White Paper on Smart Ultrasound Industry: A Comprehensive Insight into Digital Intelligence and Commercial Innovation in Medical Ultrasound

As a mature yet rapidly evolving medical imaging technology, medical ultrasound is playing an increasingly prominent role in clinical diagnosis and treatment. This report systematically reviews the development history, market size, and industrial ecosystem of medical ultrasound, with a particular focus on the latest advancements and application innovations in intelligent ultrasound. It provides an in-depth analysis of the opportunities and challenges facing the industry, and projects that ultrasound technology will continue to evolve toward greater precision, intelligence, and integration, thereby contributing to the overall enhancement of medical diagnostic and therapeutic capabilities.

Currently, medical ultrasound is accelerating its evolution toward precision diagnosis and treatment, as well as intelligent upgrades. The deep integration of multi-source heterogeneous information empowers the intelligent recognition and analytical capabilities of ultrasound systems. Innovative applications of emerging technologies—such as artificial intelligence, the Internet, big data, 5G, and cloud computing—in the field of ultrasound, along with their integrated practices across diverse scenarios, provide robust support for enhancing ultrasound equipment performance, upgrading business models, and ultimately improving the overall level of healthcare services.

However, the journey from the concept of intelligent ultrasound to its practical implementation remains long and arduous. The report concludes with a strategic analysis of the challenges currently facing the medical ultrasound industry and offers proactive recommendations for its development.

Currently, public hospitals in China are fully equipped with ultrasound devices, leaving limited room for market growth. Future incremental market demand will primarily depend on private hospitals, primary healthcare institutions, and the establishment of new departments in public hospitals. As primary healthcare institutions mainly require mid- to low-end ultrasound equipment, the significant increase in the number of such facilities will drive a corresponding expansion in the mid- to low-end ultrasound equipment market.

1Ultrasound therapy exhibits significant heterogeneity across hospitals and departments, with a substantial gap in the demand for specialized, precision diagnosis and treatment.

Historically, the sales of ultrasound equipment have been primarily concentrated in hospital radiology departments. However, with the continuous evolution of medical technology, there is a growing demand for therapeutic ultrasound devices in specialized medical fields. Due to the diversity of specialized applications, these devices have unique and still largely unmet needs regarding technological iteration and functional updates. Currently, patient and consumer awareness and acceptance of therapeutic ultrasound devices remain relatively low, which has somewhat constrained the expansion of market demand. Furthermore, in certain clinical scenarios, therapeutic ultrasound technology faces competition from other physical therapies (such as laser therapy and electrotherapy) as well as pharmacological treatments, thereby indirectly limiting the widespread adoption of therapeutic ultrasound technology.

Notably, the adoption of ultrasound therapeutic devices in tertiary Grade A hospitals has shown a steady upward trend. Currently, leveraging ultrasound technology to enhance the precision of clinical diagnosis and treatment has gradually become mainstream. To improve physicians’ proficiency in operating ultrasound equipment and promote its application across various departments, the National Health Commission launched the “Program for Enhancing Skills in Ultrasound-Guided Precise Diagnosis and Treatment in Clinical Departments” in April 2023. This program places particular emphasis on the application of ultrasound in anesthesiology, pain management, orthopedics, rehabilitation, and emergency/critical care. By enhancing physicians’ operational skills and exploring effective promotion models, the program aims to strengthen the value and practicality of ultrasound in assisting diagnosis and treatment.

2Continued Realization of Policy Dividends for Medical Devices

As a key industry supported by the state, the medical device sector has benefited from industrial policies that actively promote its development. In recent years, China has successively introduced a series of policies and regulations to support the innovative development of medical devices. The “14th Five-Year Plan” for the Development of the Medical Equipment Industry, released in 2021, proposed the development of next-generation medical imaging equipment, promoting advancements in intelligence, remote capabilities, miniaturization, rapid processing, precision, multi-modal fusion, and integrated diagnosis and treatment. In the same year, the Outline of the 14th Five-Year Plan for National Economic and Social Development and the Long-Range Objectives Through the Year 2035 called for the development of high-end medical equipment and the improvement of fast-track review and approval mechanisms for medical devices. The introduction of these favorable policies has also encouraged Chinese medical device companies to enhance their independent R&D capabilities, accelerating product innovation and iteration while driving the development of the smart ultrasound industry.

