Selling at a Premium: Key Insights from 2023’s Biotech M&A Boom

AstraZeneca

Pharmaceutical Technology Research and Development Provider

As the year draws to a close, while the biopharmaceutical industry takes stock of the top-performing companies or CEOs this year, one criterion should be given particular emphasis in the current environment: that isBiotech Companies That Sold for a Good Price, and the Decision-Makers Behind Them

Compared with financing and IPOs, mergers and acquisitions (M&A) activities were more active in the biopharmaceutical industry this year. M&A deals spanned nearly all therapeutic areas—from oncology and immunology to central nervous system (CNS) disorders and metabolic diseases, as well as ophthalmology and rare diseases. Numerous high-value transactions occurred, with 12 M&A deals exceeding $3 billion throughout the year. Furthermore, the first Chinese innovative biopharmaceutical company to be fully acquired by a multinational corporation (MNC) emerged: AstraZeneca announced at the end of the year that it would complete the acquisition of Gracell Biotechnologies for $1.2 billion.

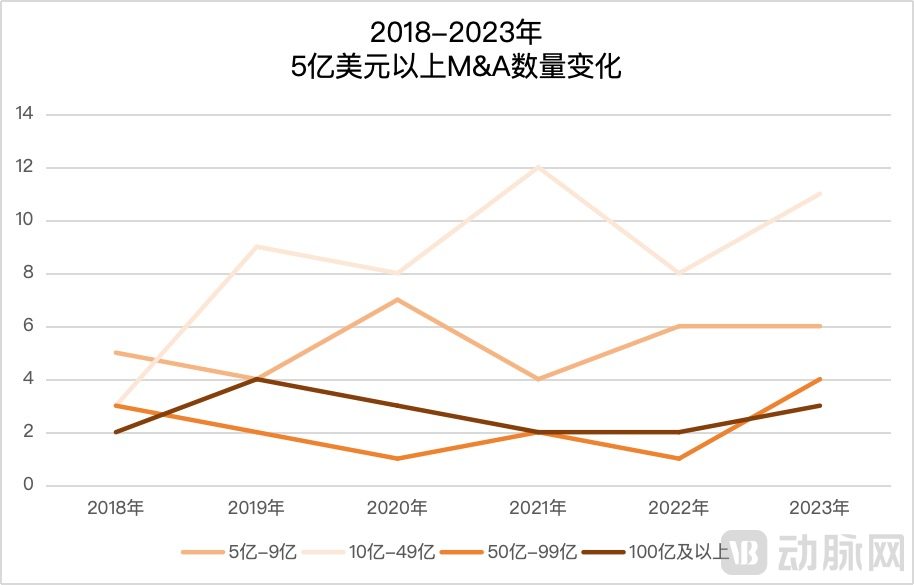

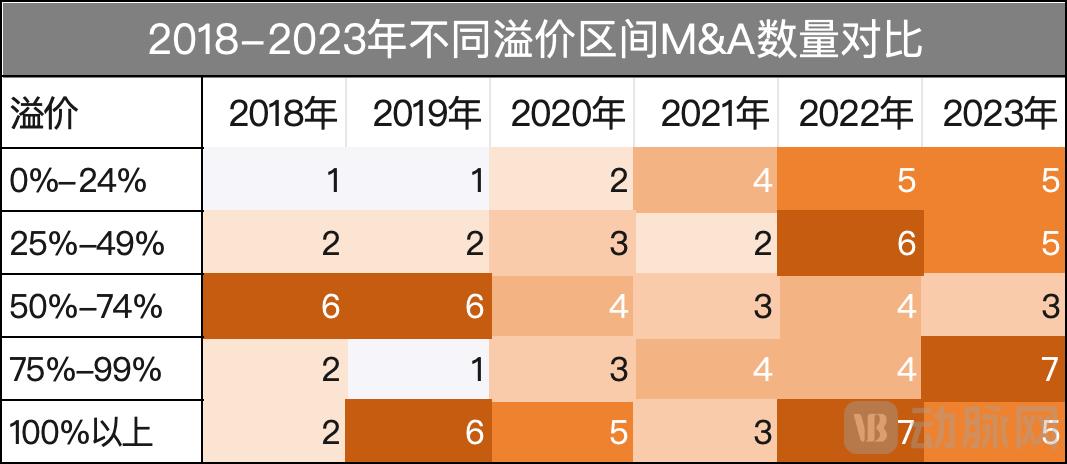

The biopharmaceutical sector saw nearly 40 M&A deals throughout the year, with a total value exceeding $140 billion. The top 10 deals amounted to $116.9 billion, compared to just $75.7 billion during the same period last year. A comparison of M&A data over the past six years reveals that large-scale transactions valued at over $5 billion have reached a new high. Amidst the underperformance of biotech companies in the secondary market, 12 M&A deals featured premiums exceeding 75%.

