From Periphery to Core: Medical AI Surges into Therapeutics

After more than a decade of exploration, AI has gradually evolved into the form that IBM Watson once envisioned. It has even transcended the realms of diagnosis and treatment, taking root in every corner of healthcare settings.

However, implementation and commercialization in the field of medical AI are two distinctly different concepts. The deployment of AI through collaboration and joint research does not necessarily mean that the algorithm can be applied on a large scale in hospitals, nor does large-scale hospital deployment guarantee that the substantial prior investments can be successfully recouped.

Due to the existence of these ambiguous concepts, the commercialization landscape of medical AI has always been shrouded in ambiguity, making it difficult to distinguish the actual progress of individual companies.

Based on this current landscape, VCBeat has conducted a comprehensive survey and analysis of the medical AI sector, aiming to leverage data to present an authentic picture of medical AI in 2023.

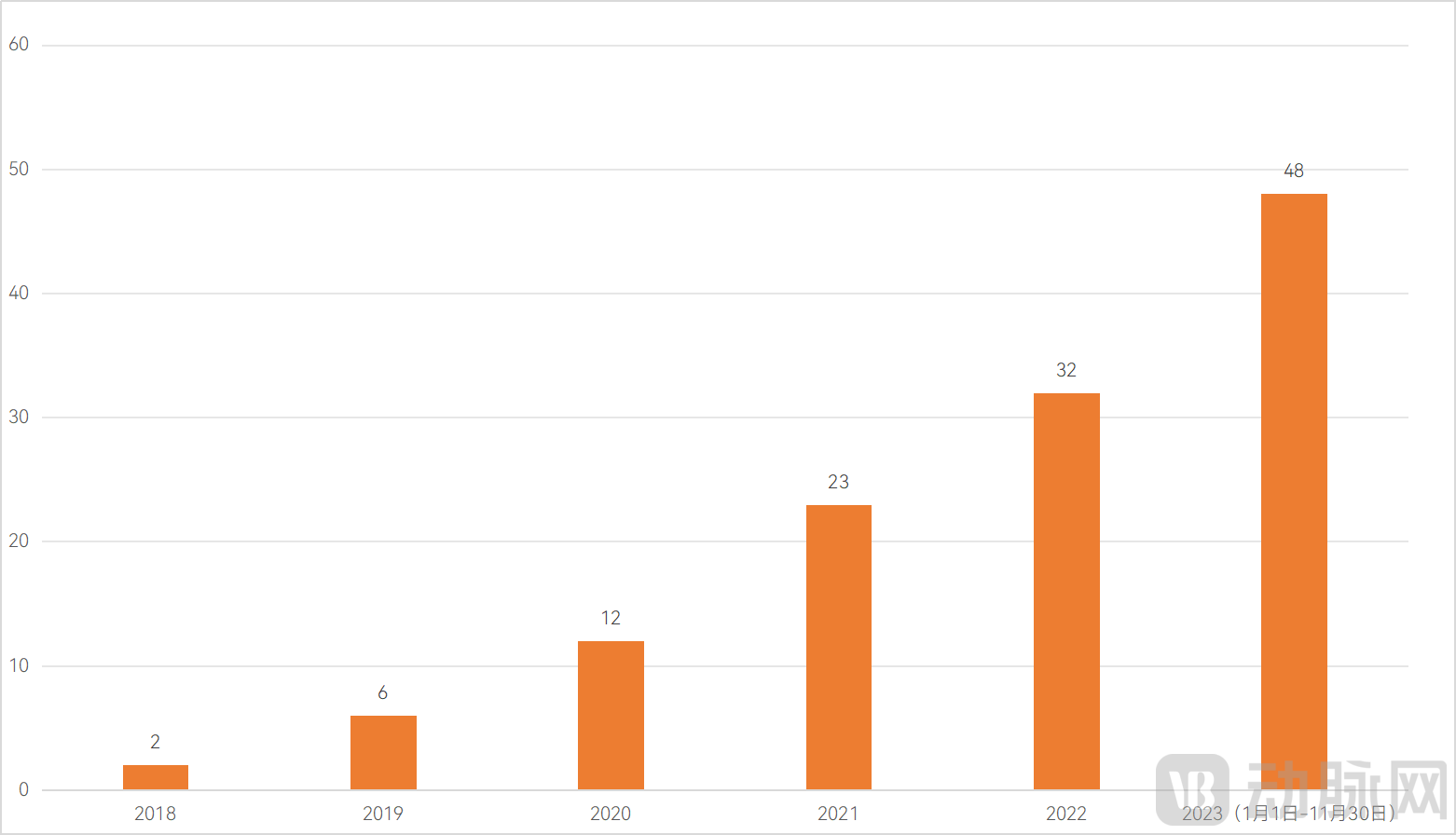

Over the past six years, the annual number of approved registration certificates for Class III medical devices has maintained rapid growth, with no signs of slowing down. Before the year’s end, review and approval data have already signaled to the market that this is the best year yet for market access performance in the imaging AI sector.

