Seeing Is Believing: Investment Opportunities in Ophthalmic Devices Under China's National Eye Health Strategy

Editor’s Note: This article is from the Shanghai Biomedical Fund, authored by Wu Chong. VCBeat has obtained permission to republish it.

The triple resonance of “demand–supply–policy” is propelling China’s ophthalmic optometry sector into a golden age for investment. Class III ophthalmic medical devices, which combine the attributes of serious medical care and consumer healthcare, are unlocking vast development opportunities in the Chinese market and catalyzing the emergence of blockbuster products with market scales ranging from hundreds of millions to tens of billions of RMB. Addressing unmet clinical needs such as precise myopia control, presbyopia, and dry eye disease, innovation (new materials, new designs, and new technologies) and mergers and acquisitions (innovative products, distribution channels, and overseas M&A), as the core growth engines, are driving rapid development in this field and generating systematic industrial investment opportunities.

Table of Contents

I. Understanding Our Eyes

II. Triple Resonance of “Demand–Supply–Policy”

III. Investment Opportunities in the Broad Vision Care Industry

IV. Ophthalmic Medical Devices from the Perspective of Industrial Ecosystem

V. Industry Characteristics of the “Broad Vision Care” Sector

VI. New Trends in the Field of Optometry and Vision Care

VII. Growth Engines for Ophthalmic Device Companies in the Broad Vision Care Sector

VIII. Investment Map of China’s Ophthalmic Consumables Industry

I. Understanding Our Eyes

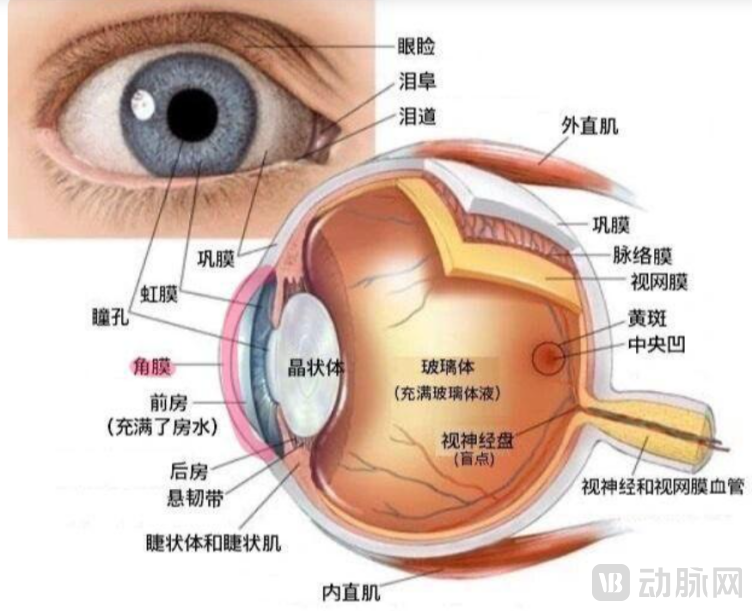

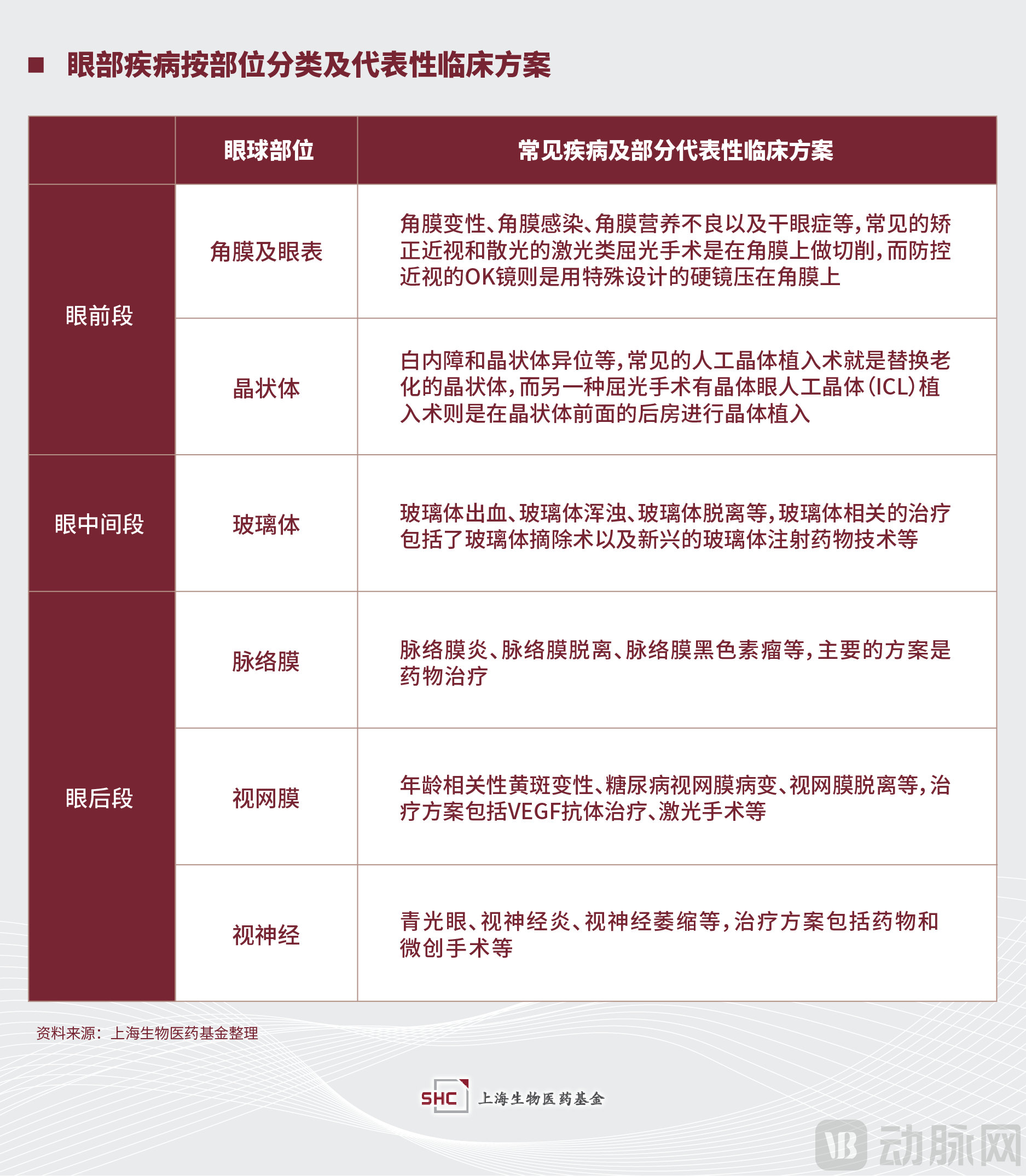

To understand ocular diseases and their corresponding clinical needs, we first examine the structure of the eyeball. The eyeball consists of three layers of the ocular wall and three intraocular contents. The outer layer of the ocular wall comprises the cornea and sclera; the middle layer, known as the uvea, includes the iris, ciliary body, and choroid; the inner layer is the retina, whose central region, the macula, is capable of recognizing most optical signals such as shape, size, color, and distance. The three intraocular contents, arranged from outside to inside, are the aqueous humor, lens, and vitreous body; together with the cornea of the outer layer, they constitute the eye’s refractive system.

