Meizhong Jihe Becomes the First Private Hospital IPO of 2024 with a Market Cap Exceeding HK$8 Billion

The First Private Hospital IPO of 2024 Has Officially Arrived.

On January 9, Meizhong Jiahe Hospital Management Group Co., Ltd. (hereinafter referred to as “Meizhong Jiahe”), a leading private oncology healthcare provider, listed on the Hong Kong Stock Exchange, with a total market capitalization exceeding HK$8 billion.

As a star enterprise focused on oncology healthcare services,Meizhong Jiahe has consistently attracted capital investment throughout its development.Prior to its listing, Meizhong Jiahe Hospital Management Group Co., Ltd. received investment from CICC Capital in 2018, introduced investments from the CITIC group in 2020, and secured strategic investment from CSPC Pharmaceutical Group in 2023. Its investor base encompasses securities firm capital, financial institution capital, industrial capital, and financial investors.

After nearly 16 years of accumulation, Meizhong Jiahe has formed two major business directions: one is self-operated medical institutions, mainly serving cancer patients; the other is empowering third-party medical institutions through online business. According to a report by Frost & Sullivan,Among all private oncology healthcare groups in China, Meizhong Jiahe ranked second in terms of the number of self-operated or managed oncology medical institutions as of December 31, 2022.。

In terms of specific revenue, the prospectus shows that Meizhong Jiahe's operating income was RMB 166 million, RMB 471 million, RMB 472 million, and RMB 285 million in 2020, 2021, 2022, and the first half of 2023, respectively, with continuous revenue growth.

However, Meizhong Jiahe has yet to achieve profitability. Its net losses for 2020, 2021, 2022, and the first half of 2023 were RMB 591 million, RMB 831 million, RMB 637 million, and RMB 214 million, respectively. This means that over a period of three and a half years, Meizhong Jiahe accumulated total losses of RMB 2.273 billion.

What are the reasons for continued growth alongside persistent losses? What strategic layout will Meizhong Jiahe adopt after its IPO? How will the private healthcare industry evolve in the future? In response to these questions, this article provides an analysis based on past industry interviews and prospectus data.

The entrepreneurial story of Meizhong Jiahe began in 2008.

At that time, Yang Jianyu, who had earned both a master’s and a doctoral degree in economics from Liaoning University, had already accumulated more than ten years of experience in the real economy sector, including serving for many years as president of Hejia Resources, a company listed on the Shenzhen Stock Exchange with core businesses in solid waste recycling and wastewater treatment. After leaving Hejia Resources, Yang joined Taihecheng at the invitation of a close friend and founded Meizhong Jiahe, which subsequently became Taihecheng’s medical services operating platform in China.

Following its establishment, Meizhong Jiahe initially focused on providing management services for radiotherapy and diagnostic equipment to hospitals in China. It subsequently expanded into online business operations and developed its hospital services through the acquisition, establishment, and operation of self-owned medical institutions.

It is worth emphasizing that Meizhong Jiahe has deeply cultivated the niche sector of oncology.From an industry perspective, oncology hospitals are characterized by high capital investment, long payback periods, and significant barriers to entry, resulting in a high threshold for market participation. Furthermore, the domestic oncology medical services market is currently dominated by public hospitals, with private medical services accounting for a relatively small share.

