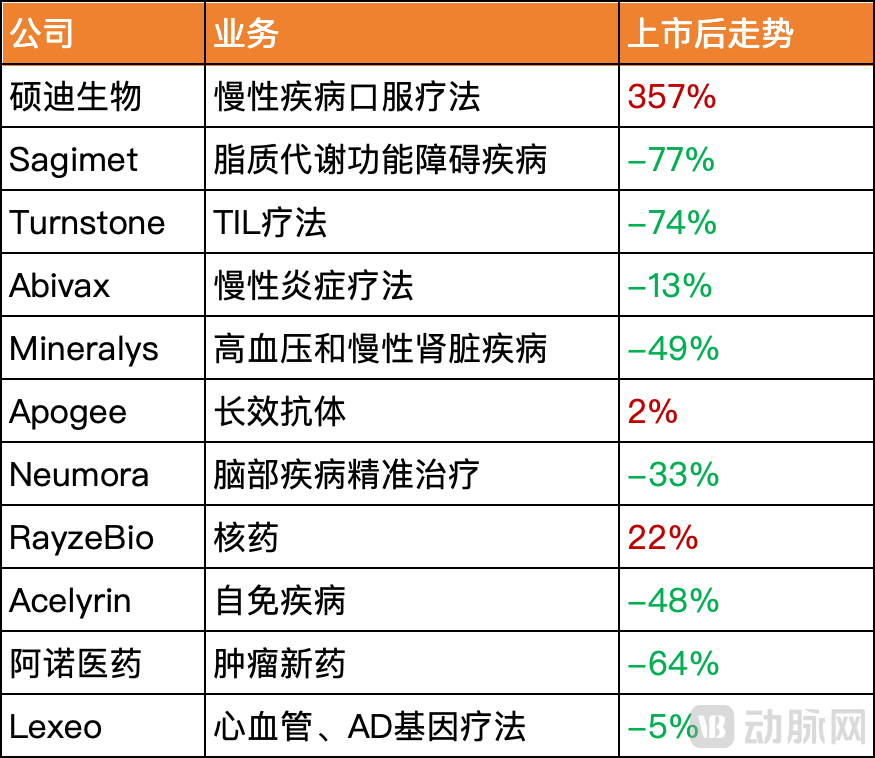

Biotech Companies Listed on U.S. Stock Exchanges in 2023 (Market Capitalization as of November 6, 2023)

Of these 11 companies that went public, all have underperformed except for Shuodi Biologics, which delivered impressive clinical results for its GLP-1R drug, and RayzeBio, which has benefited from the surge in interest in radiopharmaceuticals. This trend is also linked to the broader cooling of biotech stocks in the U.S. market. In a high-interest-rate environment, the most devastating impact on unprofitable biotech firms is the increased cost of capital, leading investors to demand higher returns or more stable profitability when allocating assets. According to data from Atlas Venture, the biotech sector has experienced severe capital outflows this year, exceeding those seen after the 2008 financial crisis and the burst of the biotech bubble in 2016.

As of October 20, while the Nasdaq Composite Index rose 25% year-to-date, the XBI, a major biotech index, declined approximately 18% over the same period.Most biotech companies selected by the XBI have not yet matured their business operations and exhibit high volatility; the industry generally considers the index to be representative of the performance of typical small- and mid-cap biotech stocks.

A report released by Stifel in November also highlighted the severe challenges facing the XBI, with a growing number of biotech companies having market capitalizations below their cash balances. The report stated, “We are uncertain whether we have ever witnessed a worse scenario… The XBI has declined 70% from its peak levels, and there appears to be no sign of improvement.”

Atlas Venture draws parallels between the current situation and the 2003 U.S. biotech crisis, noting numerous similarities between the two periods:Public markets have nearly bottomed out, venture capital investment has plummeted precipitously, IPO channels are virtually closed, and mergers and acquisitions are prevalent. Platform-based companies have fallen out of favor as the industry returns to product-centric logic, with the entire sector needing to confront challenges related to drug pricing and pharmaceutical regulations.

To this day, some still argue that 2003 marked the worst period in the history of the U.S. biotech sector: the biotech market endured seven years of stagnation and sluggishness until a new wave of technological innovation emerged in the early 2010s.

Atlas Venture believes that the current environment is perilous for biopharmaceutical venture capital firms, as many such VC firms in the United States disappeared during the previous difficult period: of the 12 VC firms with the largest biopharmaceutical funds in 2003, only MPM Capital and Versant Ventures survived.

