Has the CXO Sector Hit Bottom? Is a Biopharma Rebound Imminent?

On December 4, WuXi Biologics significantly lowered its 2023 performance guidance, with projected revenue falling approximately $400 million short of the original target. The downward revision was primarily driven by declines in both drug development and manufacturing revenues.It also pointed out that, due to the slowdown in biotechnology financing, the CXO industry is expected to experience single-digit growth over the next two years.

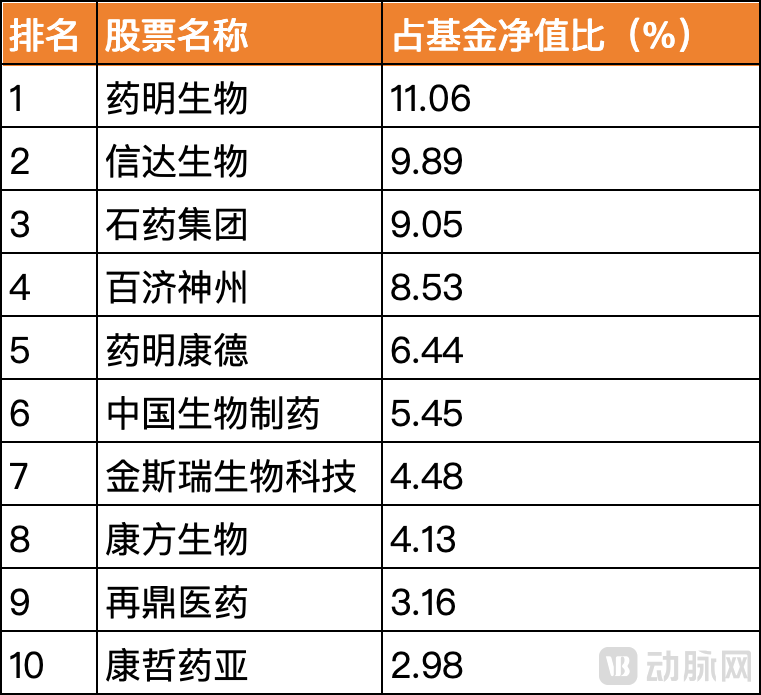

The cooling trend has become increasingly evident over the past year for both WuXi Biologics and the broader CXO sector. However, WuXi Biologics’ latest downward revision of its guidance, following WuXi AppTec’s earlier adjustment to its performance expectations, carries particular weight. As an industry leader, WuXi Biologics explicitly stated that the entire sector is entering a phase of slowed growth. This announcement sent shockwaves through Hong Kong-listed CXO companies and even the broader innovative drug segment, causing the Hang Seng Healthcare Innovation ETF to plunge nearly 7%.As of the third quarter of 2023, nearly half of the top ten holdings in the Hong Kong-listed Innovative Drug ETF were CXO companies, with WuXi Biologics alone accounting for over 10%. Therefore, the performance of the CXO sector also influences the performance of innovative drugs.

Top 10 Holdings of the Hong Kong-Listed Innovative Drug ETF as of Q3 2023

As the winter chill in the biopharmaceutical industry finally reaches the “water sellers,” has this latest downturn truly hit bottom?

Where Lies the Hope for WuXi Biologics?

WuXi Biologics’ performance is not particularly problematic if viewed in isolation from the rapid growth of the past two years: revenue increased by 10% in 2023, gross margin reached 40%, and full-year COVID-19-related income declined to 3%. China Merchants International forecasts that non-COVID-19 business revenue will achieve a 5% half-on-half sequential growth.