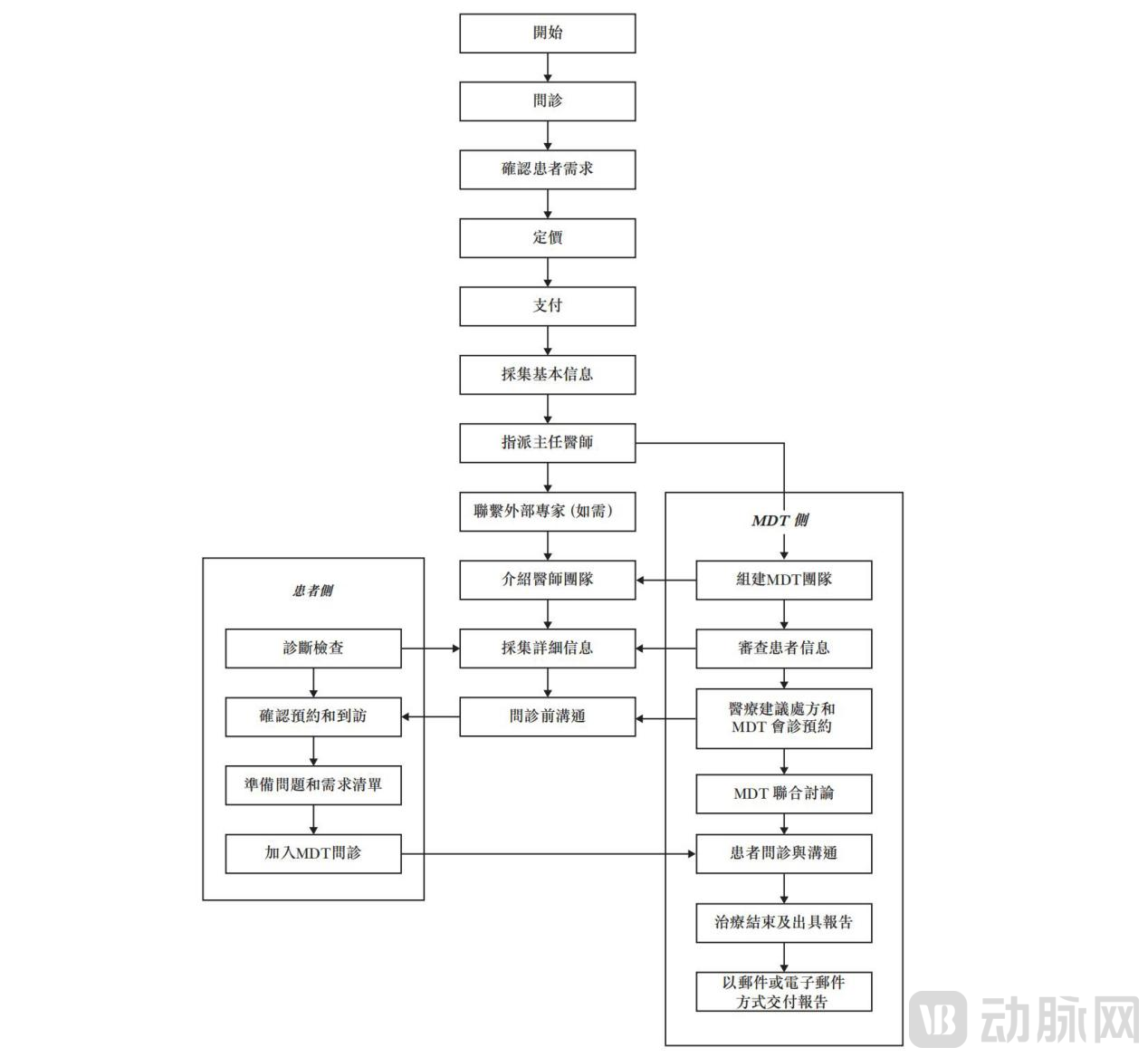

In this context, Meizhong Jiahe has adopted a differentiated approach. On one hand, it has established a dedicated team comprising full-time physicians and nursing staff from various disciplines to provide services through a Multidisciplinary Team (MDT) model. Furthermore, Meizhong Jiahe maintains long-term strategic partnerships with globally renowned medical institutions such as MD Anderson Cancer Center and the Mayo Clinic.

(MDT Practice Workflow. Image source: Prospectus)

(MDT Practice Workflow. Image source: Prospectus)

It is worth noting that multidisciplinary team (MDT) care has become standard practice in Europe and the United States. For instance, the United Kingdom has enacted legislation requiring every cancer patient to receive comprehensive MDT-based treatment. However, the adoption rate of the MDT model remains relatively low in China. According to a report by Frost & Sullivan, only about 6% of cancer treatments in China utilized the MDT model in 2022, compared with approximately 80% in the United States during the same year. Meizhong Jiahe Hospital Management Group Co., Ltd. stands out as one of the few private healthcare institutions in China capable of providing MDT services, enabling it to distinguish itself among numerous oncology service providers.

