2023 Annual Innovation White Paper on Medical Services: Slowing Investment, Accelerating Integrated, Continuous, and Accessible Service Innovations

Ping An Healthcare

One-stop Solution Provider for Health Management

In 2023, medical order was restored, supply efficiency improved, and the content of supply became more diverse. Meanwhile, healthcare services also faced challenges such as stricter regulation and slowed investment.

Regardless of the external environment, forging ahead with perseverance remains an enduring theme for industry innovation, as healthcare service innovations oriented toward integration, continuity, and accessibility continue to accelerate.

To provide a clearer understanding of the logic driving industry transformation, this white paper interprets developments across four key dimensions—model innovation, service innovation, management innovation, and payment innovation—by drawing on typical innovative initiatives and their outcomes within the industry since 2023. It highlights ten exemplary innovation cases and provides detailed analyses of the innovation pathways and value proposition of selected cases, with the aim of offering reference insights for the industry.

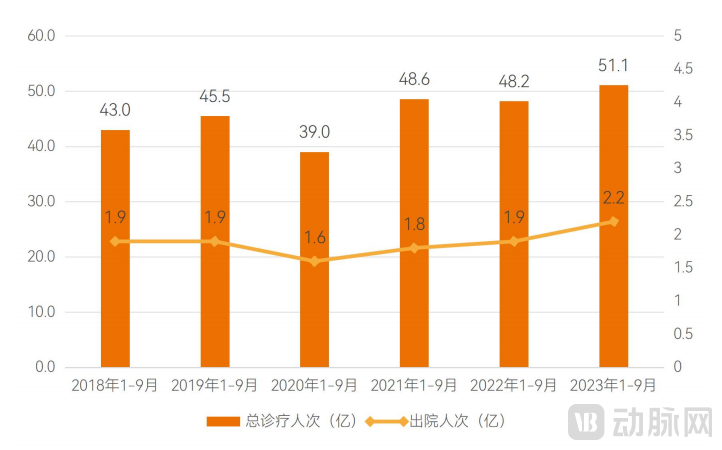

The overall volume of medical services in China has grown, with a significant increase in 2023 compared to both the same period in 2022 and the years 2019 and prior.

Data released by the National Health Commission shows that from January to September 2023, the total number of patient visits at medical and health institutions in China reached 5.11 billion, a year-on-year increase of 6% and a 12.4% increase compared to the same period in 2019. In terms of inpatient services, the number of discharges from medical and health institutions reached 220 million from January to September, a year-on-year increase of 18.9% and a 16.7% increase compared to the same period in 2019.

Changes in the Volume of Medical Services in Recent Years. Data source: National Health Commission; chart compiled by VCBeat.

On the one hand, the release of non-urgent and non-critical care demands, coupled with growth in elective surgery needs, has driven an overall increase in medical service volume. On the other hand, healthcare institutions are better meeting patient needs through supply-side innovations. In the realm of online healthcare, digital resources represented by internet hospitals continue to expand, with over 3,000 internet hospitals now providing online diagnosis and treatment services across China.

From the perspective of healthcare institution types, private hospitals experienced a significant recovery in 2023, aligning with the overall growth trend of hospitals.

According to data released by the National Health Commission, from January to May 2023, hospitals across China recorded 1.67 billion patient visits, a year-on-year increase of 3.5%. Among these, private hospitals accounted for 280 million visits, representing a year-on-year growth of 7.0%.

Policy Data: High-Quality Development and Refined Management in Hospitals Face Greater Challenges