As of December 1, 2023, a total of 122 intelligent software products had obtained market access in China. In the first 11 months of 2023, the National Medical Products Administration (NMPA) announced a total of 48 review and approval cases, surpassing the 32 cases recorded in 2022. With this progress, the review and approval system for AI-based medical imaging has matured, and the registration and market access of related AI technologies have become routine. Intelligent applications are expected to cover the entire clinical system within the next few years.

Number of Class III Medical Device Registrations Approved for AI Products by Year

A Detailed Analysis of the Distribution of AI Registration Certificates Over the Years. From 2020 to 2021, approved imaging AI products were predominantly auxiliary diagnostic AI systems, incorporating deep learning-based analysis modules designed for specific diseases on specific imaging equipment. In 2022, auxiliary diagnostic AI remained the mainstream; however, there was a notable increase in applications for radiotherapy planning, electrocardiogram (ECG) analysis, and pathology analysis, further broadening the scope of AI application scenarios.

In 2023, the previous trend continued, with the distinction that various intelligent surgical robots for planning and navigation applications were successively approved (a total of 10 models), significantly increasing the total number of AI-approved products. The main scenarios for medical AI have also shifted from "assisted diagnosis" to "parallel assisted diagnosis and treatment."

From a corporate perspective, AI companies specializing in computer-aided diagnosis still hold the largest number of Class III medical device registrations. Shukun Technology currently ranks first with 12 Class III certificates. United Imaging Group ranks second (with United Imaging Intelligence holding 7, United Imaging Healthcare holding 3, and United Imaging Zhirong holding 1). Deepwise Medical ranks third with 9 certificates, followed closely by Infervision, Pulse Medical, and Yizhun Intelligence. In contrast, AI companies focused on computer-aided treatment generally hold only 1–3 Class III certificates, indicating relatively slower progress in market access.