Schematic Diagram of Eyeball Anatomy (Image Source: Internet)

The aforementioned structures of the eyeball are susceptible to corresponding diseases due to infection, aging, genetic factors, and other causes. Among themInvestment Focuses Primarily on Myopia in Adolescents and Degenerative Eye Diseases in the Elderly(including presbyopia, age-related macular degeneration, diabetic retinopathy, glaucoma, etc.), corresponding screening, correction, and diagnostic and therapeutic products have consistently been focal points for R&D and investment.

Next, we will delve into investment trends in the ophthalmology sector using the “Demand–Supply–Policy” framework, a fundamental model for investment analysis.

II. Triple Resonance of “Demand-Supply-Policy”: The Ophthalmic Optometry Sector Is in a Golden Investment Period

(a) Demand: What Changes and What Remains Unchanged

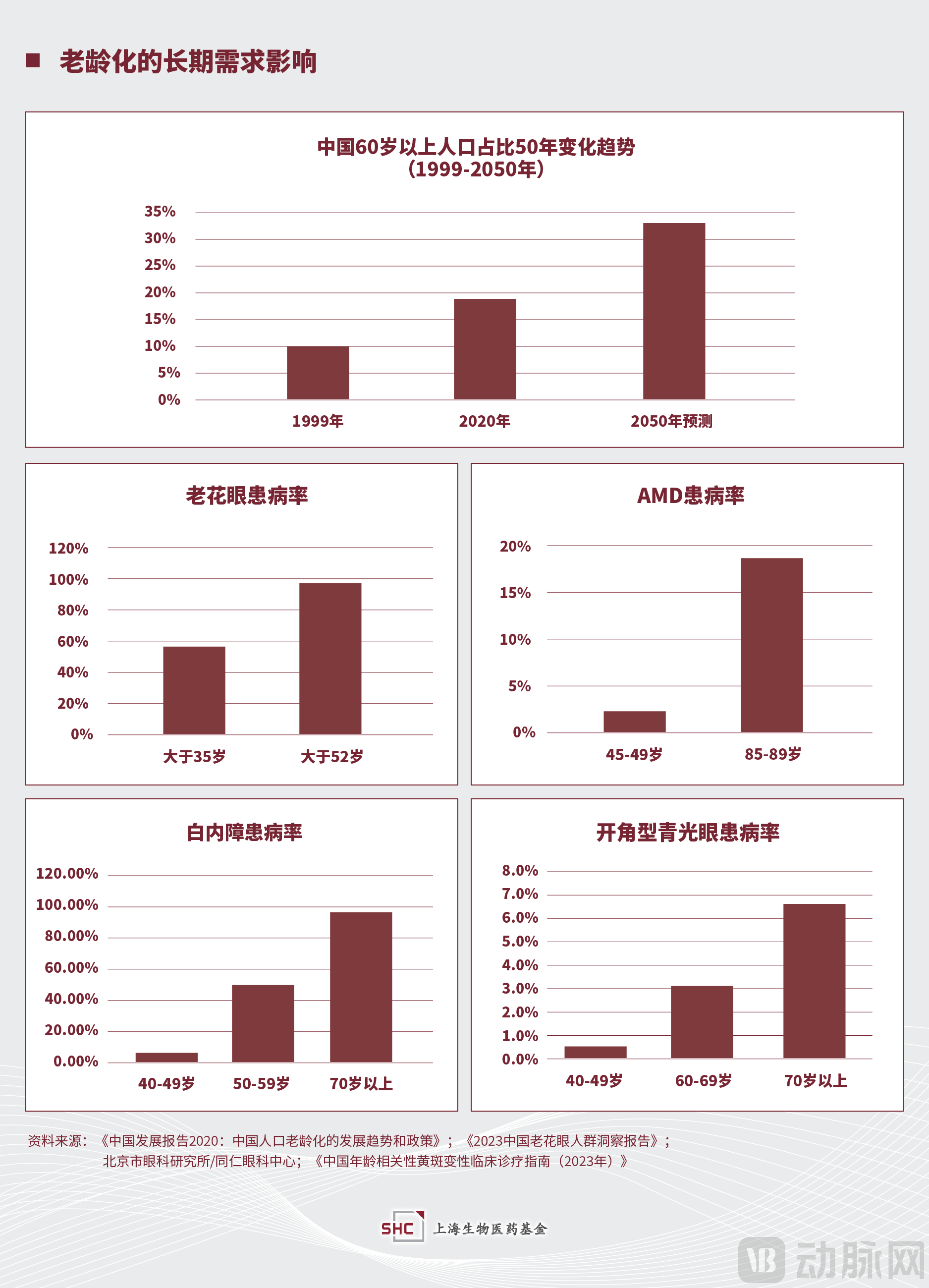

The widespread prevalence and even epidemic nature of eye diseases constitute the fundamental, unchanging source of demand for ophthalmology investments. Aging-related degeneration, lifestyle factors, genetic variations, pathogenic infections, and secondary complications are the primary causes of ocular diseases.Age-related degenerative eye diseases, including presbyopia, cataracts, glaucoma, and age-related macular degeneration (AMD), affect over 500 million people. Lifestyle-related eye conditions, such as myopia and dry eye syndrome, impact more than 1 billion individuals. Hereditary and variant eye disorders encompass over 600 diseases, including Leber congenital amaurosis. Eye diseases caused by pathogenic infections and secondary complications include trachoma, styes, conjunctivitis, diabetic retinopathy, and hypertensive retinopathy. Among these,Population aging and screen-based lifestyle habits, as long-term trends, will constitute the underlying drivers of market demand for eye diseases in the coming decades.. The figure below illustrates the long-term trend of population aging in China and the impact of age on the prevalence of representative age-related eye diseases.

Beyond accounting for the steady demand for disease diagnosis and treatment, healthcare investment places greater emphasis on the rapid release of unmet needs driven by technological advancements and increased economic affordability.In the field of ophthalmology, beyond the iterative upgrades of traditional technologies, more revolutionary changes are driven by advancements in cell and gene therapy., directly driving the development of new drugs for genetic and rare ophthalmic diseases. Examples include Luxturna, approved in the United States in 2017 for the treatment of Leber congenital amaurosis, a condition that previously had no clinical solutions.In the field of ophthalmology, improvements in economic affordability are well reflected in areas such as myopia, presbyopia, and dry eye.。

In the realm of myopia correction and control, the Chinese market has evolved from the upgraded consumption of traditional frame glasses to daily, monthly, and yearly disposable contact lenses and colored contacts; then to refractive surgeries offering one-time correction, such as laser surgery and ICL implantation; and further to myopia prevention and control measures targeting children, including defocus spectacles and orthokeratology (OK) lenses.The inconvenience and aesthetic drawbacks of traditional frame glasses have rapidly emerged from a relatively minor clinical concern into a significant demand, driven by rising economic affordability.。

Regarding presbyopia and dry eye disease, as the large cohort of middle-aged individuals with the greatest paying capacity gradually enters the age range with a high incidence of these conditions, their clinical needs differ from those of the previous generation of elderly patients; for instance, they find it difficult to accept blurred vision associated with aging.The growing demand for dry eye treatment among populations characterized by screen-centric lifestyles, contact lens use, and a history of laser refractive surgery has driven the research and development as well as clinical adoption of innovative products such as multifocal intraocular lenses and scleral lenses.。

(b) Supply: Innovation-Driven Investment

The enduring theme of healthcare investment is innovation on the supply side. In the field of ophthalmology, technological innovations can be categorized into different types, including physical, biochemical, and molecular innovations.