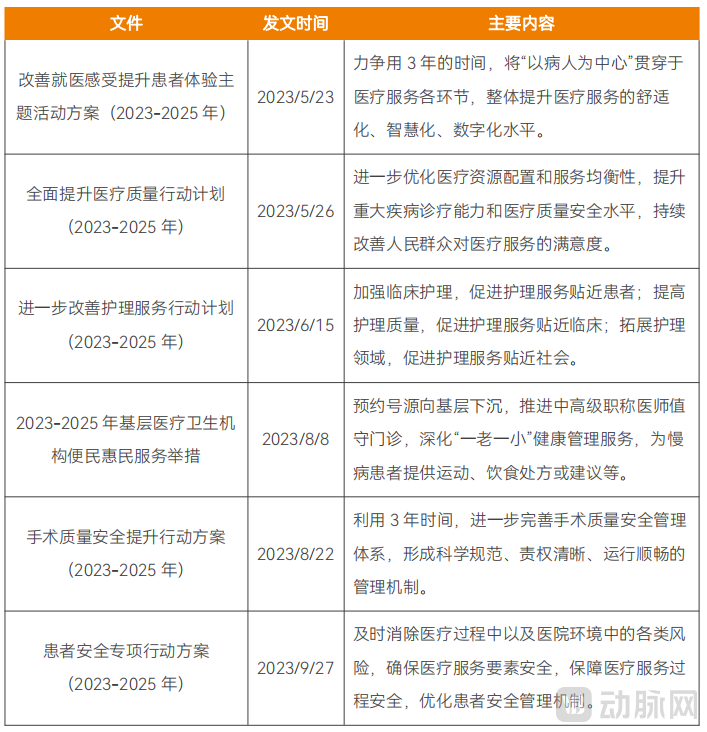

Since 2023, the National Health Commission and the National Healthcare Security Administration have jointly issued over 200 policy documents related to medical services. These policies impose higher requirements on the high-quality development and refined management of hospitals, focusing on improving service quality, anti-corruption in the healthcare sector, centralized procurement, and DRG/DIP payment reform.

In terms of improving the quality of medical services, multiple three-year plans have established phased objectives. For instance, the "Action Plan for Thematic Activities to Improve Medical Access and Enhance Patient Experience (2023–2025)" proposes striving over a three-year period to integrate the principle of "patient-centered care" into all aspects of medical services, thereby comprehensively enhancing the comfort, intelligence, and digitalization of healthcare delivery.

Source: Official Website of the National Health Commission; compiled and charted by VCBeat.

In the realm of anti-corruption in healthcare, a nationwide campaign to rectify corruption in the pharmaceutical sector has swept across China since 2023, driving transformative changes in the communication mechanisms among doctors, hospitals, and pharmaceutical companies. In addition to this concentrated rectification effort, the three-year large-scale inspection initiative will further promote standardized hospital management. The "Work Plan for Large-Scale Hospital Inspections (2023–2026)" issued by the National Health Commission stipulates that the new round of inspections will cover areas such as professional conduct development and hospital operational management, with a particular focus on the centralized rectification of corruption in the pharmaceutical sector in response to prominent issues concerning industry ethics.

Yu Jianlin, Deputy General Manager of GTJA Capital, believes that the anti-corruption campaign in the healthcare sector has impacted the entire medical ecosystem, causing significant short-term disruption. However, it will yield long-term benefits by ensuring that innovative, clinically beneficial, and cost-effective drugs and medical devices are truly accessible to patients. This represents a process of gradually returning to normalcy after enduring growing pains.