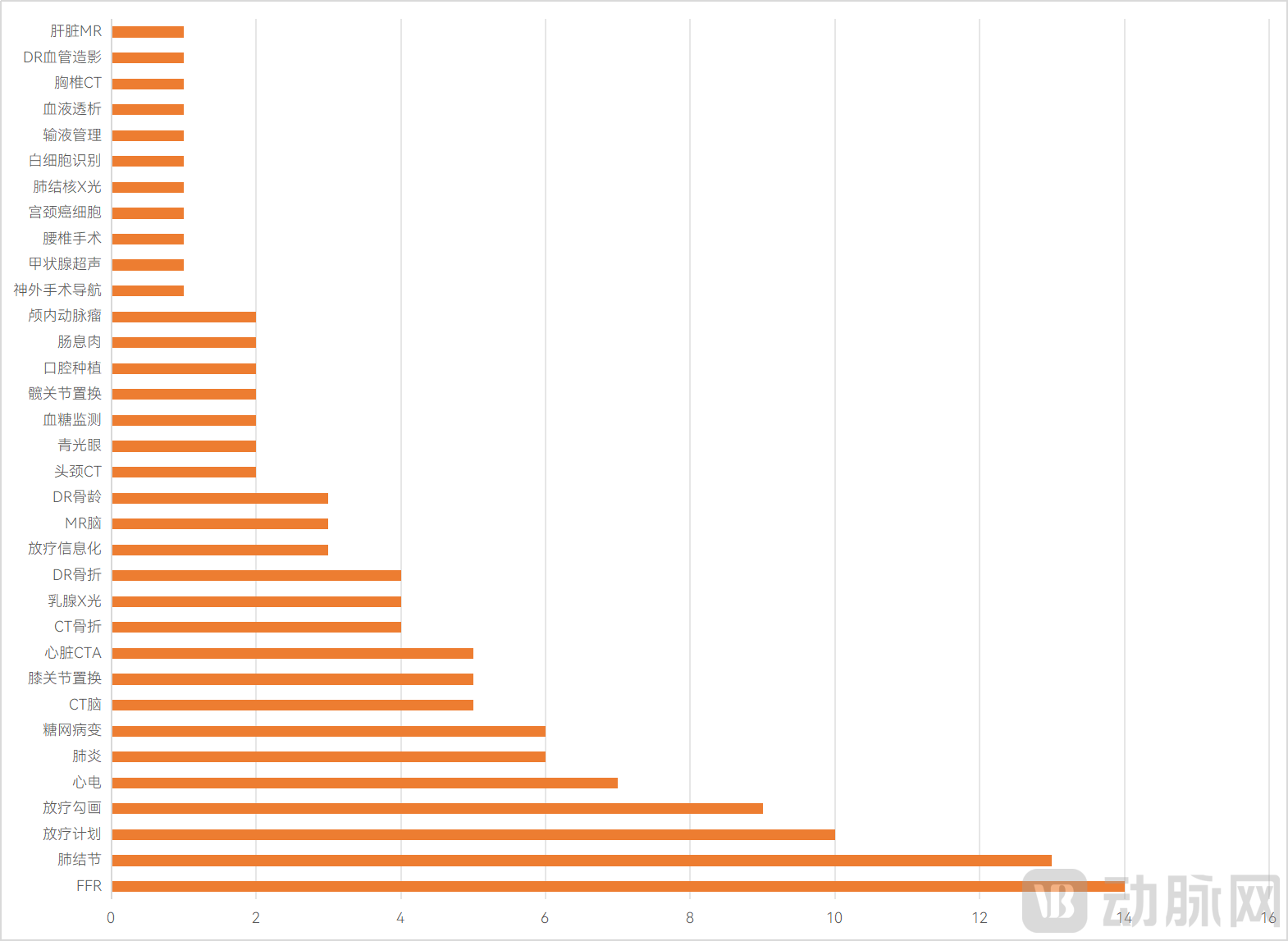

From the perspective of disease categories, AI solutions for conditions supported by public datasets—such as pulmonary nodules, pneumonia, and fundus diseases—are the easiest to obtain regulatory approval and have become a key driver for companies to achieve AI commercialization. The newly approved Class III medical device certifications predominantly originate from the surgical treatment sector. Breakthroughs in lumbar spine, hip joint, knee joint, aneurysm, stomatology, and neurosurgery have brought new growth to this track. However, given the temporary cooling of the surgical robot market in the second half of 2023, the number of registrations for intelligent planning and navigation applications in 2024 may decline.

Approval Status of Class III Medical Device Certifications for AI-Based Medical Products Across Different Disease Indications

Breakthroughs are also emerging in the field of radiation therapy. In the past, companies developing related intelligent technologies were predominantly leading domestic imaging enterprises and global radiotherapy giants; however, over the past two years, startups have successively gained market access, becoming a significant force in this sector.

Ultrasound is considered the next growth driver for medical AI, having already achieved breakthroughs in regulatory approval. In August 2023, Deshang Yunxing’s ultrasound imaging software for auxiliary diagnosis of thyroid nodules became the first to receive approval from the National Medical Products Administration (NMPA). AI ultrasound solutions from Yizhun Intelligence and Deepwise Technology are also expected to gain approval in subsequent phases.

Furthermore, domestic miniaturized ultrasound hardware and software are continuously evolving. For instance, Deepwise Technology is dedicated to promoting ultrasound screening in primary healthcare settings and has established a comprehensive layout in the intelligent miniaturization of ultrasound systems. Currently, Deepwise Technology has built an imaging database featuring algorithmic models for over ten categories and more than 30 disease types, along with a cloud-based ultrasound imaging center, enabling AI-assisted ultrasound diagnosis for over twenty conditions. With the breakthrough approval of Class III medical device certificates for ultrasound AI, the application of ultrasound AI is poised for further expansion.

The development of intelligent surgical robot planning and navigation applications is deeply intertwined with the advancement of surgical robots. Over the past two years, the accelerated approval of surgical robots in specialized fields such as orthopedics, endoscopy, pan-vascular surgery, percutaneous puncture, and dentistry has spurred continuous innovation in related intelligent applications. However, given the temporary cooling of the surgical robot market in the second half of 2023, the number of registrations for intelligent planning and navigation applications in 2024 may decline.

In the transition toward treatment empowerment, startups have played a significant role in diversifying AI applications. Taking the application of AI in radiation therapy as an example, companies previously developing related intelligent technologies were mostly leading domestic imaging enterprises such as Neusoft ZhuiRui, United Imaging Healthcare, DA Yi Group, and global radiation therapy giants like Elekta, Varian, and Accuray. However, in the past two years, startups such as Bosh Medical, MANTEIA, Lianxin Medical, and Yinuo Intelligence have successively gained market access.

A similar trend is evident in surgical interventions. Startups such as United Imaging Intelligence, Keya Medical, Naton Medical, and Changmugu Medical have obtained approval for Class III medical devices in fields including dentistry and orthopedics. Meanwhile, established AI-assisted diagnostic companies like Deepwise Healthcare, Shukun Technology, and Infervision are exploring opportunities to expand into new product lines.

While the commercialization of AI in life sciences has tightened, R&D efforts have not lagged behind.