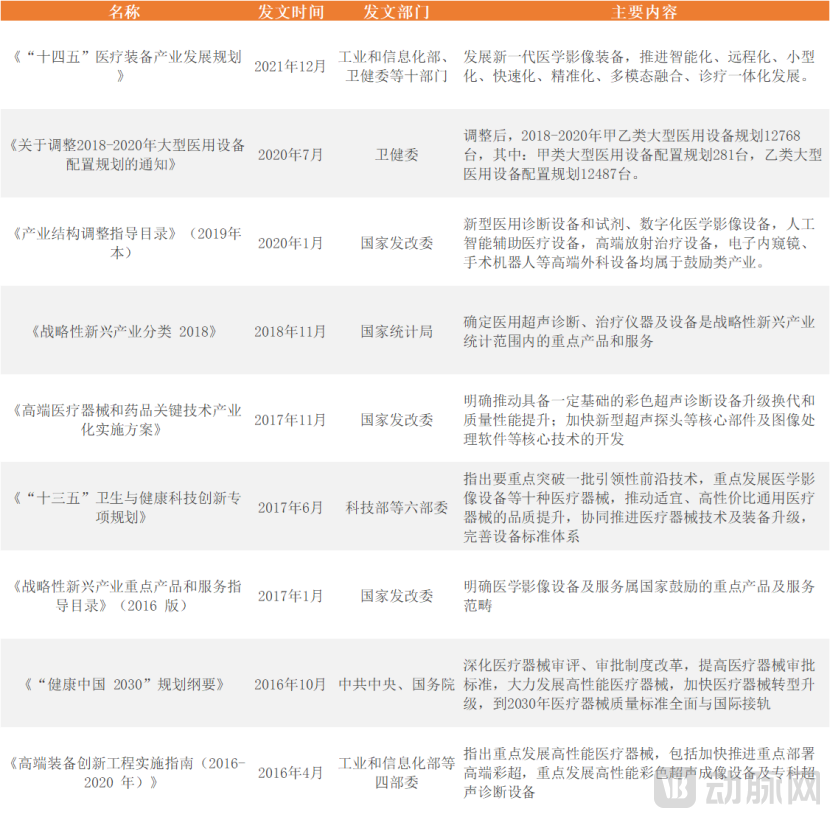

Industry Guidance Level: A Holistic Perspective on Stabilizing the Product Quality and Safety of Medical Ultrasound Devices

The implementation of the "Plan for Adjusting the Allocation of Large Medical Equipment from 2018 to 2020" aims to further optimize the allocation of large medical equipment, promote the scientific and rational distribution of medical resources, and meet the new demands of China’s health sector development. This initiative has also accelerated the upgrading of hospital medical equipment, benefiting large-scale devices such as ultrasound systems. Subsequently, the state has established regulations and guidance for the medical ultrasound industry regarding its development direction, industrial requirements, and production quality management. These measures have safeguarded the healthy development of the industry, improved product quality and safety, and contributed to the overall advancement of China’s medical device industry.

Guidance Policies for the Medical Ultrasound Industry

Data Source: Public Information, VCBeat.

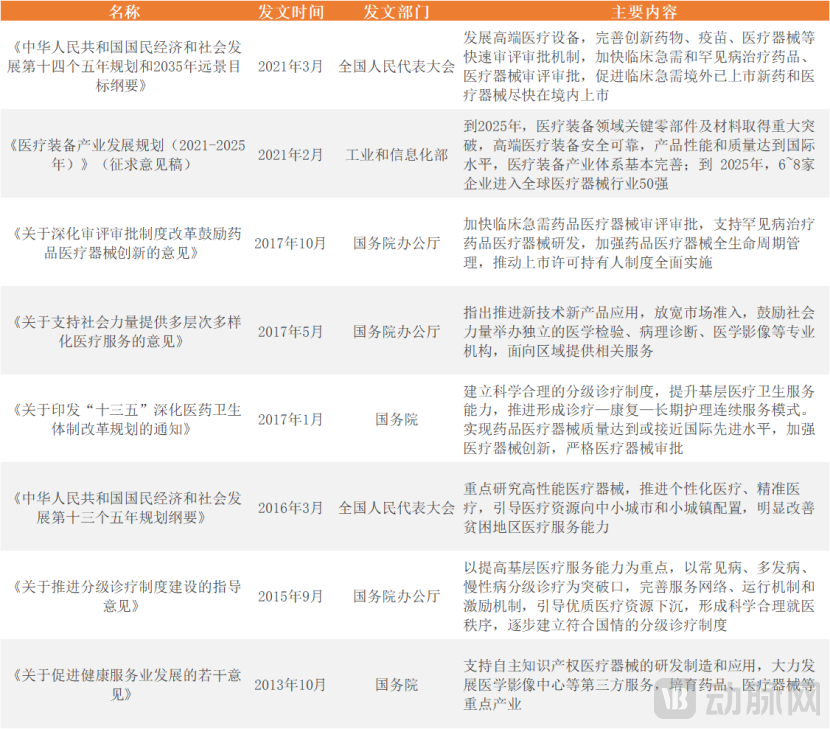

Market Promotion Level: Advocate for healthy competition within the industry to increase the market share of domestically produced medical ultrasound devices.

With the implementation of the tiered diagnosis and treatment system, enhancing the comprehensive capabilities of county-level public hospitals has become a key priority. This will drive these hospitals to optimize their medical equipment configurations, thereby increasing the demand for ultrasound medical devices to some extent. In 2017, the "Opinions on Supporting Social Forces in Providing Multi-level and Diversified Medical Services" explicitly mentioned promoting the application of new technologies and products, relaxing market access restrictions, and encouraging social forces to establish specialized institutions in fields such as medical laboratory testing, pathological diagnosis, and medical imaging. By striving for excellence in these vertical niche segments and providing standardized services to patients, these measures help weaken the competitive advantage of imported medical devices in the domestic market and promote the improvement of the quality of domestically produced medical ultrasound equipment.

Market Promotion Policies for the Medical Ultrasound Industry

Data source: Public information, VCBeat

Industry Innovation: Steadily Enhancing Domestic Technological Innovation Capabilities, Smart Ultrasound Emerges as the Times Demand

In 2020, the Ministry of Science and Technology issued a document explicitly calling for strengthened application of 5G technology and artificial intelligence (AI), facilitating their integration into high-end medical devices. With robust national support for AI in medicine—including efforts to build telemedicine systems, advance the Healthy China Cloud Service Initiative, and develop integrated healthcare service platforms—medical AI enterprises have achieved rapid growth. Against this policy backdrop, traditional medical ultrasound equipment is undergoing an intelligent transformation. By leveraging advanced cloud computing and AI technologies, ultrasound devices are continuously incorporating cutting-edge innovations to enable remote and mobile diagnostic and therapeutic services, as well as AI-assisted medical imaging. These enhanced capabilities have significantly improved the accuracy and efficiency of diagnosis and treatment.