This has indeed been a year of mutual convergence, with MNCs believing that “if not now, when is the right time to snap up assets?” and biotech firms viewing “securing a favorable price” as a testament to their respect for both scientific research and the business world.

Source: Biopharma Dive; Chart by VCBeat

M&A Transactions and Their Motivations: A Roadmap for the Future of Biopharma and Strategic Insights for BiotechBehind large-scale transactions and favorable outcomes lie years of accumulated strength, timely course corrections, or strategic withdrawals. Successful M&A takes responsibility for Biotech employees and business operations, shareholder interests, technological advancement, and even the future of disease fields.

M&A helps facilitate more efficient allocation of scarce resources across the industry: it enables promising projects from startups to reach the broadest global patient population in the shortest possible time, unlocks substantial capital that is then recycled back into the biopharmaceutical ecosystem, and further expands the scale and overall liquidity of the talent market.

“Not every biotech company needs to be ‘the chosen one.’ Biotech founding teams can focus on what they do best, and after a successful exit, start a new game.” This is how some industry insiders commented on this year’s M&A boom.

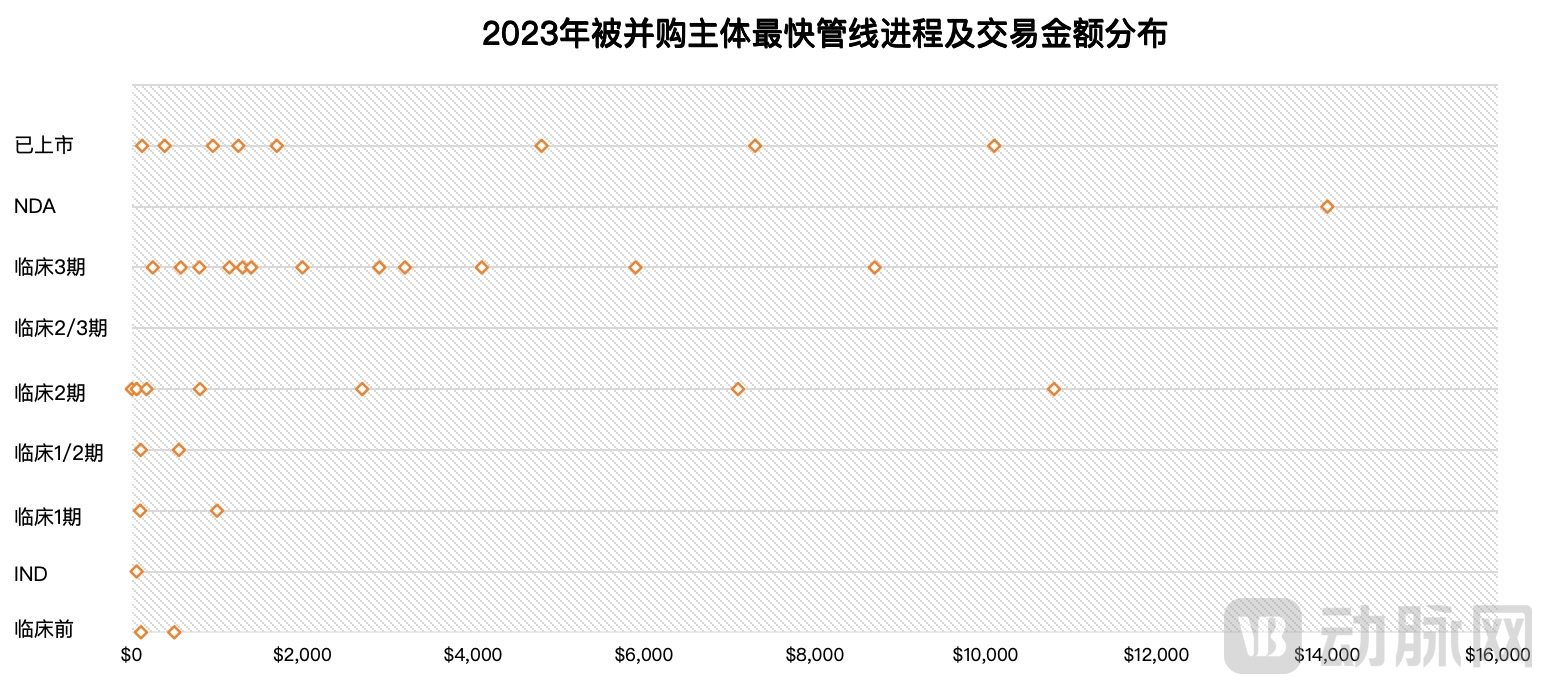

An analysis of the most advanced pipelines among acquired entities and the distribution of transaction values reveals that companies with marketed products or Phase III clinical candidates remain the most sought-after. Nevertheless, some Phase II biotech firms have commanded high valuations, while numerous Phase I and pre-clinical biotechs have also opted to cease independent operations.

