The Collapse of Four Flagship-Backed Biotechs: Is the 'Flagship Myth' Fading?

Rubius Therapeutics

Developer of Novel Therapeutics

Evelo Biosciences

Clinical-stage biopharmaceutical R&D company

Axcella

Pharmaceutical R&D Developer

Codiak

Biopharmaceutical Exosome Therapy Developer

Although 2024 is just around the corner, some companies have still collapsed under the pressure.

On December 4, by a globally renowned venture capital firmFlagship PioneeringIncubated biotech company Axcella Health announces impending collapse. As a star enterprise in the NASH field, Axcella completed seven rounds of financing since its establishment and successfully went public on NASDAQ in 2019. However, for the past two years, Axcella has been hovering on the brink of bankruptcy. Despite numerous attempts, including an all-in pivot of its core business to the Long COVID sector in 2022, it was unable to reverse its fortunes. Ultimately, shareholders approved its dissolution and liquidation by an overwhelming majority.

However, Axcella was not the only company that failed to survive this winter. According to incomplete statistics from VCBeat,To date, the number of US-listed biotech companies that have gone bankrupt this year has exceeded 30, including as many as four incubated by Flagship., in addition to Axcella Health, there are Rubius Therapeutics, a red blood cell therapy company; Codiak BioSciences, an exosome pharmaceutical company; and Evelo Biosciences, a microbiome therapy company.

Figure 1. Four Flagship-incubated biotech companies that went bankrupt in 2023 (Source: VCBeat)

Figure 1. Four Flagship-incubated biotech companies that went bankrupt in 2023 (Source: VCBeat)

The collapse of one star enterprise after another has also placed Flagship, once in the limelight, squarely in the eye of the storm. As a “myth” in the U.S. venture capital community,Since its inception, Flagship has launched and incubated more than 100 life sciences companies, with 25 having successfully completed initial public offerings (IPOs) and over 30 others continuing to grow through acquisitions or mergers.. Among these, the most successful case is none other than the “King of Biotech IPOs”Moderna, which once delivered thousands of times in investment returns for Flagship.

But just as Moderna has drifted into a period of uncertainty as the tailwinds from its COVID-19 vaccine fade, Flagship now appears to be grappling with significant challenges amid the notoriously high failure rates inherent in innovative drug development.

60% of Invested Pharmaceutical Companies Face Bleak Outcomes: How Much Responsibility Does Flagship Bear?

According to data from the Flagship Pioneering website, nearly 50 of the 87 biopharmaceutical companies it has invested in and incubated have hit a bottleneck in the past year or two.

First, on the “shutdown” front, in addition to the four companies that have gone out of business one after another this year, many others also stumbled in 2022, with typical representatives being star enterprises in microbial therapyKaleido Therapeutics, which announced its bankruptcy last April and was delisted from the Nasdaq.

Of course, the “living” days were no better, with Moderna bearing the brunt.Its Q3 net loss was $3.63 billion, and its stock price has already halved in 2023.. Additionally, Repertoire Immune Medicines, a T-cell therapy company, was named to the 2021 global “Fierce 15” list (an annual ranking of prominent biotechnology companies that highlights innovative players in the industry), but it immediately joined the wave of layoffs in 2022, with a layoff rate as high as 45%.

So, how closely is this actually related to Flagship?

Focusing on the four biotech companies that went bankrupt this year, VCBeat has observed that their demise ultimately boils down to one reason:Clinical trials faced successive setbacks, while a lack of stable cash flow led to mounting financial pressure, ultimately becoming unsustainable.。

For instance, Evelo Biosciences focuses on developing anti-inflammatory microbiome therapeutics that act through the gut microbiota. The company has three product candidates: EDP1815, EDP1867, and EDP2939. Among them, the Phase Ib clinical trial of EDP1867 failed to demonstrate evidence of efficacy and did not even advance to Phase II trials. Meanwhile, multiple Phase II clinical trials of EDP1815 and EDP2939 conducted after 2022 all yielded negative results. Notably, for EDP1815, the EASI-50 response rate (defined as a 50% improvement in the Eczema Area and Severity Index score for atopic dermatitis) in the control group (placebo group) was as high as 56%, exceeding that of all three treatment cohorts.

