2023 Smart Laboratory Industry Report: Clinical Diagnostics Seeking Growth in Tier-2-and-Below Markets, Drug R&D Emerging as a Key Application

Clinical Laboratory Testing Laboratories:

With numerous market entrants and overcapacity, the market is becoming a red ocean;

AI integration and the development of open-platform products are the prevailing product strategies at present;

Expand into tier-2 and lower-tier medical institutions, and venture into R&D-focused laboratories to seek incremental market growth.

R&D Laboratory:

The post-pandemic era has unleashed a surge in latent demand, leading to continuous expansion of the market size;

Automation modules covering end-to-end operations, coupled with rapid integration capabilities, help enterprises gain a competitive edge;

Automation facilitates the rapid accumulation of high-quality experimental data, urgently requiring a "quantitative change" to drive a "qualitative leap," thereby creating a self-driven, integrated wet-dry closed-loop laboratory;

The sector is still in its early stages of development; it is essential to start from market needs and co-create with industry leaders to help enterprises build core products.

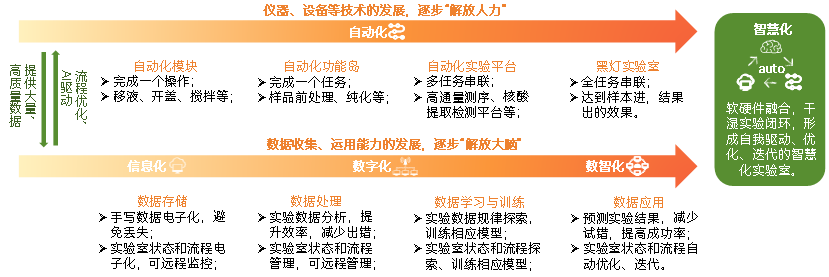

1Spiral Development of Automation and Digital Intelligence: The Industry Urgently Needs High-Quality Data

Automation solutions integrated into medical instruments and equipment serve as the primary intelligent means to “liberate manpower.” Meanwhile, capabilities in data storage, processing, and application bear the critical responsibility of “liberating the brain.”

Components and Evolution of Smart Laboratories

Smart laboratories require the spiral development of both hardware and software.Currently, the process of “liberating manpower” is overall outpacing that of “liberating brainpower,” yet both still have some way to go before reaching the “ultimate” state illustrated in the figure. The concurrent advancement of these “two legs” requires mutual “support”: the large volumes of high-quality data generated by automation constitute a critical foundation for digital-intelligent development; meanwhile, how automation can produce such high-quality data depends on “analysis” enabled by digital intelligence. Overall, medical experiments in China’s life sciences sector are currently in a phase of rapid data collection.

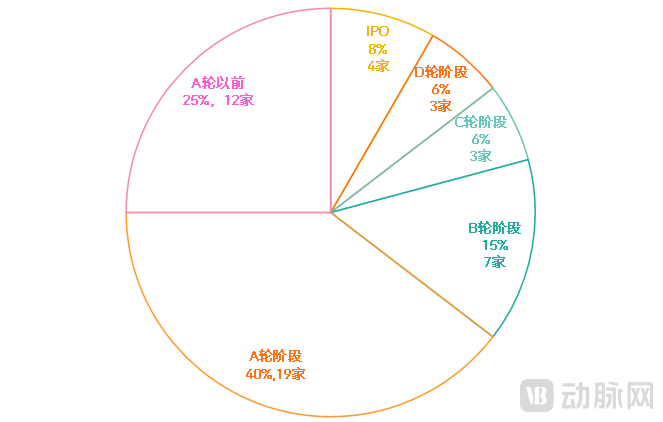

2Although the sector as a whole is still in its early stages, clinical laboratory testing has already become a red ocean.

Smart laboratories are still in the early stages of development.According to incomplete statistics from VCBeat Research Institute (data as of September 25, 2023), a total of 62 companies have entered the smart laboratory sector, with 54 of them founded after 2010. Among these, 48 companies have secured financing; the largest proportion, 40%, are at Series A stage, followed by those in pre-Series A stages, while companies at Series B and beyond account for 35%. This indicates that the smart laboratory sector remains in its early stages of development.