Excluding Seagen and technology platform transactions; unit: million USD. Chart by VCBeat

Those who understand the times are true visionaries. Yet behind every M&A deal that satisfies multiple stakeholders lies a complex and ever-changing array of tasks: flexing muscle and showcasing strengths, engaging with sellers, navigating multifaceted negotiations, and preparing for an IPO or managing market capitalization. Only exceptional biotech executives can successfully orchestrate all of these efforts.Which companies’ boards and executives strategically crafted new business cases for biotech M&A this year? We revisit five key events from 2023 at year-end.

Cerevel, a Far Cry from Its Former Self: Bain Capital Reaps a 10-Fold Profit

Cerevel

Acquirer:AbbVie

Price:$8.7 billion

Field:CNS

CEO:Ron Renaud

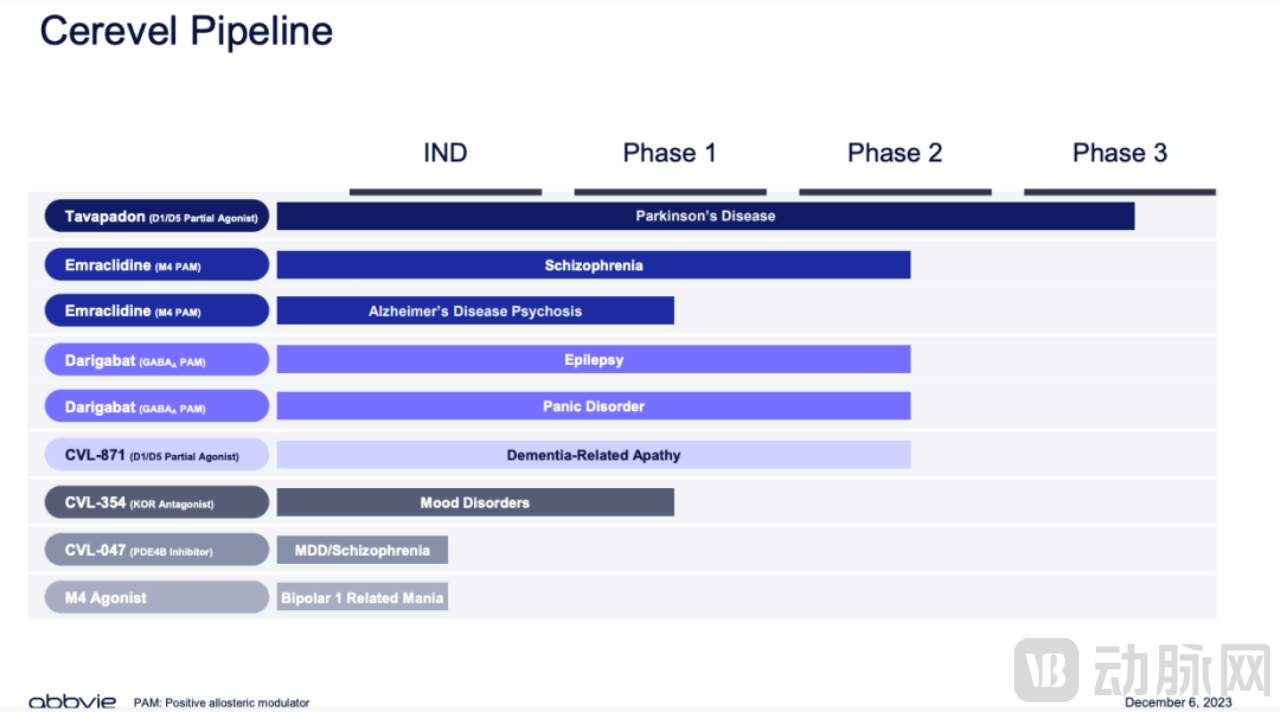

Flagship Pipeline/Products:Emraclidine

Fastest Pipeline Progress:Tavapadon is in Phase 3 clinical trials.

On December 7, AbbVie announced that it would acquire Cerevel Therapeutics for approximately $8.7 billion, thereby gaining access to its robust neuroscience pipeline. Cerevel’s most notable asset is emraclidine, a Phase II schizophrenia drug with the potential to redefine the standard of care for schizophrenia and other psychiatric disorders. Although two of Cerevel’s Phase II clinical trials were delayed, this did not affect the final acquisition price. AbbVie believes that Cerevel’s product portfolio holds billions of dollars in sales potential and serves as a strong complement to its existing neuroscience offerings.