However, the more thorny issue is that although Evelo’s clinical data were “impressive,” the company has indeed spent real money. It is reported thatIn the early stages of Evelo’s bankruptcy, the company had only $17.3 million in cash on hand, while its deficit reached as high as $588 million.。

Axcella has also been constrained by funding shortages. Due to financial difficulties, it was forced in 2022 to prioritize Long COVID over NASH among its two indications, resulting in an 85% workforce reduction. Although this “leaner” approach has yielded some results—with a patent granted by the U.S. Patent and Trademark Office this August—it remains a case of locking the barn door after the horse has bolted. According to disclosed financial statements,As of the most recent quarter, Axcella’s accumulated deficit had reached $425.8 million.。

Of course, everything has two sides. Behind the huge deficit, an objective fact cannot be ignored, namelyThese companies all champion innovation and seek to uncover value in niche market segments.For instance, Axcella initially focused on NASH, a condition once regarded as an R&D “black hole” in the pharmaceutical industry, with Novartis, Johnson & Johnson, and Merck all abandoning their efforts midway. Its later pivot to Long COVID has proven equally daunting, akin to “hell” mode; despite substantial market demand, no Long COVID therapy has been approved for marketing worldwide to date.

The same holds true for Evelo Biosciences, which focuses on microbiome therapeutics. However, as of the end of 2023, only two microbiome-based therapies had been approved globally, both indicated exclusively for Clostridioides difficile infection. The situation is similar for two other companies: Codiak Biosciences is the world’s first exosome therapy company, while Rubius Therapeutics is the world’s first company to pursue cell therapy using genetically engineered hematopoietic stem cells, and remains the only company with red blood cell therapies currently in clinical trials.

Therefore, many professionals view the “failure” of these companies as a highly probable outcome, given that they have chosen largely uncharted paths, inevitably facing more challenging innovation and higher-risk R&D. Compounded by the severe crises plaguing the global pharmaceutical industry over the past one to two years, the challenges they endure have been further amplified.

However, this is precisely one of the hallmarks of Flagship, namelyPassionate about innovating in “unoccupied” territoriesIn response, Flagship specifically renamed itself Flagship Pioneering in 2016, as “Pioneering” conveys greater innovation and exploratory significance than “Ventures,” representing a pioneering process of “institutional entrepreneurship.”

Therefore, if one must look to Flagship for the reasons behind these companies’ bankruptcies or setbacks,The blind pursuit of uniqueness is one such example.. Of course, there is one more point, namelyThe “nanny-style” incubation system has, to some extent, weakened enterprises’ market-oriented capabilities.。

Take Axcella as an example. Flagship not only assembled its team and was deeply involved in its operations, but also provided a continuous stream of funding. Reportedly, Flagship participated in five of Axcella’s seven financing rounds, including the sole participation in both the pre-IPO Series E round and a post-IPO secondary offering. This has resulted in an overly concentrated investor base for Axcella, with insufficient support from external shareholders. Coupled with the absence of major partnerships bringing in additional capital, it has become increasingly difficult to satisfy the substantial financial demands of drug development—the proverbial “gold-swallowing beast”—as the company moves closer to commercialization.

However, this is also one of the characteristics of Flagship, namelyBuild a company from the ground up and commit fully throughout the process to seize the “initiative”. According to seasoned investors, unlike conventional early-stage venture capital funds that typically hold around 20% equity in their portfolio companies, Flagship often owns more than 50%, or even 100%, of the equity in its invested companies, and still retains approximately 50% ownership at the time of their initial public offerings (IPOs).

Therefore, the ultimate fate of these companies was partly attributable to Flagship, but not entirely so.

Is the “Flagship” Model Losing Momentum? Should Changes Be Made?