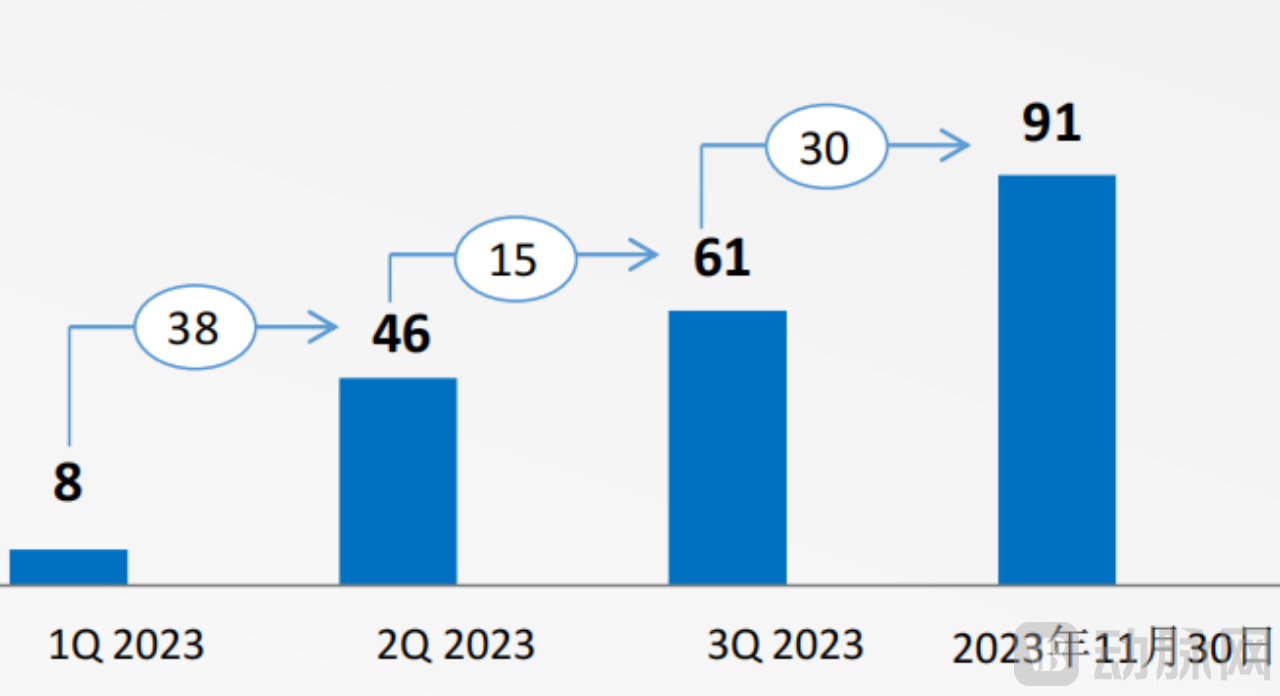

WuXi Biologics’ primary challenge this year has been a sharp decline in the number of projects. At a previous investor open day, the company disclosed that it had added 25 new CDMO projects in the first half of 2023 (before June 20), compared with 120 new CDMO projects added throughout the entire previous year.

However, with this business update, WuXi Biologics stated that the overall number of projects has actually shown a recovery since the second quarter of this year,As of November 2023, the number of newly added projects had reached 91, making this year poised to rank among the top three years for new project additions since WuXi Biologics’ listing (excluding COVID-19-related projects).

WuXi Biologics: Number of New Projects Added in 2023

WuXi Biologics: Number of New Projects Added in 2023

WuXi Biologics stated that this year’s growth was driven by: North America, as the primary engine of innovation, contributing approximately 55% of new projects; the number of new projects in China recovering to account for around 20%; and strong growth in antibody-drug conjugates (ADCs), which have gained significant market traction.

However, WuXi Biologics had also laid the groundwork in advance for a decline in net profit. The company stated that, while expectations for its drug discovery business and WuXi XDC remained unchanged, revenue from its drug development services was revised downward by 18%–20%, and revenue from its contract manufacturing organization (CMO) services was revised downward by 15%–18%. Net profit for 2023 is expected to decline by a single-digit percentage.

Growing pains are inevitable; however, WuXi Biologics has stated that it expects to achieve double-digit growth in both revenue and profit by 2024. China Merchants International forecasts the company’s revenue growth for 2024 to be in the range of 10–20%.Life will improve after 2025.Based on the comprehensive business updates and previous financial reports, several factors support an optimistic outlook for WuXi Biologics' growth:

