M&A Wave Hits Healthcare Services First: Insights and Product Overview

Kunbo Medical

Precision Minimally Invasive Interventional Diagnosis and Treatment Product Developer for Pulmonary Diseases

Aier Eye Hospital

Ophthalmology Medical Chain Institution

SINOMED

High-end interventional medical device R&D, production, and sales provider

The M&A Wave Is Surging.

On August 27, the China Securities Regulatory Commission (CSRC) released the “Arrangements for Optimizing IPO and Refinancing Regulation by Coordinating the Balance Between Primary and Secondary Markets,” deciding to temporarily tighten the pace of initial public offerings (IPOs). This move has directly disrupted the plans of numerous enterprises, particularly medical technology companies that are preparing for or have already initiated their listing processes.

At the time, following the release of the notice, some believed that mergers and acquisitions (M&A) would become a more important and common exit strategy for capital, predicting an M&A wave in the biopharmaceutical and medical device industries. Others argued that there was no causal relationship between the M&A boom and the tightening of initial public offerings (IPOs), although the number of M&A deals might see a phased increase in the short term. The emergence of an M&A wave requires joint drive from underlying factors such as transformation of industrial structure, intensified competition in niche sectors, and prosperity in the capital market.

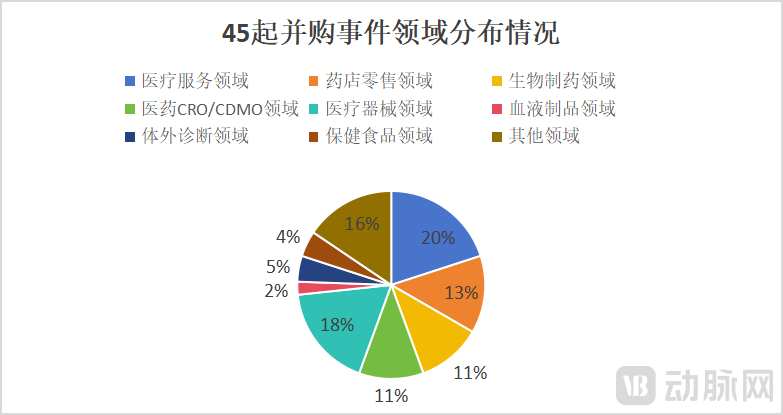

We compiled statistics on mergers and acquisitions (M&A) in the healthcare industry over a period of approximately three months, from late August to early December 2023. A total of 45 M&A transactions were recorded, compared with 26 during the same period last year.Year-on-year growth of 73%. Whether this represents a short-term, phased increase or a prelude to a wave of mergers and acquisitions, it signals that the capital exit strategies in the healthcare industry are undergoing structural changes, which are gradually influencing the sector.

(M&A Events in the Healthcare Industry from Late August to Early December 2023, Data Source: Artery Orange)

Among these 45 M&A transactions, there were fewer deals involving innovative medical devices and biopharmaceuticals, while M&A activity in the healthcare services sector was more prevalent. Why does this diverge from the trends previously predicted by industry insiders? How do this year’s M&A hotspots differ from last year’s? What trends are evident in these transactions, and what impact will they have on the industry?

According to the analysis, among 45 M&A transactions, 9 occurred in the healthcare services sector, representing the highest proportion.Why Are Healthcare Services the Hottest Sector in M&A Deals?

First, leading companies in the healthcare services sector have ample cash on hand.. The high capital threshold for mergers and acquisitions (M&A) means that such activities are inevitably concentrated among a few large enterprises with ample cash flow. Leading companies in the medical services sector precisely meet this criterion. For instance, Aier Eye Hospital reported net cash flow from operating activities of RMB 5.574 billion in the first three quarters of 2023. Additionally, medical service providers such as Clear Medical, Arrail Group, He Eye Specialist Hospital, Purui Eye Hospital, and Huaxia Eye Hospital successfully completed their initial public offerings (IPOs) in 2022, raising substantial funds.

Secondly, mergers and acquisitions are the optimal strategy for the expansion of healthcare service groups.The medical services industry exhibits distinct regional characteristics. It is constrained not only by local economic conditions and population size but also features challenges such as difficulty in cross-regional expansion, slow growth, and long payback periods. Mergers and acquisitions (M&A) can facilitate rapid expansion in the short term while minimizing the adverse impacts associated with these industry traits. For instance, Aier Eye Hospital achieved swift cross-regional deployment by acquiring equity stakes in ophthalmic hospitals in Tangshan, Hengdong, Xianyang, Taishan, Suining, and other locations.