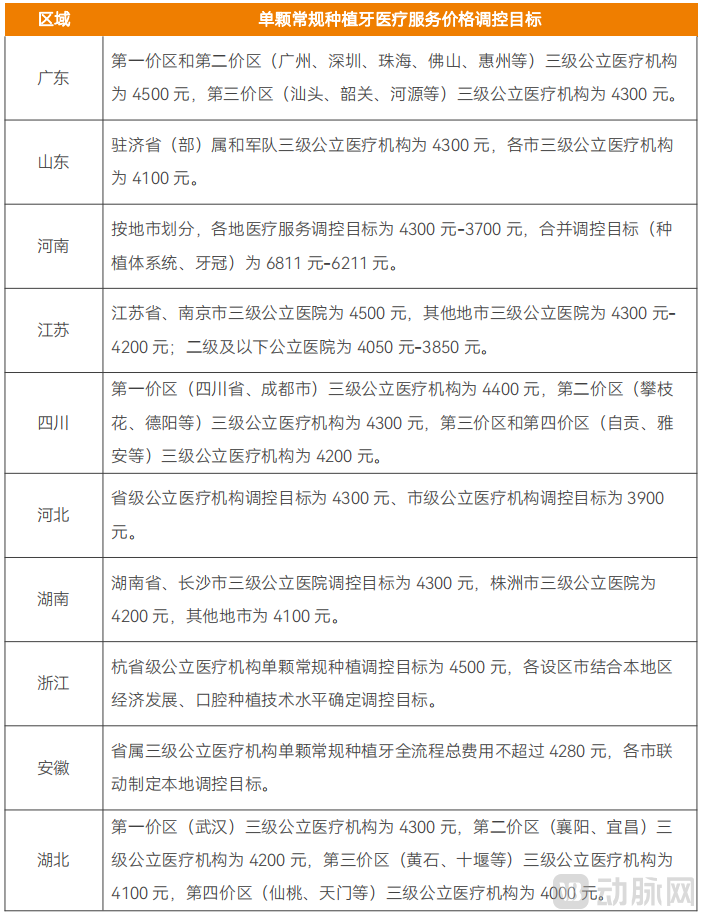

National centralized procurement of pharmaceuticals and medical consumables has become a normalized practice. Since 2023, centralized procurement policies, represented by those for dental implants and orthokeratology (OK) lenses, have extended into the consumer healthcare sector. This signifies that the logic of centralized procurement is exhibiting new characteristics: it covers not only pharmaceuticals and consumables required for disease diagnosis and treatment, but also those needed to improve health status, particularly products addressing the urgent needs and heavy financial burdens of two key demographic groups—the elderly and children. Furthermore, it encompasses not only physical products but also the “centralized procurement” of services.

Price Control on Certain Dental Implant Services in Selected Regions, Source: Official Websites of Local Medical Insurance Bureaus, Compiled and Charted by VCBeat

Furthermore, as of September 2023, actual payment implementation had been achieved in 282 pooling regions across China, accounting for 71% of the total number of pooling regions. All pooling regions under the jurisdiction of 12 provinces (autonomous regions and municipalities directly under the Central Government), including Beijing and Hebei, have fully launched DRG/DIP payment systems. The overall national progress has outpaced the phased task targets, with some regions having already fulfilled the full-coverage requirements stipulated in the Three-Year Action Plan ahead of schedule.

In accordance with policy planning, the reform tasks for DRG/DIP payment methods will be fully completed in 2024. The coming year will be a critical period for healthcare institutions to implement payment method reforms.

Capital Data: Investment Pace Slows Overall, While the Medical and Elderly Care Sector Stands Out

In 2023, overall investment and financing activity in the healthcare services sector declined, yet certain subsectors demonstrated notable resilience. Moreover, eight companies from diverse tracks successfully completed initial public offerings (IPOs), bolstering confidence within the industry.

By the end of 2023, there were a total of 59 financing deals in the primary market for medical services, with a total financing amount of approximately RMB 3.442 billion, representing a decline from the 65 deals and RMB 7.349 billion in financing recorded in 2022.

According to Jiang Xiaodong, Managing Partner at Changling Capital Management, companies with a longer operating history and multiple prior rounds of financing are more likely to secure funding smoothly in the current market. Regardless of profitability, as long as these companies achieve a certain revenue scale and their valuations are reasonable, investors may choose to invest in them to revitalize existing assets. Additionally, companies with innovative business models and rapid growth are also more likely to obtain financing.

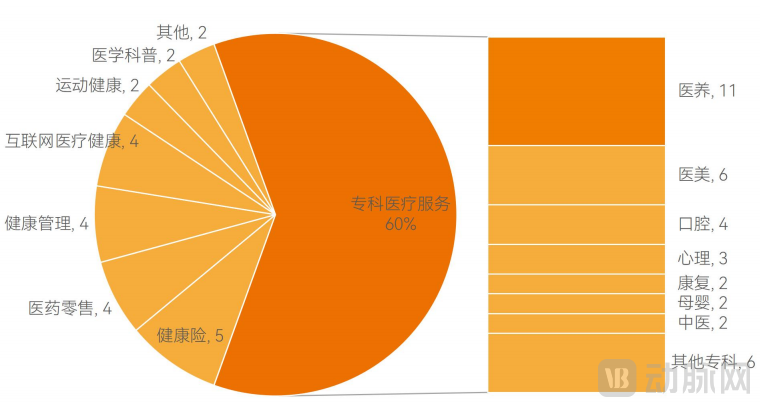

Distribution of Primary Market Financing Deals in the Healthcare Services Sector by Sub-sector. Source: Artery Orange Database; compiled and charted by VCBeat.

