Chinese Innovative Drug Exports Surge Over 10-Fold in Six Months as Global Pharma Giants Ramp Up Acquisitions

DualityBio

Innovative Molecular Type Drug Developer

Frequent cross-border licensing deals have become one of the hottest topics in China’s pharmaceutical venture capital circle. Their surge in popularity has even alleviated some of the psychological strain plaguing domestic biotech companies.

Just three weeks into November, four such deals have already been announced, with a cumulative value approaching $15 billion. Among them are transactions involving the currently hottest GLP-1 drugs and CAR-T therapies, as multinational giants such as AstraZeneca and Novartis engage in aggressive acquisition sprees, bringing many previously low-profile domestic biotech companies into the spotlight. Substantial upfront payments, promising future milestone payments, and the leap in status associated with competing in the global innovative drug market have made Chinese-made innovative drugs appear to be on the rise once again.

However, amid the constantly refreshed transaction amounts and frequency of cross-border licensing deals for drug pipelines, the fortunes of domestic biotech firms vary widely. Some have simultaneously secured offers from multiple multinational pharmaceutical companies, choosing between favorable and even more favorable commercial terms, while others, armed with less-than-impressive clinical data, shuttle among a handful of potential buyers, experiencing slow progress in their transactions.

The difficulty of cross-border licensing for drug pipelines is comparable to that of an IPO. So, whose hopes can this beam of light—cross-border pipeline licensing—ignite within the pharmaceutical venture capital sector?

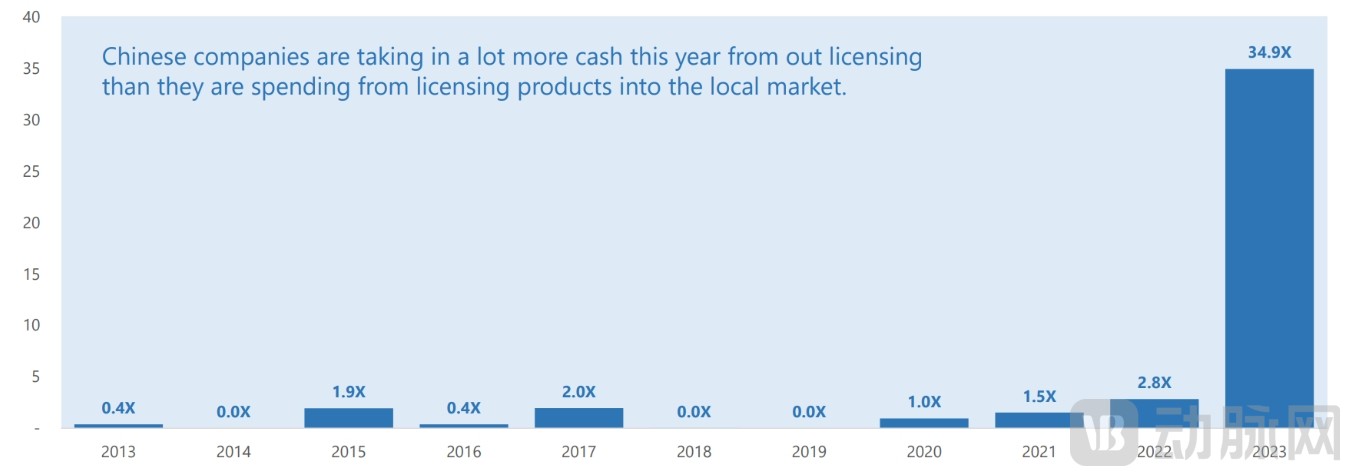

Data shows that in the first half of 2023, the proportion of upfront payments received and paid by domestic biotech companies in pipeline equity transactions surged from 2.8% to 34.9%, representing a more than tenfold increase. In other words, rather than spending capital to acquire pipelines, domestic biotech firms are increasingly licensing out their R&D pipelines to secure funding. The substantial financial commitments made by multinational pharmaceutical companies have undoubtedly instilled hope in new drug developers and provided a compelling reason for healthcare investors who were considering exiting to remain in the market.

DomesticBiotechProportion of upfront payments in pipeline equity transactions Data Source:Stifel

For biotech companies, securing funding enables the advancement of truly valuable product pipelines. Meanwhile, endorsement from major pharmaceutical firms serves as a ticket to compete on the global stage.