Finally, standalone medical service hospitals or small-scale medical service enterprises face significant operational pressures, making acquisition a win-win choice.. As can be seen from the annual reports, leading medical service providers such as Aier Eye Hospital have reaped substantial profits. However, most standalone hospitals or small-scale medical service enterprises are struggling on the brink of losses. According to the National Health Statistical Yearbook 2022, in 2021, non-public medical institutions in China reported operating revenues of RMB 738.8 billion and total expenses of RMB 749.9 billion, resulting in an overall loss of approximately RMB 11.1 billion.

In practice, since the beginning of this year, multiple healthcare service institutions have filed for bankruptcy liquidation or been put up for auction. For instance, Shangrao Hekang Hospital Co., Ltd. applied for pre-reorganization in early November, while Dalian Huageng Hospital, Gangu County Xianghe Hospital, and Chengdu Mast Tumor Hospital, among others, have proceeded to auction. In light of this, standalone hospitals or small-scale healthcare service enterprises are increasingly willing to partner with well-capitalized large groups. Such collaborations not only provide advantages in branding, talent acquisition, and supply chain management, but also allow founders to cash out a portion of their equity.

In the field of mergers and acquisitions in medical services, there were three cases involving ophthalmology hospitals, two involving medical aesthetics institutions, and one each for specialized hospitals (such as oncology, health and elderly care, and physical examination centers) and general hospitals.

This may be because ophthalmic hospital groups such as He Eye Hospital, Purui Eye Hospital, and Huaxia Eye Hospital queued up for IPOs in 2022, raising sufficient capital, while intensifying market competition has prompted leading groups to increase their investments in regional expansion.

Another Hot Area in the M&A Market Is Retail PharmaciesIn fact, mergers and acquisitions (M&A) of retail pharmacies have become commonplace in the capital markets. From Yixintang’s IPO in 2014, which sparked a wave of M&A in the retail pharmacy sector, to the entry of private equity (PE) and venture capital (VC) firms into chain pharmacies in 2017, the retail pharmacy industry seemed to enter a “buying spree” overnight. Some even joked, “If an ordinary person wants to get rich quick, they should open a pharmacy and wait to sell it at double the price to a leading pharmaceutical retail company.”

However, the consequence of frenzied acquisition sprees has been a continuous rise in the per-store valuation of retail pharmacies. Additionally, as regulatory oversight has tightened, the entire industry has experienced operational contraction, leading leading pharmaceutical retail companies to slow their acquisition pace and shift toward organic expansion by opening new stores. It was not until 2021 that these industry leaders accelerated pharmacy mergers and acquisitions again. This wave of M&A has persisted to the present day and is expected to continue, driven by clear policy support for chain pharmacies to rapidly scale up and strengthen their market position. Perhaps the pharmacy M&A sector has truly entered its golden age.

Following the announcement of a phased tightening of the IPO pace, some industry insiders anticipate an increase in mergers and acquisitions (M&A) in the innovative medical device and biopharmaceutical sectors. This is because both fields require substantial capital support, platform companies with diverse product portfolios are more favored by the market, and large pharmaceutical and medical device enterprises possess ample funding.

However, this prediction did not come true. The proportion of M&A transactions in the medical devices and biopharmaceutical sectors over the past three months accounted for a relatively low share of the total number of M&A deals.

An anonymous industry insider analyzed, “Competition in various segments of China’s medical device market is extremely intense; often, a single innovative product or technology attracts the participation of ten to dozens of companies. Within a specific niche, innovative enterprises that secure funding from investment institutions also strive to build platform-based companies, deploying R&D efforts across a wide range of products. This has led to severe homogenization of technologies and products. Nevertheless, truly unique and innovative technologies or products still receive financial support from investment institutions.”

The same holds true in the biopharmaceutical sector. Some domestic innovative drug companies were founded by former pipeline teams from large overseas pharmaceutical firms who returned to China, while others persist with imitation and engage in little genuine innovation. Furthermore, competition in China’s innovative drug sector is equally intense, with numerous companies targeting the same molecular targets or technologies, resulting in a high degree of pipeline homogenization.

From this perspective, being acquired is a “privilege” reserved for only a select few high-quality enterprises.

In the medical device industry, there have been eight M&A transactions in the past three months, with three occurring in the oral care (dental) sector, making it an undisputed hot sub-segment within the medical device field.。

It is worth noting that M&A transactions in the dental field have revealed two major trends.

First, overseas dental giants are increasing their investment in the Chinese market by acquiring local Chinese companies.. For example, on October 6, global dental giant Straumann signed an acquisition agreement with the Chinese digital dentistry company AlliedStar. This acquisition will enable Straumann to provide competitive intraoral scanner solutions to its Chinese customers and meet the needs of price-sensitive clients.

For another example, Nakanishi Inc., a long-established Japanese dental company founded in 1930, announced on November 30 that it had acquired Guilin Refine Medical. It is reported that Guilin Refine Medical is one of the few innovative enterprises in China to have mastered core technologies for dental ultrasonic equipment. Its product portfolio includes ultrasonic scalers, ultrasonic periodontal treatment devices, piezoelectric bone surgery units, and light-curing machines.

