$12 Billion Raised: The Evolution of Biotech Investment Strategies

TORL BioTherapeutics

Antibody Drug Developer

Nested Therapeutics

Oncology Drug Developer

Septerna

Targeted Small Molecule Drug Developer

At the start of the new year, Goldman Sachs made a high-profile announcement of the launch of its first life sciences fund. West Street Life Sciences Fund I, managed by Goldman Sachs Asset Management, completed its first close at $650 million and has committed approximately $90 million in investments to five startup biotech companies, including ADC drug developer TORL BioTherapeutics, molecular glue developer Nested Therapeutics, ATPase-targeted therapy developer MOMA, CNS drug developer Rapport, and GPCR metabolic disease drug developer Septerna.

Goldman Sachs has described it as one of the largest inaugural life sciences growth-stage private equity funds in history, and it has moved swiftly to invest in biotech companies across several of today’s hottest sectors, a strategy viewed as scooping up assets at the bottom of the biotech market cycle.

Over the past year, financing channels for biotech companies have narrowed. A white paper recently released by Novotech shows that global investment in early-stage biotechnology companies in 2023 decreased by 40% compared to 2022, and by 55% compared to two years ago.

In contrast, the fundraising market in the life sciences sector has also cooled over the past year. According to PitchBook data, venture capital funds dedicated to life sciences in Europe and North America raised $9.1 billion in the first three quarters of 2023.Total fundraising for the year amounted to approximately $12 billion, representing a decline of about 59% from the 2021 peak and marking the lowest level since 2020.

Changes in Life Sciences VC Fundraising Amount and Deal Count, 2013–Q3 2023, Region: Europe and North America, Source: PitchBook

However, over the past year, several notable fundraising events have occurred. For instance, OrbiMed completed fundraising for three new funds, raising over $4.3 billion, while Forbion raised approximately $1.5 billion across two funds. Additionally, Flagship Pioneering is seeking to raise $3 billion for its eighth fund.

In China, the first China Life Sciences Infrastructure Fund under Kangqiao Medical Health Industry Facilities Platform successfully completed its second final close, raising a cumulative total of $875 million; Legend Capital’s fourth RMB healthcare fund completed its first close, with an expected total size of RMB 3 billion; Warburg Pincus raised its first RMB-denominated fund, focusing on investments in the broader healthcare sector, with an expected total size of RMB 3 billion.

The fundraising fervor for life sciences special funds has cooled significantly, yet activity levels remain robust.In particular, by examining the sector allocations and innovative investment strategies of several venture capital firms in Europe and North America that have achieved successful fundraising this year, we can discern the future direction of biotech development.

Where Does the Money Come From, and Where Does It Go?

VCBeat compiled statistics on 23 investment firms in Europe and North America that completed fundraising for life sciences-focused funds in 2023, with total capital raised exceeding $12 billion. Major investor types included pharmaceutical companies, healthcare institutions, foundations, pension funds, sovereign wealth funds, and family offices, while financial institutions such as banks, insurance companies, and asset management firms also participated.

Life sciences require patient capital. Limited partners (LPs) such as pension funds and sovereign wealth funds, which prioritize long-term returns over short-term volatility and possess substantial scale and ample capital, are the ideal investors in this sector. Pharmaceutical companies, meanwhile, seek to strengthen their product portfolios through venture capital investments. For instance, the latest fund of BioGeneration Ventures secured commitments from major pharmaceutical firms like Eli Lilly and Bristol Myers Squibb (BMS), a testament to its strong track record in areas such as antibody-drug conjugates (ADCs), immunotherapy, and gene therapy. Regardless of the investor type, a common characteristic is their understanding and tolerance of the high risks and potential failures inherent in biotech companies.

2023 Life Sciences Fundraising Events in North America and Europe, Compiled from Public Sources

Despite the setbacks faced by life sciences innovation in the capital markets last year—marked by the shock of Silicon Valley Bank’s collapse at the beginning of the year, the poor annual performance of the XBI Index representing small and mid-cap biotech companies, and the bankruptcy and liquidation of several companies incubated under the Flagship Pioneering model—transformative technologies and therapeutics remain the central focus from the perspective of fund investment directions. This spans from drug development platforms and the application of computational methods, to cross-disciplinary innovations integrating physical and computational sciences with life sciences, as well as advanced personalized treatment models, all addressing therapeutic areas that still present significant unmet needs.