Advancements in physical technologies, including Optical Coherence Tomography (OCT) and multifocal/extended depth of focus intraocular lenses, have driven corresponding investments in these technologies both domestically and internationally.OCT technology saw its first original paper published in 1991, with the first commercial device developed in 1996. It has since undergone continuous iteration through three generations: time-domain OCT, spectral-domain OCT, and swept-source OCT. Chinese innovative companies, represented by Shuowei and Topcon (Tupai), have achieved global leadership in third-generation swept-source OCT technology. Meanwhile, intraocular lens (IOL) technology has evolved from monofocal to bifocal, trifocal, and extended depth of focus (EDOF) IOLs, providing cataract patients with increasingly clear, comprehensive vision. Domestic IOL manufacturers, such as Aierbo Nuode (Aibonide), have continued to innovate beyond monofocal lenses, promoting the domestic substitution of multifocal and EDOF IOLs. Furthermore, multifocal optical designs are increasingly being extended to contact lenses, including soft lenses and rigid gas permeable (RGP)/scleral lenses.

In the field of ophthalmology, the core of biochemical technology innovation lies in the innovation of new materials.Leveraging China's vast market and continuously improving payment capacity,The pace of introducing innovative foreign materials into China, as well as the speed of innovation translation and domestic substitution, is accelerating., such as Mingyi Ophthalmology’s introduction of STAAR Surgical’s globally exclusive ICL product from the United States; YandeLe’s innovative translation and development of a new generation of aspheric intraocular lenses based on its global patented “cross-linked polyolefin” technology; Aierbode’s achievement of full domestic substitution for the raw materials used in its orthokeratology (OK) lenses; and Ruitai Biologics’ innovative development of high-activity hydrated amniotic membrane, among others.

In terms of molecular technology innovation, it represents the latest technological development in the field of ophthalmology.Key areas include the application of gene sequencing in ophthalmic diagnostics and the use of gene therapy for inherited or rare eye diseases, as well as common ocular conditions. Representative companies in the former category include Puxi Gene, which has developed risk screening products for high myopia specific to the Chinese population using technologies such as whole-exome sequencing (WES). In the latter category, companies like Langxin Biopharma are leveraging adeno-associated virus (AAV) vectors to develop treatments for inherited/rare eye diseases such as Leber congenital amaurosis, as well as common conditions like neovascular age-related macular degeneration (nAMD).

(c) Policies: Catalysts for Industrial Development

The field of ophthalmology has consistently received national-level policy support, with core policy themes evolving from infectious trachoma to age-related blinding cataracts, and most recently to myopia prevention and control in children and adolescents.

● Policies for the Prevention and Control of Infectious Trachoma:From the widespread prevalence of trachoma at the time of the founding of the People’s Republic of China, to the world’s first identification in 1956 by Chinese researchers of Chlamydia trachomatis as the causative agent of trachoma, and the subsequent nationwide trachoma prevention and control hygiene campaign conducted from 1957 to 1959, nearly six decades of efforts enabled China to meet the World Health Organization’s criteria for the elimination of blinding trachoma in 2014 (Source: The 68th World Health Assembly, 2015; National Health and Family Planning Commission of China).

● Policies for the Prevention and Treatment of Age-Related Blindness-Causing Cataracts:In July 2006, the National Plan for Prevention and Treatment of Blindness (2006–2010) set a target to achieve a cataract surgical rate of 800 cases per million population and an intraocular lens implantation rate of over 85% by the end of 2010. Starting in 2009, the “Million Poor Cataract Patients Vision Restoration Project” was implemented nationwide. By 2018, the cataract surgical rate had increased from 8.3 per 100,000 population in 1988 to 220.5 per 100,000 population in 2017, thereby achieving the original targets ahead of schedule (Source: “Progress in Cataract Prevention and Control in China from a Big Data Perspective”).

● Policies for the Prevention and Control of Myopia in Children and Adolescents:In 2015, the National Visual Health Report projected that by 2020, the total number of myopia cases among individuals aged five and older would exceed 700 million, with high myopia affecting an estimated 40 to 51.55 million people. In 2018, President Xi Jinping emphasized that all sectors of society must take action to jointly protect children’s eyesight and ensure they have a bright future. In August 2018, eight departments, including the Ministry of Education and the National Health Commission, jointly released the Implementation Plan for Comprehensive Prevention and Control of Myopia in Children and Adolescents (Draft for Comment). Since then, myopia prevention and control has officially become a national strategy.