Statistics on the Number of Companies by Financing Stage (Only the Latest Round of Financing is Counted)

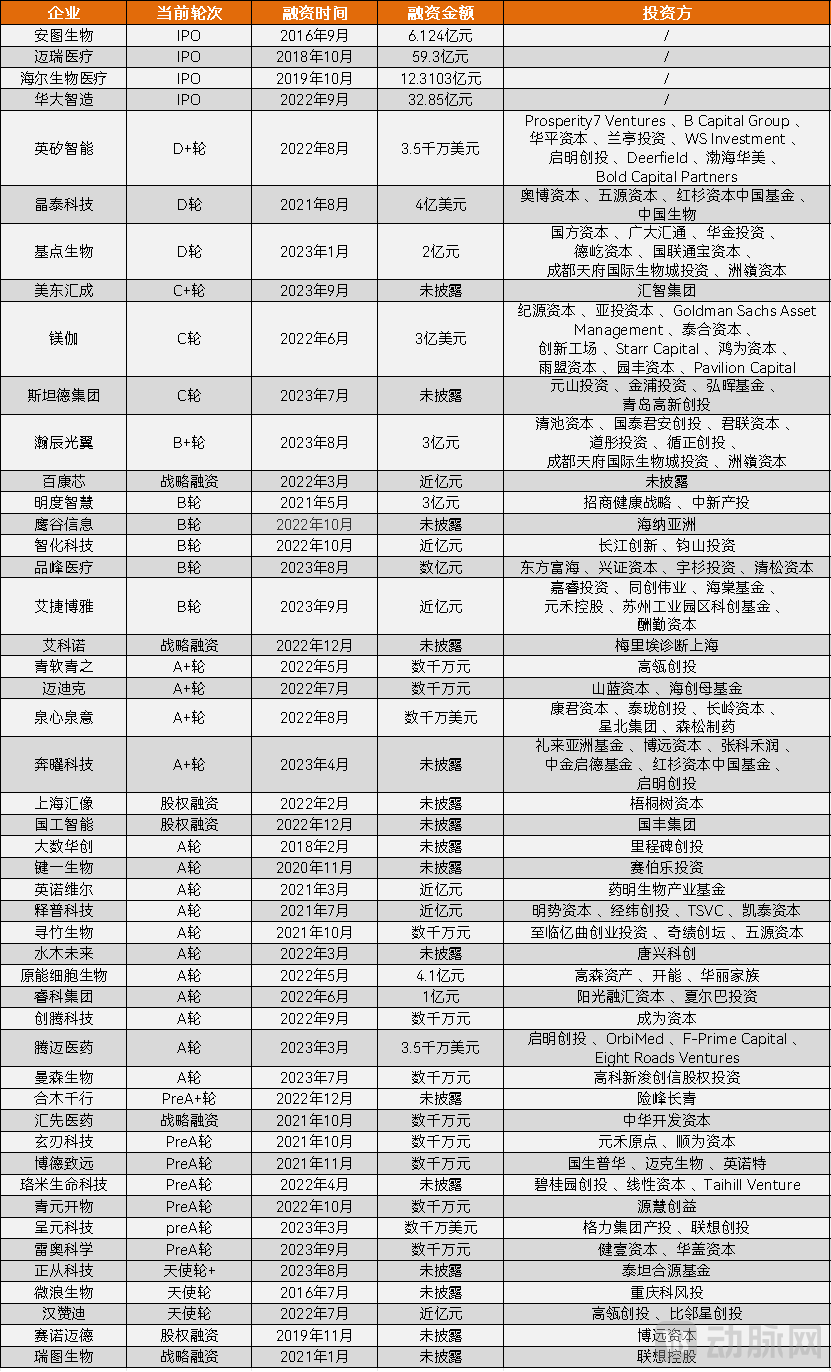

However, further segmentation reveals that companies focusing on the intelligent construction of clinical or third-party testing laboratories are generally at later stages of financing, with listed enterprises such as Autobio Diagnostics and MGI Tech already emerging. In particular, following the pandemic, the maturity of this sector has risen rapidly, attracting a surge of entrants. This has led to intense competition, turning the market into a relatively red ocean.

Financing Status of Selected Smart Laboratory Construction Companies (Only the Latest Round of Financing Is Shown)

Data sources: VBInsight, Qichacha, Tianyancha; sorted by financing round, with ties broken by date.

In the life sciences sector, the competitive landscape for companies providing laboratory automation solutions for drug development or basic research remains unclear. Many enterprises are leveraging their unique strengths to address specific pain points, thereby contributing to the intelligent transformation of laboratories in this field. Examples include Hansense Di, which entered the market through liquid handling; Zhengcong Technology and Ustc Tech, which focused on solid weighing; and Chuangze Biology, which specialized in cell preparation technologies. These new entrants driving laboratory intelligence have also gained recognition in the marketplace.