Leveraging its clinical advantages, Meizhong Jiahe has continuously expanded its service network. It currently operates six self-owned medical institutions in Guangzhou, Shanghai, and Datong, comprising two oncology hospitals, three outpatient centers (or clinics), one diagnostic imaging center, and one internet hospital. Additionally, it has a self-owned oncology hospital under construction in Shanghai. According to the prospectus, the Guangzhou hospital is scheduled to commence operations of its proton center and provide proton therapy services in 2024.

Beyond TO C (providing medical services to patients), Meizhong Jiahe has developed medical devices, software, and related services underpinned by its extensive expertise accumulated over many years in oncology treatment and hospital operations.B2B Business, Serving Enterprise Clients and Hospitals,Especially hospitals in lower-tier cities not covered by Meizhong Jiahe’s own facilities.

According to the prospectus, the number of corporate clients for Meizhong Jiahe’s medical equipment, software, and related services reached 29, 88, 77, and 47 in 2020, 2021, 2022, and the first half of 2023, respectively. As of June 30, 2023, the company provided cloud platform services, management and technical support, and operating lease services to 17 partner hospitals.

Taking cloud platform services as an example, Meizhong Jiahe launched its CSS (Cloud System Solution) service in early 2019. The solution was subsequently iterated and upgraded, leading to the launch of the Jiahe Cloud Imaging Telemedicine Information Diagnosis Platform in December 2020, followed by the Jiahe Feiyun Intelligent Radiotherapy Cloud Service Platform in September 2021, with a focus on enhancing the efficiency and efficacy of cancer treatment.

According to Meizhong Jiahe’s prior introduction, by leveraging CSS, Meizhong Jiahe and its partner hospitals can jointly establish regional oncology diagnostic centers and oncology treatment centers. This enables the centers to provide unified medical services to partner healthcare institutions, while also offering regular training courses to primary-level hospitals and inviting them to participate in scientific research projects.