From a segmented perspective, the integrated medical and elderly care sector emerged as the most prominent track, with 11 transactions recorded, accounting for the highest proportion.

According to data from the National Bureau of Statistics, China’s natural population growth rate stood at -0.60‰ by the end of 2022, marking the first negative population growth in 61 years and signaling a critical turning point in the country’s demographic structure. Integrated medical and elderly care services are gaining increasing market attention, with high-quality enterprises becoming favored targets for institutional investors.

“Elderly care services are not a traditionally profitable sector,” admitted Wang Bin, Managing Director at iCapital. However, amid heavy industry caution driven by various market conditions, elderly care has emerged as one of the more certain investment areas. Nevertheless, key challenges remain: Will the growth in the elderly population be proportional to the rise in demand? And how can society address the issue of “getting old before getting rich”? These are hurdles that elderly care services must still confront.

Notably, as government-guided funds and state-owned enterprises ramp up their investments in healthcare, several “national team” institutions have also invested in medical services.

Payment Data: Accelerated Digitalization and the Initial Interoperability of Public Health Insurance and Commercial Insurance Information

In 2023, the overall level of medical security continued to improve.

First, the implementation of outpatient benefits under basic medical insurance has yielded significant results. A general outpatient pooling system has been basically established for employee basic medical insurance, covering more than 400,000 pharmaceutical and healthcare institutions. Within the year, reimbursement claims exceeded 2.5 billion visits, with total reimbursed amounts surpassing RMB 200 billion. The outpatient medication guarantee mechanism for hypertension and diabetes (“two diseases”) under resident basic medical insurance has been continuously optimized.

Regarding the National Reimbursement Drug List (NRDL), 126 new drugs have been added to the latest edition, bringing the total to 3,088. In 2023, drugs negotiated during the agreement period benefited over 210 million patient visits. Combined with price reductions and insurance reimbursement, these measures have reduced the financial burden on patients by more than RMB 200 billion.

In terms of centralized procurement of pharmaceuticals and consumables, two national batches covering 80 drugs were conducted within the year, achieving an average price reduction of 57%; centralized procurement was carried out for intraocular lenses and sports medicine consumables, with an average price reduction of 70%; a special governance initiative was implemented for dental implant medical service fees and consumable prices, reducing the overall cost per single dental implant from an average of RMB 15,000 to approximately RMB 6,000–7,000, with a cumulative total of 1.5 million implants placed.

Revenue and Expenditure of the Basic Medical Insurance Fund in Recent Years. Source: Official Website of the National Healthcare Security Administration; Chart compiled by VCBeat.

Data from the National Healthcare Security Administration shows that from January to November 2023, the total revenue of the basic medical insurance fund reached RMB 2.936215 trillion, with total expenditures amounting to RMB 2.491094 trillion. Based on normalized revenue and expenditure trends, the growth rate of expenditures has generally outpaced that of revenues. This disparity is likely to be exacerbated by accelerating population aging, indicating that cost containment remains a severe challenge.

In the commercial insurance sector, the growth rate of health insurance has plummeted from a peak of 67% to 4%, urgently requiring a breakthrough.

According to data from the National Financial Regulatory Administration, the revenue scale of health insurance has continued to grow over the past decade, and its proportion in life insurance has also been steadily increasing.

However, on the other hand, health insurance has shown a trend of slowing growth, declining from 50%-60% during its peak growth period to below 5% in the past three years. In light of current demands and trends within the healthcare service system, health insurers need to expand coverage for individuals with non-standard health risks through product innovation and strengthen health management services for this population.

Growth in Original Premiums of Health Insurance Over the Past Decade; Source: Official Website of the National Healthcare Security Administration, Chart Compiled by VCBeat

In July 2023, the Shanghai Municipal Healthcare Security Administration and six other departments jointly issued the "Several Measures of Shanghai Municipality to Further Improve the Multi-Payer Mechanism in Support of the Development of Innovative Drugs and Medical Devices," which outlined 28 key tasks, 16 of which pertained to promoting the standardized development of commercial health insurance. For instance, eligible commercial insurance companies may, on the basis of compliance and security, legally leverage big data from healthcare and medical insurance sources to conduct actuarial analyses, develop market-appropriate products, achieve scientific and precise pricing, effectively reduce risk control costs, and lower product prices.