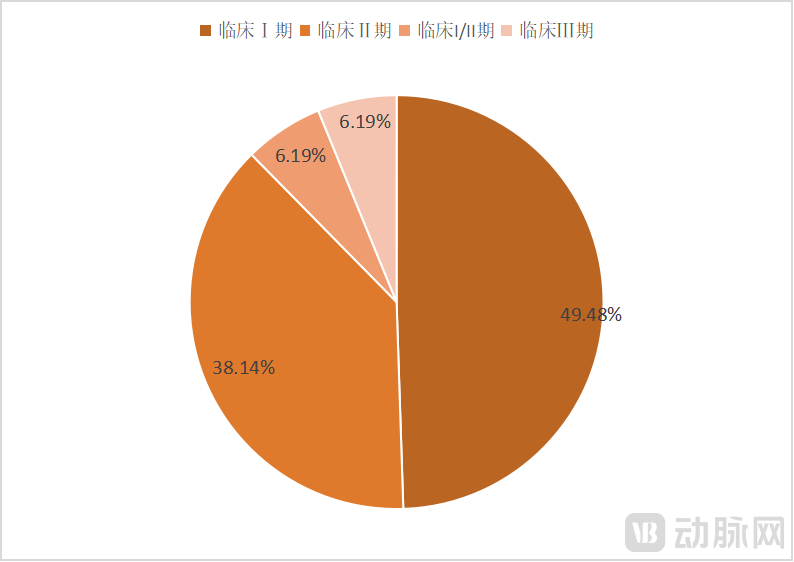

According to incomplete statistics from VCBeat, as of November 2023, 16 AI-driven life science pipelines that had entered clinical trials were either discontinued or removed from official websites, and one drug candidate had its clinical trial priority downgraded. Nevertheless, the total number of pipelines continues to grow rapidly. Globally, there are 97 active AI-involved pipelines in the clinical stage, with more than half in Phase I clinical trials and over one-third in Phase II clinical trials.

Global Distribution of Clinical Stages for Active AI-Involved R&D Pipelines in Clinical Trials

(Incomplete statistics, as of October 2023)

Of these pipelines, 67 originate from abroad, accounting for 69.07%, while 30 are domestic, representing 30.93%. Companies such as Insilico Medicine, Calcite Biosciences, Xbiome, Elicio Therapeutics, Drug Farm, and Rigor Pharmaceuticals have multiple pipelines undergoing clinical trials simultaneously, propelling China into the ranks of global leaders in AI-driven drug discovery.

In-house drug development is the primary model for AI-driven life sciences companies in developing new drugs. Among the aforementioned pipelines, 85.57% are self-developed by the enterprises, while 14.43% are co-developed, primarily involving AI-driven life sciences companies assisting large pharmaceutical firms in R&D.

Although the number of co-developed pipelines is small, they are predominantly held by established AI-driven life sciences companies. Exscientia’s two clinical-stage pipelines originate from Bristol Myers Squibb and Pylon Bio; Insilico Medicine is advancing Aulos Bioscience’s monoclonal antibody AU-007; Lantern Pharma holds pipelines from TTC Oncology, Harmonic, and Actuate Therapeutics; and Schrödinger has partnered with Structure Therapeutics on ANPA-0073 and GSBR-1290, as well as with Morphic Therapeutic on MORF-057.

Among the aforementioned pipelines, drugs already marketed and handled by AI companies such as Schrödinger and BioXcel Therapeutics were all acquired, and those in Phase III clinical trials are mostly repurposed existing drugs. In other words, self-developed pipelines from life science AI companies that have entered clinical stages are all in Phase I or Phase II, with no drug having yet completed the full clinical trial process.

For AI companies in the life sciences sector, the only way to generate substantial revenue and create significant value is to independently develop or assist multinational corporations (MNCs) in bringing approved drugs to market. In 2023, no drug meeting these criteria advanced beyond Phase II clinical trials, which somewhat dampened market valuations for life science AI firms and led to a tightening of collaborations and investments throughout the year.

Compared with the innovative markets pioneered by medical imaging and life sciences, AI in informatics faces a relatively traditional market lacking flexibility for innovation, thus giving rise to differentiated R&D strategies.

In medical imaging and life sciences, AI serves as the core technological foundation, forming independent products or solutions. In contrast, within health informatics, with the exception of specialty-specific Clinical Decision Support Systems (CDSS) that are marketed as standalone products, the vast majority of AI applications exist as supporting technologies. These are embedded within mature products or solutions to enhance competitiveness by optimizing performance and providing additional services.

Nevertheless, this characteristic has not dampened the enthusiasm of medical IT enterprises for developing informatics AI. On one hand, leading medical IT vendors such as Winning Health, Neusoft Group, and Donghua Medical have adjusted the architecture of their Hospital Information Systems (HIS) to better accommodate intelligent applications, facilitate smarter hospital management, and continuously reduce the likelihood of errors in daily hospital operations. On the other hand, the rise of digital therapeutics has enhanced AI capabilities in scenarios such as human-computer interaction, scale analysis, intelligent early warning, and quality control, enabling informatics AI to expand into the therapeutic domain and further unlock the value of digital intelligence.