Industrial Innovation Policies for the Medical Ultrasound Industry

Data Source: Public Information, VCBeat

As the macroeconomic environment continues to improve, application scenarios for medical devices are gradually recovering and expanding, driving a rise in market demand for ultrasound equipment. Against the backdrop of increasingly robust policy support in China, domestic enterprises should remain steadfast in their commitment to independent innovation and R&D, continuously advance the upgrading and iteration of core products, increase their market share, and help propel the medical ultrasound industry toward intelligent transformation.

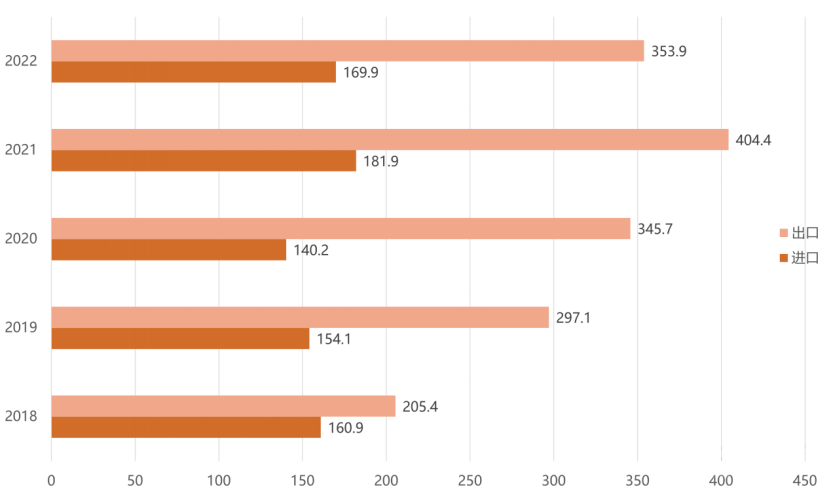

3Chinese-Made Equipment Achieves Trade Surplus, Accelerating Benefits for Industry Leaders

While steadily increasing their domestic market share, Chinese manufacturers of medical ultrasound diagnostic equipment are also continuously expanding into international markets. Developing countries with lower income levels and high cost sensitivity, such as those in Southeast Asia, the Middle East, and Africa, constitute the primary export destinations for Chinese ultrasound devices. In 2022, China’s import volume of ultrasound instruments reached 1.699 million units. On the export side, the quantity of Chinese ultrasound instruments exported has continued to rise, growing from 2.054 million units in 2018 to 3.539 million units in 2022, among which the export value of Chinese color Doppler ultrasound equipment reached US$1.07 billion.

2018–2022 Import and Export Volume of Ultrasound Instruments in China (Units)

Data Source: General Administration of Customs, VCBeat

In terms of import value, China’s market for imported medical ultrasound equipment remains substantial, with a pronounced reliance on high-end products. China primarily imports ultrasound systems from the United States, South Korea, Japan, Austria, and Norway. In the first half of 2022, imports from the United States accounted for 34% of China’s total ultrasound system imports, while those from South Korea, Japan, Austria, and Norway represented 19%, 15%, 14%, and 6%, respectively. These countries possess foundational expertise in ultrasound technology, and their well-established brand reputations confer strong competitiveness among high-end users in the market.

Driven by policy incentives and advancements in the technological capabilities of domestic enterprises, the import share of China’s ultrasound equipment market has been gradually shrinking, a trend particularly evident in the low-end segment. If leading companies can sustain their efforts in intelligent R&D and brand building to capture market share in the mid-to-high-end segments, China’s international competitiveness will be further enhanced. Furthermore, by targeting customers in developing countries and certain middle-income nations and highlighting cost-performance advantages, China can accelerate the development of its smart ultrasound equipment industry.

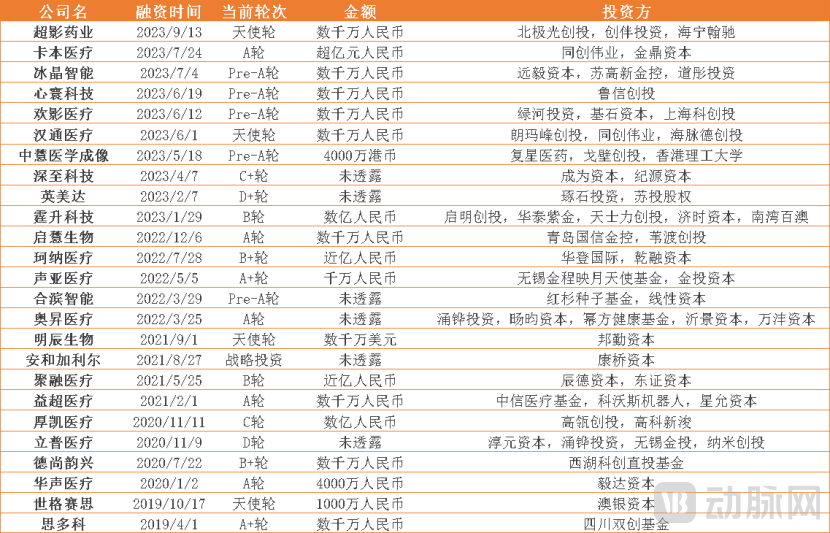

4Capital Empowers the Enhancement of Local Strength

Based on investment and financing data, the ultrasound industry in China has remained active in recent years. Current capital investments are primarily directed toward the field of medical ultrasound diagnostic equipment, with a particular focus on companies that prioritize technological R&D and innovation, as well as those demonstrating excellence in developing high-performance, cost-effective, and portable ultrasound diagnostic devices. Meanwhile, investors also favor enterprises that exhibit outstanding capabilities in expanding production capacity and integrating the industrial chain.