Cerevel was once a “non-core asset” of Pfizer. In 2018, Pfizer decided to scale back its neuroscience R&D and spin off part of the related assets, partnering with Bain Capital to establish Cerevel. Recognizing the potential of Cerevel’s central nervous system (CNS) pipeline, Bain Capital injected $350 million into the company. In 2020, Cerevel went public on the Nasdaq through a special purpose acquisition company (SPAC), raising $445 million.

The public listing has provided financial security for its subsequent development. Throughout its growth trajectory, Cerevel has maintained a robust financial position, supporting mid-to-late stage clinical trials and corporate operations. With $825.1 million in cash on hand, the company has sufficient runway to fund operations through 2025, creating favorable conditions for merger and acquisition evaluations.

Starting in 2021, multiple pipeline candidates from Cerevel entered pivotal Phase II clinical trials; however, regulatory approvals proceeded slowly, and clinical trial progress lagged behind expectations. From 2022 to 2023, Cerevel repeatedly postponed the release of key trial data. These repeated delays in clinical trials and data readouts not only eroded investor confidence but also signaled a potential setback in the competitive race for central nervous system (CNS) therapeutics.

Mid-to-late-stage clinical trials require substantial funding, not to mention the arduous path to commercialization post-launch—a reality recognized by both Bain Capital and Cerevel. With multinational corporations (MNCs) well-capitalized and Emraclidine viewed favorably, the optimal window for mergers and acquisitions has arrived.

Cerevel appointed Ron Renaud as its new CEO in May this year. A partner at Bain Capital, Mr. Renaud brings extensive experience in mergers and acquisitions and operations, having previously led companies including Idenix (acquired by Merck for $3.85 billion) and Translate Bio (acquired by Sanofi for $3.2 billion). Since his appointment, Cerevel has rapidly upgraded its management team, successively announcing the appointments of a new Chief Financial Officer and a new Chief Business Development and Strategic Operations Officer.

Less than six months into Renaud’s tenure, Cerevel completed the $8.7 billion acquisition. The biggest winner, however, is not AbbVie for the time being, but Bain Capital, which has reaped substantial returns. Bain Capital held approximately 58% of Cerevel’s shares. At a price of $45 per share, Bain Capital will realize gains of roughly $5 billion, representing an approximate 10-fold return on its investment.

Bain Capital excels at identifying undervalued assets in the biotechnology sector and executing business turnarounds, with Cerevel standing as another successful example. Notably, the high-priced acquisition of Cerevel has further fueled criticism among some industry observers regarding Pfizer CEO’s underwhelming performance this year. However, such dramatic scenarios are an inevitable part of strategic decision-making at multinational corporations (MNCs).

Bold and Decisive: Carmot Acquired by Roche at a Premium Half a Month After Filing for IPO