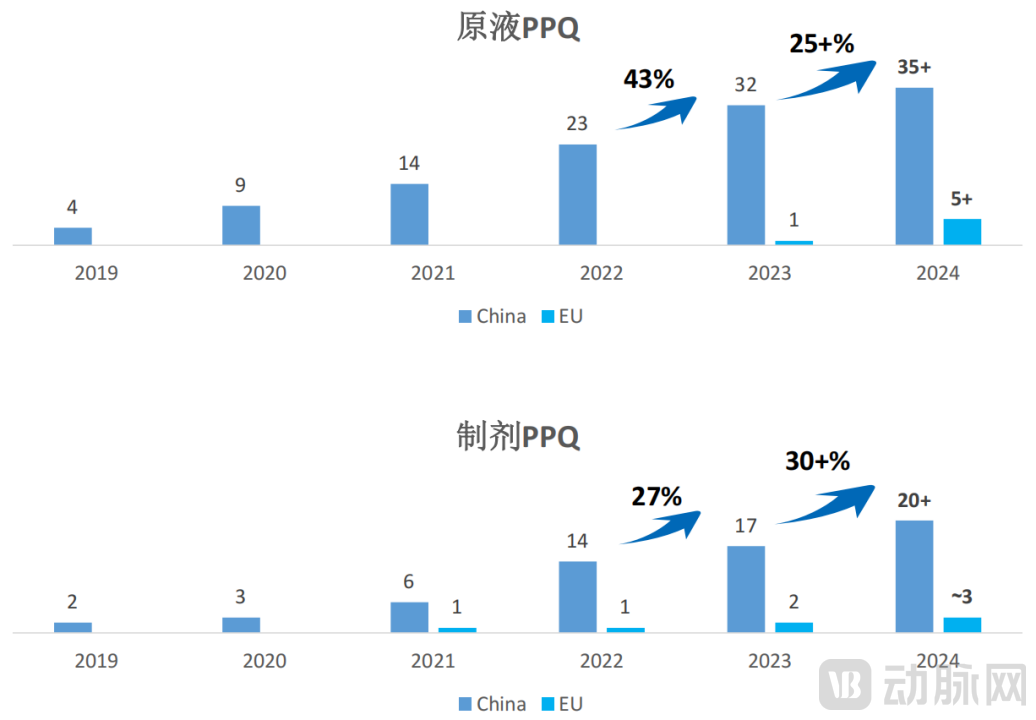

Robust growth in PPQ for drug substance and drug product,In parallel with the growth in CMO projects, more will be added in 2024. PPQ marks the transition of product processes from design and development to commercial manufacturing, laying a solid foundation for successful BLA submissions. WuXi Biologics has achieved a PPQ success rate of over 97%, ranking among the best in the industry.

WuXi Biologics' Leading Indicator: PPQ Batches Show Steady Growth

WuXi Biologics' Leading Indicator: PPQ Batches Show Steady Growth

WuXi Biologics’ average revenue from long-tail customers has risen year by year,This reflects deepening customer trust, while some early-stage customers are progressively advancing to later and commercialization stages, gradually evolving into more substantial revenue sources.

WuXi Biologics' production capacity will continue to increase,Production capacity will reach 588,000 liters by 2026. The Irish facility will commence commercial production next year. Capacity for 2025 is nearly fully booked, with 70% of projects secured through “Win-the-Molecule” strategies; these are all potential blockbuster drugs, the majority of which are already marketed products.

The company will launch 2-3 blockbuster biologic drug projects in 2025,Sales peaked at $2–3 billion.

In 2023, contracts worth $3 billion were signed.Milestones in drug discovery could reach $5 billion, setting a new historical high.

CXO 2023: Competing for a Shrinking Market

The revenue gap in the post-pandemic era and sluggish demand for CXO services are not challenges faced solely by WuXi Biologics or the WuXi AppTec group. Regarding downward revisions to performance expectations, Thermo Fisher Scientific lowered its annual profit forecast for the second consecutive quarter in Q2 and Q3 of this year. In terms of sluggish growth, Lonza reported a year-on-year revenue increase of 3.2% in the first half of this year, while its net profit declined by 17.5% year on year. As for declining revenue, Catalent’s total revenue for fiscal year 2023 fell by 11% year on year, with its net loss widening by 146% compared to the previous year.

The CXO sector is undergoing a downturn, with both peer revenues and upstream supplier revenues showing grim prospects. WuXi Biologics has pointed out that the industry is transitioning from the 15% growth rate seen in recent years to a phase of single-digit growth over the next two years.

Source: WuXi Biologics Business Update

Source: WuXi Biologics Business Update

On the other hand, the most obvious influencing factor is naturally the tightening of financing in the biotechnology industry.

According to statistics from SPDB Silicon Valley Bank, there were 188 financing transactions in China’s biopharmaceutical sector in the first half of 2023, compared with 842 and 604 for the full years of 2021 and 2022, respectively—a stark and visible decline.