“Chinese biotech companies often lack experience in conducting clinical development overseas and therefore tend to opt for collaborative approaches,” Deng Liang, Partner at Huagai Capital’s Early-Stage Fund, told VCBeat. In reality, the value of out-licensing a pipeline extends beyond mere financial gain; it enables companies to partner with others for clinical trials and future commercialization when they are not yet capable of effectively penetrating overseas markets on their own. Typically, retaining rights for the Greater China region is sufficient for most domestic projects. At this stage, Chinese biotech firms generally do not possess enough resources or bandwidth to pursue global rights for new drug development. “If a product is sufficiently compelling, focusing development efforts on Greater China rights still holds significant potential and can complement overseas markets,” he added.

This trend is also evident in the brief history of innovative drug development in China. VCBeat’s review of past cross-border licensing deals reveals that domestic biotech companies that transfer rights to their core pipelines for co-development with multinational pharmaceutical firms not only gain significant recognition from capital markets but also realize the commercial value of their innovative products more rapidly.

A representative case is the previous round of collaboration between Legend Biotech and Johnson & Johnson. In December 2017, Legend Biotech entered into an exclusive global license and collaboration agreement with Janssen Biotech, a subsidiary of Johnson & Johnson, for the development and commercialization of the cell therapy ciltacabtagene autoleucel. More than four years later, in March 2022, the Biologics License Application (BLA) for ciltacabtagene autoleucel was officially approved by the FDA, making it the second BCMA-targeted CAR-T product globally. As a result, Legend Biotech successfully received upfront and milestone payments from Janssen Biotech, totaling $600 million. Just a few days ago, another multinational pharmaceutical company, Novartis, also extended an olive branch to Legend Biotech, with both parties reaching a new global licensing collaboration for cell therapies.

Compared to the biotech companies themselves, pharmaceutical investors may be even more excited. “From the perspective of early-stage investors in China, overseas licensing of drug pipelines, including the out-licensing of global rights to core product pipelines, is a positive development. It serves as a testament to a company’s strength and signifies that domestic biotech firms are further integrating into the international new drug R&D market,” pointed out Deng Liang.

First, at this stage, the maturity of domestic biotech companies remains relatively low; thus, gaining overseas recognition is, in essence, a significant advancement.Out-licensing ensures the immediate receipt of upfront payments, which can urgently address liquidity constraints during the R&D phase. More importantly, out-licensing core assets serves as an endorsement from multinational pharmaceutical companies in the eyes of capital markets. Although valuation perspectives on such collaborations may vary across different capital markets, overall, it facilitates higher valuations and advances IPO processes for innovative biotech startups.

Typically, following the completion of a business development (BD) deal, companies undergo repricing, with their market capitalization often jumping to a significantly higher tier compared to the previous financing round. In the capital markets, biotech firms such as Legend Biotech, RemeGen, and Kelun-Biotech have demonstrated strong stock performance after securing cross-border licensing deals for their core pipelines. For domestic biotech companies, such transactions serve primarily as a value-added catalyst.

“If capital markets had more patience and confidence to support these companies, many Phase I and Phase II clinical projects could advance further with adequate funding, potentially yielding greater returns. This is a matter of balance, which depends on each company’s development strategy at the time, but there is an equilibrium point,” Deng Liang further stated. Of course, choices often need to be made between financing and pipeline licensing, requiring comprehensive consideration of the company’s development strategy and the prevailing market environment.

Secondly, from a pure investment analysis perspective, pipeline licensing makes the revenue potential of products in development more tangible and the risks more controllable.Building on pipeline licensing deals, a basis for estimation has been established for a series of previously unknown data points, including future milestone payments, revenue sharing, and the potential market value of retained rights. In this process, while the overall value of the product pipeline may decrease, investment and development risks are significantly reduced.

“If there is no out-licensing, the product has significant market potential, but bearing all responsibilities in-house entails substantial risk,” said an investor. “Meanwhile, the company would need to secure additional funding, which is challenging for early-stage teams. Once the core pipeline is licensed out, a portion of the overseas market translates into royalty-based revenue. While overall returns may be somewhat lower, partnering with a reputable collaborator helps mitigate risk.”

Finally, amid increasingly constrained investment exit channels, out-licensing of pipeline assets has generated cash flow and revenue.In other cases, after the core pipeline is out-licensed, investment institutions may directly exit their equity stakes on a pro rata basis, or receive the upfront payment on a pro rata basis and share in future milestone payments. This serves as a viable exit strategy.