Second, digital dentistry companies are currently more favored by the capital market.Among the three acquired dental companies, two are digital dentistry enterprises. For instance, AlliedStar, acquired by global dental giant Straumann, is a digital dentistry company; similarly, Zhe'an Medical, acquired in October by Sailuo Medical, a leading domestic global platform for dental instruments, is also a digital dentistry enterprise.

According to reports, the core product of Zhe'an Medical is an intraoral digital scanner (digital intraoral scanner). As a key entry point for dental digitization, this product plays a vital role in building a digital dental diagnosis and treatment ecosystem. Following the acquisition, Saile Medical will leverage the digital intraoral scanner, combined with subsequent digital products such as CBCT, to promote the establishment of a comprehensive digital dental ecosystem.

Beyond the competitive landscape, these acquired medical device companies share another common characteristic: they all possess core technologies that can provide technical support for the acquirers’ product innovation.. Taking Kunbo Medical’s acquisitions of Hangzhou Jingliang Science and Technology and Fibernova Holding Corporation as examples, Hangzhou Jingliang Science and Technology possesses innovative capabilities in intelligent manufacturing. The acquisition of Hangzhou Jingliang enables Kunbo Medical to supplement its technologies related to the development of robot control and drive system platforms, allowing Kunbo Medical to leverage complementary advantages through resource integration and further strengthen the innovation capability of its respiratory interventional diagnosis and treatment products.

Fibernova Holding Corporation is developing fiber-optic navigation and imaging systems for various medical catheters and endoscopes. The acquisition of Fibernova Holding Corporation will help Kunbo Medical enhance the precision of its real-time imaging technology products, enrich its product portfolio, and promote technological advancement.

In the biopharmaceutical sector, while M&A transactions involving innovative drugs are relatively scarce, deals in the pharmaceutical CXO space are more frequent.。

In fact, Chinese CXO companies have had a difficult time this year. On one hand, the industry has entered a downturn, with revenue growth slowing for related companies and even continuous downward revisions to performance expectations for some CXO firms. On the other hand, CXO companies from Japan, South Korea, and India have begun to snatch orders from their Chinese counterparts. For instance, Samsung Biologics secured orders this year from global pharmaceutical giants such as BMS, Novartis, and Pfizer. Sai Life Sciences, one of India’s top four CDMOs, reported being highly favored by European and American pharmaceutical manufacturers, with its performance growing by 25% to 30% in recent years.

Even in such an environment, CXO companies such as Huaveast Pharmaceutical, Porton Pharma Solutions, Viva Biotech, Ruizelian, and Keyuan Pharmaceuticals have still decided to spend heavily on acquisitions. They may be doing so for the following three reasons.

First, market expectations are for an increase in demand for clinical-stage CDMO services in 2024.. As investment firms such as Novo Holdings Ventures, under Novo Nordisk, have recently stated: With the financing environment stabilizing, early-stage biopharmaceutical companies are expected to outsource production orders.

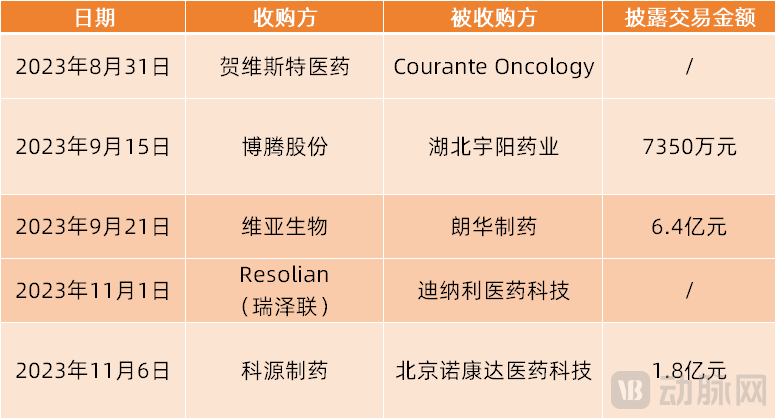

Second, M&A integration will enhance the company's market competitiveness.. For example, Hovest Pharma has advanced its global expansion strategy by acquiring the U.S.-based CRO Courante Oncology, thereby enhancing its capacity to manage global clinical trial projects and rapidly extending its market coverage to the United States. Resolian has established a bioanalytical laboratory footprint in the United States, the United Kingdom, Australia, and China by acquiring Denali Medical Technology, a leading Chinese CXO company, and has integrated Denali’s advantageous services into its service portfolio.