A key investment direction to watch is “Tech Bio,” a sector that has seen sustained rising popularity in North America over the past two years. In 2023, two funds specifically highlighted in their fundraising efforts that they would invest in biotechnology companies based on the Tech Bio model. Tech Bio emphasizes that the technological revolution has finally reached the biological domain, focusing more on leveraging an understanding of biology to program and design biological systems, rather than merely seeking individual drug assets. By integrating technologies such as AI, quantum computing, and engineering with diagnostics, innovative therapies, and prognostics, this approach aims to transform healthcare. Companies like Moderna and Ginkgo Bioworks can be regarded as representatives of Tech Bio.

Source: Artis Venture

Statistics show that more than 60 venture capital (VC) firms have invested in the Tech Bio sector. Compared to traditional drug development, Tech Bio aligns more closely with the investment logic of software, featuring return models and speeds that are more familiar and appealing to tech-focused VCs. McKinsey estimates that Tech Bio has the potential to reshape the global economy, generating an annual direct impact of $2 trillion to $4 trillion. Innovations in Tech Bio could account for 60% of the world’s physical inputs and alleviate 45% of the global disease burden.

Equity Investment Is Not the Only Solution

Compared with other industries, the life sciences industry has its own unique characteristics. For example, many biotech companies start with a pipeline of 5–8 molecules, but these molecules may not be closely related; rather, they are included primarily to diversify risk.

Furthermore, once an innovative drug enters the clinical stage, its risk and cost of capital curves become very steep. From a funding perspective, the capital consumed by clinical trials for a single drug is at least 3–5 times the total cost of all preclinical projects.

Therefore, not all innovative pharmaceutical companies are suitable for the “standardized” equity investment model. Among the life science funds established in 2023, there are many innovative investment strategies worth learning from.

Licensing Investment, Pipeline Monetization

OrbiMed’s Royalty & Credit Opportunities IV is a royalty and credit fund that offers greater flexibility in deal structuring.

Compared with traditional equity investment, pharmaceutical royalty financing exhibits characteristics reminiscent of business development (BD) transactions.Its key features include: identifying assets with commercially viable pipelines and sharing a portion of the company’s operating revenue as investment returns; transactions are directly tied to specific molecules, enabling companies in need of financing to secure capital without equity dilution or valuation challenges, while also allowing for staged monetization of pipeline assets with high flexibility.