As early as the onset of the current wave of domestically developed innovative drugs in China, some startup biotech companies would sell their drug development molecules to generate cash flow.

At that time, multinational pharmaceutical companies paid little attention to drug molecules at early stages of development, and domestic buyers were reluctant to offer high prices. Such transactions failed to achieve scale, serving more as stopgap measures for corporate survival. However, current cross-border licensing of pipelines represents the process by which Chinese biotech firms integrate into the global pharmaceutical innovation ecosystem, a trend that will gain popularity in the future.

In the global pharmaceutical industry, achieving precise strategic positioning in unfamiliar disease areas and drug modalities through pipeline in-licensing has long become one of the core competencies of multinational pharmaceutical companies.

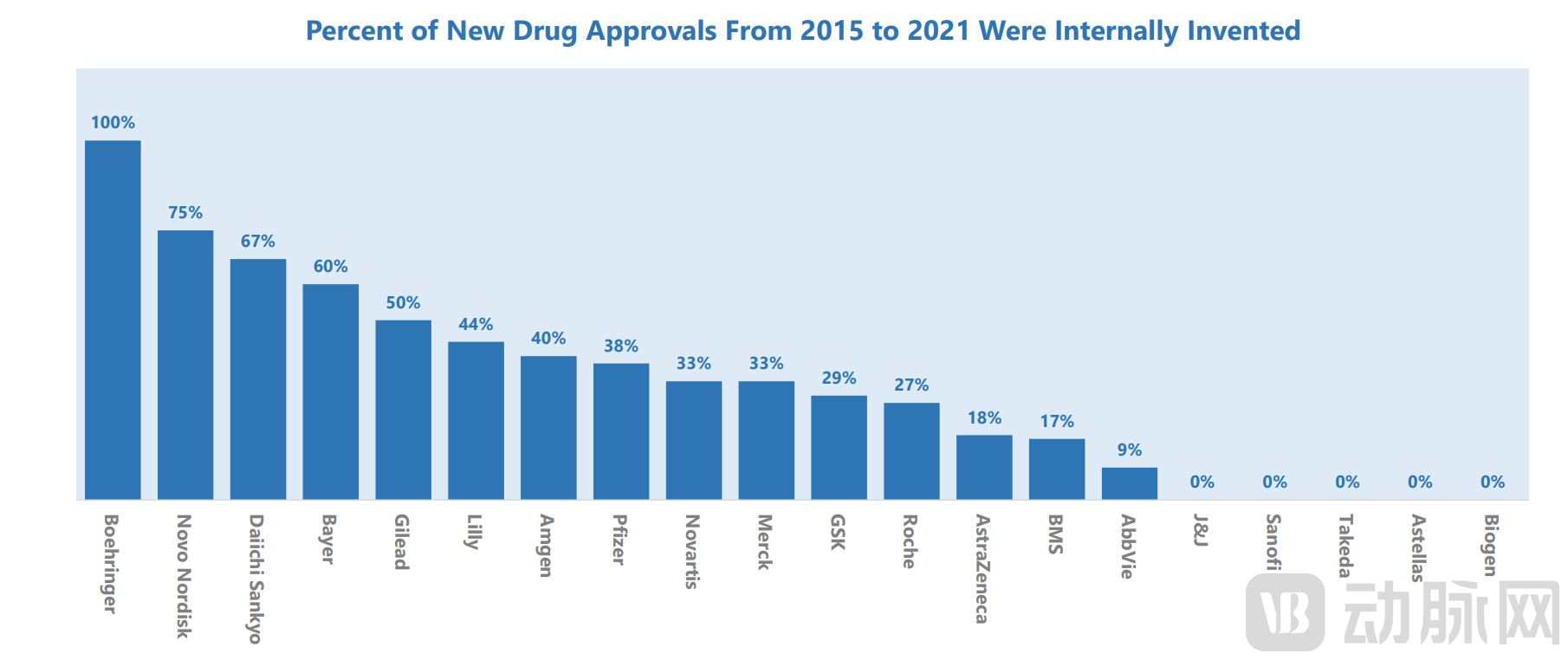

A significant proportion of innovative projects at multinational pharmaceutical companies are sourced from external in-licensing.Data shows that between 2015 and 2021, the FDA approved a total of 323 new drugs, 138 of which were applied for by the top 20 global biopharmaceutical companies. The majority (65%) of these new drugs originated from external pipeline acquisitions, including direct mergers and acquisitions as well as licensing agreements. During this period, with the exception of Boehringer Ingelheim, most multinational pharmaceutical companies did not obtain their approved drugs solely through internal R&D. Notably, Johnson & Johnson, Thermo Fisher Scientific, Takeda, Astellas, and Biogen had zero internal R&D contribution to their approved drugs during this timeframe.