Carmot

Acquirer:Roche

Price:$3.1 billion

Field:Metabolism

CEO:Heather Turner

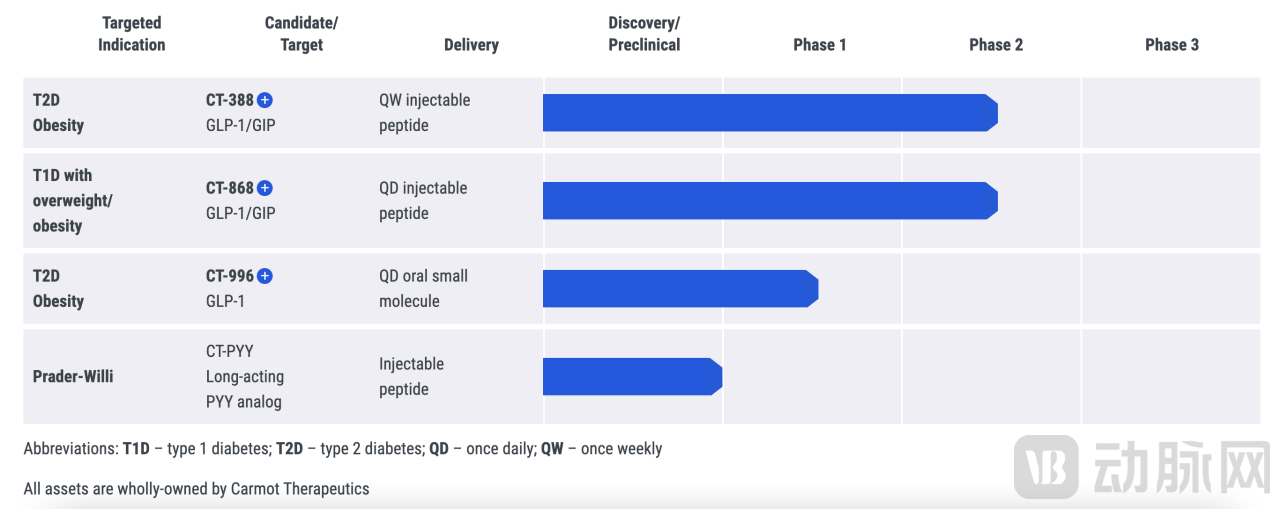

Star Pipeline/Products:CT-388

Fastest Pipeline Progress:CT-388 and CT-868 are in Phase II clinical trials

On December 4, Roche announced an agreement to acquire Carmot Therapeutics. Roche will pay Carmot a $2.7 billion upfront payment and an additional $400 million in milestone payments. Through this transaction, Roche will obtain Carmot’s entire pipeline portfolio, and a portion of Carmot’s employees will join Roche. As a prominent biotech player in the GLP-1 field, Carmot possesses its own drug discovery platform and has made smooth progress in its pipeline, which covers both oral and injectable formulations. Notably, CT-388, which has demonstrated impressive weight-loss efficacy, holds the potential to become a best-in-class (BIC) therapy.

Carmot initially operated as a company with parallel advancements in metabolism, oncology, and autoimmune diseases. Later, in 2020, it shifted its R&D focus to GLP-1 drugs for diabetes and obesity. Carmot’s successful bet, driven by its focused strategy and high-quality pipeline, made it highly favored in the capital markets. The company raised $310 million between 2022 and 2023 and filed for an IPO in November 2023. At the time, the market widely believed that Carmot would bring long-awaited momentum to biotech IPOs.

But Roche quickly turned the IPO into a premium acquisition with a total price of $3.1 billion. In fact, this was not the first time Carmot had received an offer; Bloomberg reported in the second half of this year that Carmot had rejected a $1 billion acquisition bid—a figure that held little appeal for a high-potential biotech company with total financing of $400 million.

However, Carmot CEO Heather Turner stated that the company was indeed preparing for an initial public offering (IPO) while simultaneously seeking a more suitable buyer. In July, Charles W. Newton, Carmot’s newly appointed board member, assumed his position. Previously, Newton held roles at financial institutions such as BofA Securities, Credit Suisse, and Morgan Stanley, where he provided advisory services for mergers and acquisitions (M&A) deals worth $200 billion and completed transactions totaling $60 billion. Ultimately, under the leadership of the new executive team, Carmot reached an agreement with Roche, with the total acquisition value exceeding twice the previous valuation.

Roche is a high-quality buyer: as of October 2023, Roche had over $60 billion in available cash on its balance sheet; lacking weight-loss assets, it urgently needs differentiated GLP-1 products to compete in the upcoming multinational corporation (MNC) landscape, and Carmot will likely receive significant attention post-acquisition; Roche’s investigational anti-myostatin antibody, although developed for the treatment of spinal muscular atrophy (SMA), provides a therapeutic agent that supports muscle development and could be combined with weight-loss therapies to mitigate associated muscle loss.

Carmot’s IPO plans were likely driven more by its own financing and development needs than by a mere desire to secure a high offer from Roche. When Roche presented sufficiently favorable terms, Carmot chose to accept the acquisition in its own best interest. Moreover, Roche intends to continue utilizing Carmot’s drug discovery platform and retain its team. After all, independent survival is exceedingly difficult for biotech companies in the field of chronic diseases.

