State Capital's Surge in 2023: 388 Direct Investments and Nearly Trillion-Yuan Commitment in China's Healthcare Sector

ADDOR

Venture Capital Institution

Chengdu Biological City Equity Investment Fund

Biomedical Investment Institutions

SHC

Innovative Investment Institutions in the Biomedical Field

CICC Capital

Private Equity Investment Management Firm

SCGC

Investment Institutions in Innovative Fields

Fortune Capital

Venture Capital Institution

HTI

Financial Services Institution

Looking back on the past year, those working in the healthcare industry have rarely felt a sense of satisfaction or accomplishment; instead, confusion and helplessness have been more prevalent. Amidst this interplay of emotions, one keyword remains unavoidable:“State-owned Capital”. In response, some investors joked, ““If you haven’t dealt with state-owned capital in 2023, you’ve basically lived in vain.””

While this may seem somewhat exaggerated, it is not without merit upon careful consideration. Let the facts speak: since the beginning of 2023, mother funds with scales of tens of billions and even hundreds of billions have emerged in various regions across China; according to incomplete statistics,As early as last August, the total scale of government guidance funds established in multiple regions had already exceeded RMB 1 trillion.. In the following months, local governments across various regions remained active, with major local government guidance funds being announced from time to time; on the last day of 2023, Suzhou even registered and establishedRMB 50 billion in Suzhou state-owned capital, which can be described as a year-long "rat race" from the beginning to the end of the year.

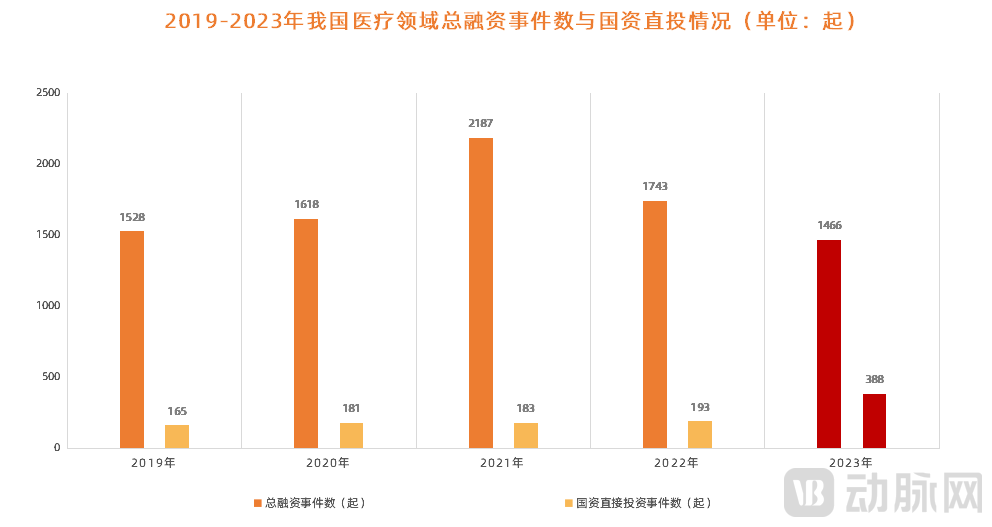

Focusing further on the healthcare sector, a key area of emphasis for state-owned capital, the scale of investment has been unprecedented. According to incomplete statistics from the VCBeat Orange Database,In 2023, there were 388 investment events in China's healthcare sector with direct participation from state-owned capital, exactly double the number in 2022.. In response to this, an investor lamented, “State-owned institutions are almost always present at the fundraising events of every hot project.。”

Figure 1. Total Number of Financing Events and Direct State-Owned Capital Investments in China’s Healthcare Sector, 2019–2023 (Source: VCBeat)

Figure 1. Total Number of Financing Events and Direct State-Owned Capital Investments in China’s Healthcare Sector, 2019–2023 (Source: VCBeat)

Yet beyond the hype, an objective fact cannot be overlooked: the entire healthcare industry was actually in a downturn in 2023. Taking the primary market, the most intuitive indicator, as an example, although state-owned capital participation was high, the overall number of financing deals declined significantly. According to incomplete statistics from the VCBeat Orange Database,In 2023, there were a total of 1,466 financing deals in China's healthcare sector, representing a 19% year-on-year decrease.. Turning to the secondary market, constrained by factors such as the tightening of IPOs,The Number of Healthcare IPOs in 2023 Shrunk by Nearly 60%, taking the last month of 2023 as an example, nearly 10 medical companies announced the termination of their IPOs.