2015Age2021over the years, globalTOP20Proportion of In-House New Drug Development in Pharmaceutical Companies Data Source:Stifel

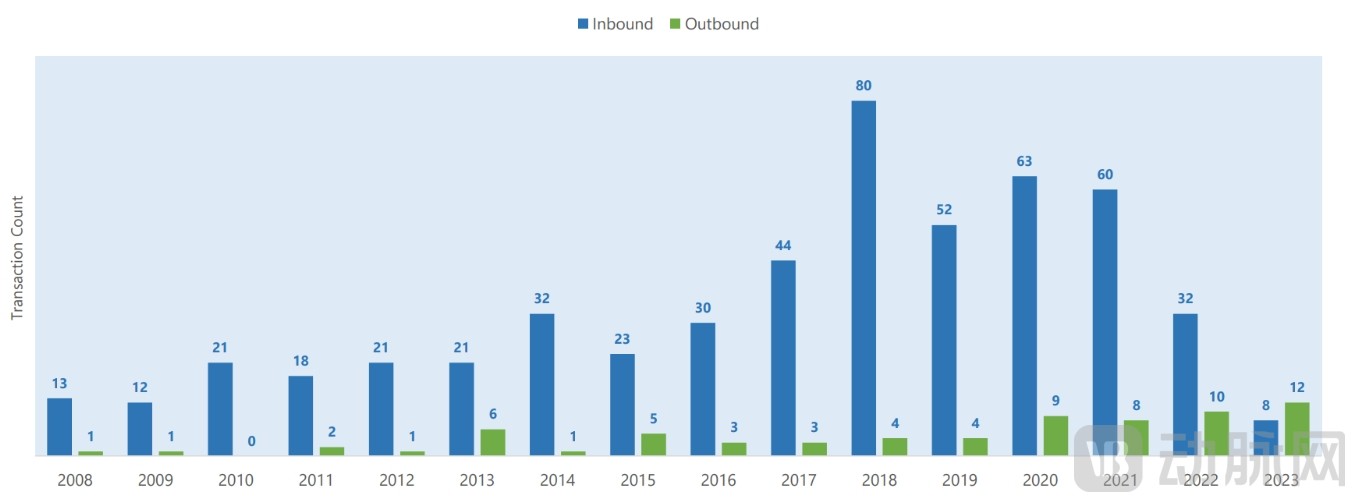

Amid the surge in cross-border licensing, the role of domestic biotech companies in the global pipeline rights market has undergone a reversal.In the first half of 2023, China became a net exporter of pharmaceutical innovation for the first time, with 12 asset out-licensing deals compared to 8 in-licensing deals.

2008Since [Year], Pipeline Licensing Deals of Domestic Enterprises Data Source:Stifel

Amid fierce competition in the global pharmaceutical market, multinational pharmaceutical companies need to continuously identify promising R&D pipelines to strengthen their product portfolios.Since 2023, Chinese biotech companies have completed dozens of cross-border licensing deals for their drug pipelines, with global pharmaceutical giants actively acquiring assets. Among these buyers, BioNTech and AstraZeneca have been the most active, though their strategic focuses differ. BioNTech has been aggressively expanding its global ADC (antibody-drug conjugate) portfolio and has targeted in-development pipelines from leading Chinese ADC developers. In contrast, AstraZeneca has focused on acquiring pipelines with strong global competitiveness in the metabolic disease sector.

“As far as I know, most multinational pharmaceutical companies do not specifically target projects for the Chinese market. After all, these acquisitions require substantial upfront investment and entail significant future development costs, so they naturally seek products with sufficient potential and quality,” said an investor. “In fact, prior to its collaboration with Legend Biotech, Johnson & Johnson had representative licensing deals in China. In most cases, cooperation was reached because both parties were optimistic about the product’s prospects during negotiations.”