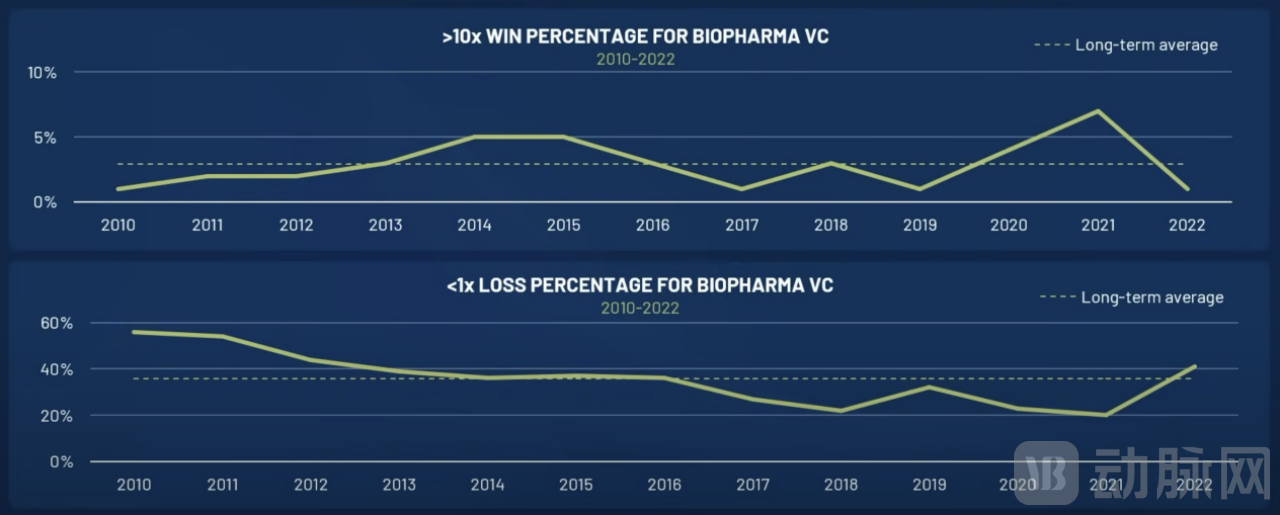

Today, biomedical venture capital (VC) is also facing the challenge of “industry consolidation.” Signs of this trend are evident in the U.S. biomedical VC return data presented by Atlas Venture: the proportion of star projects delivering returns of more than 10x hit a historic low in 2022, while the rate of principal loss rose to over 40%.

Source: Atlas Venture

Strategic Shifts Among Top Biopharma VCs

When a survival crisis looms, safe-haven assets become more attractive. Over the past two years, venture capital in the biopharmaceutical sector has shifted away from chasing conceptual hype, instead focusing on overall market size and commercial viability. There is now greater emphasis on product validation, innovation with clear certainty, and predictable revenue streams.

This is evident from the shifts in Atlas Venture’s investment strategy. With an active portfolio of over 160 companies, Atlas Venture has achieved 39 IPOs and 32 M&A exits, and its portfolio companies have developed more than 25 marketed drugs to date. Representative investments include leading companies in niche frontier fields that have drawn widespread discussion this year, such as Intellia, Nimbus, Akero, and Versanis. Furthermore, Atlas Venture’s incubator has helped 70 early-stage biotech startups get off the ground.

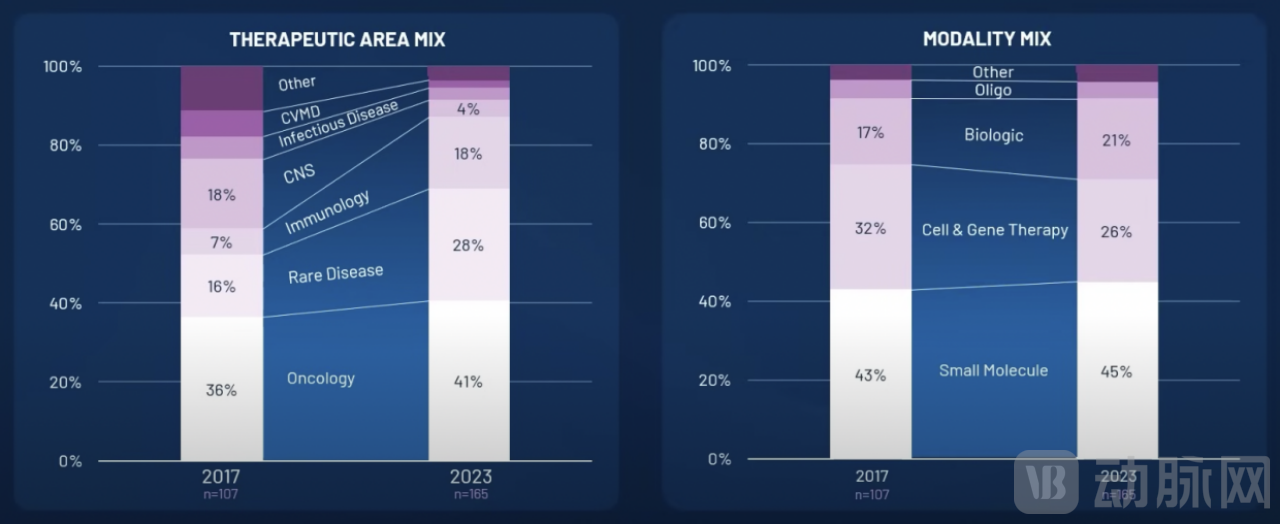

As a biomedical venture capital firm with such a distinctively innovative style, it has higher expectations for certainty in its investments.Comparing Atlas Venture’s investment portfolio in 2017 and 2023, the allocation across disease areas saw oncology, rare diseases, and autoimmune disorders increase from 36%, 16%, and 7% to 41%, 28%, and 18%, respectively, while allocations in CNS, infectious diseases, and other fields declined significantly. In terms of therapeutic modalities, the allocation for small-molecule drugs rose from 43% to 45%, whereas the more cutting-edge cell and gene therapy (CGT) segment decreased from 32% to 26%.