ImmunoGen Cashes in at the Right Time: ADC Leader Finally Joins an MNC

ImmunoGen

Acquirer:AbbVie

Price:$10.1 billion

Field:ADC

CEO:Mark Enyedy

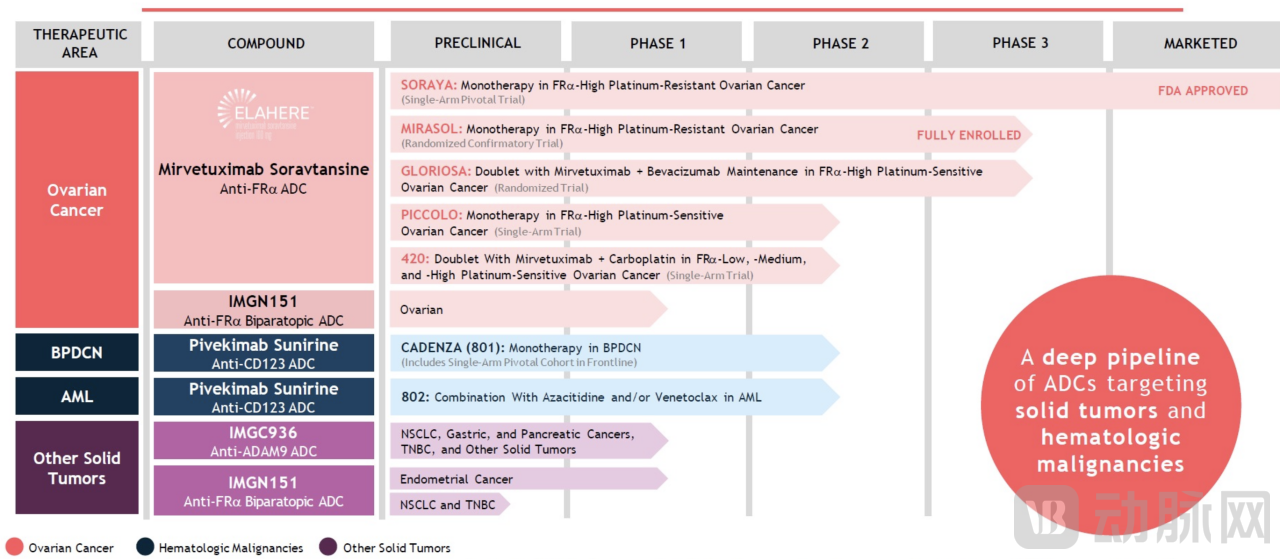

Star Pipeline/Products:Elahere

Fastest Pipeline Progress:Elahere has been launched

In terms of experience navigating the biotechnology cycle, ImmunoGen certainly has a strong voice. Yet, despite operating for 40 years, ImmunoGen can still only be classified as a biotech company, having relied primarily on technology licensing fees for its livelihood over the decades.

On November 30, AbbVie announced the acquisition of ImmunoGen and its core antibody-drug conjugate (ADC) therapy, Elahere, for $10.1 billion, further bolstering AbbVie’s oncology portfolio. The leading ADC company has finally found its place amid this year’s wave of mergers and acquisitions.

Elahere, ImmunoGen’s marketed product and the world’s first FRα-targeting antibody-drug conjugate (ADC), is a significant revenue driver for the company. With cumulative sales of $212.1 million in the first three quarters of this year, the drug enabled ImmunoGen to achieve profitability for the first time in its 40-year history, reporting a net income of $30 million in the third quarter.

Despite ImmunoGen’s clear technological advantages and first-mover experience in the antibody-drug conjugate (ADC) field, it has long failed to translate these strengths into successful commercialized products. The company’s stock performance has been weak, failing to deliver substantial returns to shareholders except during brief periods. Previously, under operational pressure, ImmunoGen was compelled to issue corporate bonds to raise capital. Furthermore, ImmunoGen has long maintained a “small but elegant” profile, with its headcount remaining relatively stable over the years and no robust commercialization team having been established.

During the second and third quarters of this year, as ImmunoGen’s stock price rose, CEO Mark Enyedy and numerous other executives chose to reduce their holdings and cash out, even as the company was simultaneously engaged in acquisition negotiations. Ultimately, AbbVie’s acquisition deal was priced at $31.26 per share, significantly higher than ImmunoGen’s recent stock price, resulting in a high-premium acquisition.

This acquisition comes at a time when AbbVie’s oncology business is facing challenges. In the first nine months of 2023, revenue from AbbVie’s flagship drug, Imbruvica, declined by more than 20% year-over-year. Upon completion of the acquisition, AbbVie will not only gain Elahere, a first-in-class therapy for platinum-resistant ovarian cancer, but also leverage ImmunoGen’s antibody-drug conjugate (ADC) platform and toolkit to develop next-generation innovative ADC therapies.

In the ensuing ADC arms race, ImmunoGen would face significant uncertainties and risks if it continued to operate independently. Capitalizing on this profitable opportunity, the completion of this acquisition represents a perfect answer sheet for shareholders from Mark Enyedy.