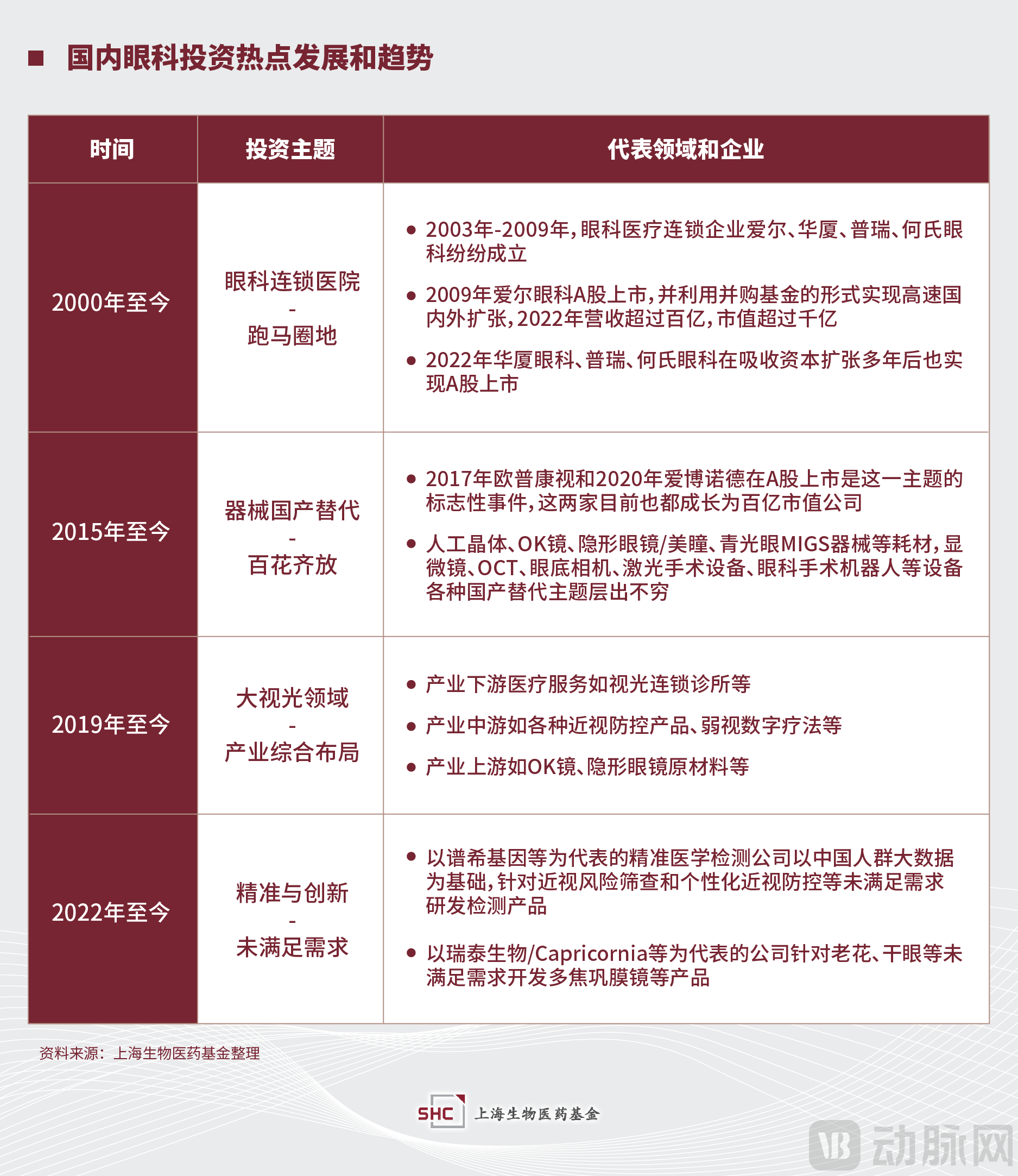

III. Investment Opportunities in the Large Optometry Industry Under the Triple Resonance of “Demand-Supply-Policy”

Based on the above “demand-supply-policy” framework analysis, it is evident that the broader optometry sector, which encompasses myopia prevention and control, satisfies all three factors. Consequently, it has emerged as a key investment hotspot in ophthalmology, following the trends of chain hospital expansion and domestic substitution. The term “broader” is prefixed to “optometry” because, from an investment perspective, the patient population for “refractive surgery,” typically categorized under specialized ophthalmology, constitutes the core demographic for myopia within the optometry sector. Therefore, refractive surgery is also included within the scope of industrial investment considerations for the “broader optometry” field. Meanwhile, as domestic investment shifted toward strengthening First-in-Class (FIC) innovation in 2022, precision and innovation have become new trends in ophthalmic investment. This shift, combined with developments in the broader optometry sector, has accelerated the R&D and investment in innovative products addressing unmet clinical needs, such as myopia risk screening, personalized myopia prevention and control, presbyopia, and dry eye disease.