Investment and financing channels for participants in China’s ultrasound industry are well-defined, and companies that have secured funding possess relatively robust strategic layouts. The vast majority of these enterprises plan to utilize the capital to expand production scale, improve capacity utilization rates, and achieve industry-wide economies of scale by optimizing the industrial chain and resource allocation.

Investment and Financing Data in China's Ultrasound Industry Over the Past Five Years

Data source: VCBeat

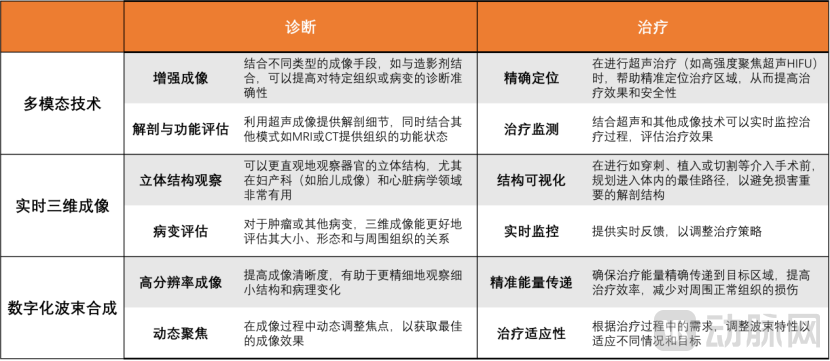

1Multi-Technology Powering: Decoding the Cornerstone of Smart Ultrasound Technology

In accordance with the specific provisions of the “Implementation Plan for the Industrialization of Key Technologies in High-End Medical Devices and Pharmaceuticals” regarding key technologies, critical components, and major performance indicators for color ultrasound diagnostic equipment, a review of the technological status of major domestic and international manufacturers in the same industry reveals that “multimodal technology, real-time 3D imaging, and digital beamforming” remain the core focus of ultrasound research and development. The integrated advancement of these three technologies has not only significantly improved the diagnostic accuracy and efficiency of ultrasound but also opened up new possibilities for its widespread adoption and precision across various medical scenarios, serving as a key driver of future transformation in the field of smart ultrasound.

Overview of Key Technologies in Smart Ultrasound

Source: VCBeat

2A Blossoming of Smart Ultrasound Technologies Continuously Expands the Boundaries of Application

With the rapid advancement of intelligent ultrasound technology, cutting-edge innovations such as multimodal technology, real-time 3D imaging, and digital beamforming are undoubtedly driving industry transformation, while other complementary technologies also play a significant role in the field of ultrasound.

For instance, high-frequency ultrasound technology provides higher-resolution images by utilizing ultrasound waves at higher frequencies. This enhancement is particularly significant for image clarity, especially in applications requiring high-detail resolution, such as dermatology, ophthalmology, and animal imaging. This not only strengthens the application potential of ultrasound in these specific fields but also sets new standards for the detection of subtle structures. Meanwhile, the emergence of elastography has further broadened the scope of ultrasound applications, with its importance in oncology being self-evident. It offers a non-invasive means to assess the physical properties of tumors, thereby assisting physicians in making more precise diagnoses. By measuring tissue response to mechanical stress, elastography reveals tissue elasticity properties, providing new perspectives for the differential diagnosis of benign and malignant tumors.

Furthermore, the deep integration of artificial intelligence (AI) and ultrasound has become an inevitable trend. It is reported that Hefei Hebin Intelligent Robot Co., Ltd. (hereinafter referred to as “Hebin Intelligence”) has successfully combined high-precision, low-latency robotic teleoperation technology with full-stack AI technologies and applied them to the field of ultrasound diagnosis and treatment. Through this initiative, the company has established a standardized system for automated acquisition of ultrasound images. By adopting a model that separates scanning from diagnosis, it has expanded remote services, fundamentally addressing the shortage and uneven distribution of ultrasound medical resources.

Advancements in the smart ultrasound industry depend not only on the evolution of cutting-edge technologies but also, and more critically, on the continuous innovation and expanded application of supporting technologies, which make substantial contributions to improving diagnostic and therapeutic quality. It is through the convergence of these technologies that a new chapter in future ultrasound medicine—integrating high-end imaging, intelligent analysis, and automated operations—can be fully realized.