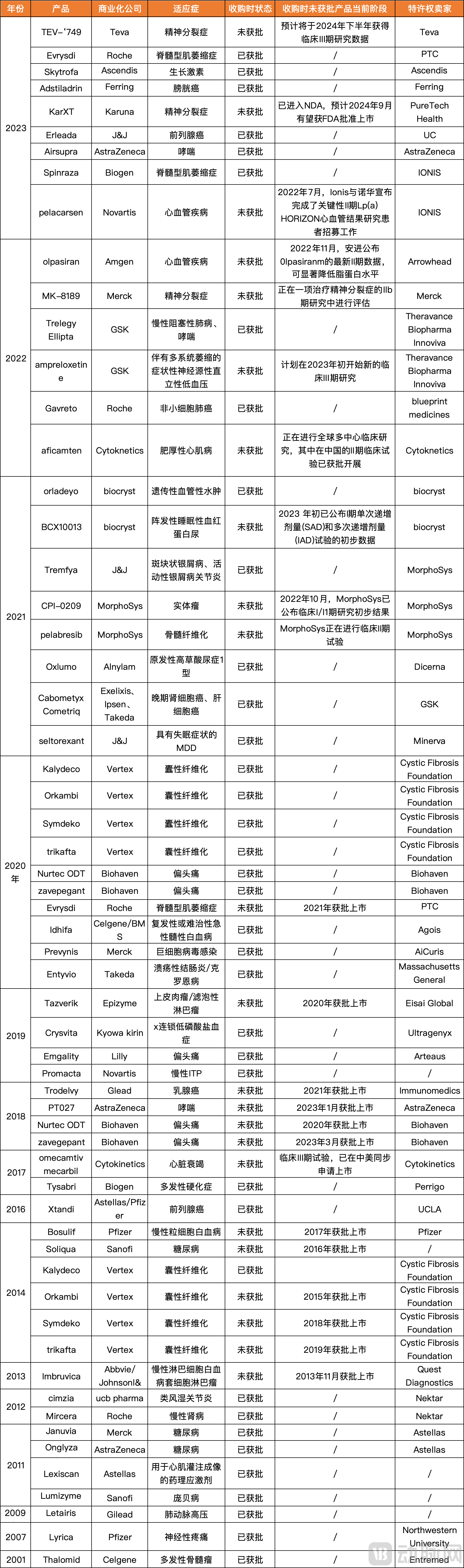

Royalty Pharma is the pioneer of this investment model. Over more than two decades of investing in pharmaceutical royalties, Royalty Pharma has initiated over 50 royalty acquisitions and invested in a portfolio of more than 35 commercialized products. This portfolio includes blockbuster drugs with revenues exceeding $5 billion, such as the Symdeko and Trikafta combination, Entyvio, Januvia/Janumet XR, and Imbruvica.

Royalty Pharma’s Investment Pipeline, Source: Royalty Pharma Official Website

In 2023, Royalty Pharma conducted a statistical analysis of its historical transactions. The results indicated that if an initial investment of $1 billion were made to acquire a royalty stream, cash flows would peak at approximately $160–200 million annually within 5 to 10 years post-acquisition, before declining year by year. Nevertheless, the asset would typically continue to generate substantial revenue for another decade after reaching its peak.

Domestic players have also begun to explore this approach. Last year, Ruiqiao Credit Fund, under CB Capital, achieved a successful exit from the biopharmaceutical company Paratek through this method.

In December 2020, Ruiqiao Credit Fund provided a total investment of $60 million to Paratek, whose pharmaceutical products had not yet been launched or sold in China at that time. The two parties agreed that the repayment sources for this investment would include a share of the net sales revenue of Paratek’s core product, Nuzyra®, in the United States, as well as all royalties from the Greater China region under the licensing agreement signed with its Greater China partner, Zai Lab.

This exit stemmed from Paratek’s early repayment within the agreed timeframe, enabling Qiaokang to receive a total of $85 million in principal repayments and profit sharing from this investment. This means that Qiaokang recouped its principal in less than three years without diluting its equity stake, while also securing a $25 million return.

Joint Development, Risk Sharing

Abingworth, the life sciences investment group under Carlyle, has consistently employed a Clinical Co-Development (CCD) investment strategy, which was pioneered in 2009.Abingworth seeks out late-stage clinical products, providing biotech companies with funding for clinical R&D and offering resources beyond capital—such as clinical and regulatory teams—while minimizing equity dilution.

CCD investments typically exceed $30 million, offering flexible financing solutions within the overall capital structure and, where appropriate, collaborating with companies to evaluate combinations of equity and CCD financing. CCD due diligence is conducted rapidly, with initial investment decisions made within a few weeks.

Representative CCD cases include Apellis, for which Abingworth provided $28 million, contributing to a total financing of $128 million. The CCD investment supported Apellis’s Phase 3 clinical trial of its C3 complement inhibitor for paroxysmal nocturnal hemoglobinuria (PNH). This bicyclic peptide, one of the most renowned products in its class, received accelerated approval from the FDA in May 2021.

Early-stage investment can also facilitate collaborative scientific translation.For example, Cure Ventures’ investment strategy is based on three principles: a seed-funding model in which Cure collaborates with biotech founders during the initial stage to conduct key experiments that validate, explore, and de-risk foundational science, thereby determining whether breakthrough ideas have commercialization potential; genetic validation to increase the probability of success by elucidating a drug’s mechanism of action, as well as its efficacy, toxicity, and target patient population; and close collaboration with founders to stay abreast of company needs and progress, enabling optimal day-to-day decision-making.

In contrast, life sciences venture capital has been present in China for some time, yet its models have become entrenched. As an industry that aspires to “invest in innovation,” it must inevitably continue to evolve and develop investment approaches better aligned with contemporary trends. With life sciences technologies advancing at a rapid pace, the time has come for innovative investment practices to undergo meaningful change.

References:

Biotech Investment Insights, https://mp.weixin.qq.com/s/tUOTLFfXanfkmfJUqZNjgg

Waves, https://mp.weixin.qq.com/s/Pf-J73oKYrskAl9oswNqxQ