Thus, as we look back on 2023, a question has grown increasingly prominent in “year-end reviews,” namelyAmid the Market Winter, What Exactly Is State-Owned Capital “Hot” About?

From Behind the Scenes to Center Stage: Is State-Owned Capital Also Eager to "Steal the Spotlight"?

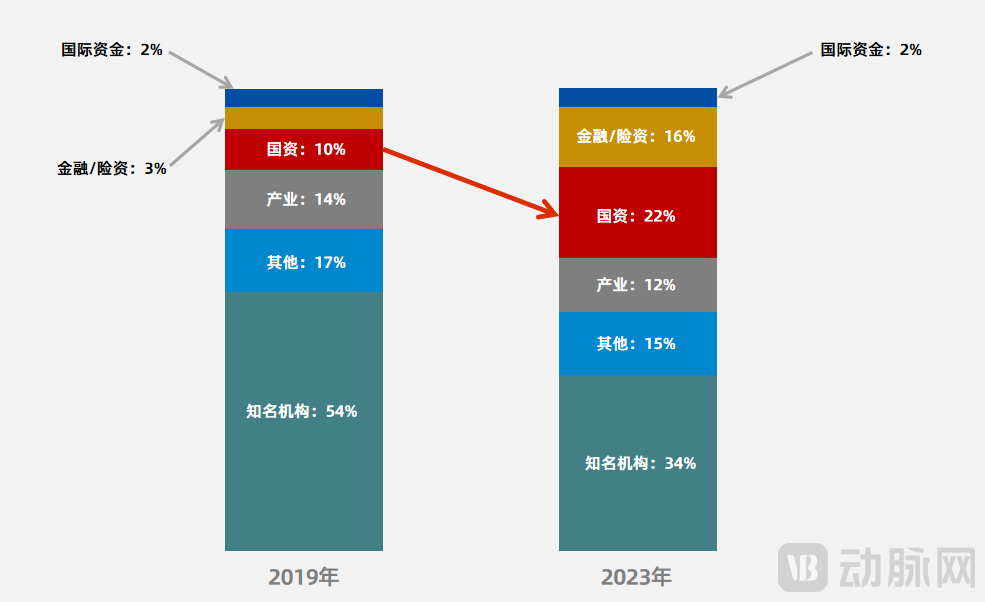

In fact, state-owned capital began to exert its influence early on. According to the “2022 Interpretation Report on Limited Partners of Chinese Private Equity Funds,”Since 2018, policy-driven capital (including government-funded platforms and government guidance funds) has become the largest source of investment in China, a position it has maintained to this day.。

Figure 2. Comparison of Backgrounds of Actively Investing Institutions in 2019 and 2023 (Data Source: Zero2IPO Research Center)

Figure 2. Comparison of Backgrounds of Actively Investing Institutions in 2019 and 2023 (Data Source: Zero2IPO Research Center)

The primary reasons it only began to “emerge” in 2023 are threefold: first, substantial capital investment; according to data from Zero2IPO Research Center, in the first half of 2023,The combined disclosed capital contributions from state-controlled and state-participating LPs accounted for 71.2%.; second, there has been a significant increase in participants. In addition to Beijing, Shanghai, Guangzhou, and Shenzhen, numerous new first-tier cities as well as districts and counties successively established government guidance funds in 2023, with a particular focus on increasing investments in the healthcare sector, giving rise to the industry narrative of “investors going to the countryside”; third, state-owned capital has increasingly engaged in direct investments, leading to more frequent direct interactions with the primary market.