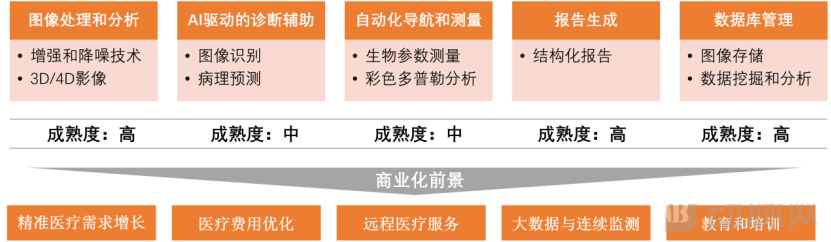

Endless Application Expansion, Uncovering Opportunities in Innovative Fields

Overview of Core Technologies and Commercial Prospects in Smart Ultrasound

Source: VCBeat

With the advancement of 5G and cloud computing technologies, smart ultrasound enables efficient telemedicine services, extending high-quality medical resources to remote areas and primary healthcare institutions. This is of great significance in alleviating the uneven distribution of medical resources and improving the level of primary healthcare services. Furthermore, smart ultrasound demonstrates broad prospects in the application of big data. It can seamlessly integrate with electronic health record (EHR) systems, providing valuable information resources for epidemiological research and even the long-term management of chronic diseases through continuous monitoring and data analysis. In the field of education and training, smart ultrasound technology also plays a pivotal role. Through simulation and analytical tools, it helps medical students and novice physicians master key skills in ultrasound diagnosis more quickly and effectively, thereby enhancing the professional standards of the healthcare industry.

Overall, intelligent ultrasound technology boasts broad application prospects. With continuous technological innovation and the expansion of application scenarios, intelligent ultrasound is poised to become a significant growth driver in the future healthcare sector. Amidst the overarching trend of comprehensive digital transformation in the medical industry, the application potential of intelligent ultrasound is being rapidly unlocked and translated into tangible commercial market value.

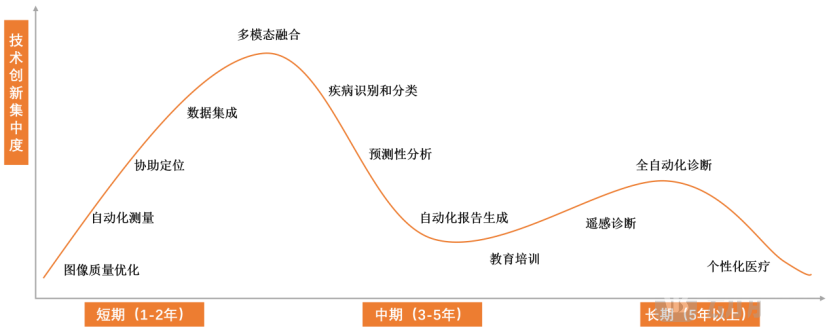

The Evolution Curve of Smart Ultrasound Technology Is Clear and Steep

Panoramic View of Technological Innovation Concentration

Data source: VCBeat

Over the short term of one to two years, technological innovations are expected to focus primarily on optimizing image quality by improving resolution and contrast to enhance diagnostic clarity. Furthermore, automated measurement technologies will leverage algorithms to automatically identify and measure anatomical structures, thereby reducing manual intervention. AI-assisted positioning technologies are poised to help clinicians acquire standard imaging planes more rapidly and accurately, while also providing more comprehensive diagnostic support through the integration of ultrasound data with electronic medical records and other information.

Looking ahead to the technological development prospects over the next 3–5 years, smart ultrasound technology will advance toward more sophisticated applications. This includes the development of advanced algorithms to identify and differentiate disease features in ultrasound images, as well as the use of historical data for predictive analytics to forecast disease progression and treatment outcomes. Furthermore, continuous advancements in artificial intelligence will enable the automatic generation of preliminary diagnostic reports based on imaging and clinical information, and facilitate the integration of ultrasound data with other imaging modalities such as CT and MRI, thereby providing a more comprehensive diagnostic perspective.

In the long term, over a timeframe of more than five years, the development of smart ultrasound technology will achieve fully automated diagnostic workflows, with AI capable of independently handling everything from scanning to report generation. Personalized medicine will also become feasible, offering customized diagnostic and treatment plans by integrating patient data such as genomics and metabolomics. Continuous advancements in remote diagnosis and treatment technologies will enable experts to transcend geographical barriers, extending beyond remote diagnosis to include remote therapeutic interventions, thereby providing patients with professional remote ultrasound diagnostic and therapeutic services. Furthermore, the field of education and training will benefit from smart ultrasound technology, leveraging VR and AR technologies integrated with smart ultrasound to provide physicians with simulation-based training, thereby enhancing their clinical operational skills.

3Boundless Potential, Yet a Long and Arduous Path to Practice

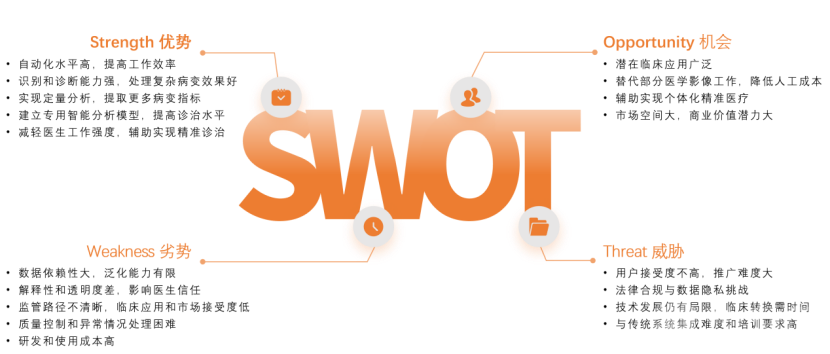

Intelligent ultrasound, as a cutting-edge product that combines traditional medical ultrasound imaging with artificial intelligence deep learning technology, demonstrates significant advantages in automating clinical workflows, image recognition, and quantitative analysis. However, facing multiple challenges such as the regulatory environment and user acceptance, the translation of this technology from the laboratory to the clinic still requires time.