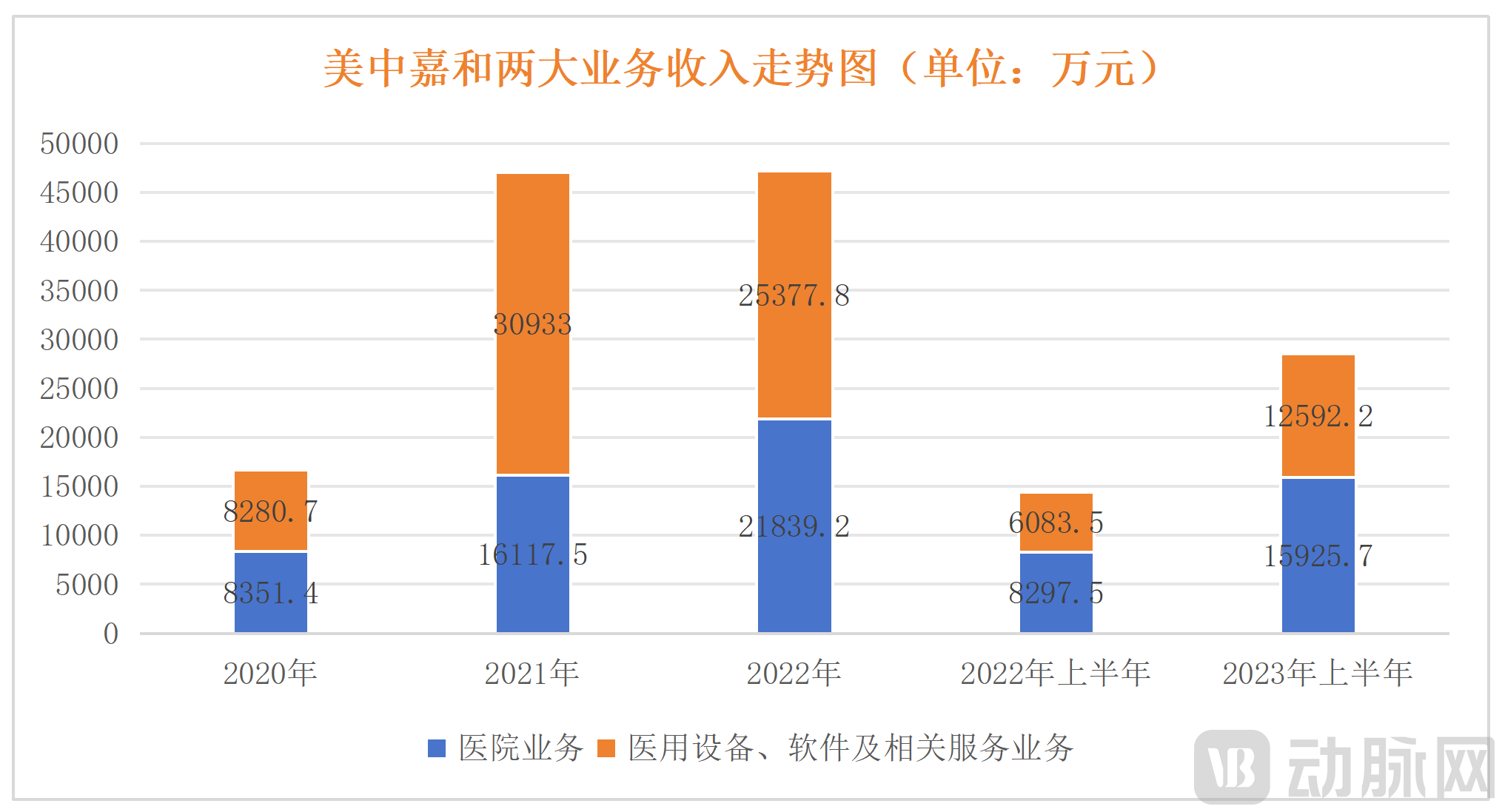

In terms of revenue from respective business segments, the proportions contributed by hospital operations and by medical devices, software, and related services are currently quite similar.: For the hospital operations segment, revenues in 2020, 2021, and 2022 were RMB 83.514 million, RMB 161.175 million, and RMB 218.392 million, respectively; revenues for the first half of 2022 and the first half of 2023 were RMB 82.975 million and RMB 159.257 million, respectively. For the medical equipment, software, and related services segment, revenues in 2020, 2021, and 2022 were RMB 82.807 million, RMB 309.33 million, and RMB 253.778 million, respectively; revenues for the first half of 2022 and the first half of 2023 were RMB 60.835 million and RMB 125.922 million, respectively. Both business segments demonstrated an overall upward trend.

(Data source: Prospectus; Chart by VCBeat)

(Data source: Prospectus; Chart by VCBeat)