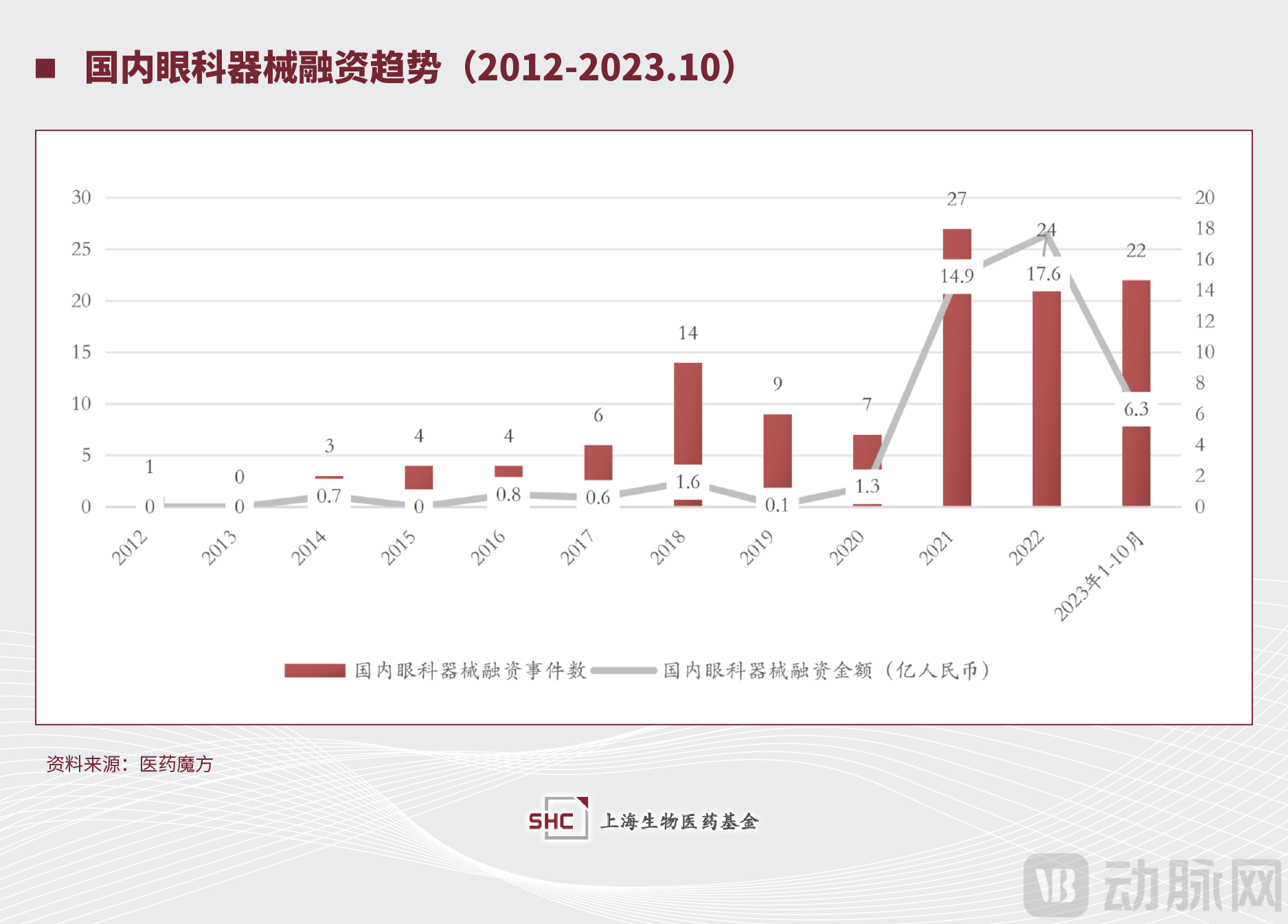

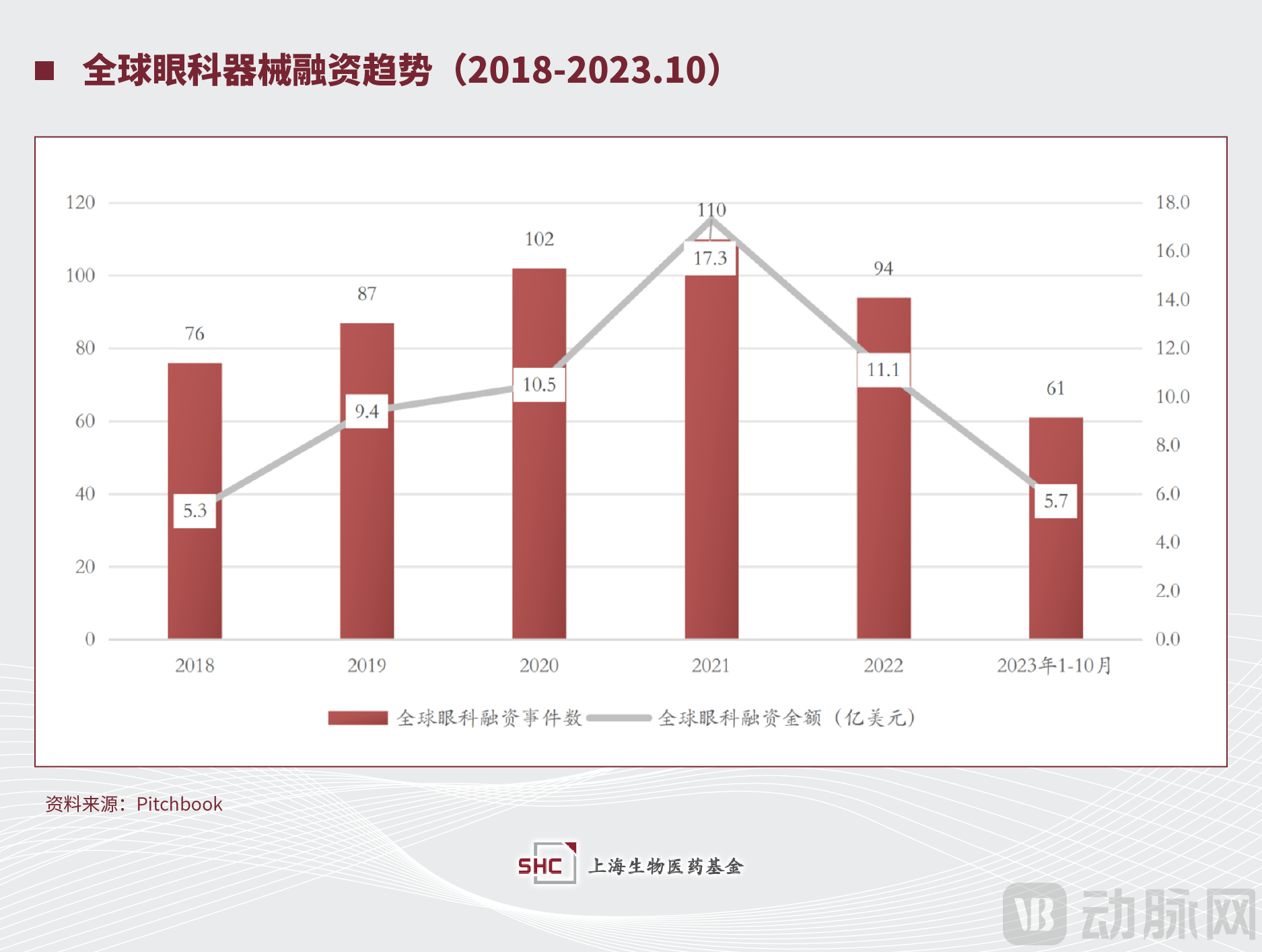

In addition, looking at the investment in the entire domestic ophthalmic device sector in China over the past decade from 2012 to 2023, it can be divided into three stages.2012–2013: Minimal Investment, the number began to increase from 2014 to 2017, but the annual number of financings remained in the single digits; starting in 2018, it grew rapidly to 14 project financings,After a slight decline in 2019–2020, the outbreak resurged in 2021.. Since 2018, the financing trends in the international ophthalmology sector have been more stable and consistent compared to those in China, with both the amount and number of financings gradually reaching a peak in 2021 over the past five years.Began a gradual decline in 2022。

It should be noted thatThe primary reason for the decline in domestic ophthalmology investments in 2022 was changes in the macro financing and investment environment., consistent with the overall investment and financing trends in the biopharmaceutical and medical device sectors. Based on our fund’s tracking of investment activities both domestically and internationally,In 2023, ophthalmic device financing in China remained one of the most active segments within the broader medical device investment landscape, with significantly higher activity levels than those observed overseas.。

IV. Ophthalmic Medical Devices from an Industrial Ecosystem Perspective: Class III Medical Device Consumables and Consumer Healthcare Hold the Greatest Potential for Cultivating Blockbuster Products

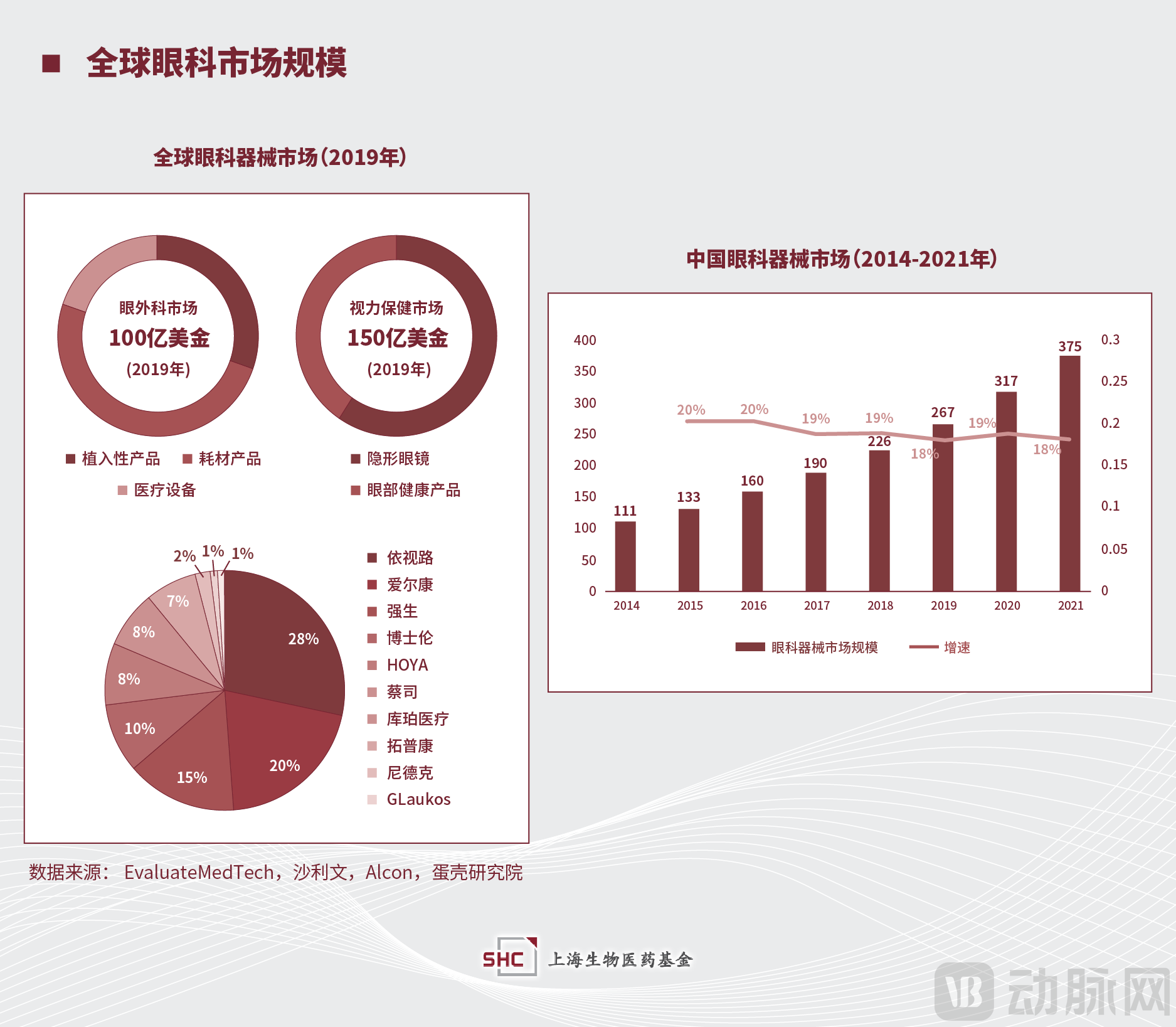

Ophthalmic Devices (Equipment + Consumables): A Rapidly Growing Multi-Billion Dollar MarketDao. In 2019, the global ophthalmic device market exceeded USD 25 billion, with a very high level of market concentration; the top 10 players, including Essilor, Alcon, Johnson & Johnson, Bausch + Lomb, Hoya, and Zeiss, accounted for over 90% of the market share. China's ophthalmic device market was estimated to exceed RMB 37 billion in 2021, with a compound annual growth rate (CAGR) of as high as 19% over the past five years.International Ophthalmology Giants Still Dominate the Majority of Market Share in China, with Significant Potential for Domestic Substitution。