SWOT Analysis of Smart Ultrasound

Data Source: VCBeat

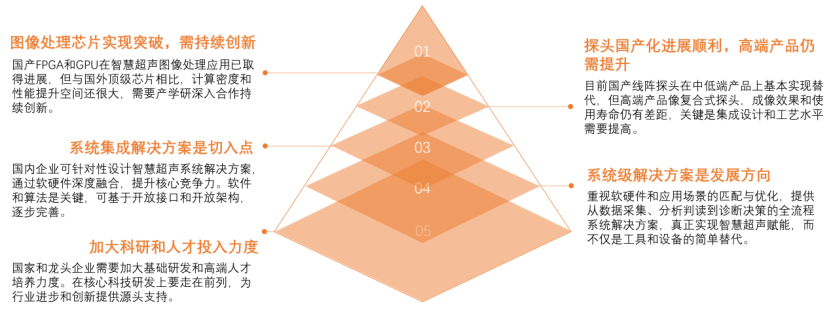

Domestic Ultrasound: Intelligent Hardware Manufacturing as the Path to Breakthrough

Since the core of AI technology lies in software development and the optimization of data algorithms, both of which depend on existing open-source platforms and tools. Furthermore, the rapid iteration and update cycle of software development facilitates continuous optimization and improvement. The application of AI in the field of ultrasound, such as image recognition, automated measurements, and computer-aided diagnosis, is primarily achieved through the training of deep learning and machine learning algorithms. These algorithms process and analyze standardized medical data without requiring complex physical equipment or high material costs. Consequently, AI algorithms can leverage existing data and platforms to enable cost-effective applications in the ultrasound domain.

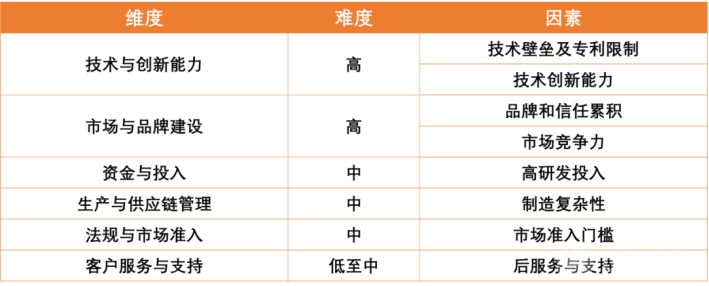

On the other hand, achieving domestic production of ultrasound equipment hardware presents significant challenges, as the research, development, and manufacturing of such hardware span multiple disciplines within precision engineering and materials science. High-quality ultrasound devices require the integration of advanced acoustic principles, precise mechanical design, high-performance electronic components, and mature manufacturing technologies. The manufacturing process demands stringent quality control and high-standard production lines, entailing substantial technical barriers and considerable capital investment.

Furthermore, established manufacturers of traditional ultrasound equipment have built up extensive technological expertise and brand reputation in the market over a long period, making it difficult for new entrants to break through these barriers and compete effectively in the short term. Meanwhile, domestic companies are still in the catch-up phase regarding the manufacturing technology of core components for high-end ultrasound devices, such as transducers. These core components are often subject to foreign patent protections, posing significant challenges for domestically produced hardware to reach international advanced levels. Therefore, compared with the rapid iteration of AI software technologies, it is undoubtedly more challenging for domestically produced ultrasound hardware to gain a foothold in the market.

Analysis of the Challenges in Localizing Smart Ultrasound Hardware in China

Data Source: VCBeat

To achieve the localization of Chinese enterprises in the field of ultrasound hardware, a series of challenges urgently need to be addressed. Among these, the most severe tests stem from technical barriers and patent restrictions. Domestic companies not only need to achieve technological breakthroughs but also navigate around existing patent constraints. This dual challenge of innovation capability and legal strategy places high demands on the comprehensive strength of enterprises. In the medical device industry, especially in the realm of high-end equipment, trust from doctors and medical institutions is typically earned by long-established brands. For emerging domestic companies, building brand image and accumulating trust is a long-term and arduous task.

While the challenges are multidimensional, they are not insurmountable. High R&D investment is the norm in the ultrasound hardware sector, and support from national policies and financing channels provides a strong backing for domestic enterprises. Although difficult, this is by no means a dead end. Meanwhile, market entry barriers and manufacturing complexity require patience and perseverance from domestic ultrasound manufacturers. Regulatory approvals—such as China’s NMPA (formerly CFDA) certification, Europe’s CE marking, and the U.S. FDA clearance—are indeed cumbersome, but they represent predictable and surmountable obstacles. A thorough understanding of and strict adherence to these processes are essential steps for companies entering the market. Furthermore, regarding the complexities of manufacturing processes, China’s existing industrial base and excellent management standards have laid a solid foundation for enterprises to advance in this field.

It is worth noting that domestic enterprises hold a significant home-field advantage in the after-sales service and support sector. By optimizing service processes and enhancing response times, while leveraging their closer geographical and cultural ties with local customers, these companies have full potential to match international brands in terms of service quality.