1It is an industry consensus to persist in independent R&D and establish open testing and inspection laboratories with deep AI integration.

Clinical testing and laboratory diagnostics face significant pain points, which have driven rapid development accelerated by the pandemic.The vast market potential and the impetus provided by the pandemic have attracted significant capital investment and numerous enterprises to enter the field, driving rapid advancements in the automation of clinical laboratory testing. According to research, China currently has more than 3,000 installed total laboratory automation (TLA) lines, with a penetration rate exceeding 80% in tertiary hospitals; some hospitals have even deployed multiple TLA lines. Given the current trends, the remaining untapped market for TLA lines is less than 50%. At an annual installation rate of over 500 lines, the domestic market for clinical laboratory automation lines is projected to approach saturation within the next three to five years.

Overcapacity: Securing a Larger Share of the “Cake” Through Genuine Cost-Effectiveness.In the face of overcapacity, companies have adjusted their product strategies, with a key development direction being to enhance brand strength, service capabilities, and openness, thereby improving the overall cost-effectiveness of clinical laboratory automation lines.

Three Major Strategic Directions for Key Products of Domestic Enterprises

Brand power is crucial for long-term development and requires sustained accumulation to achieve breakthroughs.Currently, the brand influence of multinational corporations such as Roche and Beckman remains unshakable. When budget allows, hospitals still firmly prioritize brand strength over cost-effectiveness. Brand strength requires the synergy of high-quality products and effective marketing strategies; it is crucial for long-term development and represents a process of gradual accumulation leading to significant breakthroughs.

Service Capability Is the Entry Point for Differentiated Competition at This Stage.Service capability is another important and effective product strategy. Imported products still maintain a clear advantage in stability, but related services have long been a pain point in clinical settings; for instance, the pace of product iteration and updates is relatively slow, and the response speed and resolution efficiency of after-sales service are generally low. In this area, domestic manufacturers possess inherent localization advantages, enabling them to more flexibly keep up with changes in clinical demands, which provides Chinese-made manufacturers with a differentiated entry point for competition.

Openness is the general trend.If brand strength lays the foundation for long-term competitiveness, and service capability provides a differentiated entry point, then openness is the most direct and powerful competitive weapon. Currently, multinational leaders in the clinical laboratory automation line market predominantly offer closed systems. In this landscape, adopting the same strategy would likely result in domestic brands remaining in a perpetual catch-up mode, whether in terms of the speed of comprehensive product portfolio deployment or brand building. Therefore, open automated solutions present Chinese brands with an opportunity to overtake competitors on the curve.

Uphold independent technology R&D and strengthen AI integration.In the field of laboratory testing, developing a functional automated assembly line product may seem straightforward; however, creating an open modular automation system that stably integrates with mainstream instruments while ensuring high throughput consistent with instrument capabilities, precise sample identification, and seamless connectivity for pre- and post-analytical processing presents significant challenges.

In the past, many automation products were rapidly assembled from components sourced from various suppliers to capture market share. However, in the future, self-developed products featuring core technologies will demonstrate increasingly strong competitiveness. On one hand, proprietary technology maximizes product flexibility and iteration speed; on the other, a key advantage is that the costs of self-developed products are controllable.

Further analysis of core technologies reveals that the application and integration of AI are urgent priorities. Highly integrated and stable automation products serve as a robust physical foundation, while the accompanying high-intelligence software acts as their soul. An open-ecosystem automation product not only ensures compatibility with third-party hardware but also enables seamless hardware operation through unified scheduling software. Developing a control and scheduling system capable of optimally orchestrating each operational stage, real-time status identification, data logging, and adaptive adjustments will significantly expand the applicability of automation products and enhance user convenience and experience.

Rapidly advancing AI technologies hold immense potential in this area, enabling software to become more intelligent. Furthermore, the deep integration of AI can directly lower the usage threshold for operators, making product interactions more aligned with the thinking patterns and habits of clinical practitioners.

MGI Tech is a pioneer in this field. Building upon unmanned operations achieved through automated products, flexible robotics, and Laboratory Information Management Systems (LIMS), it has integrated AI algorithms into laboratories. Leveraging modules such as natural language processing, machine learning, computer vision recognition, and data processing and analysis, the system enables 24/7 dynamic monitoring of environmental safety. Furthermore, it can autonomously assess optimal operational configurations and optimize experimental workflows based on throughput and output requirements, thereby creating a self-driven “lights-out laboratory.”