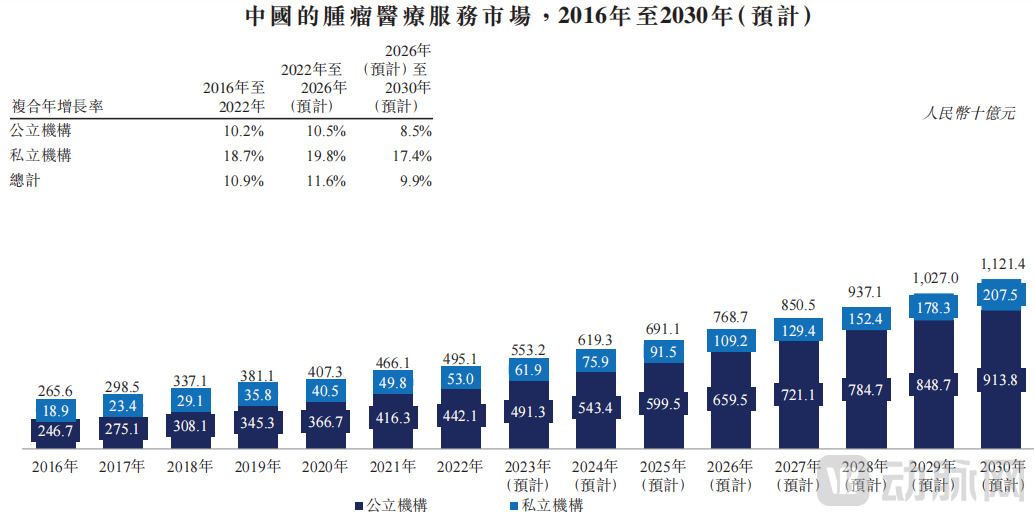

Furthermore, the prospectus specifically notes that revenue of China’s private oncology medical institutions increased from RMB 18.9 billion in 2016 to RMB 53.0 billion in 2022, representing a compound annual growth rate (CAGR) of 18.7%. It is projected to reach RMB 109.2 billion by 2026, indicating substantial market growth potential and broad opportunities for Meizhong Jiahe as a participant in this sector.

As is evident from the above, it was precisely by leveraging the continuous deepening of its B2C and B2B businesses and the rapid market growth that Meizhong Jiahe, after nearly 16 years of dedicated cultivation in the oncology services sector, successfully achieved its initial public offering (IPO).

Is Oncology Really a Good Business?

First, as previously mentioned,The oncology services market is still in a phase of rapid development, with the sector’s growth ceiling yet to be reached.According to the Frost & Sullivan report, the market size of China's private oncology medical services market grew from RMB 18.9 billion in 2016 to RMB 53.0 billion in 2022, with a compound annual growth rate (CAGR) of 18.7%. It is projected to reach RMB 109.2 billion by 2026, representing a CAGR of 19.8% from 2022 to 2026.

(Source of data on China’s oncology medical services market: Prospectus)

(Source of data on China’s oncology medical services market: Prospectus)

Therefore, for companies entering the market,More importantly, it is still essential to build business growth capabilities and synergy, thereby securing a larger share of the “cake.”

Unlike private specialized sectors such as ophthalmology, dentistry, and medical aesthetics, oncology is a capital-intensive business. According to data previously released by Pacific Securities, the average assets per oncology hospital in China amount to RMB 717 million, with an average investment of RMB 226 million in equipment valued at over RMB 10,000 per unit, and an average building area of 44,000 square meters per hospital—all significantly higher than those of other specialized hospitals. It can be seen thatOncology is a specialty that requires greater capital investment.。

Therefore, compared with the scale of dozens or even hundreds of service providers in other specialties, Meizhong Jiahe currently has only six self-operated medical institutions in operation. To continue expanding its scale, Meizhong Jiahe also mentioned in its prospectus that it will continue to increase the number of hospitals.

Furthermore,Oncology, as a field within the more serious realm of medical care, also places significant importance on its academic and clinical accumulation.In response, in addition to continuously strengthening its hospital operations and its business in medical equipment, software, and related services, Meizhong Jiahe is also actively participating in the development of national industry standards, having become a key drafter of national standards for radiation therapy. Currently, three national standard-setting projects have been launched: Guidelines for Quality Assurance Practices in Radiation Therapy Data Review, Guidelines for Building 5G-Based Remote Radiotherapy Planning, Implementation, and Quality Control Platforms, and Practice Guidelines for Total Skin Electron Beam Therapy.