Ophthalmic devices represent a sector that combines rigid medical requirements with consumer attributes. We categorize ophthalmic device products into 18 subcategories based on two dimensions: medical regulatory attributes (six classes: Class III, II, and I devices, clinical research products, functional products, and general products) and consumer attributes (three classes: diagnostic/therapeutic, correction/prevention, and aesthetic). Most individual ophthalmic device products have limited market sizes; for instance, among the diverse array of equipment and consumables falling under the "diagnostic & therapeutic" category, only intraocular lenses have a market size ranging from RMB 1 billion to 10 billion, while others fall within the RMB 100 million to 1 billion range. In contrast, high-value consumables with consumer healthcare attributes boast the highest market ceilings. As shown in the chart, ophthalmic blockbuster products with market sizes exceeding RMB 10 billion are concentrated in the "correction & prevention" segment of major optometry (optometry/refractive) products, such as laser surgery, ICL implantation, orthokeratology lenses (OK lenses), contact lenses, and defocus spectacles.Class III medical devices and consumables present high barriers to entry, fostering the growth of large corporations. For instance, in 2022, laser surgery and ICL procedures accounted for nearly 40% of Aier Eye Hospital’s RMB 10 billion revenue; orthokeratology (OK) lenses contributed over 80% of Oukang Vision’s total revenue of RMB 1.5 billion; and contact lens sales represented 25% of Alcon, the U.S. ophthalmic giant’s USD 8.7 billion revenue.

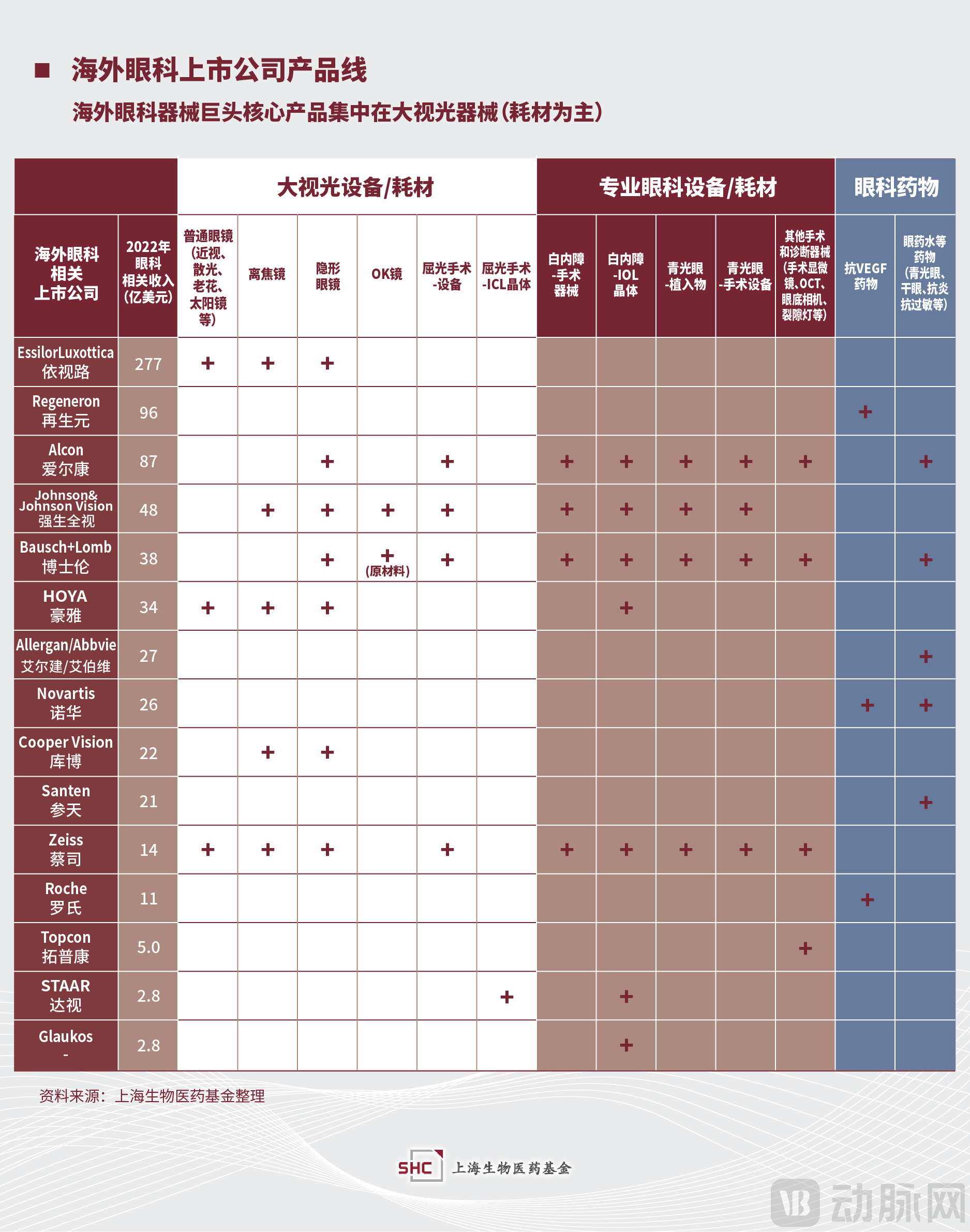

Benchmarking against overseas ophthalmic giants, their core products are also concentrated in large-scale optometry devices (primarily consumables).。Among these companies, Essilor, CooperVision, and STAAR derive the vast majority of their revenue from vision care devices and consumables. Alcon, Johnson & Johnson Vision, and Bausch + Lomb offer the most comprehensive product portfolios, spanning three major categories: vision care devices and consumables, specialized ophthalmic devices and consumables, and ophthalmic pharmaceuticals. For these three companies, revenue from vision care devices and consumables is estimated to account for more than one-third of their total income.

Amidst the massive demand, the market size of domestic large-scale optometry medical devices on the supply side urgently needs to be expanded.The State has introduced a series of relevant policies to support the domestic substitution of medical devices., and with the primary goal of enhancing corporate innovation capabilities, coupled with favorable policies, consumer-oriented Class III medical devices have gradually become the focal point of industry investment.