To be frank, Flagship’s performance this year has indeed been lackluster, but the primary reason lies largely in the cooling of the entire capital market, which has led to a shift in project trends.

In response, a senior investor remarked, “Amid the harsh winter, the market will favor companies with late-stage pipelines or even marketed drugs, while frontier technology companies face significant financial pressure.”. In other words, the market currently favors pharmaceutical companies with strong certainty and stable cash flows, while it remains “unable to assist” innovative pharmaceutical firms that face high uncertainty and require continuous investment, despite their significant potential.

In fact, Flagship founder Noubar Afeyan had long anticipated this year’s outcome. In early 2023, he published a post stating, “The economic downturn has cast a shadow over the development path of emerging biotechnology companies, causing many once-promising startups to fail, including some founded by Flagship.”

However, Flagship has no intention of compromising on this matter; instead, it remains optimistic. Its founder, Noubar Afeyan, stated, “Uncertainty is tantamount to opportunity. No matter how unsettling this storm of uncertainty may be, it is important to remember that it has nothing to do with the opportunities, prospects, and value of biotechnology.“In other words, Flagship will continue to pursue innovation and remain committed to heavily investing in cutting-edge technologies with extremely high risk profiles.”

This represents the current overarching direction of the pharmaceutical industry. On one hand, significant demographic shifts and evolving social environments are giving rise to a new wave of clinical demands. On the other hand, many niche sectors, after experiencing rapid growth over the past decade, are now approaching saturation and mired in intense “involution,” urgently seeking new breakthroughs for industrial development. Furthermore, the increasing maturity of emerging technologies such as AI, cloud computing, and semiconductors is expanding the horizons for innovation in the pharmaceutical field.

Therefore, the global pharmaceutical industry is entering a new cycle of innovation, where numerous future opportunities lie. In this regard, Noubar Afeyan, founder of Flagship Pioneering, cited a specific example: he noted that innovative technologies such as cell and gene therapy, mRNA, protein degraders, multispecific antibodies, and antibody-drug conjugates are transitioning from areas of uncertainty to those with near-certain therapeutic potential; however, at the outset,These pioneering sciences seemed unworkable until they were finally realized.。