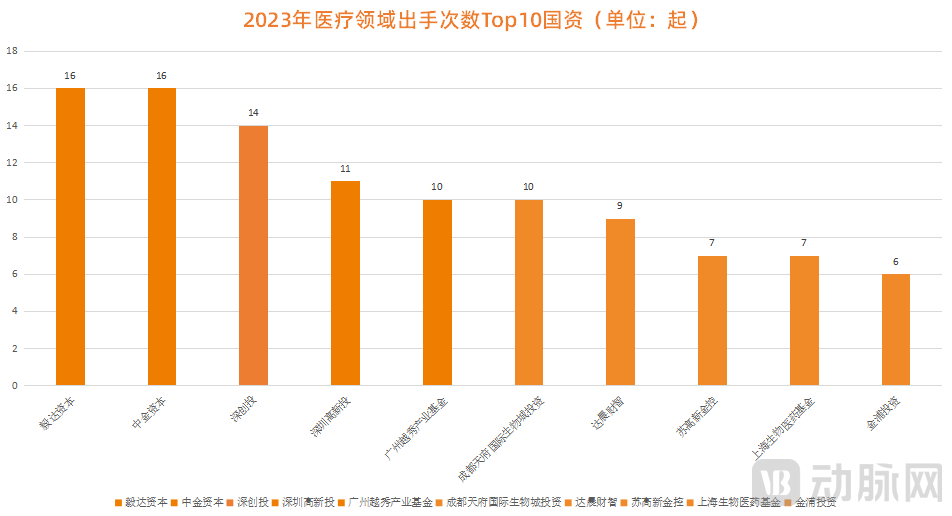

Figure 3. Top 10 State-Owned Investors by Number of Deals in the Healthcare Sector in 2023 (Source: VCBeat)

Figure 3. Top 10 State-Owned Investors by Number of Deals in the Healthcare Sector in 2023 (Source: VCBeat)

So, what is the underlying logic behind the aggressive “emergence” of state-owned capital?

Let’s begin with an external perspective, namely the market level. As mentioned earlier, the entire capital market was relatively cool in 2023; against this backdrop,State-owned capital actually plays a key role in boosting confidence in the industry.. On this basis, looking deeper into the healthcare industry, it was inevitable for state-owned capital to step forward in 2023.

On one hand, the healthcare industry is undergoing cyclical changes, with innovation emerging as a key investment theme. State-owned capital, characterized by greater strategic patience, will naturally take the forefront in this sector. Commenting on this trend, a seasoned investor stated, “The fundamental nature of innovation requires substantial and long-term capital investment, along with the assumption of certain risks. This inevitably means that it will be driven by ‘national teams’ or through the spillover of state resources into the market. This is because, compared to market-oriented institutions pursuing rapid profitability,”State-owned capital with more diversified evaluation dimensions will have greater patience, which is necessary for innovation.。”

On the other hand, the focus is on empowerment by state-owned capital. In this regard, a leading venture capital firm in Beijing stated, “Beyond providing endorsements and public support, hard-tech companies, upon reaching a certain stage of development, will inevitably need to expand production capacity, andState-owned assets can precisely provide services such as land and tax incentives.”. In fact, after two years of industry boom, a large number of companies in the healthcare sector are now poised to “ramp up production”.

Of course, these are merely “external factors.” Looking inward, the decision by state-owned capital to concentrate its efforts at this juncture also reflects its own “strategic considerations.”

The primary focus is on investment promotion, in the post-pandemic era,The demand for economic and social development, as well as the introduction and cultivation of emerging industries, is significantly increasing across various regions.. In this process, the healthcare sector has become a common choice for local governments across various regions. This is partly because it is a livelihood industry that also possesses hard-tech attributes, and partly because its substantial market size is fully capable of supporting further advancement of the local economy.