It is foreseeable that, with the assistance of AI, intelligent software will truly enable the digitalization and data-driven intelligence of automated clinical laboratory testing pipelines, thereby establishing smart laboratories characterized by a “sample-in, report-out” workflow.

2The Second Half of Intelligent Drug R&D: Data Accumulation and Foundational Modules

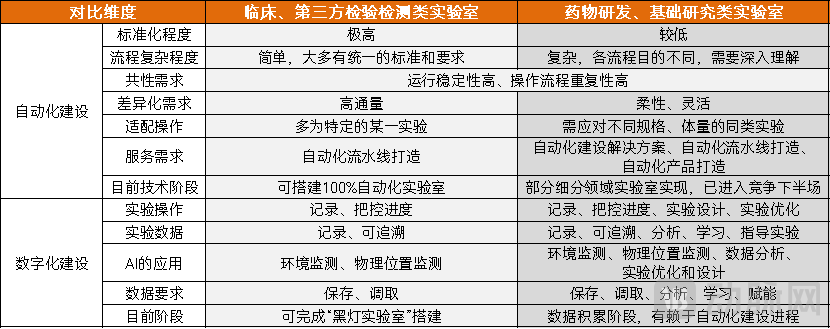

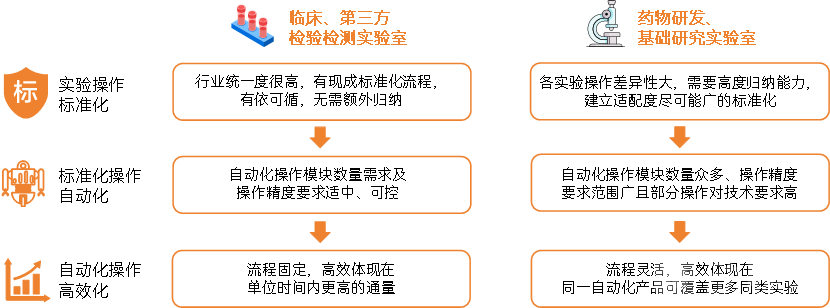

Varying degrees of standardization and differing volumes of decision-making requirements lead to diverse needs for intelligent infrastructure development.Strategies for laboratory intelligence in drug development and basic research differ from those in clinical testing, owing to differences in the standardization of operational procedures and the volume of analyses and decisions required during experiments.

Comparison of Products Required for Smart Laboratory Construction in Two Categories

When data reaches a “qualitative leap,” laboratory intelligence will achieve breakthrough development.Drug R&D laboratories are witnessing an order-of-magnitude increase in demands for digitalization and intelligence. Beyond monitoring physical locations and environmental conditions, there is a critical need to conduct multidimensional analysis of experimental data to generate insights that guide the optimization and execution of subsequent experiments, as well as the hypothesis and validation of experimental outcomes. Such advanced digital-intelligent infrastructure must be built upon a robust foundation of high-quality data. In addition to data from cutting-edge literature and academic papers, this foundation requires extensive real-world wet-lab data, encompassing both successful and failed experiments.

Currently, the collection and utilization of literature and paper data have become relatively mature. In contrast, data generated from real-world wet-lab experiments rely on efficient automation infrastructure to ensure both massive scale and high quality. In this domain, the industry is in a phase of rapid data accumulation. Once the data volume reaches a tipping point for qualitative transformation, the intelligent development of laboratories involved in drug discovery and basic research will achieve leapfrog progress. At that stage, self-driving dry-wet closed-loop laboratories powered by artificial intelligence will significantly reduce the trial-and-error costs associated with drug discovery and basic research.

Automation construction follows the same logic but adopts different implementation approaches.In the construction of automation, both types of laboratories follow the same underlying logic: first standardizing operations, then automating these standardized processes, and finally optimizing the automated workflows for greater efficiency. However, due to the differing ultimate missions of the two laboratory types, the intelligent infrastructure services required for each of these three stages vary accordingly.

Different Smart Construction Requirements for Two Types of Laboratories Under the Same Underlying Logic

During the automation implementation process, drug R&D and basic research laboratories require an additional “upfront” phase of summarization and standardization compared to testing and inspection laboratories. These laboratories exhibit a high degree of customization; however, extensive non-standard customized services are detrimental to the long-term development of enterprises. Therefore, companies must categorize myriad operations into minimal units to broaden the applicability of a single product suite. Examples include enabling random combinations of several experimental operational steps, allowing concurrent execution of different reagent preparation workflows, and automatically selecting subsequent operational procedures based on the results of preceding steps.