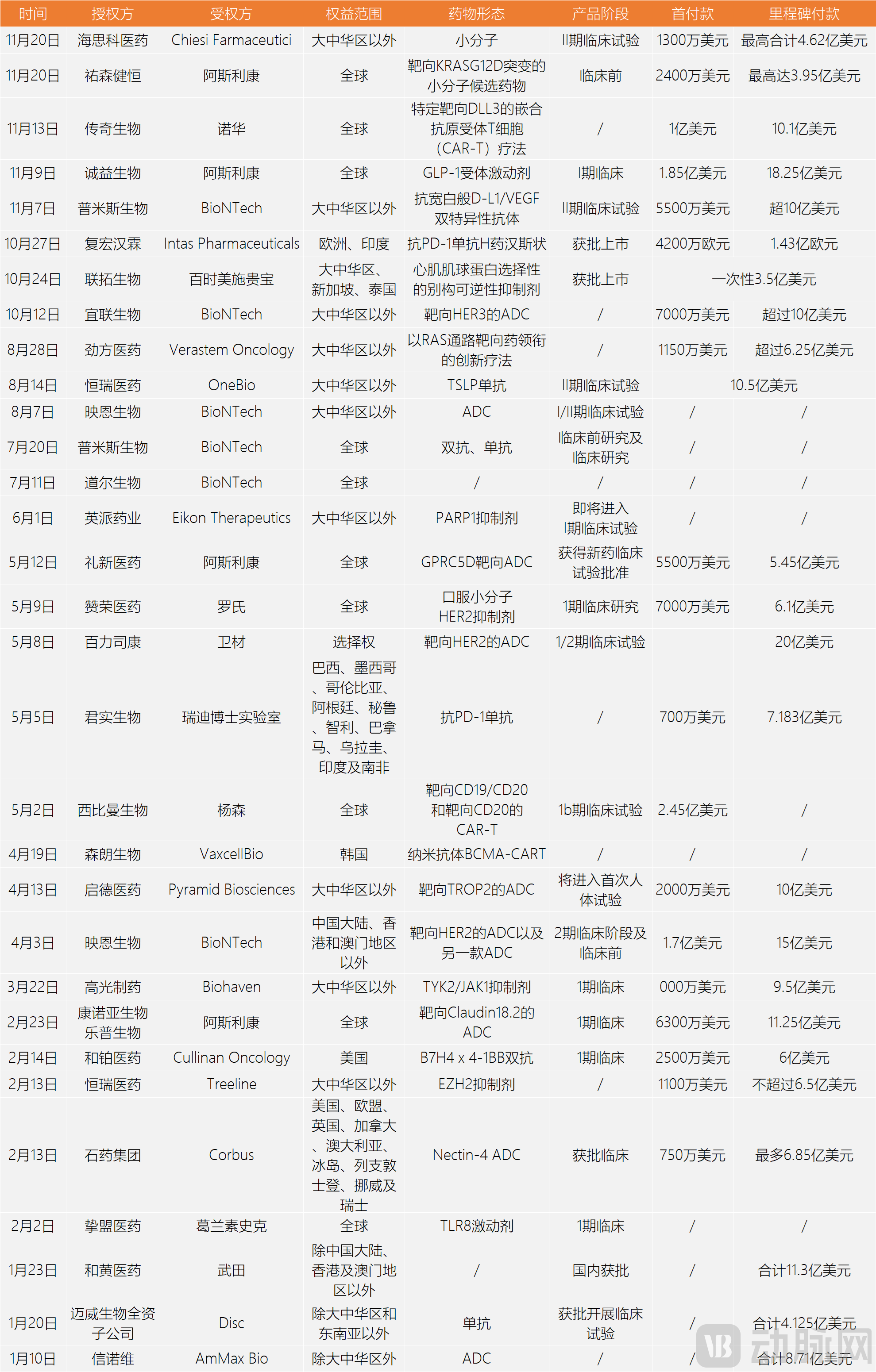

2023Cross-border licensing deals for select pipelines since [year] Data Source: VBOrange Database

Based on overseas licensing deals involving drug pipelines since 2023, biotech companies that have proactively positioned themselves in cutting-edge medical technologies—such as antibody-drug conjugates (ADCs), GLP-1 receptor agonists, cell therapies, and bispecific antibodies—have demonstrated the capability to deliver valuable R&D pipelines to multinational pharmaceutical companies, which in turn have offered substantial consideration. For instance, among the numerous ADC development programs, DualityBio targeted HER2 and was among the first to initiate overseas clinical trials, making its asset a scarce offering in its class. BioNTech secured the rights with an upfront payment of $170 million plus potential milestone payments totaling $1.5 billion, ranking this deal fourth among global licensing transactions in the first half of the year.