Reata, with Only One Rare Disease Drug, Prompts Biogen to Offer Highest Price in History

Reata

Acquirer:Biogen

Price:$7.3 billion

Domain:CNS

CEO:Warren Huff

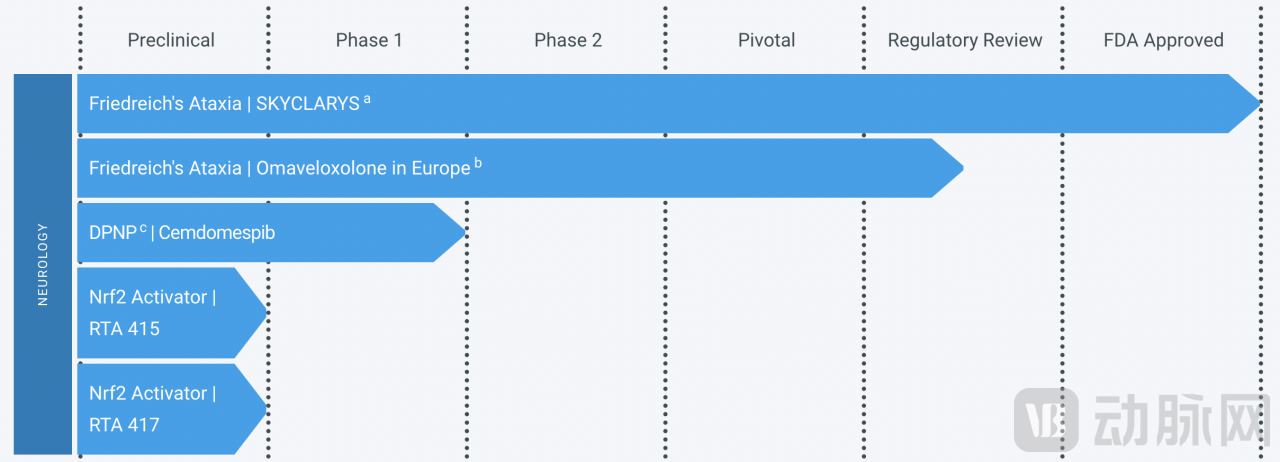

Flagship Pipeline/Products:Skyclarys

Fastest Pipeline Progress:Skyclarys Has Been Launched

On July 28, Biogen acquired rare disease company Reata for $7.3 billion. Through this acquisition, Biogen will gain access to Skyclarys, a drug approved by the U.S. FDA in February of this year. Skyclarys is the first and only FDA-approved treatment for Friedreich's ataxia. Facing no competitive market pressure, Skyclarys is projected to have a U.S. sales potential of $400 million.

This marks Biogen’s largest acquisition in its history, coming just three days after the company announced a plan to lay off 1,000 employees, aiming to save $1 billion in annual operating costs by 2025.

On one hand, the company is cutting costs through layoffs; on the other, it is gaining growth momentum by acquiring Reata. Although Reata’s Skyclarys has been controversial due to the lack of clinical significance in mFARS score improvements, it can help offset the sales decline associated with Biogen’s core products. Furthermore, Reata has numerous early-stage investigational projects. Biogen stated that these assets were priced very reasonably and noted that Reata’s Nrf2 agonists hold promise for treating conditions such as Alzheimer’s disease and amyotrophic lateral sclerosis (ALS).

Reata’s CEO, Warren Huff, has been instrumental in guiding this rare-disease biotech to where it is today. A former securities lawyer, Huff served as Reata’s CEO for over two decades, steadfastly pursuing research in innovative areas largely untouched by other companies. Reata has long focused on Nrf2 activators, ultimately developing the Nrf2 agonists bardoxolone and omaveloxolone. In 2021, the FDA rejected its first-generation Nrf2 drug, causing the company’s stock price to plummet by 40% at one point. Subsequently, the successful market launch of its second-generation Nrf2 therapy, Skyclarys, completely transformed Reata’s fate.

The acquisition of Reata marks the first major deal spearheaded by Biogen’s new CEO, who has articulated a strategy to strengthen and expand the company’s presence in the rare disease sector. Biogen’s spinal muscular atrophy (SMA) therapy, Spinraza, has generated substantial revenue for the company. Meanwhile, its newly approved amyotrophic lateral sclerosis (ALS) treatment, Qalsody, continues to demonstrate Biogen’s prowess in commercializing complex rare disease therapies.

Nrf2 Agonists Propelled Reata’s Success; MNCs Such as Bayer and AstraZeneca Are Also Investing in Nrf2—Now the Question Is Whether Biogen Can Sustain Reata’s First-Mover Advantage in This Field.

FocusIBD’s Prometheus, or the Reason Why Merck Abandoned Seagen

Prometheus

Acquirer:Merck & Co.