The U.S. and European markets experienced a significant decline in both transaction volume and value in 2022. This was primarily due to the closure of IPO windows and weak post-listing performance of public companies, which exerted downward pressure on valuations in the primary market. Additionally, some large overseas late-stage funds slowed their pre-IPO investments, while certain transition funds suspended new investments in the healthcare sector.

In the secondary market, the U.S. biotech sector has experienced severe capital outflows this year, exceeding those seen after the 2008 financial crisis and the 2016 biotech bubble burst.

WuXi Biologics also disclosed that the launch of three blockbuster drugs from major pharmaceutical companies has been delayed in the second half of this year, impacting approximately $100 million in revenue. The number of new drugs approved by the FDA in recent years has not been small; a total of 37 were approved in 2022, and 52 have been approved so far this year through November. However, approval standards are becoming increasingly stringent, bringing greater uncertainty to the CXO business.

Another frequently discussed topic this year is the high-profile entry of CXO companies from South Korea, Japan, and even India into the race for market share. For instance, Samsung Biologics has publicly disclosed orders worth over $1.7 billion this year, with multinational corporations (MNCs) such as Bristol Myers Squibb (BMS), Novartis, and Pfizer placing substantial consecutive orders.

India’s four largest CDMOs—Syngene, Aragen Life Sciences, Piramal Pharma Solutions, and Sai Life Sciences—have all reported strong demand from European and American pharmaceutical companies this year, with Sai Life Sciences noting that its sales have grown by 25% to 30% in recent years.

Nevertheless, WuXi Biologics’ industry position remains secure. Its years of mature management systems and the engineer dividend that cannot be surpassed in the short term have enabled its market share to continue rising.

In terms of sales revenue, WuXi Biologics’ global market share increased from 2.4% in 2017 to 12.8% in 2022. Although no specific figures were provided in this business update, WuXi Biologics clearly stated:Against the backdrop of a significant contraction in the global market in 2023, the company’s market share continued to rise.

“Squat a little longer”

As the biopharmaceutical industry first began to feel the chill, some investors and related companies flocked upstream. Since the prosperity of CXOs directly depends on demand from downstream pharmaceutical companies, orders for CXOs began to vanish rapidly as capital chose to cluster upstream in a “flight to safety.”

Thus, as the year drew to a close, the chill was transmitted back by the CXO sector. However, if CXOs are the last segment to enter a downturn, they are inevitably also a late-cycle segment that recovers later. Sustained activity in the innovative drug sector is required before the positive effects can further translate into financial performance.

As the lagging CXO sector also hits bottom, is a rebound in biopharma truly on the horizon?

From a funding perspective, as the Federal Reserve concludes its rate-hiking cycle and interest rates are poised to enter a downward trajectory, the most severe phase of the external environment may have already passed. Although venture capital (VC) funding in the U.S. biopharmaceutical market has declined significantly this year compared to 2021, it has overall stabilized at $6 billion, a level comparable to pre-pandemic figures. This indicates that VC funding for the biopharmaceutical sector remains ample.

This year remains challenging for pre-revenue biotech companies, but it has been a fruitful one for multinational corporations (MNCs) and biopharma or biotech firms with established scale and revenue-generating capabilities.

Globally, M&A capital from multinational corporations (MNCs) is flowing in abundantly. As of October 2023, 15 MNCs held over $20 billion in available cash on their balance sheets, with Roche, Merck, Novo Nordisk, and Novartis each boasting more than $60 billion. Among pharmaceutical companies listed on the Hong Kong Stock Exchange, many have reported profitable results, driven by enhanced differentiated competitive capabilities, significant progress in global expansion, and increased reimbursement rates under national medical insurance. These companies represent a crucial revenue source for contract research, development, and manufacturing organizations (CXOs).

Moreover, the CXO sector is not uniformly bleak; for instance, the supply-demand imbalance for GLP-1 drugs has driven growth in CDMO and upstream demand, while ADCs have entered a new round of capacity competition.

Investment firms such as Novo Holdings Ventures, under Novo Nordisk, recently stated that early-stage biopharmaceutical companies will outsource production orders as the financing environment stabilizes. Consequently, demand for clinical-stage CDMO services is expected to increase in 2024.

If, as WuXi Biologics claims, the first half of 2024 was the most challenging period and strong growth resumes after 2025, then the current strategy is to hold position a little longer and wait for the takeoff.