Previously, the National Healthcare Security Administration launched a pilot program for authorized access and use of personal medical insurance information in 12 cities across China. In these pilot cities, insured individuals can not only query and obtain their personal medical insurance information through various online and offline channels but also, upon granting personal authorization, share relevant personal information with commercial insurance companies, thereby facilitating processes such as purchasing commercial insurance policies and filing claims.

Historically, commercial health insurance has faced numerous pain points in underwriting and claims settlement due to a lack of in-hospital diagnosis and treatment data. This data insufficiency is one of the key reasons why few insurance products have been designed for individuals with non-standard health profiles.

With the accelerating digitalization of medical insurance and the expanding scope of data applications, medical insurance data is poised to play an increasingly vital role in driving innovation in commercial health insurance. In turn, such innovation will better complement public medical insurance, contributing to the refinement of China’s multi-tiered healthcare security system.

Model Innovation: Expanding Resource Supply to Promote the Expansion and Balanced Distribution of High-Quality Resources

To further promote the expansion, decentralization, and balanced distribution of high-quality medical resources, China is currently making vigorous efforts to accelerate the development of National Medical Centers and Regional Medical Centers. To date, 13 National Medical Centers have been established, and five batches of approvals have been granted for 125 construction projects across 29 provinces for National Regional Medical Centers.

The essence of National Medical Centers and Regional Medical Centers lies in, on the one hand, further strengthening the capabilities of existing high-quality medical resources in the diagnosis and treatment of complex and critical conditions, the training of high-level medical professionals, and the translation of high-level basic medical research and clinical research findings; and on the other hand, promoting the rational allocation of high-quality resources through the flow and joint development of technology, talent, infrastructure, and other elements.

For private healthcare providers, it is still possible to promote the expansion and balanced distribution of high-quality medical resources through the development or circulation of premium assets, thereby forming a complementary relationship with the public healthcare system.

As Bang’er Orthopedics was selected as one of the first batch of alliance members of the National Orthopedic Medical Center’s 5G + Orthopedic Robot Initiative, it leverages 5G-enabled orthopedic robotic technology to make surgeries more intelligent and minimally invasive, thereby promoting the decentralization of high-quality medical resources.

Service Innovation: Strengthening Integration, Continuity, and Accessibility to Enhance the Quality of Medical Services

Enhancing the quality of medical services encompasses all aspects, including improving the management systems and standards for medical quality and safety, implementing codes of conduct for medical service delivery, and raising the level of standardization and normalization in medical services.

Currently, the country is advancing the establishment of medical quality control centers, including national-level, provincial-level, municipal (prefectural)-level, and county (district)-level medical quality control centers (groups). These centers will play a significant role in carrying out medical quality safety management and control work in medical institutions.

Ensuring medical quality requires establishing robust institutional frameworks as a baseline, while pursuing value-based healthcare as an overarching goal to achieve higher levels of care.

Guolian Healthcare leverages payment system reform as a breakthrough to explore value-based healthcare, while focusing on building “high-quality rehabilitation” to maximize medical quality and treatment outcomes, thereby fully implementing value-based healthcare.

Enhancing drug supply assurance and pharmaceutical care services is also an integral part of improving healthcare quality.

Shanghai Pharma Cloud Health Launches Yiyao·Integrated Flagship Model, Integrating Innovative Drug Specialty Pharmacies with Internet-Plus Cloud Pharmacies to Enhance Accessibility of New Specialty Drugs and Common Chronic Disease Medications, While Continuously Innovating Pharmaceutical Care Services.

Currently,The healthcare service system is advancing a shift from being “disease-centered” to “health-centered,” necessitating the accelerated development of an integrated prevention-and-treatment model and the establishment of a comprehensive prevention-and-treatment system., including disease control and prevention institutions at all levels, medical institutions, and primary healthcare facilities, to strengthen collaboration and coordination among different entities, thereby forming a synergistic effort to enhance the effectiveness of prevention and treatment. In particular, it is essential to strengthen the management of key populations and priority diseases, such as providing targeted health promotion and preventive care services for pregnant and postpartum women, infants and young children, students, occupational groups, and the elderly.