In addition, technological innovation capability and market competitiveness are indispensable components of brand building. Domestic enterprises can leverage leading research institutions both at home and abroad to attract and cultivate top-tier talent, thereby fostering an innovation culture with distinct characteristics. On the other hand, by leveraging their in-depth understanding of the local ultrasound market, they can provide cost-effective and personalized products to enhance their market competitiveness. As external conditions for corporate development, the policy and regulatory environment can help mitigate risks and uncertainties to some extent if companies respond flexibly under the guidance of national policies, thereby facilitating business growth.

Although smart ultrasound faces numerous challenges, targeted breakthroughs in single dimensions and coordinated development across comprehensive dimensions will be the key path for domestic ultrasound hardware manufacturers to ultimately achieve localization.

As a rising star in the field of medical imaging diagnostics, smart ultrasound is rapidly emerging and reshaping this multi-billion-dollar market. Guided by three core values, smart ultrasound will achieve three major leaps: from “visual” to “intelligent” through algorithm empowerment, from “product” to “service” via differentiated solutions, and from “diagnosis and treatment” to “research” by leveraging large-scale medical big data. This will accelerate the replacement of imported equipment with domestically produced alternatives, usher in new business models for the industry, and drive clinical healthcare to new heights in work efficiency and treatment quality. It is foreseeable that smart ultrasound will quickly integrate into mainstream medical institutions both domestically and internationally, becoming a new engine for optimizing and upgrading the healthcare industry.

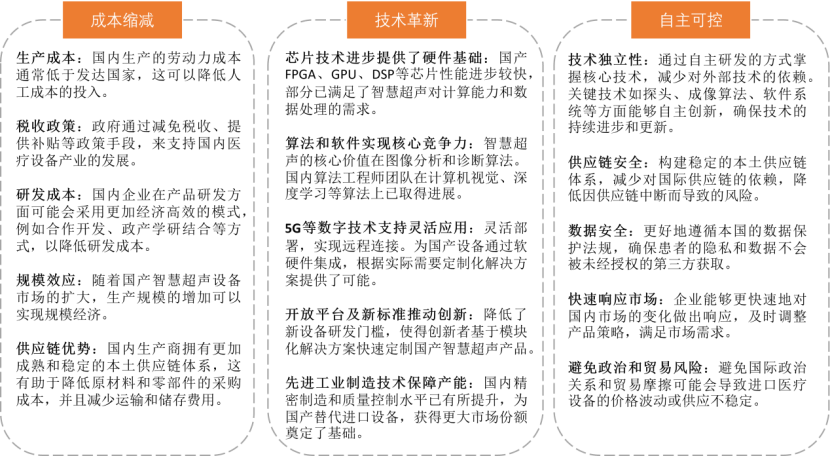

1Domestic Equipment and Consumables Are Gradually Achieving Substitution

As the performance of domestically produced equipment continues to improve and their price advantages become more apparent, they are expected to gradually replace imported equipment and expand their market share. Meanwhile, domestic probes, consumables, and other products are also accelerating their iteration and upgrades, achieving import substitution, reducing procurement and usage costs for hospitals, and providing strong support for the development of the healthcare industry.

Drivers for the Domestic Substitution of Smart Ultrasound in China

Data Source: VCBeat

Software Intelligence, Hardware Integration, and Industry-Academia-Research Collaboration: Three Technological Engines Drive the Localization of Smart Ultrasound

Empowerment by software and artificial intelligence, improvement of hardware and information infrastructure, and acceleration of industry-academia-research collaboration constitute the three major drivers advancing smart ultrasound. These elements not only enhance diagnostic accuracy and operational efficiency but also lay the foundation for future intelligent and personalized healthcare services. To foster substantial development and innovative breakthroughs in the field of smart ultrasound, it is essential to define clear roadmaps for core technology development, innovate market and business models, and establish a robust industrial ecosystem.

Key Pathways for the Domestic Substitution of Smart Ultrasound in China

Source: VCBeat

Software and AI empowerment are key to driving the development of smart ultrasound.Smart ultrasound, as an emerging medical imaging diagnostic technology, derives its core value from the intelligent analysis and diagnosis of ultrasound images through software algorithms. Currently, smart ultrasound software equipped with deep learning and other AI technologies can already achieve automatic identification and quantitative analysis of lesions in multiple areas, including the heart and blood vessels. In the future, smart ultrasound software needs to continue expanding the range of covered diseases and leverage the growing clinical imaging datasets to train lesion detection and diagnostic models with superior performance. Meanwhile, providing open software platforms and interfaces to attract more algorithm and application developers will further enrich the functionalities of smart ultrasound.

Advance hardware and information technology infrastructure to build an intelligent diagnostic system.Another core value of smart ultrasound lies in providing more efficient healthcare solutions through the deep integration of upstream and downstream segments of the industrial chain with clinical diagnosis and treatment scenarios. This requires full consideration of subsequent data acquisition, transmission, storage, analysis, and application during the design and development of smart ultrasound devices. For instance, the research and development of new ultrasound imaging probes can be combined with digital network technologies such as 5G, enabling real-time data processing and cloud transmission at the probe end. On the server side, big data and AI technologies can be leveraged to provide personalized health management covering the entire lifecycle. Meanwhile, the terminal end must offer concise and user-friendly interfaces for both physicians and patients. Establishing an integrated “device-cloud-terminal” smart healthcare solution will significantly enhance the performance of traditional ultrasound in terms of detection accuracy, work efficiency, and other key metrics. This is the inevitable path for smart ultrasound to achieve new breakthroughs and unlock greater potential.