Smart Construction of R&D Laboratories Enters the Second Half, Gradually Penetrating Low-Standardization Operations.In the second half of the competition for smart laboratory development, automation will increasingly penetrate into operations with progressively lower levels of standardization. This trend will impose higher demands on industrial automation technologies and gradually raise the bar for enterprises’ ability to balance costs and investments.

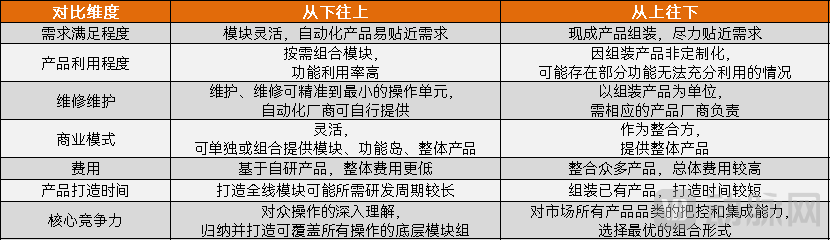

Currently, the mainstream product development models in the industry can be categorized into two approaches: “bottom-up” and “top-down.” The former involves understanding and decomposing underlying modules, then integrating them according to requirements to create the desired automated products. The latter entails establishing a framework for the required automated products first, then sourcing compatible components that meet the specifications, aiming to synthesize a product that closely aligns with the predefined framework.

Comparison of the Two Mainstream Models for Laboratory Automation in Drug R&D

In the “top-down” model, the greatest appeal lies in short product development cycles, low initial investment, and rapid monetization, offering certain advantages for quickly capturing market share when the early-stage market is relatively untapped. However, as more players enter the field, drawbacks such as inherent cost constraints and limited pricing power due to a lack of core technologies will become increasingly prominent. After all, the goal of automation is not full automation, but rather maximizing cost reduction and efficiency improvement. Therefore, according to survey data, the “bottom-up” model is currently more widely recognized.

Build an automated module suite with the finest operational granularity to establish core competitiveness.In the “bottom-up” model, the core competency lies in developing a suite of foundational modules that cover all laboratory operations, enabling service providers to flexibly select and integrate the most appropriate modules to meet demands with high quality.

To achieve this core competency, the fundamental requirement is a deep understanding of the numerous operations conducted in the laboratory, thereby leveraging industrial automation to enable machines to replicate the outcomes achieved by researchers. In product delivery and implementation, this model is also expected to significantly shorten the laboratory construction cycle due to the rapid integration of flexible modules.

Taking HanZanDi as an example, the company has adhered since its inception to meeting the personalized needs of laboratories by combining robust technical modules with rapid integration capabilities. HanZanDi categorizes life science experimental workflows into seven key segments: foundational innovation, design and implementation, task decomposition, core standalone instruments, application methods, core applications, and research domains. Each segment is further refined in detail, resulting in the development of over 80 modules to date. Leveraging this model, the company achieved the remarkable feat of completing delivery within six months for a large-scale automation project focused on high-throughput protein drug discovery and screening.

The design, development, and iterative refinement of numerous module groups is a time-consuming process that requires substantial investment. However, rich and comprehensive multi-module groups enable smart laboratory construction enterprises to precisely integrate the products needed according to specific laboratory requirements. This approach offers significant advantages in terms of user experience and cost efficiency, thereby injecting enduring core competitiveness into enterprises throughout the marathon of smart laboratory development.

3Unlocking AI Potential: Building Smart Laboratories with a “Software” Mindset

"World-Class Challenges" to Be Addressed in Smart Healthcare Development.In the overall development of smart laboratories, there is a growing consensus within the industry on solution frameworks. Automation initiatives are primarily driven by industrial technologies, while digital and intelligent transformation is spearheaded by the Internet of Things (IoT) and artificial intelligence (AI). Following this approach, it is evident that automation in the biopharmaceutical sector has advanced more rapidly overall. Since these laboratories mainly involve liquid-phase reactions, China’s current industrial technologies in pipetting are well-suited to meet laboratory requirements; moreover, the reaction conditions involved are relatively mild.

Comparison of Selected Dimensions in Biological and Chemical Laboratory Operations

In the field of chemical pharmaceuticals, the requirements for industry are more extensive and stringent.In the field of chemical experimentation, solid weighing is extensively involved. In traditional laboratories, manually weighing various types and forms of solid reagents is a tedious, time-consuming, and error-prone process. Solids that exceed the target weight are often non-recoverable (a frequent occurrence), leading to inevitable waste. Furthermore, the weighing of certain solids poses safety risks to operators. Additionally, it is difficult to avoid human errors amidst large volumes of repetitive weighing and recording tasks.