Amid the accelerating trend of population aging, cancer prevention and control must not be underestimated. Currently, strengthening cancer prevention, screening, early diagnosis and treatment, and scientific research has become a priority. Concentrating superior resources to achieve key breakthroughs in critical areas—such as pathogenesis, prevention and treatment technologies, resource allocation, and policy support—has emerged as the focal point of these efforts.

Following the initial proposal of “Ecological Cancer Prevention” in 2022, Yingkang Life continued in 2023 to drive the transformation of oncology medical services from disease diagnosis and treatment to full-lifecycle management encompassing “prevention, diagnosis, treatment, and rehabilitation,” thereby accelerating the shift in cancer prevention and control models.

Based on the number of participants in China's national employee basic medical insurance, the working population is substantial, and workplace health has become an increasingly prominent social issue.

Ping An Healthcare has upgraded its “Yi Qi Jian Kang” product suite, offering more flexible and efficient customized solutions to provide enterprises with systematic, end-to-end employee health management services, thereby helping them enhance human resource efficiency.

In the traditional healthcare service system, fragmentation exists among different types of services—such as prevention, diagnosis and treatment, and health maintenance—resulting in a lack of effective integration. Healthcare institutions at various levels often deliver discontinuous services with poor information flow. When patients seek care across different facilities, the discontinuity in medical information transfer hinders the creation of comprehensive records and assessments, thereby compromising the quality of healthcare services.

In recent years, driven by digitalization, continuous medical services spanning online and offline channels, in-hospital and out-of-hospital settings, and across all service stages have emerged., particularly by organizing various resources into continuous services centered on specialized departments or specific diseases, has played a significant role in enhancing healthcare quality.

For example, JD Health has currently launched 27 specialty centers. In 2023, it focused on refining services in dermatology, mental health, and traditional Chinese medicine (TCM), by detailing the content of specialty-specific and disease-specific services and establishing a closed-loop service model.

Furthermore, in terms of enhancing the convenience and accessibility of services, Xiaocheng Group, taking into account the varying needs of users at different stages, addresses the conflict between high product unit prices and usage demands through an assistive device rental model, and empowers the assistive device rental industry with full-process digitalization.

Management Innovation: Revitalizing Management Models through Human Resources, Standardization, and Other Dimensions to Generate Sustained Momentum

Management innovation in healthcare institutions must be approached from multiple dimensions, including operational systems, human resources, and brand building. Meanwhile, healthcare institutions across different specialties and tiers need to establish management models tailored to their specific contexts.

Taking human resource management as an example, although both ophthalmology and dentistry are consumer healthcare institutions, ophthalmology is highly dependent on equipment, whereas dentistry relies heavily on physicians’ clinical skills. This distinction necessitates that dental institutions prioritize investment in human resource management.

In 2023, Meivi Dental’s newly upgraded “Star Program” was fully implemented across its affiliated institutions, establishing a sustainable human resources advantage; it will continue toIterationThe Partnership Model: Helping to Solve the Talent Shortage in Dentistry.

Chain management of healthcare institutions also involves the critical issue of standardization. Standardization makes management more standardized and simplified, reduces operating costs, and improves management efficiency; it also enables enterprises to achieve rapid replication more easily, capture larger market shares, and accelerate expansion. Standardization is particularly important in asset-heavy, low-gross-margin segments with a scarcity of talent.

For example, Jinxin Fuxing Health and Elderly Care centers on the integration of medical care and elderly support. In 2023, it established a career grading and promotion system for care specialists, refined standardized management practices in elderly care institutions, and laid the foundation for expanding its chain operations.

Payment Innovation: Precisely Reducing the Payment Burden on Target Populations to Promote the Diversification of Health Insurance Products

Amid the trend of population aging, the incidence of chronic diseases characterized by long disease courses and high treatment costs is rising. Meanwhile, as elderly individuals experience declining organ function, some partially or completely lose their ability to perform activities of daily living, and even develop cognitive impairments, leading to increased demand for nursing services and a heavier caregiving burden. Furthermore, in recent years, influenced by factors such as life stress and lifestyle habits, the population with conditions represented by breast abnormalities, pulmonary nodules, thyroid nodules, and prediabetes has been growing.