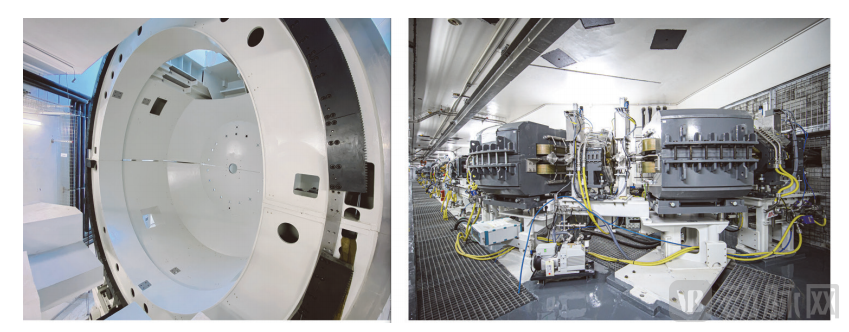

In terms of future strategic layout, Meizhong Jiahe is highly optimistic about proton therapy. The prospectus mentions that Meizhong Jiahe’s Guangzhou hospital has procured a customized four-room proton therapy system, featuring treatment bunkers equipped with four rotating gantries. It is expected to obtain the license in early 2024 and commence operations at the Proton Therapy Center of the Guangzhou hospital in March 2024. Additionally, Meizhong Jiahe will equip its Shanghai hospital with a proton therapy system and four treatment bunkers.

According to the Frost & Sullivan report, as of December 31, 2022, there were approximately 100 operational proton therapy centers worldwide, with only two in China. Furthermore, among the top ten cancer treatment institutions globally, five operate their own proton therapy centers.

(Guangzhou Hospital’s Proton Accelerator and Facilities. Image source: Prospectus)

(Guangzhou Hospital’s Proton Accelerator and Facilities. Image source: Prospectus)

To further promote the application of proton therapy technology, Meizhong Jiahe launched the digital journal *Proton China* in 2014. The journal primarily provides clinical and technical information on proton and heavy ion radiotherapy for reference by patients and the medical community.

Business Synergy, in the course of providing management and technical support services to hospitals, Meizhong Jiahe has accumulated valuable industry expertise and resources. Building on this foundation, it has expanded its hospital business through the acquisition, establishment, and operation of self-owned medical institutions, thereby creating synergies.

