Fall of Star Microbiome Firms: Does Microbial Pharma Have a Future?

Seres Therapeutics

Novel Drug Developer

Evelo Biosciences

Clinical-stage biopharmaceutical R&D company

4D Pharma

Biological Product R&D Developer

Finch Therapeutics

Developer of Novel Microbial Therapy Technologies

Kaleido BioSciences

Innovative Drug Developer

Successful business stories are naturally gratifying. Yet the logic behind the rise and fall of once-dominant enterprises is even more worth pondering.

Compared with traditional pharmaceuticals, microbial therapeutics differ significantly throughout the entire process, from early-stage development and clinical trials to commercial application. Gut microbiota have long been considered as a late-stage therapeutic option for certain diseases. Previously, the FDA had allowed fecal microbiota transplantation (FMT) to be performed without approval under a unique “enforcement discretion” policy.

The turning point came in 2012, when the FDA established a new product category, Live Biotherapeutic Products (LBPs), for the approval of microbial drugs. This sparked a surge in the development and investment of microbial therapeutics. In 2022, the world’s first microbial drug was approved for market launch. By the end of 2023, three microbial drugs had been approved globally.

However, the major retreat of star pharmaceutical companies also occurred around 2022, just as the industry began to see a glimmer of hope. Layoffs, delistings, return of partnered pipelines, and even direct dissolution of teams took place. The prospects for microbiome-based drug development seemed clouded with uncertainty. In this article, we attempt to identify the risk factors most likely to undermine microbiome pharmaceutical companies, enabling those still fighting on the front lines of microbial drug development to avoid them as much as possible.

If time were to turn back, the signs of retreat among star companies in the microbiome pharmaceutical sector would have emerged as early as 2019. In 2019, when global capital made significant inroads into the field, Seres Therapeutics, a leading microbiome therapeutics company, laid off 30% of its workforce to refocus on advancing the clinical development of its core pipeline. Subsequently, as an increasing number of drug candidates entered the mid-to-late stages of clinical trials, operational risks for microbiome pharmaceutical companies grew even greater.

In fact, a brief review of the R&D investment and clinical achievements of microbiome pharmaceutical companies in distress over the past few years reveals that the reasons behind the difficulties in advancing clinical trials are often quite disheartening.

On the one hand, as startups developing innovative biotechnologies, microbiome pharmaceutical companies lack experience in clinical trial strategies and require a relatively lenient environment for trial and error, leveraging failures to pave the way for potential success.Evelo Biosciences, which dissolved its entire workforce in late November, serves as a typical cautionary tale. External interpretations attribute the company’s collapse and subsequent dissolution to the successive clinical trial failures of its core in-house pipelines—EDP1867, EDP1815, and EDP2393—suggesting it could no longer sustain operations. However, until the very end, EDP1815 continued to demonstrate excellent safety and efficacy data in the treatment of psoriasis, and the long-term data for EDP2393 outperformed the control group. In a sense, Evelo’s critical error lay in allocating its limited liquidity to the wrong indications.

On November 20, Evelo’s board of directors filed its dissolution plan with the U.S. Securities and Exchange Commission, bringing an end to nearly a decade of operations. Established in 2014 under the incubation of Flagship Pioneering, Evelo focused on developing oral microbiome therapeutics for immune-mediated diseases, utilizing drug formulations composed of single microbial strains to upregulate or downregulate immune pathway functions. In 2018, Evelo went public on the Nasdaq, raising $85 million and achieving a market capitalization that once reached $2 billion. Prior to its IPO, top-tier institutions and corporations such as Mayo Clinic, GV, and Celgene participated in its funding rounds, establishing Evelo as a prominent star enterprise in the microbiome pharmaceutical sector.

The first candidate abandoned by Evelo was EDP1867. In April 2022, the Phase I clinical trial of EDP1867 for the treatment of atopic dermatitis was declared a failure. Among the 15 patients who received low-dose EDP1867, there was no clear evidence of benefit after 8 weeks, leading to the suspension of EDP1867.