V. Industry Characteristics of the “Broad Vision Care” Sector: A China-U.S. Comparison

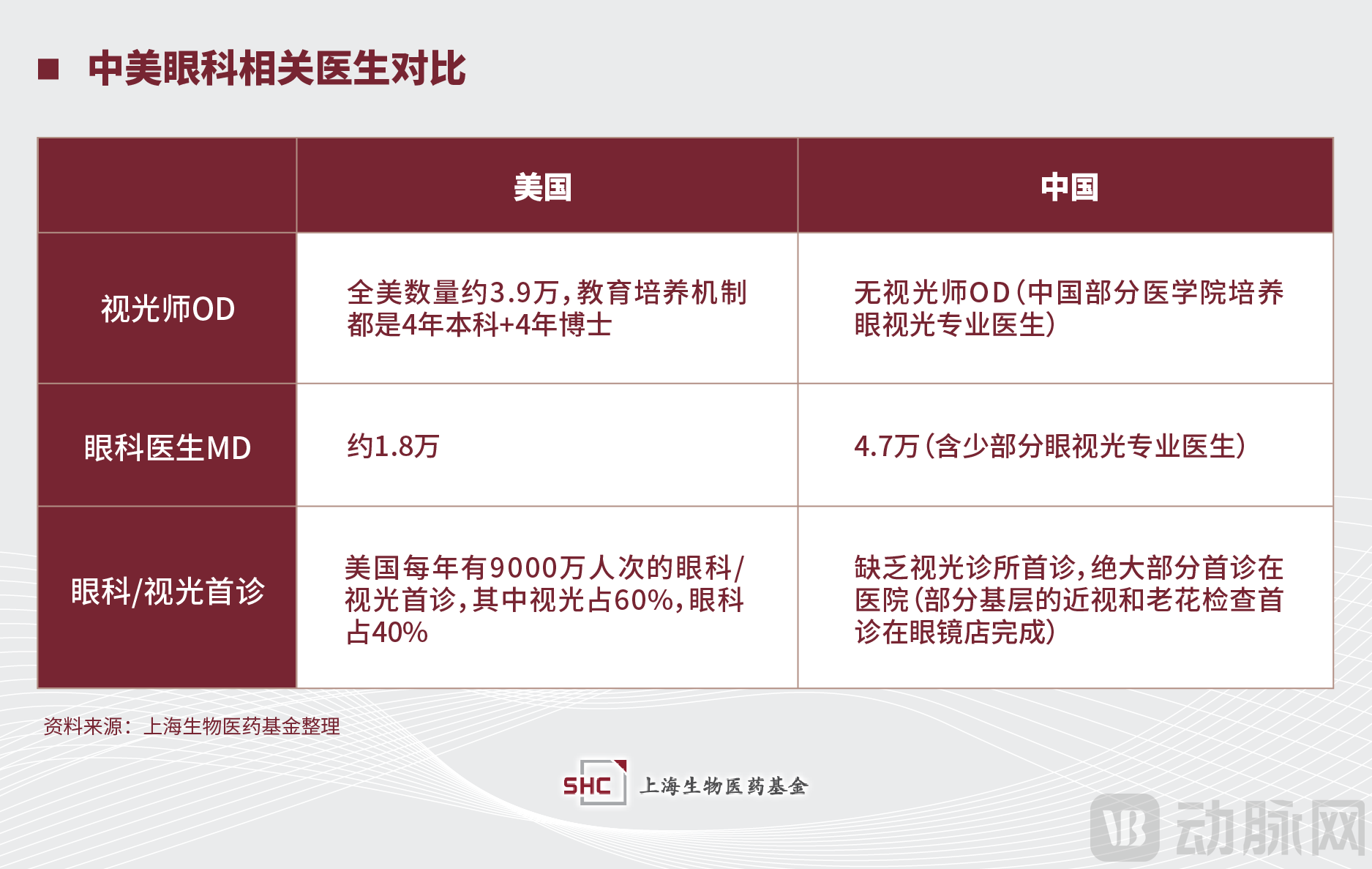

Overall, the optometry sector in the United States is far more advanced than that in China, serving as a benchmark for China’s “domestic substitution” strategy in areas such as product innovation and R&D, as well as the accessibility of optometric medical services. However, it is essential to first highlight the significant differences between the two countries in terms of epidemiology, the number of specialized physicians, hospital ownership structures, and health insurance systems. For instance, China’s myopia prevalence rate is substantially higher than that of the U.S.; the per capita number of professional ophthalmology-related physicians in China is far lower than in the U.S.; ophthalmic diagnosis and treatment in China are concentrated in public hospitals, whereas private hospitals and clinics are highly developed in the U.S.; and while China’s health insurance system is predominantly state-run, various forms of commercial insurance play a more critical role in the U.S.

A separate comparison of professional eye-care providers in China and the United States reveals fundamental differences between the two countries in the field of optometry.The U.S. population is 330 million, with an estimated 39,000 optometrists and 18,000 ophthalmologists., the combined total approaches 60,000 professionals. In the United States, there are on average 1.23 optometrists and 0.57 ophthalmologists per 10,000 people. Based on this ratio, China would require approximately 300,000 eye care professionals (optometrists plus ophthalmologists); however, in reality,Currently, China has approximately 47,000 qualified optometrists, with a shortage exceeding 200,000.Due to the absence of optometrists (ODs) responsible for basic eye care and vision health management, China has long lacked sufficient emphasis on professional medical services for the most common refractive errors, such as myopia and presbyopia. Instead, simple lens fitting services are provided by optical retailers without medical qualifications. In contrast, in the United States, any prescription lenses require a prior prescription from an optometrist (OD) before being dispensed by optical retailers.

Therefore, a comparison of product regulatory requirements in the broad optometry sector between China and the United States reveals significant differences. For instance, prescription eyeglasses and sunglasses are regulated as Class I devices in the U.S., whereas they are not regulated as medical devices in China. Defocus spectacle lenses are classified as Class II devices in the U.S., but are also not regulated as medical devices in China. Contact lenses, orthokeratology (OK) lenses, defocus soft contact lenses, and rigid gas permeable (RGP) lenses are regulated as Class II devices in the U.S.; however, in China, they are subject to the highest level of regulation, Class III, due to their placement into the eye. It is precisely this high barrier associated with Class III regulation, combined with the unmet needs of China’s vast myopic population and supportive national policies, that...In China, products such as ICLs and orthokeratology (OK) lenses, which combine serious medical applications with consumer attributes, have independently achieved scales ranging from billions to tens of billions of yuan (based on ex-factory prices).。

Due to the aforementioned differences in ophthalmic professionals—specifically, the absence of Optometrists (ODs) in China—and the distinct regulatory mechanisms for medical device registration, the optometry industries in China and the United States inevitably exhibit different characteristics. The foundation of the U.S. optometry industry lies in the clinical services provided by ODs. Through a “prescription portability” model, patients purchase eyeglasses at offline or online optical retailers. Alternatively, under an “integrated clinic-and-dispensing” model, they obtain eyeglasses or orthokeratology (OK) lenses directly at clinics or hospitals. Furthermore, U.S. optometry practices offer a broader range of visual function diagnosis and treatment services.