However, as the industry cools down, investment promotion has become increasingly challenging. The traditional, straightforward approach to attracting businesses is no longer effective in bringing in high-quality medical enterprises at this stage, soMany state-owned capital entities have begun to experiment with the new model of “replacing investment promotion with direct investment,” transitioning from being limited partners behind funds to making direct investments themselves.。

Regarding the shift in their roles, a representative from a state-owned enterprise (SOE) in Hefei shared profound insights. He remarked, “In the past, government guidance funds operated as funds of funds (FOFs), selecting general partners (GPs) for investment based on their professional expertise and information asymmetry. However, after many years, the government’s cognitive understanding, investment capabilities, and risk control mechanisms have all evolved. For them, establishing an in-house investment department is no longer a particularly challenging task. Furthermore, with GPs’ performance generally underwhelming—issues such as failure to meet local reinvestment requirements and insufficient distributed paid-in capital (DPI) have become increasingly apparent—this has created favorable conditions for state-owned capital to take a more hands-on approach.”

Therefore, in retrospect, it is hardly surprising that state-owned capital became the industry’s buzzword and stole the spotlight in 2023. This is because when entrepreneurial opportunities in the healthcare sector are no longer confined to major cities,The vast majority of once-obscure cities hope to seize the opportunity presented by emerging industries to “defy fate and transform their destiny.”, and in this process, state-owned capital serves as both an important instrument and a significant bargaining chip.

State-owned capital: It’s not just about the money

When state-owned capital is mentioned, many people’s first association is with deep pockets—a trait that becomes even more pronounced amid the current investment winter.

However, capital is not the sole prerequisite for industrial development, particularly in the healthcare sector. In other words, state-owned assets must undergo certain transformations to genuinely transition into healthcare investors. According to observations by VCBeat, this shift has already been quietly underway since 2023.

First, state-owned capital is moving toward greater professionalism and market orientation, with the solution being to recruit a large number of investment professionals from top-tier funds.Generally speaking, teams at state-owned direct investment platforms tend to be small, with personnel exhibiting strong governmental characteristics but weaker capital-market orientation. However, the innovation demands of the healthcare industry are compelling investment institutions to become more professional. The quickest way to bridge this gap is to recruit top talent from leading venture capital funds, which has led to a widespread phenomenon of investors transitioning into state-owned enterprises.

In response, a professional who joined a Chengdu state-owned enterprise in early 2023 shared his personal experience, “Nearly half of our group ultimately joined state-owned enterprises., there are many reasons for this at various levels, but in my personal view, the most critical factor is that state-owned capital has become a vital component of the industry. At the same time, it is shedding its past stereotypes and rapidly aligning itself with market-oriented funds.”

Following this logic, it is necessary to mention the second significant change in state-owned capital,Specifically, at the investment strategy level, the focus is on investing in early-stage, small-scale, and innovative ventures, while also giving consideration to mid- to late-stage healthcare projects.. In fact, there is an intriguing phenomenon in the capital market: social capital often proceeds by “crossing the river by feeling the stones,” whereas state-owned capital frequently crosses by “feeling” social capital. Consequently, state-owned capital has primarily adopted a follow-on strategy in the past, co-investing in healthcare enterprises at mid-to-late stages. At this stage, companies typically boast relatively larger revenue scales and operational volumes, have largely established mature commercialization pathways, and offer greater industrial certainty.

However, as the industry continues to evolve, such medical enterprises are becoming increasingly scarce, and their overall profitability is declining. Moreover, in certain regions, investing in late-stage projects offers limited advantages due to the lack of available facilities and high labor costs, which hinder companies’ ability to expand production capacity.