Automation has undoubtedly provided an effective solution; however, current automated solid weighing applications remain predominantly focused on powders. From an industrial perspective, the flowability and viscosity of such materials are more conducive to real-time weighing. In contrast, substances with more complex physical forms—such as oils, pastes, and flakes—are prone to compression, adsorption, moisture absorption, and static electricity generation, posing significant challenges for precise weighing. Consequently, the industry has long struggled to achieve automated weighing for these materials. Following the trajectory of industrial technology development, even if automated weighing for such substances becomes feasible in the future, the associated R&D costs would likely remain prohibitively high.

New Technologies Bring New Ideas, Leading Revolutionary Innovation.Currently, the industry is actively exploring and attempting to achieve equivalent outcomes through methods that can “replace” traditional industrial technologies, with AI demonstrating significant potential. According to research feedback, major breakthroughs have been made in the field of solid weighing by leveraging AI-based computer vision. In early 2023, Zhengcong Technology launched its fully self-developed, fully automated solid medication weighing and dispensing instrument. Relying on artificial intelligence machine vision technology and combined with mechanical methods such as vibration, stirring, electromagnetic forces, static electricity, and airflow disturbance, the system achieves precise weighing and dispensing for thousands of solid medications with varying physical properties. This innovative product not only addresses the “global challenge” of automating solid weighing in laboratories but also offers highly competitive pricing, thanks to Zhengcong Technology’s mature supply chain management capabilities for standardized products.

In the future, as data accumulation accelerates, AI will demonstrate even more promising potential in advancing laboratory automation and digital-intelligent transformation. It will progressively address currently unresolved challenges, optimize existing costly solutions, drive revolutionary innovations, and propel significant industry advancement.

1Expanding Testing and Inspection Products into Lower-Tier Markets, Entering the R&D Sector, and Tapping into Incremental Market Growth

Product penetration into lower-tier markets, proactively expanding incremental market share.In the field of clinical laboratory testing, beyond passively waiting for opportunities to replace imported systems with domestically produced ones as existing automated lines in tertiary medical institutions reach the end of their service life, product penetration into lower-tier markets represents a more proactive market-oriented strategy for smart laboratory manufacturers. According to research, many county-level people’s hospitals and secondary hospitals in China are actively introducing automated laboratory lines following expansion and renovation projects, providing domestic smart laboratory manufacturers with a favorable opportunity to enter this growing market segment.

Venturing into R&D laboratories to seek broader market opportunities.While the expansion of products into tier-2 and lower-tier medical institutions has undoubtedly broadened the market for the smart development of clinical testing laboratories, this incremental growth has been insufficient to offset the rapid contraction in market demand following the pandemic, driven by a sharp decline in nucleic acid testing needs. Survey data indicate that companies whose primary revenue stems from the construction of automated assembly lines for clinical testing have experienced an average post-pandemic turnover decline of over 50%, prompting them to explore new frontiers.

Currently, another major trend is that companies in the sector are gradually “venturing into” research and development (R&D) laboratories. Leveraging their robust R&D capabilities, these companies are entering the market through similar underlying operational modules and progressively exploring smart laboratory construction solutions for drug discovery and basic research laboratories, aiming to deliver greater value in the relatively untapped blue-ocean market of smart laboratory development.

2Demand-Driven + Co-Creation with Industry Leaders: Accelerating the Exploration of New Frontiers in Drug R&D

Start by gradually penetrating from the "maximum intersection" of demand.For laboratories, the construction of smart infrastructure is typically carried out in stages. The initial areas to undergo smart transformation are those with clearly defined standards and regulations, as well as operational processes centered on “red-line” issues such as ensuring laboratory safety.

In addition, laboratory operational modules will be developed sequentially in descending order based on three dimensions: standardization, operational repeatability, and reliance on manual labor. Priority for intelligent automation upgrades will be given to those modules with higher levels of standardization and operational repeatability (i.e., more frequent application), and where the cost of implementing smart solutions is lower than that of traditional manual operations.

Thus, guided by this “penetration” sequence, companies dedicated to the intelligent transformation of drug R&D laboratories will prioritize product development around operational modules that comply with relevant standards and regulations and address laboratory “red-line” issues. Meanwhile, they will conduct an in-depth understanding, decomposition, and synthesis of the needs across various drug R&D laboratories, rank the “intersecting needs” from largest to smallest, and then match them with their own technological strengths to identify the operational module representing the “largest intersection” suitable for their capabilities, thereby creating flagship products.