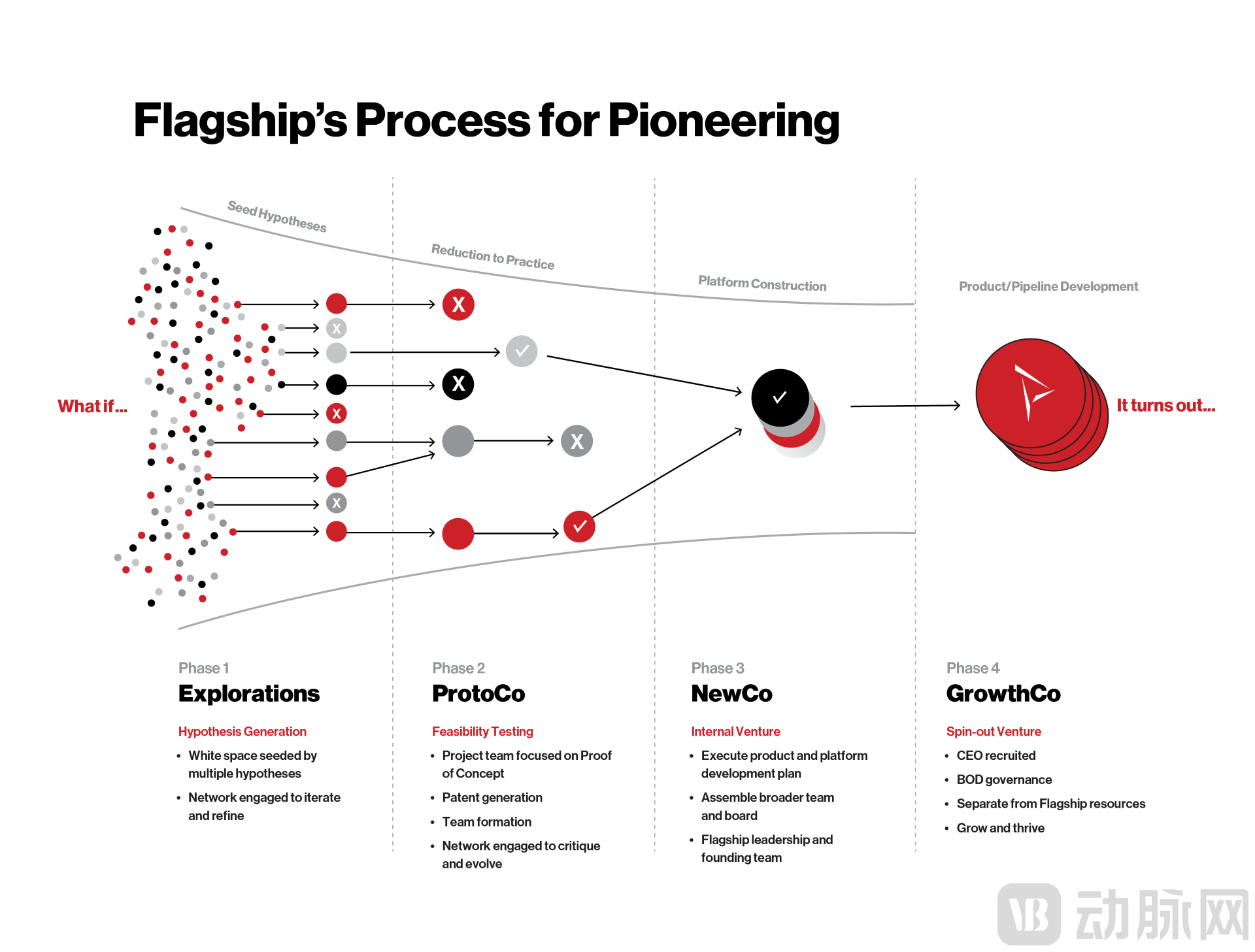

However, Flagship does not innovate “blindly”; in the four stages of creating and incubating innovative projects, the first two are respectivelyHypothesis Exploration (Explorations)andScientific Validation (ProtoCos), and its primary objective is "trial and error," through repeated scientific validation, to ultimately identify "results" with genuine innovative value.

Figure 2. Four Stages of Flagship’s Company Creation and Incubation (Source: Official Website)

Figure 2. Four Stages of Flagship’s Company Creation and Incubation (Source: Official Website)

Specifically, taking the ProtoCos (Proof-of-Concept) stage as an example, Flagship assembles a team of talent with relevant scientific and operational backgrounds for each project, while simultaneously engaging external scientific advisors. Each project is then assigned a corresponding identifier—“FL1,” “FL2,” “FL3,” and so on—and undergoes experiments designed to expose potential fatal flaws, known as “killer experiments,” to scientifically validate the concept. Projects that successfully pass this rigorous evaluation are spun out as genuine startup companies.

Of course, greater “tests” lie ahead. On this point, Flagship Pioneering founder Noubar Afeyan stated bluntly, “Currently, the tools available to us for probing the depths of unknown biological territories are still very limited. To address biological questions, we are forced to resort to ‘guesswork’ and oversimplification, which is a costly and time-consuming endeavor with a low probability of success.。”

To maximize the success rate as much as possible, systematic and timely incubation services are essential. This is precisely what the latter two stages of Flagship’s incubation of innovative pharmaceutical projects entail, namelyEstablishment of New Company (NewCo)andExternal Venture Capital, specific implementation scenarios includeInvest heavily in internal fundsandProvide a capable CEO executive, and in most cases, Flagship internal partners serve as interim CEOs of these startups. For instance, Noubar Afeyan is the founder of Moderna.