Although the pathways vary, AI-enabled imaging, life sciences, and informatics are each striving in their own ways to empower the therapeutic sector. It is worth noting that this trend has significantly influenced the financing landscape of medical AI in 2023.

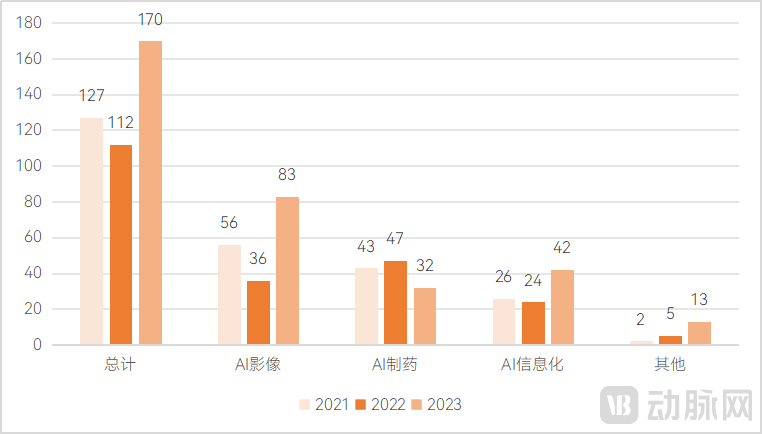

According to statistics from VCBeat Research Institute, a total of 170 financing deals were completed in the medical AI sector during the period from August 31, 2022, to October 31, 2023 (hereinafter referred to as the “2023 Statistical Year”), with a total financing amount of RMB 16.124 billion.

The number of financing events in the 2023 statistical year saw a significant increase compared to 127 in the same period of 2022 and 112 in the same period of 2021. This growth can be attributed to the transition from AI-assisted diagnosis to AI-assisted treatment, as well as the rise of AI-based image-guided surgical navigation and surgical planning solutions, which collectively drove up the financing scale for companies specializing in AI medical imaging and AI-driven healthcare informatics.

Financing Trends Across Different Medical AI Sectors

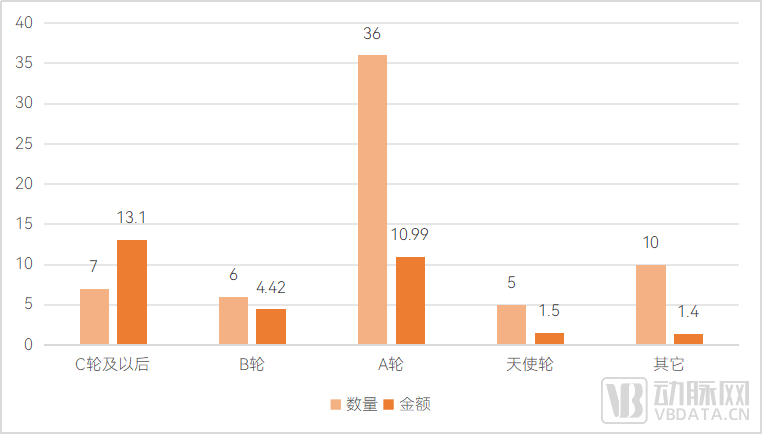

AI medical imaging financing is currently more focused on commercial implementation. Even at the early Series A funding stage, product registration and commercialization status have become important considerations for capital investment. For example, Yizhiying has completed its Series A funding, and its product "RT-Mind Radiation Therapy Contouring Software" has obtained NMPA Class III medical device registration certification and FDA market clearance; Huiwei Intelligence is in the Series A funding stage, and its Class II certified products are already being used in multiple hospitals.

Number and Amount of AI Medical Imaging Financing Rounds by Stage (Unit: RMB 100 Million)

The strong performance of AI companies specializing in head imaging has contributed positively to this financing landscape. According to statistics from VCBeat, AI firms such as Deepwise, Yizhun Medical, Shukun Technology, Airdoc, Infervision, and ShenZhiTouYi have all achieved annual revenues exceeding RMB 100 million, with some expected to turn profitable in 2024.

Taking DeepWise Medical Imaging as an example, the company has accelerated its strategic expansion across markets in China, the United States, and Europe. Its AI products have been deployed in over 500 medical institutions and imaging centers worldwide, with total global orders approaching RMB 100 million. Recently, this leading enterprise in the field of AI-enhanced medical imaging announced the launch of its new brand, “DeepWise Medical Imaging,” in the Chinese market. At the Chinese Congress of Radiology (CCR) and the Radiological Society of North America (RSNA) annual meeting, it showcased the intelligent upgrading of the medical imaging industry powered by its AI platform.