However, mainstream health insurance products have long covered mostly healthy individuals, but these products are becoming increasingly homogeneous, competition is intensifying, and their penetration rate among the healthy population has already reached a high level.

On one hand, a large population of non-standard and pre-existing condition holders struggles to obtain health insurance coverage that matches their needs; on the other hand, the health insurance market is experiencing sluggish growth.

The “Implementation Plan for the Healthy China Action—Cancer Prevention and Control Action (2023–2030)” proposes encouraging qualified commercial insurance institutions to develop commercial health insurance products related to cancer prevention and control. Previously, the “Guiding Opinions on Further Enriching the Supply of Life Insurance Products” issued by the General Office of the former China Banking and Insurance Regulatory Commission also mentioned further raising the upper age limit for policyholders and accelerating the fulfillment of insurance coverage needs for elderly individuals aged 70 and above. It called for appropriately relaxing underwriting conditions to provide reasonable coverage for elderly individuals with pre-existing conditions and chronic diseases.

Thus, health insurance products tailored for individuals with non-standard risk profiles or pre-existing conditions are poised to become a breakthrough in resolving this contradiction.

In 2023, Yuanmeng Health, in collaboration with industry partners, launched the “Brain Health Care” specialized insurance product for Alzheimer’s disease, and will focus on exploring innovative integration of “health insurance + health services” for individuals with chronic diseases and the elderly population.

In an ecosystem aimed at innovating health insurance for non-standard and pre-existing condition populations, medical providers, pharmaceutical companies, insurers, and third-party service platforms can leverage their respective strengths to create complementary advantages, thereby serving a broader population while achieving their own development.

The above is an excerpt of the main content of the report. Below are outstanding innovation case studies of the year. Scan the QR code on the poster to access the full report.

Report Table of Contents:

PART 01: 2023 Healthcare Services in Numbers

1.1 Service Data: Full Restoration of the Medical Service System and Improved Service Efficiency

1.2 Policy Data: Greater Challenges for High-Quality Development and Refined Management in Hospitals

1.3 Capital Data: Overall Investment Pace Slows, While the Medical and Elderly Care Sector Stands Out

1.4 Payment Data: Accelerated Digitalization and the Initiation of Information Interoperability Between Basic Medical Insurance and Commercial Health Insurance

PART 02 Innovative Insights into the Healthcare Services Sector

2.1 Model Innovation: Expanding Resource Supply to Promote the Expansion and Balanced Distribution of High-Quality Resources

2.2 Service Innovation: Strengthening Integration, Continuity, and Accessibility to Enhance the Quality of Medical Services

2.3 Management Innovation: Revolutionizing management models from dimensions such as human resources and standardization to create sustained momentum

2.4 Payment Innovation: Precisely Reducing the Financial Burden on Target Populations to Promote Diversification of Health Insurance Products

PART 03: Interpretation of Innovative Cases in Medical Services

3.1 Ping An Healthcare: Upgrading the Corporate Health Management Product Portfolio and Accelerating Market Ecosystem Development

3.2 Yuanmeng Health: Leveraging Alzheimer’s Disease-Specific Insurance as an Entry Point to Explore Innovations in the “Insurance + Health Services” Model

3.3 Yinkang Life: Implementing Full-Lifecycle Management of “Prediction, Diagnosis, Treatment, and Rehabilitation” to Accelerate the Transformation of Cancer Prevention and Control Models

3.4 Meiwei Dental: Upgrading the Partner System to Build a Sustainable Human Resources Advantage

3.5 GuLian Medical: Building “High-Quality Rehabilitation” and Implementing the Concept of Value-Based Healthcare

3.6 JD Health: Innovating Specialized Internet Healthcare Services through In-Depth Resource Integration and Process Reengineering

Appendix 1: Details of Financing for Healthcare Service Enterprises in 2023

Appendix 2: Key Policies in the Medical Services Sector in 2023