Based on this, Flagship has proposed a new concept:“Parallel Entrepreneurship”, which involves sourcing cutting-edge global biotechnologies from universities and other originators, acquiring full ownership, internalizing them as proprietary intellectual property (IP), and installing company partners as key executives. It also encompasses managing R&D incubation, team building, and attracting external investment. After undergoing rigorous funnel-style screening, the successful ventures spin off to pursue initial public offerings (IPOs), yet their “roots” remain with Flagship.

In response, a frontline investor stated, “Flagship has actually pioneered an entirely new venture capital model in the VC industry, breaking with traditional investment conventions in the field, andTransforming innovation into a 'replicable' process, which shares many similarities with the 'shell creation' process of SPACs."

When Winter Meets Innovation: How to Strategize with Limited Ammunition?

In fact, it is not only US-listed biotech companies that are experiencing a wave of bankruptcies; Chinese pharmaceutical enterprises are currently undergoing their own “trial by fire.” In the secondary market, many listed companies are facing the predicament of falling stock prices and weakening profitability. Meanwhile, a large number of companies awaiting listing are finding their path to IPOs increasingly difficult due to tighter regulations, with submitting filings two or even three times a year becoming the norm.

Of course, the primary market has not fared much better either, as startups are facing increasingly difficult fundraising conditions.The most intuitive manifestation is that the number of financing deals and the amount of capital raised in China’s pharmaceutical sector over the past one to two years have declined significantly compared with previous years.. Meanwhile, pharmaceutical companies that have secured financing are also treading on thin ice at this stage. According to a top-tier investor, a biotech firm with promising technological prospects raised only RMB 10 million in its angel round, forcing the core team to inject personal funds and accept a collective 50% salary cut just to barely sustain the company’s normal operations and development.

But on the other side of the harsh winter,Innovation is also becoming increasingly urgent in the pharmaceutical sector., on the one hand, because China’s pharmaceutical industry still faces numerous “chokepoint” technologies that need to be overcome; on the other hand, because China’s basic research capabilities are rapidly improving and can already support more cutting-edge life science innovations. Nevertheless, difficulties and challenges remain.

In this process, a question is prompting more pharmaceutical professionals to reflect, namely:How to Balance Innovation and Value Creation During a Harsh Winter?

According to a top-tier investor, many investors have adopted a “lying flat” stance over the past year or two. This trend is driven not only by increasingly difficult fundraising conditions but also by the fundamental challenge of identifying high-quality pharmaceutical projects. Meanwhile, some pharmaceutical companies have opted for a more “conservative” approach, prioritizing short-term cash flow generation through commercial operations while postponing more challenging innovation and R&D efforts, with the immediate goal of simply staying afloat.

Of course, a significant portion of the pharmaceutical industry continues to push against the headwinds. Flagship Pioneering, for instance, has not halted its innovation despite facing repeated setbacks. This June, Flagship launched a new biotechnology startup, Empress Therapeutics, providing it with $50 million in seed funding to accelerate small-molecule drug discovery through DNA-encoded chemistry research. Similarly, in China, numerous investors and pharmaceutical companies are pursuing innovation across various dimensions.

Therefore,There is actually no standard answer to this question., except that Flagship chose innovation, opting to venture into an uninhabited desert. In the words of founder Noubar Afeyan, it is “"Far from the coast, deep into the vast expanse of the ocean."”。

This is tied to Flagship’s endogenous logic. From its perspective, the value of innovations in life sciences often does not manifest immediately; it frequently takes a decade or even longer to materialize. Therefore, for Flagship, “repeated failures” are hardly a major concern. After all, there are countless paths to wealth creation, and no one can predict which avenue will yield the next Moderna.

1. “Bankruptcy Wave Spreads as Biotech Insolvencies Hit Record High” – Amino Observation;

2. “Yet Another Biotech Goes Bust: Flagship Really Can’t Take the Hit”—Zhi Yao Ju;

3. “Is the Flagship Model Collapsing? After Spinning Out Moderna, 60% of Its Invested Pharma Companies Have Struggled, with Three Recent Bankruptcies” – Deep Dive into Science.