MANTEIA achieved rapid commercialization by simultaneously expanding into domestic and overseas markets. Currently,Manteia has served over 1,000 hospitals domestically and internationally, including renowned medical institutions such as Peking Union Medical College Hospital, the Chinese PLA General Hospital, Shandong Cancer Hospital, and the Mayo Clinic in the United States. The company’s products have obtained three Class III certifications and one Class II certification from China’s National Medical Products Administration (NMPA), four approvals from the U.S. Food and Drug Administration (FDA), two CE markings in Europe, and four additional approvals in other countries and regions. By delivering high-quality products to multiple global markets, Manteia is building international competitive advantages and leveraging technology to steadily advance the field of precision radiotherapy.

Yizhun AI emphasizes the parallel deployment of multi-scenario applications across tertiary hospitals and primary healthcare institutions. Through collaborations with multiple provincial and municipal governments, Yizhun AI has achieved large-scale implementation of its three core solutions—namely, the “Zhi Zai Quan Neng” comprehensive intelligent imaging solution, the “Fen Hong Guan” AI-powered integrated screening, diagnosis, and treatment solution for breast cancer, and the “What You See Is What You Diagnose” real-time dynamic intelligent ultrasound analysis platform—thereby generating substantial revenue.

Shukun Technology’s extensive product portfolio serves as a key safeguard for its revenue. Currently, the Digital Human Platform 2.0 has accumulated more than 40 AI products, covering multiple imaging modalities such as CT, MRI, DR, ultrasound, DSA, and mammography. It also comprehensively addresses all stages of screening, diagnosis, and treatment for various major and chronic diseases, enabling high-precision, coordinated navigation throughout the entire disease management pathway and facilitating precise diagnosis and therapy.

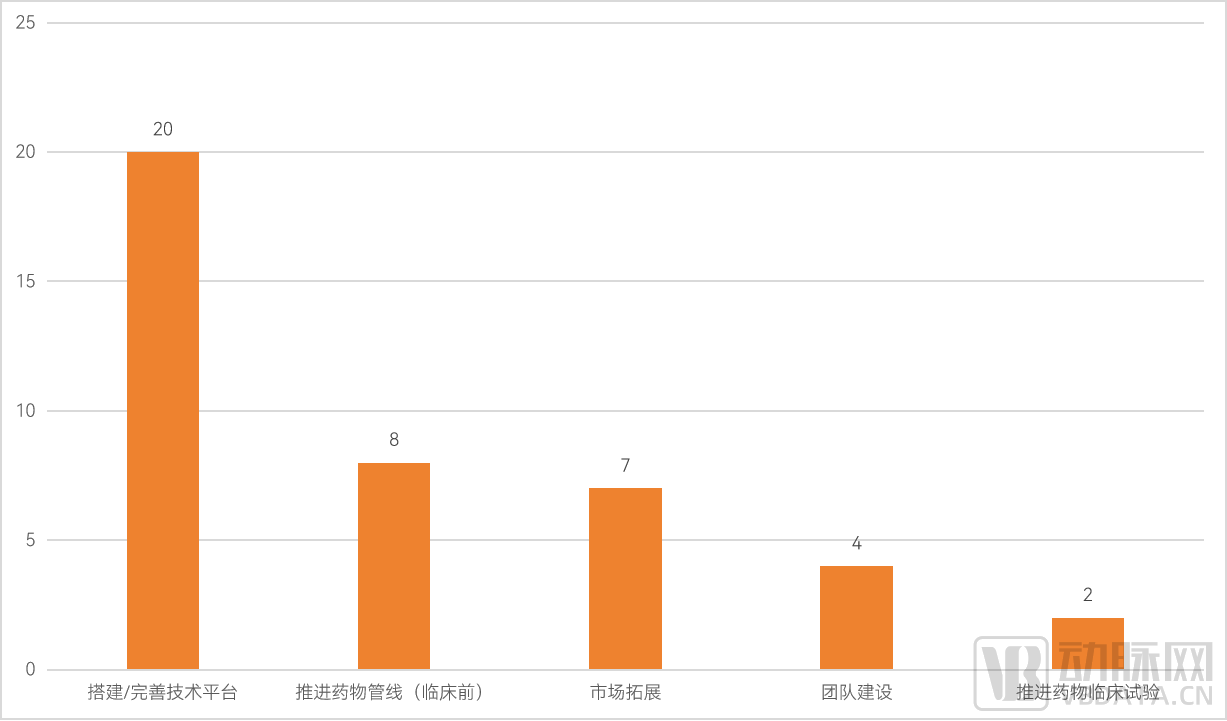

AI Drug Discovery Sector Experiences Its First Cooling in Financing. The number of financing events in the 2023 statistical year was only 32, representing a notable decline from 43 in the same period of 2021 and 47 in 2022. Furthermore, financing activities in the AI drug discovery sector during 2023 were predominantly concentrated in projects at pre-Series A stages.