As Evelo concentrated its efforts on developing EDP1815 and EDP2393, its strategy gradually went astray. The most widespread perception of EDP1815 in the external community is that it demonstrated lower efficacy than placebo in treating atopic dermatitis. In February this year, the Phase II clinical trial of EDP1815 for atopic dermatitis failed to meet its primary endpoint. According to the trial results, the EASI-50 response rate (defined as a 50% improvement in the Eczema Area and Severity Index score) in the control group (placebo group) was 56%, whereas in the EDP1815 group, only 41%, 38%, and 32% of patients in Cohorts 1, 2, and 3, respectively, achieved an EASI-50 or greater response at Week 16, indicating inferior efficacy compared to placebo.

At the time, Evelo attributed the issue to an overly potent placebo effect. Unfortunately, upon re-examination of the clinical trial data released in April 2023, EDP1815 still failed to outperform the placebo. In Cohort 4, 37.9% of patients in the EDP1815 group achieved an EASI-50 or greater response at Week 16, compared with 44.7% in the placebo group.

Interestingly, EDP1815 had already demonstrated promising results in an earlier Phase II trial for psoriasis. According to Evelo’s plan, the company intended to advance the development of EDP1815 to broadly treat patients with mild-to-moderate psoriasis who have limited therapeutic options. However, for reasons unclear, Evelo did not concentrate its efforts on conducting a Phase III clinical trial of EDP1815 for psoriasis. In the field of psoriasis, Evelo has actually placed its bets on EDP2393. This March, Evelo received a delisting warning from Nasdaq. At that time, Dr. Simba Gill, CEO of Evelo, stated that the company would focus its resources on the development of EDP2939, the first candidate drug based on its next-generation extracellular vesicle platform.

Unfortunately, the Phase II clinical trial data for EDP2939 in the treatment of psoriasis, released in October, remained suboptimal. The study’s primary endpoint—the difference in the proportion of patients achieving a 50% improvement from baseline in the Psoriasis Area and Severity Index (PASI-50 response) between EDP2939 and placebo after 16 weeks of daily treatment—was not met. Notably, however, this proportion shifted from being lower than that of the placebo group at Week 16 (19.6% in the EDP2939 group vs. 25% in the placebo group) to surpassing the placebo group by the Week 20 follow-up (33.9% in the EDP2939 group vs. 26.9% in the placebo group). In other words, the clinical trial failure of EDP2939 might have been avoided had the study design been more appropriately structured.

At this point, Evelo attempted to change course, preparing to abandon EDP2939 and refocus on EDP1815. Dr. Simba Gill stated, “Although we are disappointed with the Phase II results for EDP2939, we remain confident in the value of our Small Intestine Axis (SINTAX) platform and our potential product, EDP1815. We previously reported positive efficacy and safety data from a Phase 2 study of EDP1815 in patients with mild-to-moderate psoriasis. In light of these results, we will discontinue the development of EDP2939 and are reviewing potential strategic alternatives, including seeking partnerships for EDP1815 and the SINTAX platform.”

During the heyday of innovative drug financing and investment, strategic failures were not necessarily fatal as long as there was sufficient data to support clinical value. Today’s clinical trials, however, carry a certain air of all-or-nothing gamble. Previously, Evelo attempted to alleviate financial pressure through layoffs. In January 2023, Evelo laid off 45% of its workforce, with further reductions in the second quarter. However, for innovative pharmaceutical companies, cost-cutting measures are too little, too late.

On the other hand, during the clinical trial phase, which has the greatest capital requirements, two potential external financing channels tightened simultaneously, leaving microbiome pharmaceutical companies with no room for trial and error.In terms of equity financing, the total capital flowing into biotechnology has shrunk significantly. Data from BioWorld shows that global investment and financing in the innovative drug sector have cooled rapidly since 2020. In terms of total financing amount, global innovative drug companies raised a total of $60.8 billion in 2022, less than half of the $134.5 billion at the peak in 2020. Meanwhile, in the first half of 2023, the XBI index in the secondary market fell against the trend while the S&P 500 Index rose by 15.9%. During this period, a large number of biotech startups, including microbiome pharmaceutical companies, received delisting warnings.

In June 2022, another star enterprise in the microbial pharmaceutical industry, 4D Pharma, was delisted from the NASDAQ stock market. Public information indicates that 4D Pharma did not commit any major misconduct, and clinical trials of its products under development were progressing smoothly. Apart from financing difficulties, it is hard to identify other reasons for its decline. 4D Pharma is a global leader in the development of live biotherapeutic drugs, adhering to the same principle of using single bacterial strains administered orally to treat various diseases.