For instance, against the backdrop of rapid advancements in regenerative medicine, synthetic biology, and cell and gene therapy, the demand for cell culture has intensified. Nevertheless, this step still relies heavily on manual labor in many laboratories. The success rate and quality of cell culture depend on the operator’s experience and proficiency, making the process time-consuming and labor-intensive. Amid the surge in demand for clinical and laboratory cell culture, achieving efficient, high-quality cell culture has become a common challenge faced by laboratories in the life sciences sector.

Some companies with keen market insight have already begun to lay out their relevant product portfolios. For instance, AceMan, the flagship fully automated cell preparation system developed by Chuangze Bio, was included in the “2023 Shandong Province List of First-Set (Batch) Technical Equipment and Key Core Components Enterprises and Products” in November 2023. AceMan enables automated, standardized culture of both adherent and suspension cells, freeing up three researchers and achieving uninterrupted 24-hour multi-type cell culture. Moreover, its analytical results demonstrate over 95% consistency with those obtained by cell culture operators with more than three years of experience.

Co-create with industry leaders to build products that better align with real-world needs.In the current relatively early-stage market, rapid market positioning is crucial. Specifically, this entails how to more quickly develop products that closely align with market demands, how to adapt a single product to a wider range of application scenarios to capture a larger market share, and how to rapidly establish industry awareness and secure a steady stream of orders.

According to research, co-creation with leading enterprises is one of the advantageous strategies. Leading enterprises can provide a sufficient number of application scenarios, enabling companies to obtain more comprehensive and rich information, so as to summarize operational modules that are more comprehensive and closer to real needs. This can greatly shorten the product verification and refinement cycle, saving product R&D costs.

For instance, USTC entered the field of chemical drug R&D by collaborating with leading CROs to co-develop a series of automated process products, including solid powder weighing and dispensing, liquid-liquid extraction, and vacuum concentration systems, as well as small-scale automation equipment such as automatic bottle feeders and microplate labeling machines. Its product portfolio includes standalone benchtop instruments and integrated workstations designed for fully automated laboratory environments. By overcoming the limitation of performing only single tasks, these systems can execute multiple tasks simultaneously, meeting experimental research needs across various throughput levels.

Beyond enabling rapid mastery of product features and minimizing R&D detours, leading companies serve as references or even benchmarks for other players in the field, making co-developed products more adaptable to a wider range of market application scenarios. Moreover, once a product is successfully developed and deployed, its industry influence cannot be underestimated. This approach offers a “shortcut” to addressing the highly non-standardized nature of laboratory operations in drug development. As the industry gradually reaches consensus and an increasing number of operational modules become standardized, the pace of smart laboratory construction will accelerate significantly.

3Drug R&D Attracts a Wave of Entrepreneurs, with an Even Larger Market Emerging Post-Pandemic

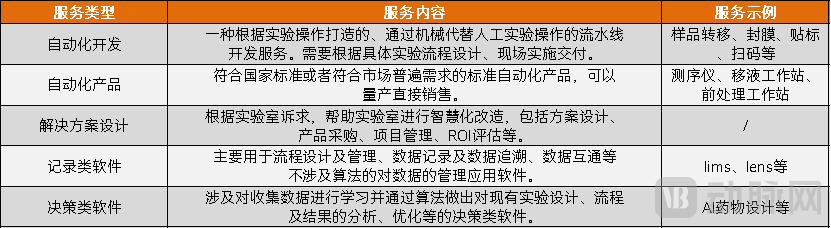

Five Smart Services, Combined to Meet the Diverse Needs of Various Laboratories. Currently, the services supporting the intelligent development of laboratories can be broadly categorized into five types: automated assembly lines, automated products, solution design, documentation software, and decision-support software.

Five Major Service Categories for Smart Laboratory Construction

Demand Aligns with Market Service Capacity; Smart Drug Development Takes the “Headline” Spotlight.The three main entities of smart laboratories are categorized as testing and inspection laboratories, biopharmaceutical drug R&D laboratories, and basic research laboratories in universities and research institutes. Due to differences in market size, task attributes, and revenue performance, these three entities have varying service demands in the process of laboratory intelligence transformation.