The core reason is that AI-driven drug discovery remains some distance from commercialization, with a lack of typical success stories in the industry. Furthermore, the failure of the high-profile candidate DSP-1181 in 2022 cooled investor enthusiasm. According to statistics, among the uses of financing funds, only Drug Farm (Yaowu Muchang), which completed its Series C round, and Hongyun Biotech, which completed its Series B+ round, allocated capital to advancing clinical trials. The remaining financing activities were at earlier stages, primarily directed toward building technology platforms and conducting preclinical drug research.

Figure 16. Uses of AI Drug Discovery Financing in 2023

Financing events in the health informatics sector saw a slight increase in 2023, with a total of 42 deals. Most traditional health informatics companies have reached later stages of development, and the industry as a whole has remained relatively stable. A notable highlight was the rise of digital therapeutics companies, which accounted for 25% of AI-driven health informatics financing events in 2023.

Generative AI has also seen initial exploratory applications in the informatics sector. Glowe has completed its Series A+ financing round, leveraging AIGC to empower psychological counseling. Wanmu Health has secured strategic funding to accelerate the development of single-disease and physician-specific knowledge databases, reconstruct content creation workflows within doctor-patient interaction scenarios through AIGC, and explore practical applications of vertical large language models.

Compared to the primary market, changes in the secondary market are relatively smaller.

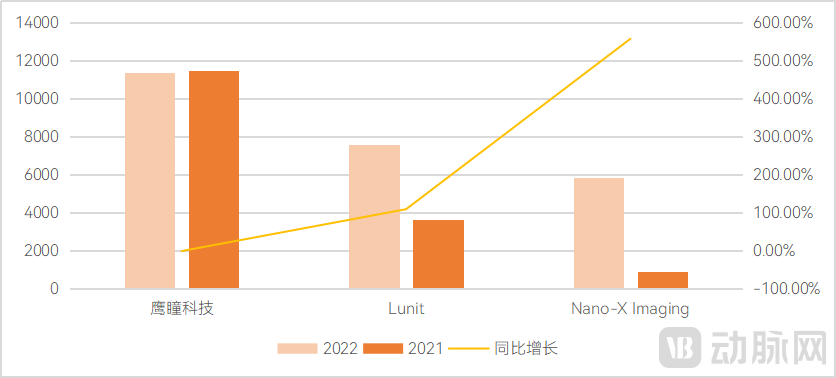

An analysis of three representative medical AI companies, both domestic and international: Airdoc, Lunit, and Nanox AI. In terms of revenue, Airdoc remained flat compared to the previous year, while Lunit and Nano-X Imaging achieved growth at a certain scale.

Comparison of Revenue Data for Medical AI Companies (Unit: 10,000 RMB)

Airdoc2022 revenue was RMB 114 million. AirdocConstrained by restrictions on offline activities during the pandemic, such as itsShanghai, a key city in its strategic layout, has previouslyThe company was closed for three months in the first half of 2022 due to the pandemic, which adversely affected its full-year revenue. Annual report data show that the number of clients increased from 244 in 2021 to 397, representing a year-on-year growth of 62.7%. A total of 4.3298 million tests were conducted. Although the testing volume decreased by 12% compared with 2021, the average fee per test rose by 4.5%, indicating strong momentum in development.

Airdoc’s interim performance in 2023 also sent a positive signal to the industry. The company’s revenue in the first half of 2023 reached RMB 82.5 million, representing a year-on-year increase of 120.6%. Revenue from Airdoc Medical, Airdoc Health, and Airdoc Eye Health grew by 137.3%, 26%, and 307% year-on-year, respectively. Gross profit amounted to RMB 51.36 million, up 132.7% year-on-year, while net loss narrowed by 58.8% year-on-year to RMB 41.02 million. The gross margin stood at 62.3%, an increase of 3.3 percentage points. Driven by the increasingly rigid demand for eye health management and treatment among hospitals and patients, the commercial value of AI-based ophthalmic imaging is maturing and gaining accelerated recognition from hospitals, physical examination institutions, and health management centers.

Furthermore, AI companies have maintained relatively low debt-to-asset ratios, and many have already identified effective pathways to control losses. For these AI firms, which are still in the early stages of commercial expansion, sound financial health means they have several years of runway for trial and error, ultimately enabling them to establish a reliable and sustainable path to profitability.

So, where might the opportunities reflected in the financial data lie? Let us begin by analyzing the current challenges facing AI.

Although the value of medical artificial intelligence (AI) has been preliminarily validated in clinical practice and pharmaceutical development, with many medical AI products becoming an integral part of physicians’ daily workflows and demonstrably improving efficiency in screening for drug targets and lead compounds, healthcare AI companies still face operational challenges.