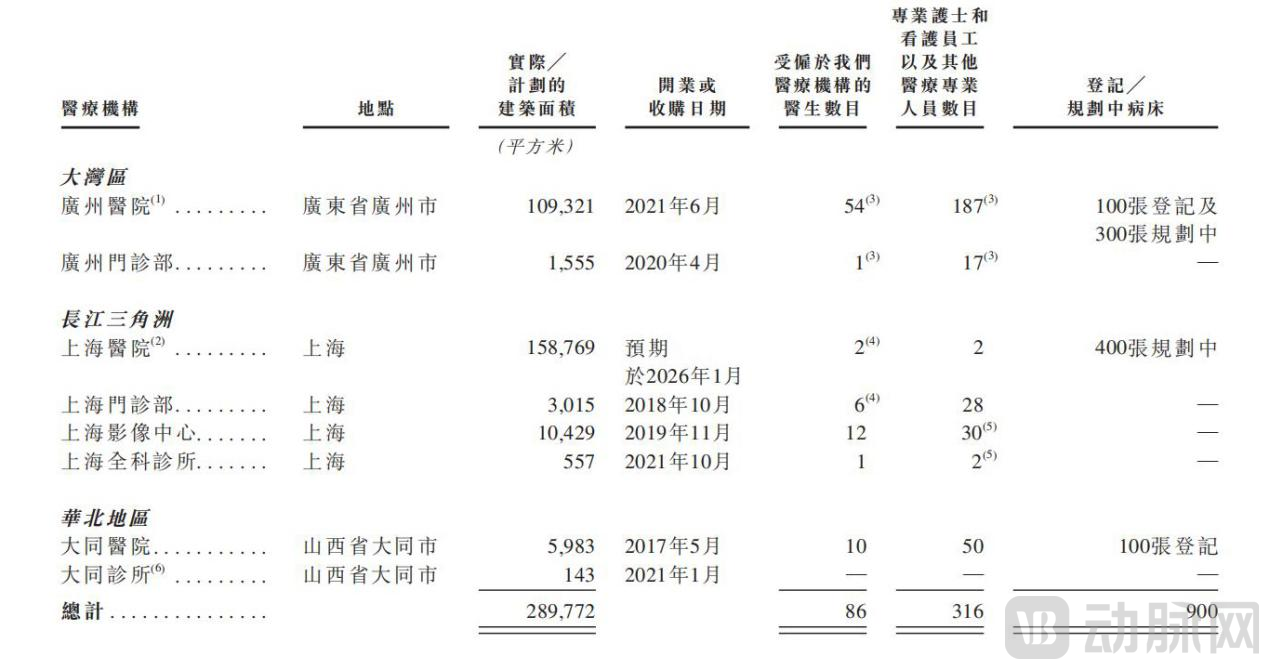

Another example is the strategic synergy considered in the geographic distribution of hospitals. According to the prospectus, Meizhong Jiahe’s hospitals are primarily located in the Greater Bay Area, the Yangtze River Delta, and North China, with differentiated and synergistic business operations in each region, as detailed below:

· In the Greater Bay Area, Guangzhou Hospital and Guangzhou Outpatient Department specialize in radiotherapy for nasopharyngeal carcinoma, surgical treatment of breast cancer, and other comprehensive oncology medical services;

· The Shanghai Imaging Center in the Yangtze River Delta region is a diagnostic center that provides early cancer screening and diagnostic services to patients in the Yangtze River Delta region and across China, leveraging advanced imaging equipment and cloud-based platforms. As a complement to the independent diagnostic services of the Shanghai Imaging Center, the Shanghai General Practice Clinic offers general practice services and collaborates with the Shanghai Imaging Center to provide referral services for patients requiring imaging examinations.

· Datong Hospital and Datong Clinic in North China provide post-treatment health management services using traditional Chinese medicine therapies.

·Furthermore, in May 2021, Meizhong Jiahe launched an internet hospital as a one-stop portal connecting cancer patients with comprehensive oncology healthcare resources.

(Overview of Meizhong Jiahe’s Offline Medical Institutions and Employed Medical Professionals. Image source: Prospectus)

(Overview of Meizhong Jiahe’s Offline Medical Institutions and Employed Medical Professionals. Image source: Prospectus)

As can be seen, Meizhong JiaheHas achieved significant results in building business growth capabilities and enhancing synergy., and proactively positioning for the future, laying a solid foundation for its continued steady growth in the years ahead.

Nevertheless, Meizhong Jiahe remains in a loss-making position, with its gross profit margin turning negative since 2021 (the gross profit margins from 2019 to 2022 were 25.8%, 4.4%, -10.0%, and -30.2%, respectively), indicating significant operational pressure. The prospectus states that many of its medical institutions are still in the start-up phase, and the trial volume expansion stage of new hospitals may have a substantial impact on profitability. Consequently, operating results may fluctuate significantly across different periods. In addition, financing costs (primarily including interest expenses related to redeemable capital injections) are also a major contributor to the losses.

Undoubtedly, following this listing, in facing investors,How to improve profitability will be one of the topics that Meizhong Jiahe needs to think about for a long period of time.

As the first IPO of a private hospital this year, Meizhong Jiahe has undoubtedly provided a significant confidence boost to practitioners in the private specialized medical services sector. From consumer-oriented healthcare segments such as medical aesthetics, dentistry, and ophthalmology, to more serious medical specialties including neurology and oncology, one or multiple listed companies have emerged in each niche. Notable stars include Langzi Medical Aesthetics, Topchoice Medical, Aier Eye Hospital, Hygeia Healthcare, and Sanbo Brain Hospital.

This means that, with excellent diagnostic and treatment capabilities and innovation, private specialized medical services can also transcend disciplinary barriers and emerge as leaders in various niche sectors.

Certainly. In this process, as substantial capital is required for chain expansion and scaling, enterprises’ demand for capital is also very strong. Through past interviews with investors, VCBeat has identified two key factors that venture capital (VC) and private equity (PE) firms consider when assessing whether private specialized healthcare service providers have high growth potential.