For multinational pharmaceutical companies, factors such as the drug modality, indication selection, and clinical strategy of candidates in the development pipeline are all considered during in-licensing evaluations.“Multinational pharmaceutical companies show high activity in pipeline evaluation, but they are highly selective,” said an industry practitioner. “They need to screen the most suitable candidates from a vast pool of pipelines.” In fact, as an important source of innovative products, the upfront payment for in-licensing pipelines is secondary; the key lies in the subsequent clinical development costs and timelines. It takes several years and substantial clinical investment to advance a product, making it difficult for multinational pharmaceutical companies to change course. If the acquired pipeline proves suboptimal, pursuing another acquisition later may result in missing the critical time window.

However, the decision-making costs for cross-border pipeline transactions are substantial. A single deal often determines the R&D direction of a multinational pharmaceutical company for years to come and involves investments amounting to billions of dollars. Consequently, multinational pharmaceutical companies emphasize making judgments based on preclinical pharmacokinetic (PK) results and Phase I clinical study data; nevertheless, future development potential remains difficult to predict. The greater challenge lies in the fact that if one waits repeatedly until there is sufficient information to support a low-risk decision, high-quality pipelines will likely have already been acquired by competitors. Multinational pharmaceutical companies face a difficult trade-off between efficiency and effectiveness.

This brings to light another undeniable reality: very few domestic biotech companies can achieve a leap in status through cross-border licensing of their core pipelines. Taking the currently hot ADC drug licensing market as an example, although there are over a hundred domestic ADC developers with extensive pipeline layouts, fewer than 10 of these pipelines have been integrated into the product portfolios of multinational pharmaceutical companies. The spotlight from multinational pharma ultimately illuminates only a select few domestic biotech firms.

For most biotech companies, value lies beyond pipeline deals.

The surge in cross-border licensing of drug pipelines is driven by the fact that, over the past eight to nine years, a cohort of innovative pharmaceutical companies founded by overseas-returning scientists has developed robust product portfolios with capital support. This phenomenon was absent in China’s pharmaceutical industry in earlier periods.

Nowadays, although domestic biotech companies are experiencing turbulence in the capital market, the industry’s maturation is undeniable. After years of accumulating talent and core products, signs of a harvest are beginning to emerge among Chinese biotech firms. In the future, the scope of cross-border licensing for drug pipelines is likely to expand increasingly. Rather than focusing solely on antibody-drug conjugates (ADCs), Chinese biotech companies will make their mark globally across diverse sectors, including small molecules, large molecules, ADCs, and small nucleic acids.

In this sense, rather than seeking cross-border licensing opportunities for their pipelines, domestic biotech companies should focus more on product development itself to compete globally, especially in a consistently upward-trending environment.

First, to advance global clinical trials more efficiently.Within the global R&D ecosystem, multinational pharmaceutical companies generally regard overseas Phase I clinical data as more credible and indicative of safety. Typically, assets entering licensing pipelines are not based on entirely novel targets; their druggability has already been validated, and certain safety trends have emerged. In such cases, multinational pharmaceutical companies are more inclined to engage during the Phase I clinical trial stage, which requires companies to conduct robust preclinical research and early-stage clinical trials.

Second, improve the quality of pipeline layout.In the pipeline licensing market, only those pipelines that biotech companies have not invested sufficient time and resources to develop properly may be selected for licensing. Once the global rights to the core pipeline are licensed out, the development potential of the candidate pipelines will determine the company’s future strategic direction. Beyond the core pipeline, prudent project initiation is essential for biotechs to maintain their competitiveness within the global pharmaceutical ecosystem and to maximize the value derived from pipeline licensing deals.

Third, and critically important, is that biotech companies must continuously strengthen their clinical capabilities, leveraging the cash flow and industrial resource endorsements generated from pipeline licensing.On the one hand, once a pipeline asset is out-licensed, its development strategy is determined by the multinational pharmaceutical company. If the biotech firm is dissatisfied with the partner’s performance, it may choose to reclaim the rights and develop the asset independently. On the other hand, for assets where partial rights are retained, the biotech company must align with the multinational pharmaceutical company’s pace to facilitate further development. This underscores that out-licensing a pipeline asset does not mark the end of a new drug’s development journey, but rather a new beginning, posing fresh challenges to the biotech company’s comprehensive capabilities.

The substantial capital from multinational pharmaceutical companies may only illuminate the future of a select few domestic biotech firms, but a continuously improving ecosystem for new drug development deserves greater patience.