The reasons behind this outcome are multifaceted. First, for AI in medical imaging, the core issue to address is how much efficiency AI can enhance and what value it can create for hospitals; for AI in life sciences, the central question is whether AI can develop a new drug that successfully reaches the market. Currently, lacking support from health insurance payment models and without any approved drugs developed through AI as case studies, the multiple cost components associated with AI adoption remain, while the validation of its value is still unresolved and has not been precisely quantified.

Second, the content and form of many AI products/solutions are overly homogeneous, making it difficult for hospitals/enterprises to justify significant investment in a single product. Pharmaceutical companies have also failed to perceive tangible cost savings from AI adoption. In other words, these products have not yet reached a level capable of transforming the entire industry, thereby proving insufficient to drive customer purchasing decisions.

Third, there are inherent issues with medical AI technology itself. For instance, encapsulating AI stifles its advantage of continuous evolution in practice. Conversely, if AI is not encapsulated and clinicians intervene with patients after receiving AI recommendations, the AI fails to capture the outcomes that should have occurred given the input data. In such scenarios, the AI system, despite achieving high prediction accuracy in the short term, will gradually deviate over time, leading to progressively deteriorating predictive performance.

In 2023, various forms of commercial, business model, and technological innovations emerged in an attempt to address the aforementioned challenges.

A typical model innovation stems from the SYNTAX score criteria and scoring system. This system serves as a core scoring standard throughout the diagnosis and treatment of coronary artery disease; however, in practice, it presents challenges such as difficulty in scoring, heavy reliance on experience, time consumption, strong subjectivity, and difficulty in ensuring accuracy.To improveTo enhance the speed and accuracy of SYNTAX scoring and broaden its clinical application, Yuewei Medical, an innovative medical device R&D company, has developed an AI-powered automated SYNTAX scoring tool.It can significantly enhance the precision of disease assessment in patients with coronary heart disease, providing robust support for preoperative risk stratification, intraoperative surgical planning, and postoperative prognosis estimation.

Large language models, generative AI, and their related applications are significant technological innovations this year.Deepwise Medical introduces large model technology into the vertical field of healthcare, transforming existing imagingComprehensively empower AI and medical big data middle-platform products by developing general-purpose large models for medical data, creating a one-stop AI platform for multimodal data such as text and imaging, to better support the development of clinical intelligence.

DeepWisdom Medical applies generative AI to image enhancement. Its research findings indicate that certain sequences in clinical MR scans often suffer from low signal-to-noise ratios and prominent artifacts, which compromise the final image quality. AndLeveraging models such as Transformer to indirectly generate new images (e.g., higher-resolution images, other contrast types, and simulated contrast-enhanced images) from existing T1- and T2-weighted scans can yield results that even surpass those of direct magnetic resonance imaging.

Special Thanks (in alphabetical order by company name):Jianpei Technology,MANTEIA、Deepwise Medical,Shenzhi Technology,Deep Intelligence Penetrating Medicine,Shukun Technology,Infervision,Winning Health,YiZhun Intelligence,Acknowledgment of the support provided by Airdoc and Yuewei Medical for the research conducted in this report.

The above is an excerpt of the main content of the report. Scan the QR code to download the full report for free.

Table of Contents

Chapter 1: Artificial Intelligence Has Become an Indispensable Part of the Healthcare Sector

1.1 Over 100 AI Products Approved as Class III Medical Devices, AI Moves Beyond Assisted Diagnosis

1.2 Nearly 100 AI-empowered pipelines have entered clinical trials, but none have progressed to the market approval stage

1.3 Informatics Restructuring Underway: Infrastructure Development Emerges as the Biggest Barrier

Chapter 2: Capital Flow Rebounds, Medical AI Enters a Period of Steady Growth

2.1 Secondary Market Review: AI Profitability Remains Elusive, Pandemic Impact Leads to Widespread Slowdown in Growth

2.2 Primary Market Review: Macro Cooling, Imaging Sector Slows

Chapter 3: Surviving Against the Tide, Medical AI Still Requires High-Frequency Innovation

3.1 Standard Setting: A Potential Prerequisite for the Inclusion of Imaging AI in Medical Insurance

3.2 Model Innovation: Seeking New Drivers for AI Profitability

3.3 Data-Centric: New Technologies Reshape the AI Landscape

Chapter 4: Large Models Enter the Fray, Introducing New Variables to Medical AI

4.1 Nine Major Application Scenarios: Large Models Have Penetrated Healthcare

4.2 Limitations in Deployment and Application: Large Models Are Not Yet Ready for Large-Scale Implementation

4.3 Opportunities and Challenges Coexist: Large Models Are Poised to Become the Next Disruptive Technology in Healthcare

Chapter 5: Three Major Tracks Converge to Form the Core Competitiveness of Medical AI