Third, acquire the remaining equity in subsidiaries to better manage the companyAmong them, Porton Pharma Solutions acquired the remaining 30% equity interest in Yuyang Pharmaceutical for RMB 73.5 million; Yuyang Pharmaceutical’s core business involves the research and development, manufacturing, and sales of pharmaceutical intermediates. Viva Biotech acquired the remaining 20% equity interest in Lonhua Pharmatech, whose core business includes the production of active pharmaceutical ingredients (APIs) and intermediates, as well as contract research and manufacturing services.

Although the harsh winter causes flowers to wither, it also nurtures the wax plum blossoms that proudly bloom amidst the frost. The business world is no different; during a market downturn, many companies will fail, but great enterprises emerge from these challenging times.

M&A transactions often embody the strategic foresight of large enterprises. Among these 45 deals, we can observe the acquirers’ forward-thinking perspectives and discern the industry trends hidden beneath these M&A activities.

Overall, cross-border M&A transactions have become more frequent.This indicates that healthcare companies, which previously focused solely on the Chinese market, are increasingly engaging in global competition with an international perspective.

On one hand, Chinese medical enterprises are enhancing their market competitiveness by acquiring overseas companies. For instance, Mindray’s acquisition of DiaSys, a globally renowned in vitro diagnostics (IVD) brand, for €115 million will help Mindray rapidly build an overseas supply chain platform, improve its IVD product portfolio, achieve localized production and delivery in key international markets, enhance the overall cost competitiveness of its products, and accelerate breakthroughs in acquiring mid-to-large volume customer segments abroad.

(Cross-border M&A Transactions in the Healthcare Sector Over the Past Three Months)

On the other hand, domestic medical enterprises have also achieved faster access to global customers and met global clinical market demands by being acquired by international giants. For instance, Nakanishi Inc. of Japan acquired Guilin Refine Medical Instrument Co., Ltd. to obtain its core technologies and products in dental ultrasound equipment; Straumann Group acquired AlliedStar to secure its competitive intraoral scanning solutions.This signifies that domestic medical enterprises have transitioned from past imitation and followership to present-day original innovation, with these innovations gaining recognition from leading global companies.

From the perspective of healthcare service providers, ophthalmology remains the focal point of M&A activity, while the pace of transactions in specialties such as dentistry and traditional Chinese medicine has slowed.From late August to early December last year, there were approximately nine mergers and acquisitions (M&A) in the healthcare services sector, including two in ophthalmology, two in dentistry, and three in traditional Chinese medicine (TCM). During the same period this year, M&A transactions in the healthcare services sector included three in ophthalmology, two in medical aesthetics, and one each in oncology, elderly care and wellness, and health checkups.

(M&A Transactions in the Medical Services Sector from Late August to Early December 2022, Data Source: VCBeat)

Mergers and acquisitions in specialized sectors such as dentistry have slowed, likely because dental and other medical institutions frequently suspended operations over the past three years. This led to a sharp decline in revenue without a corresponding significant reduction in expenditures, resulting in severe cash flow shortages and even the closure of some facilities.

In the field of Traditional Chinese Medicine (TCM), while M&A transactions involving TCM clinics are declining, mergers and acquisitions in the upstream traditional Chinese medicine sector are accelerating.For example, Lifang Pharmaceutical acquired Jiufang Pharmaceutical, a leading brand in modern traditional Chinese medicine (TCM), for RMB 221 million; Baosha Development acquired Jiashisen TCM, a comprehensive developer of TCM products, on September 7; and Guizhou Sanli acquired Hanfang Pharmaceutical, a specialized TCM manufacturer, for RMB 500 million.

Additionally, among the 45 mergers and acquisitions (M&A) in the healthcare sector over the past three months, 17 were valued at over RMB 100 million. Of these, four occurred in the pharmacy retail sector, two in traditional Chinese medicine (TCM) manufacturing, and two in medical services. This also indirectly highlights the high valuations of pharmacy businesses.

(Billion-Yuan M&A Deals in the Healthcare Sector Over the Past Three Months)

In addition, some mergers and acquisitions are aimed at forming strong alliances to enhance market competitiveness.. For example, after Saito Biopharma, whose core business is steroid drug intermediates, acquired Yingu Pharmaceutical, which is engaged in innovative drug research, active pharmaceutical ingredient (API) synthesis, and formulation production, the latter’s flagship products, R&D capabilities, and sales network will help Saito Biopharma accelerate its R&D progress, broaden its product portfolio, and drive product sales. Meanwhile, Saito Biopharma’s intermediate and API manufacturing capabilities will stabilize Yingu Pharmaceutical’s API supply and help it expand production capacity to capture market share. Similarly, following Medlive’s acquisition of Lingbo Consulting, the combined resources are expected to deliver upgraded research services and products to pharmaceutical company clients.

Overall, the M&A market is gradually becoming more vibrant, but the targets being acquired are often the few companies with clear competitive advantages—whether through technological breakthroughs, differentiated product offerings, or well-established sales networks.