Demand Levels for Five Major Service Categories Across Various Laboratories

For drug R&D laboratories, intelligentization offers sufficient cost and efficiency optimization, providing the impetus for smart transformation. Coupled with the high alignment between laboratory needs and current market service capabilities, this has given laboratory managers ample confidence in pursuing intelligent infrastructure development. Furthermore, in biology laboratories primarily focused on liquid handling, domestic pipetting technologies—whether in terms of channel count or minimum operational units—are highly compatible with laboratory requirements and can meet relevant compliance standards with high quality, thereby accelerating the intelligentization process. In contrast, chemistry laboratories involving more solid-phase operations require additional time to refine their processes due to the greater complexity of experimental procedures; nevertheless, continuous breakthroughs and innovations within the industry are steadily advancing the overall intelligentization journey.

Post-pandemic, the smart laboratory sector has emerged with greater market potential.The pandemic has accelerated the digital transformation of clinical testing laboratories, significantly boosting automation levels in this niche sector. While the other two types of laboratories have not seen direct manifestations of such smart upgrades, the importance of building smart laboratories has been greatly elevated, serving as a milestone “market education” for the industry.

Post-pandemic, the substantial market demand potential cultivated within drug R&D laboratories will be unleashed at an accelerated pace, while the service capabilities of smartization enterprises, honed through market competition, will be better positioned to meet flexible needs. In the future, life sciences—particularly drug R&D laboratories—will emerge as the next niche segment for the rapid development of laboratory smartization.

Not

Completing domestic substitution and even surpassing foreign counterparts, more open intelligent products are the general trend

Rapid Data Accumulation Makes the Rise of Self-Driving Laboratories with Dry-Wet Closed Loops Irresistible

In-House Core Technologies Paired with Industrial Collaboration to Balance Product R&D and Commercialization

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1: The Track Is Still in Its Early Stages, with Drug R&D Demonstrating Strong Intelligent Appeal

1.1 The Spiral Development of Automation and Digital Intelligence: An Urgent Need for High-Quality Data in the Industry

1.2 Although the sector as a whole is still in its early stages, clinical laboratory testing has already become a red ocean

1.3 In the Post-Pandemic Era, More “Flexible” Smart Infrastructure Initiatives Are Gaining Favor with Capital

Chapter 2 Deep AI Integration: Upholding In-House R&D as the Core and Accelerating Data Accumulation

2.1 It is an industry consensus to adhere to self-developed, deeply AI-integrated open testing and inspection laboratories

2.2 The Second Half of Intelligent Drug R&D: Data Accumulation and Foundational Modules

2.3 Unleashing AI Potential: Building Smart Laboratories with a “Software” Mindset

Chapter 3: Diagnostic Products Seek Incremental Growth in Lower-Tier Markets, While Drug R&D Scenarios Are Poised to Rise

3.1 Extending Testing and Inspection Services to Lower-Tier Markets, Entering the R&D Sector, and Expanding into Incremental Markets

3.2 Driven by Demand + Co-Creation with Industry Leaders to Accelerate the Exploration of New Frontiers in Drug R&D

3.3 Drug Development Attracts Numerous Entrepreneurs, with a Larger Market Emerging Post-Pandemic

Chapter 4 Future Trends

4.1 Achieving domestic substitution and even surpassing foreign counterparts, with more open and intelligent products, is the general trend

4.2 Rapid Data Accumulation: The Rise of Self-Driving Laboratories with a Dry-Wet Closed Loop Is Unstoppable

4.3 In-house Development of Core Technologies Combined with Industrial Collaboration to Balance Product R&D and Commercialization

Chapter 5 Corporate Case Studies

5.1 Hanzandi: Powerful Underlying Modules + Rapid Integration Capabilities, Leading the Way in End-to-End Intelligent Solutions

5.2 MGI Tech – Innovating Intelligent Manufacturing to Lead Life Sciences, Becoming the Creator of Core Tools for Life Science Technology

5.3 Zhengcong Technology: Leveraging AI Vision Machine Technology to Break the International Patent Blockade on Solid Dispensing and Weighing

5.4 Chuangze Biotech – Fully Automated Cell Intelligent Manufacturing, Driving the Development of Smart Biological Laboratories

5.5 USTC – Manufacturer of Unmanned Smart Laboratories and Laboratory Automation Products

Special Acknowledgments (in order of interview):

Dr. He Dan, CMO of Hanzandi; Mr. Wu Junwei, Founder and CEO of Zhengcong Technology; Professor Wang Zenan, Co-founder of Chuangze Biology; Mr. Hou Mingtao, Founder of Ustek; Mr. Lin Siyuan, Director of the Business Development Center at MGI Tech; and Ms. He Ying, Project Manager of the Business Development Center at MGI Tech.

Please scan the QR code to add our assistant and obtain the full report. If you have already added us, please proactively reach out for assistance.