Changes in Atlas Venture’s Portfolio from 2017 to 2022

From the perspective of pipeline progress, the number of early discovery and preclinical projects held by companies invested in by Atlas Venture has decreased significantly compared to 2017. More pipelines have entered Phase I, Phase II, or even later-stage clinical trials, and there is an increasing trend of advancing pipelines in collaboration with external partners.

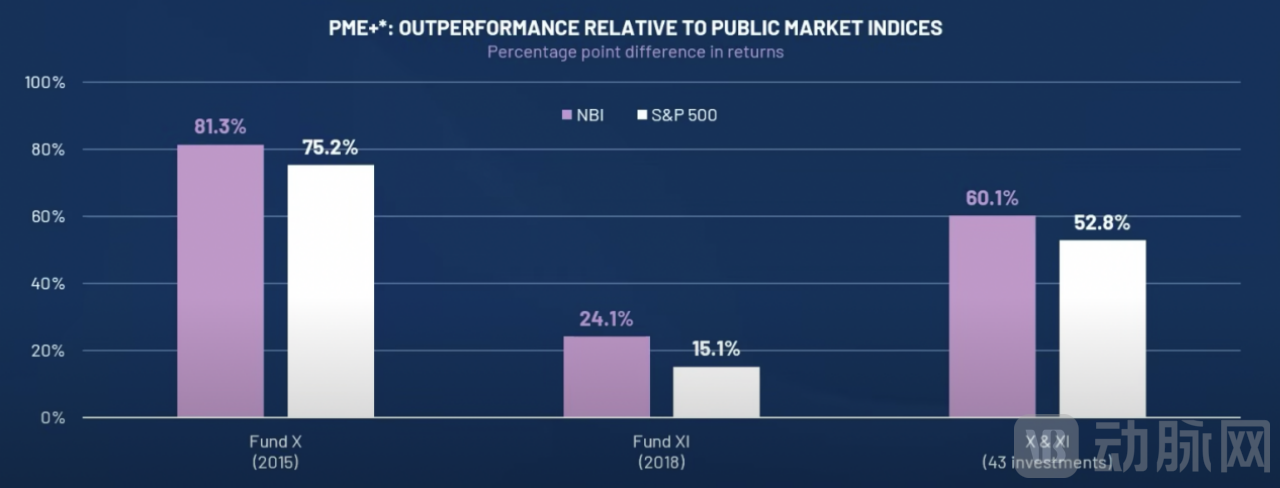

Atlas Venture remains one of the most prominent biopharmaceutical venture capital firms. Measured by PME (Public Market Equivalent), as of June this year, its two most recent funds have outperformed the NBI (Nasdaq Biotechnology Index) and the S&P 500 by 60.1% and 52.8%, respectively. However, its latest Fund XI, raised in 2018, has indeed underperformed.

Performance of Atlas Venture’s Two Most Recent Funds

The operating environment and business models of biotech companies have experienced a roller-coaster ride over the past three years. Since the beginning of this year, layoffs in the biotech industry have been announced one after another, with some companies even filing for bankruptcy and liquidation directly following clinical trial failures.

Even star companies backed by top-tier venture capital firms struggle to withstand market cycles without robust product support. For instance, several biotech companies invested in and incubated by Flagship Pioneering have collapsed this year, including the red blood cell therapy company Rubius, the exosome therapy company Codiak, and the microbiome therapy company Evelo. Each of these was a benchmark company in its field, and their demise suggests that exploration in their respective niche sectors may enter a period of temporary stagnation. This has also led to growing skepticism about whether Flagship’s model is “losing its efficacy.”

Some secondary market investors have stated that the probability of bankruptcy among companies in the XBI is too high, and they prefer to allocate the majority of their capital to large pharmaceutical companies rather than pursuing high-potential U.S. biotech targets.

The path forward for biotech companies has narrowed, and even more concerning is that some biomedical venture capital firms may have fewer options than the biotechs themselves. Nevertheless, Atlas Venture believes that the current situation is somewhat more optimistic than the darkest period for the biomedical sector around 2003:

The overall scale of the private equity market has expanded; the growing number of successful large- and mid-cap biotech companies is attracting generalist investors; research achievements with translational potential continue to emerge; the industrial structure is conducive to external innovation; and limited partners (LPs) are adopting a more long-term perspective.

The biting cold persists, yet biopharma venture capital firms and biotech companies continue to bear the high expectations of the industry, even in an era marked by a decline in the number of new drug products and increasingly prolonged R&D cycles.