Data shows that 4D Pharma has simultaneously launched six clinical programs: a Phase I/II study of MRx0518 in combination with KEYTRUDA® (pembrolizumab) for the treatment of solid tumors; a Phase II clinical trial of MRx0518 in combination with BAVENCIO® (avelumab) as first-line maintenance therapy for urothelial carcinoma; a Phase I study of MRx0518 in the neoadjuvant setting for patients with solid tumors; a Phase I study of MRx0518 in patients with pancreatic cancer; and a Phase I/II study of MRx-4DP0004 for the treatment of asthma. This underscores the significant cash flow pressure the company faces.

Notably, in March 2022, just three months before its delisting, the company announced that its investigational microbiome-based therapy, MRx0518, in combination with the anti-PD-1 antibody Keytruda, had met the primary efficacy endpoint in a Phase 1/2 clinical trial for the treatment of renal cell carcinoma. However, given the significantly heightened investment decision thresholds in the current market, such clinical progress is clearly insufficient to attract adequate external funding.

For biotech startups, licensing deals are undoubtedly a significant source of funding. The early rise of microbial therapeutics was also driven by substantial investments from multinational pharmaceutical companies. However, in recent years, the enthusiasm of multinational pharmaceutical companies for microbial therapeutics has noticeably waned. According to Stifel’s statistics, the global pipeline licensing market maintained an M&A pace in 2023 that was nearly identical to the previous year; however, skin and gastrointestinal diseases—the key therapeutic areas targeted by microbial therapeutics companies—were not among the top three indications.

In fact, multinational pharmaceutical companies are no longer aggressive in their approach to microbiome-based drug development; instead, they have begun to retreat. In August 2022, after thoroughly reviewing its product strategy, Takeda Pharmaceutical decided to terminate its collaboration with Finch Therapeutics on FIN-524 and FIN-525. Shortly thereafter, Finch also halted the Phase III clinical trial of its core product, CP101, raising concerns about its ongoing business viability.

In August 2022, three months after initiating layoffs, Kaleido Biosciences failed to secure suitable transaction opportunities and halted all research and development activities, plunging the Flagship Pioneering-backed microbiome pharmaceutical company into bankruptcy. Yet, just over half a year earlier, Kaleido’s CEO Daniel Menichella had told the media that the company was poised to commence Phase II clinical trials for ulcerative colitis in the first half of 2022.

Kaleido BioSciences was founded in 2017 with $65 million in funding from Flagship Pioneering and went public in 2019. The company has entered into collaboration agreements with Janssen, the pharmaceutical subsidiary of Johnson & Johnson, and the MD Anderson Cancer Center. In January 2022, Kaleido was reported to have undergone layoffs and subsequently suspended the Phase II clinical trial of KB109. However, just weeks before this news broke, Janssen Biotech, Inc., a subsidiary of Johnson & Johnson, had expanded its research collaboration with Kaleido to pursue treatments for atopic, immune, and metabolic diseases.

With the loss of a loose external funding environment, the commercialization of new drugs has undoubtedly become much more difficult.

Certainly, setting aside the challenges in clinical development, the market demand for microbial therapeutics is clear.

In April 2023, Seres Therapeutics’ SER-109 was approved for marketing under the brand name VOWST for the treatment of recurrent Clostridioides difficile infection. VOWST is the world’s first oral microbiome therapeutic, containing beneficial gut bacteria from the phylum Firmicutes. Its commercialization will be jointly carried out by Seres and Nestlé, with both parties sharing VOWST’s sales revenue equally.

As a novel clinical drug, VOWST achieved impressive market feedback upon its launch. According to the latest financial report released by Seres Therapeutics, VOWST was approved and launched in the United States in June 2023. By the end of September, the company had received 610 completed prescription enrollment forms. Among these, 282 patients had already initiated treatment with VOWST. Furthermore, although VOWST is not yet covered by commercial insurance, these prescription enrollment forms were submitted by more than 480 different healthcare providers, with 78 healthcare providers having prescribed VOWST to more than one patient.