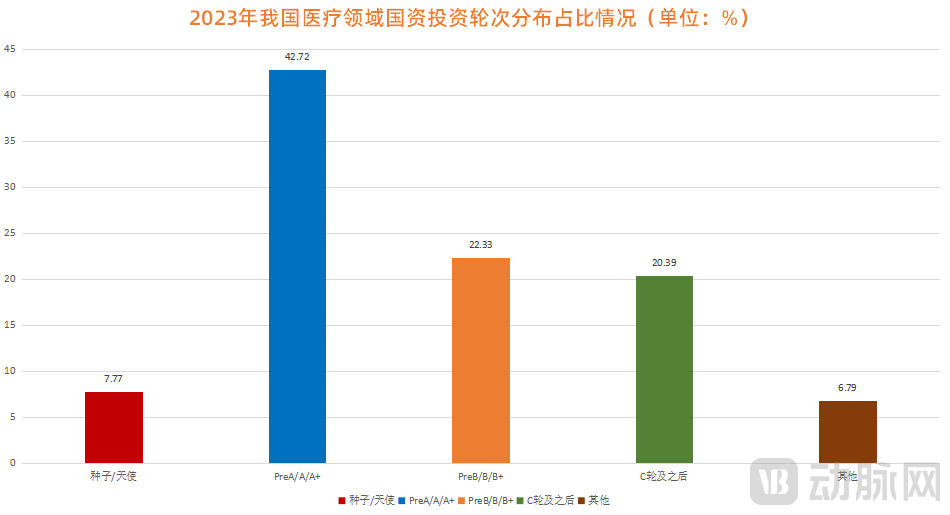

Figure 4. Distribution of State-Owned Capital Investment Rounds in China’s Healthcare Sector in 2023 (Source: VCBeat)

Figure 4. Distribution of State-Owned Capital Investment Rounds in China’s Healthcare Sector in 2023 (Source: VCBeat)

Investing in early-stage, small-scale, and innovative ventures not only aligns with the current fundamental market investment logic but also yields relatively substantial returns.After all, if just one or two early-stage healthcare projects succeed, the overall return of the fund will be secured.. Thus, among the 388 financing deals completed by state-owned capital in the healthcare sector in 2023,The financing ratio prior to Series A was 50.49%, accounting for more than half.. Focusing further on specific niche sectors,CGT, Medical Robots, AI Healthcare, Innovative Drugs, Imaging EquipmentFrontier fields have become popular areas for increased investment by state-owned capital.

Of course, on the basis of investing early, investing in small businesses, and investing in innovation,State-owned capital is also more inclined to invest in the upstream and downstream sectors, building a complete industrial chain.In this regard, a representative from Hefei’s state-owned assets sector commented, “Currently, in the pharmaceutical sector, Hefei has not devoted significant efforts to relocating the headquarters of any major enterprise to the city. This is due to both the operational complexities and the high risks involved. Over the past one to two years, Hefei has focused more on its own development, prioritizing the incubation of its own pharmaceutical industry ecosystem. Within this ecosystem, it aims to nurture promising startups and propel them to become chain leaders, thereby integrating the upstream and downstream segments of the industrial chain.”

Nevertheless, some state-owned capital firms continue to prioritize investments in mid-to-late-stage healthcare projects. This is because, despite the inherent challenges, such investments offer significant scalability, enabling rapid deployment at a lower cost. Furthermore, these projects benefit from an established market foundation, eliminating the need to build entirely from scratch. Commenting on this trend, Wang Xiaoyan, Partner at GSR Ventures, stated: “Under the current market environment, a new exit channel has effectively emerged: selling to state-owned assets.”。

Lastly, it should be mentionedState-owned capital’s drive for change and innovation is focused on empowerment, becoming both more diversified and more systematic.. Based on this, a partner at a top-tier venture capital firm stated bluntly that local governments are now offering funding, land, and policy support to any enterprise that approaches them, which is indeed highly attractive.

A founder focused on the field of innovative drugs also strongly agreed, stating, “Starting a business nowadays inevitably involves dealing with the government,”Which founder doesn’t know a few high-ranking government officials?. Furthermore, compared with market-oriented GPs, government guidance funds possess inherent advantages in post-investment value creation, such as acting as intermediaries to help companies secure upstream industrial materials and obtain downstream orders; more directly, tax authorities can also provide certain supportive policies.”

This kind of “explicit empowerment” is highly valuable for healthcare companies currently navigating a market winter. In the short term, it addresses urgent needs; in the long run, as startups grow—from incubators to industrial parks—they typically maintain certain ties with state-owned capital. Early introduction of such capital therefore facilitates future cooperation negotiations. Consequently, some investors have summarized the current latest financing sequence in the venture capital community:Priority is given to securing capital from industrial investors and local governments, followed by state-backed funds, with purely financial capital being the last resort.。

Thus, in 2023, many state-owned capital entities emphasized “empowerment,” as they gradually realized that state-owned capital cannot rely solely on financial resources. In the current market environment, the core competitiveness of state-owned capital is no longer limited to investment capabilities; rather, it increasingly hinges on resource integration capabilities.