First, the size of the market in which the enterprise operates, and whether the supply-demand imbalance in this field is prominent.It is important to recognize that the choice of market segment often determines the pace of a company’s growth. Therefore, private specialized healthcare service providers should focus on development paths that do not rely on public medical insurance reimbursement or compete with public hospitals for patients and market share, thereby securing greater room for expansion.

Second, the enterprise’s own operational capabilities.From the perspective of investors, for single-store operations, the focus is on calculating the ramp-up period and return on investment (ROI), with requirements for the enterprise to achieve specific operational and financial targets within a set timeframe. For chain institutions, the evaluation correspondingly examines regional distribution, economies of scale, and the degree of standardization, followed by metrics such as conversion rates, patient retention, and repeat purchase rates.

Among the two factors mentioned above, the market track determines the ceiling for a company’s future growth, while operational capability determines the size of the “cake” the company can capture. Specifically, the quality of products and services influences conversion strength; optimization of medical processes and efficiency improvements determine patient retention; and physician caliber combined with brand management capabilities drive patient repurchase. This cyclical interaction forms a closed loop in specialized medical services.

Based on this logic, VCBeat, in conjunction with industry interviews, believes thatFour Key Trends to Watch in the Future of Specialized Medical Services

First, the ability of enterprises to leverage SaaS will become increasingly important in the course of their development.This is because SaaS can bring impacts on three levels: first, it means that enterprises have the ability to build a "strong headquarters"; second, it represents that enterprises possess rapid replication capabilities; and third, it enables enterprises to accumulate data from the outset, thereby unlocking the value of subsequent data mining.

Regarding timing, it is best to build a SaaS platform as early as possible. In the initial stages, employees tend to be more receptive to SaaS solutions. However, as the enterprise scales up, employees become accustomed to their existing workflows, and the growing workforce further reduces acceptance of SaaS systems.

In its prospectus, Meizhong Jiahe Hospital Management Group Co., Ltd. stated that following its listing, it will continue to accelerate the National Medical Products Administration (NMPA) registration and commercialization processes for its SaaS products, and develop telemedicine SaaS products.

Second, for private specialized medical institutions, the aggregation of high-quality expert resources is of paramount importance, especially for specialized service providers focused on serious medical care.

Taking the publicly listed Sanbo Brain Hospital as an example, its flagship institution is Capital Medical University Sanbo Brain Hospital. In the medical service capability rankings published by the Beijing Municipal Health and Family Planning Commission, this hospital has consistently ranked among the top in neurosurgery for many years, alongside Tiantan Hospital and Xuanwu Hospital. In terms of its expert team, Sanbo Brain Hospital boasts renowned neuromedicine specialists such as Luan Guoming, Yu Chunjiang, Shi Xiang’en, Wang Baoguo, Yan Changxiang, Wu Bin, Lin Zhixiong, and Fan Tao, thereby forming a robust team of experts.

Third, brand building will bring greater recognition and trust to private specialized medical service institutions.In China, given that public trust in public hospitals is inherently higher than that in private medical service institutions, private specialized healthcare enterprises must place greater emphasis on brand building to instill sufficient confidence among patients.

It is important to note that prioritizing brand building involves more than just marketing and promotion; it also encompasses high-quality service experiences and medical standards. Excessive marketing not only fails to generate positive word-of-mouth and a strong brand reputation, but can also instill insecurity in patients, thereby eroding their trust.

Fourth, high-quality enterprises will also emerge in more segmented and even niche medical specialty service sectors.In fields such as pediatric dentistry, otolaryngology and ophthalmology, and aesthetic dermatology, there is still significant room for improvement in patient education. By offering segmented and precise positioning while ensuring the quality of medical services and patient experience, healthcare providers can effectively capture their target customer base.

The successful IPO of Meizhong Jiahe, along with the prior listings of companies such as Hygeia Healthcare and Sanbo Brain Hospital, demonstrates to the market the immense potential of specialized medical service providers.

Going forward, as healthcare reforms deepen and the overall living standards of the Chinese people continue to rise—accompanied by greater emphasis on and investment in health—the specialized medical services sector is poised to see more companies go public, thereby delivering a broader range of higher-quality solutions to patients.