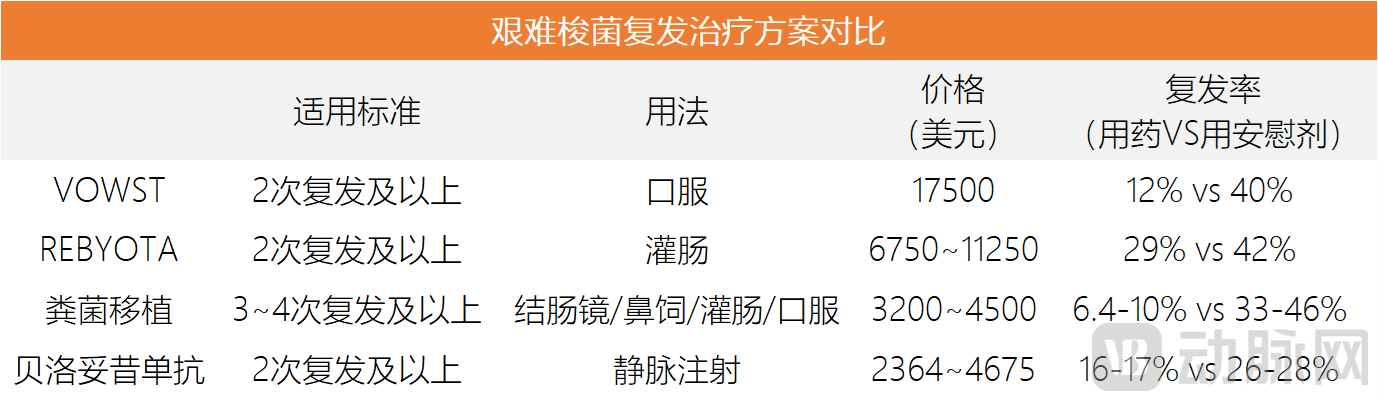

It is worth noting that VOWST is not priced low, and there are other clinical options available for the treatment of Clostridioides difficile infection besides VOWST. Clostridioides difficile is a bacterium commonly found in healthy gut microbiota. When an individual takes antibiotics, the balance of gut microbiota may be disrupted, leading to life-threatening Clostridioides difficile infection (CDI). Even after the bacteria are cleared, infections may recur multiple times due to dysbiosis of the gut microbiota.

Currently, the most common clinical treatment regimen for Clostridioides difficile infection is fecal microbiota transplantation (FMT); however, this approach is associated with poor patient experience, prompting ongoing efforts to develop new therapeutic options. In addition to VOWST, novel therapies that have emerged in recent years include the biologic agent bezlotoxumab and the enema formulation REBYOTA. Launched in 2022, REBYOTA is the second approved microbial drug worldwide. Like traditional FMT, it requires the collection of intestinal microbial samples from healthy donors; however, unlike conventional FMT, REBYOTA’s manufacturing process involves stringent quality control measures to ensure the consistency and stability of the microbial therapy.

At this stage, due to the relatively short time since market launch, there are no research data directly comparing VOWST with the aforementioned alternative treatments. However, cross-comparison of available data suggests that VOWST’s efficacy is superior to that of REBYOTA and bezlotoxumab but inferior to fecal microbiota transplantation (FMT). While VOWST has the highest treatment cost among the four options, it offers the most patient-friendly route of administration. Its relatively favorable efficacy combined with the convenience of an oral formulation may well explain its widespread popularity.

Comparison of Treatment Regimens for Recurrent Clostridioides difficile Infection Data Source: Compiled by VCBeat from public information

In this financial report, Seres Therapeutics also acknowledged that VOWST is an excellent product, but its commercial prospects remain uncertain due to its high price. From a cost-control perspective, commercial insurance plans may position VOWST only as a second-line therapy, to be used after cheaper alternatives have failed. Were price not a factor, VOWST would easily become the preferred first-line option for physicians and patients in preventing recurrent Clostridioides difficile infection. Naturally, Seres Therapeutics is also attempting to reduce the commercialization costs of VOWST. In August 2023, Seres Therapeutics closed one of its three donor collection centers and established a donor screening laboratory to lower costs.

In a sense, over the past decade, hundreds of clinical trials have rapidly validated the clinical value of microbiome-based pharmaceuticals. Currently, however, the sector is stalled in demonstrating its commercial viability. With nearly half of the star overseas microbiome pharmaceutical companies having collapsed one after another, concerns about the industry’s future are mounting. Yet, a more granular observation reveals that the industry still has the opportunity to crouch before leaping forward. We remain hopeful that, as the tolerance for trial-and-error and the funding environment become appropriately more lenient, more novel microbiome-based drugs will emerge to address complex clinical challenges.