Homogeneous Competition Among State-Owned Assets Has Just Begun: How to Break Through?

When evaluating developments, one must not look at only one side; behind the state-owned capital’s aggressive expansion into the healthcare sector, turbulent undercurrents are also at play.

First, state-owned capital is currently oversaturated, which will, to some extent, hinder the marketization process of the healthcare industry. In this regard, a top-tier investor remarked, “In the current market environment, it is understandable for state-owned capital, as a participant, to support local enterprises. However, in many cases, the financiers of some companies,”Eight out of nine have state-owned capital backing.“, this results in many projects not undergoing proper market assessment and screening, and as these projects progress, their issues tend to become more pronounced.” This underscores the investment logic repeatedly emphasized within the industry: letting the market function as the market.

And extending further downward,A major contradiction facing state-owned assets themselves is balancing their strategic objectives as government entities with the profit-driven goals of capital investors.。

Figure 5. Trend Chart of Land Finance Revenue from January to October, 2016–2023 (Data Source: Changlei Capital)

In fact, although state-owned assets are well-funded, they are not actually flush with cash. Taking land transfer fees, the most significant source of revenue for local governments, as an example, statistical data show that local government land transfer revenue in 2023 was less than half of that in 2021. This implies that by utilizing local fiscal funds, state-owned enterprises naturally assume the mission of contributing to local infrastructure and development.On the one hand, projects must meet the requirements for industrial implementation and headquarters relocation; on the other hand, project proponents are required to calculate their tax contributions. Additionally, it is necessary to cooperate with local governments to complete the supporting infrastructure for major projects, while also coping with annual audits and performance evaluations from higher authorities.。

In this regard, an investor remarked, “Although the overarching goal of supporting innovation and entrepreneurship is aligned, the strategic and profitability interests are not fully congruent. Certain bottlenecks and pain points—such as assessment requirements concerning local reinvestment ratios, investment directions, and performance returns—have placed considerable additional pressure on investors. This has significantly compressed the time and energy available for thorough project evaluation, thereby undermining the ability to practice disciplined investing.”

The final concern, of course, is the inevitable homogenized competition among state-owned assets in the future.. In 2023, state-owned capital emerged in large numbers like bamboo shoots after a spring rain, and this trend is set to continue into 2024, signaling even fiercer competition. Thus, a question has become evident: how can state-owned capital stand out in the face of such competition in the future?

However, many investors see little cause for concern, as the capital market has always been a realm where only the fittest survive. In this regard, a seasoned investor remarked, “In the wake of market exuberance, clearing out state-owned assets that lack core competitiveness may not necessarily be a bad thing, given that the industry is perpetually oversupplied with practitioners,”Rather than engaging in cutthroat competition within a limited space, it is better to allocate investments to the most suitable candidates.。”

As for how to define the “most suitable person” within state-owned assets, it boils down to one point: avoiding homogenization caused by simple “copy-and-paste” approaches or blind imitation. It is essential to fully understand the distinct characteristics and underlying logic of the healthcare industry and capital markets, and to combine this understanding with one’s own strengths and weaknesses to ultimately build differentiated core competitiveness. In short, it isAdept at leveraging market logic for strategic planning and harnessing the power of capital for execution.。

Therefore, for the many state-owned entities currently standing in the healthcare sector, a classic quote is particularly apt:The future is undoubtedly bright, yet the path remains winding. But as long as you survive, there will be opportunities.

1. “The VC/PE Year in Review: A Kaleidoscope of Industry Players” — Changlei Capital;

2. “Recently, FAs Have Been Pitching Projects to State-Owned Investment Institutions” – PE Daily;

3. “Government Guidance Funds Are Now Making Direct Investments—What’s Left for Financial GPs?” — Xiaofanzhuo.