China has historically had only ophthalmology, without optometric medical services. Therefore, the development of optometric services has been driven by “optometric products,” including refractive surgery in the broader field of vision care and orthokeratology (OK) lenses in the specialized field of optometry. According to the founder of Autek China, “Without the emergence of OK lenses, there would be no optometry industry in China.” Products continually joining this category include more digital therapeutics for strabismus and amblyopia, as well as defocus spectacle lenses and soft contact lenses for myopia control.If future visual function products (non-surgical) become more diverse and purchasing power continues to rise, China’s optometric services may evolve into an independent specialty, thereby establishing optometry (eye health management) as a professional discipline parallel to ophthalmology (diagnosis and treatment of eye diseases).。

VI. New Trends in the Field of Optometry and Vision Care—Eye Health Management and Precision Prevention and Control

Driven by macroeconomic policies, the economic environment, and advances in precision medicine technologies, two clear long-term trends have emerged in China’s broad optometry and vision care sector:One is the shift from passive diagnosis and treatment of ophthalmic diseases to proactive eye health management; the other is the transition from population-based symptomatic treatment to personalized, precision prevention and control.。

From an industry perspective, eye health management is extending the competition in optometric services from children and adolescents to preschoolers aged 0–6 years, while transforming care from episodic disease diagnosis and treatment into continuous “membership-based” health management services.We predict that light-medical optometry services will become the patient acquisition channel and competitive focal point for ophthalmic hospitals.However, how various enterprises break through the bottleneck of insufficient supply of qualified optometrists will become the decisive factor in the fierce competition within the optometry industry. On the other hand, as previously mentioned, with the increasingly affluent middle-aged population gradually entering the age range with high incidence of ophthalmic conditions such as presbyopia and dry eye syndrome, eye health management will also provide more and better innovative products and services for this vast population.

Precision medicine has achieved tremendous success in the diagnosis and treatment of oncology and genetic disorders, and is now expanding irreversibly to a broader range of medical specialties, such as the management of rare genetic mutation-related diseases in ophthalmology, as previously mentioned.We predict that as large-scale cohort data, such as those for high myopia, continue to accumulate, even complex and common conditions like myopia will move toward precision diagnosis and treatment., such as screening for inherited eye diseases, risk assessment for high myopia, and genotype-guided personalized myopia prevention and control strategies.If integrated with big data on personal genomics in the future, national-level strategies for myopia prevention and control will further evolve toward precision and personalization.。

VII. Growth Engines for Ophthalmic Device Companies in the Broad Vision Care Sector

Optometry services have become a key business segment for listed ophthalmology hospital chains in China. In 2022, optometry accounted for 23.5%, 36.7%, 15.10%, 9.30%, and 12.27% of the total revenues of Aier Eye Hospital, He’s Eye Hospital, Purui Eye Hospital, C-MER Eye Hospital, and Huaxia Eye Hospital, respectively, serving as significant revenue pillars and growth drivers.The future development of China’s large optometry sector will be driven primarily by two growth engines: innovation and mergers and acquisitions.

● Innovation:Innovation is the primary driver of growth. In China, innovation in the optometry sector mainly encompasses the localization of underlying materials, new designs, and new technologies. The localization of materials in the optometry field primarily involves the domestic production of specialized lens materials, such as resin lenses for spectacle frames, raw materials for soft contact lenses and colored contact lenses (e.g., hydrogel and silicone hydrogel), and raw materials for orthokeratology (OK) lenses (e.g., high-oxygen-permeability fluorosilicone acrylate).Domestic production has ensured the stability of the domestic supply chain (e.g., the market share of Chinese-made orthokeratology lenses increased rapidly during the pandemic), while also significantly reducing costs.(In 2022, the cost of OK lenses for Autek China was RMB 115 per lens, while the cost for iStar Medical, which achieved full localization, was RMB 73 per lens, representing a one-third reduction in cost.) A typical representative of new designs is the multifocal/defocus optical design of lenses, which enables the development of multifunctional intraocular lenses (IOLs) and contact lenses. Examples include multifocal IOLs that address presbyopia, myopia, and cataracts; Implantable Collamer Lenses (ICLs) and progressive multifocal reading glasses that address presbyopia and myopia; and multifocal scleral lenses that address presbyopia, myopia, and dry eye.New technologies include IT-enabled digital therapeutics in ophthalmology and precision ophthalmic diagnosis and treatment integrated with gene sequencing technology.. Typical examples of the former include digital therapeutics for amblyopia developed by companies such as Shijing Medical and Jingzhun Optometry, achievingVision therapy that is more convenient, offers better compliance, and delivers superior efficacy. The latter includes whole-exome sequencing services provided by companies such as Puxi Gene, enabling risk screening for eye diseases, genetic diagnosis, and guidance for personalized treatment plans.

● Mergers and Acquisitions:The development of ophthalmic enterprises is inseparable from mergers and acquisitions (M&A), driven by the decentralized distribution of service channels and the high technological and talent barriers between different products. An examination of the growth trajectories of both global and Chinese ophthalmic companies reveals a consistent pattern of ongoing M&A and integration. Notable international examples include the 2017 merger, valued at €46 billion, between Essilor, the world’s largest manufacturer of optical lenses, and Luxottica, the world’s largest eyewear manufacturer; and Alcon’s 2022 acquisition of Aerie Pharmaceuticals for $770 million, which secured marketed glaucoma treatments and a pipeline of dry eye disease drugs.Typical M&A Integration Cases in China’s Ophthalmology Sector Initially Occurred Primarily in Chain Eye Hospitals, as Aier Eye Hospital has continued to acquire eye hospitals in China and Europe, ophthalmic device companies have subsequently begun to exert greater effort. For instance, Aibo Medical, Okvision, and Haohai Biological Technology are all leveraging mergers and acquisitions to expand their product portfolios and distribution channels. Relying on the vast market for optometry in China, we anticipate that domestic ophthalmic device and consumable companies will inevitably accelerate overseas M&A activities in the coming years, particularly targeting small innovative optometry product companies in Europe and the United States. Additionally, it should be noted thatAs optometry products and eye health services continue to expand, mergers and acquisitions among the three channels—ophthalmic hospitals, clinics, and optical stores—will become more frequent, further strengthening the trend toward group-based and centralized operations.. MainThe companies leading such M&A integration will primarily be listed chain ophthalmic hospital groups, while innovative product companies need to collaborate with these industrial groups earlier and more closely.

VIII. Investment Landscape of the Domestic Ophthalmic Consumables Industry

In summary, it is not difficult to see thatThe Medical Device Investment in the Field of Broad Ophthalmology Is at Its Peak, the consumer healthcare attributes of a billion-strong population determine that the market ceiling in this sector is exceptionally high; leveraging independent innovation, channel expansion, and M&A integration,It is worth looking forward to future vision care industry leaders achieving market capitalizations of tens of billions, or even hundreds of billions.。

The table below lists the major ophthalmic consumables in China and their representative companies. The Shanghai Biomedical Fund will also follow the aforementioned investment logic to identify and support future leading enterprises in the field of ophthalmic devices and optometry.

About the Shanghai Biomedical Fund

The Shanghai Biomedical Fund is a municipal-level industrial fund approved by the Shanghai Municipal People’s Government, with a total target management scale of RMB 50 billion. Initiated and established by Shanghai Industrial Holdings (SIH) Group, the fund will leverage Shanghai’s comprehensive advantages in biomedical development and rely on industrial resources to build an innovative investment platform for the biomedical sector that is “based in Shanghai and Hong Kong, linked with the Yangtze River Delta, and oriented toward the global market.” By combining financial capital with industrial resources and integrating domestic and overseas operations, the fund will focus its investments on key areas aligned with Shanghai’s biomedical industry development strategy. These priority sectors include high-end biological products, innovative chemical drugs and formulations, high-end medical devices and diagnostics, and innovative business models within the healthcare field.