Price:$10.8 billion

Field:Immunity

CEO:Mark McKenna

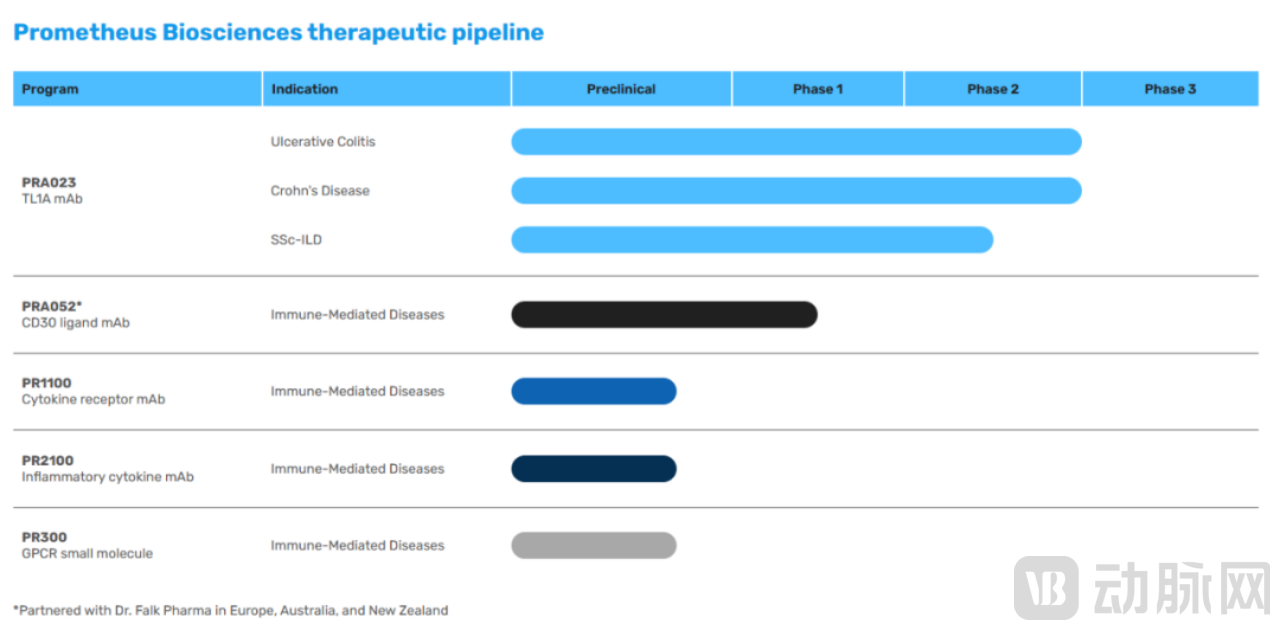

Star Pipeline/Products:PRA023

Fastest Pipeline Progress:PRA023 is in Phase 2 clinical trials.

On April 16, Merck & Co. announced plans to acquire Prometheus for $10.8 billion in cash, gaining new candidate drugs for ulcerative colitis (UC), Crohn’s disease (CD), and other autoimmune diseases to strengthen its immunology pipeline. Inflammatory bowel disease (IBD) has been a hot spot in the past two years, with complex etiologies, a large patient population, and limited efficacy of existing biologics.

Prometheus has incurred continuous operating losses since its inception. Its total operating revenue from 2018 to 2022 amounted to only $6.81 million, while net losses increased year by year, reaching $142 million in 2022. As of the end of 2022, Prometheus held approximately $292 million in cash reserves. Given its persistently high net losses, this cash runway is limited.

Wall Street feedback suggests that Merck’s offer was high, but the acquisition of Prometheus can help Merck further expand its footprint in immunology and strengthen its position in this rapidly growing therapeutic area. Phase 2 clinical trial data for PRA023 demonstrated favorable safety and efficacy; if Phase 3 trials continue to validate these results, the product could become a potential new first-line treatment option for ulcerative colitis (UC) and Crohn’s disease (CD). The IBD market is projected to grow to nearly $50 billion within five years, and the combination of a strong Phase 2 asset and broad market prospects prompted Merck to move forward with the acquisition of Prometheus.

CEO Mark McKenna has played a pivotal role in the development of Prometheus. In 2019, Mark McKenna joined Prometheus as CEO. Under his leadership, Prometheus rapidly expanded its pipeline, with multiple drug candidates advancing into clinical trials. The Phase 2 clinical trial of its lead product, PRA023, laid the foundation for subsequent development. Meanwhile, McKenna also guided Prometheus to successfully complete an initial public offering (IPO) in the capital markets, securing funding to support the company’s strategic objectives. Leveraging his extensive management experience in the pharmaceutical industry and strong engagement with the capital markets, McKenna ultimately finalized the merger and acquisition transaction with Merck & Co.

For Merck & Co., although the impact is not as direct and rapid as the acquisition of Seagen, a ticket into the autoimmune field is extremely valuable. From Prometheus’s perspective, the outcome thus far is quite satisfactory for an autoimmune biotech company that has posted annual losses, after all, Phase 3 trials are not every pharmaceutical company’s strong suit.

Appendix: Full-Year 2023 Pharmaceutical M&A Transactions