Deepen Industry-Academia-Research Collaboration to Accelerate Innovation in Smart Ultrasound Technology and Industry.Currently, smart ultrasound technology is in a stage of rapid development. The pathways for realizing core technologies remain to be explored, while market size and business models continue to evolve through innovation. These highly uncertain aspects require deep integration and collaborative participation among industry, academia, and research institutions to achieve breakthroughs and sustain optimization. Specifically, investment from industrial capital can accelerate commercialization and facilitate user feedback; basic research conducted by universities and scientific research institutions can advance core technologies, such as new materials and algorithms; and government agencies need to provide regulatory and policy support. Collaborative efforts among industry, academia, and research entities to create an ecosystem that drives the rapid iteration of smart ultrasound technology and its associated industries are essential prerequisites for achieving swift industrial growth.

2Differentiated Development Pathways Unlock International Growth Opportunities for Smart Ultrasound

Amid the tide of globalization, the importance of differentiated, customized solutions has become increasingly prominent, particularly for multinational corporations and healthcare institutions with international operations. Business entities of these organizations in different countries face disparities in technological capabilities and staffing configurations. Adapting to local market demands by providing differentiated and customized smart ultrasound solutions has thus become the key to unlocking high-end overseas markets.

The attitude of countries in Europe and North America toward ultrasound technology can be summarized as “open” and “innovative.” They actively embrace emerging technologies, demonstrating strong enthusiasm for the research, development, and application of ultrasound. In the healthcare sector, they place significant emphasis on ultrasound technology, continuously exploring its applications in clinical diagnosis and treatment. Meanwhile, due to their relatively high economic levels, demand for ultrasound equipment is also comparatively high. When purchasing ultrasound systems, they prioritize device performance and functionality, showing relatively low price sensitivity.

In contrast, consumers in Southeast Asia place greater emphasis on the cost-effectiveness of ultrasound equipment. They tend to purchase relatively low-priced yet high-performance ultrasound systems to align with the region’s economic conditions. This consumption pattern is linked to the level of economic development in Southeast Asia and also reflects differing demands for and perceptions of ultrasound technology.

To make corresponding adjustments in ultrasound product design and services, enterprises must not only gain a deep understanding of the unique characteristics of local markets but also drive innovation in their products and services. The development stages and application scenarios of medical ultrasound vary across different regions; therefore, companies need to formulate tailored product design and service strategies that address the specific needs and pain points of diverse international markets. By collaborating closely with local physicians to assess clinical needs and technical capabilities, and by deeply understanding regional market nuances, enterprises can adjust their product designs and service offerings accordingly. This approach ensures the adaptability and effectiveness of their solutions, ultimately securing market share and earning customer recognition.

3Business Model Transitioning to Integrated Solutions

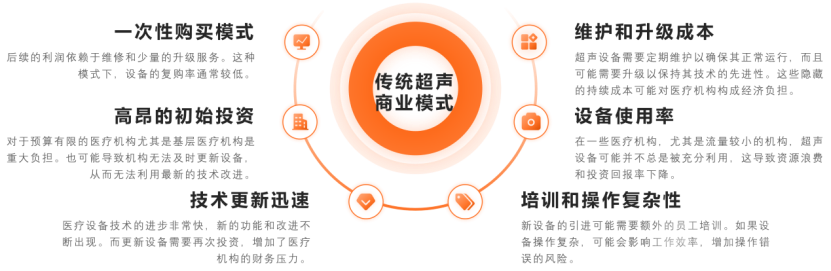

Given the long service life of ultrasound equipment, natural repurchase rates are relatively low. Meanwhile, healthcare institutions, particularly primary care facilities with limited budgets, face high initial acquisition costs. This financial burden may hinder their ability to acquire the latest technologies or upgrade existing equipment, thereby compromising the quality and efficiency of patient diagnosis and treatment. In an era of rapid technological advancement, ultrasound systems purchased through one-time transactions can quickly become obsolete, necessitating replacement or upgrades within a short timeframe and imposing continuous investment pressure on healthcare institutions. Furthermore, operational maintenance costs—including preventive maintenance and emergency repairs—cannot be overlooked; these hidden, ongoing expenses may account for a significant proportion of a healthcare institution’s annual budget.

In addition to economic factors, operating ultrasound equipment requires specialized skills, and the introduction of next-generation devices entails the need for staff training. If new equipment is complex to operate, it may compromise diagnostic efficiency and increase the risk of operational errors, thereby posing additional challenges to clinical workflows. Therefore, training on new equipment and continuous skill enhancement are critical components in ensuring the quality of medical services, which undoubtedly increases the human resource investment required by healthcare institutions.

To address these challenges, some ultrasound equipment manufacturers are considering a shift in their business models. Furthermore, at the national level in China, the leasing of ultrasound equipment has been actively encouraged. In October 2023, the General Office of the People’s Government of Guangdong Province officially issued the “Notice on the Work Plan for Implementing Pilot Programs for Equipment Leasing in Education, Science and Technology, Health, and Other Sectors in Our Province,” in accordance with the decision-making and deployment of the Provincial Government. This plan aims to tackle challenges such as low efficiency in the use of fiscal funds and uneven regional resource allocation, particularly addressing the difficulty faced by some regions with limited financial capacity in acquiring advanced equipment. The pilot programs will initially be launched in public schools, research institutions, and healthcare facilities across the province, while encouraging other specific sectors to refer to the provincial pilot scheme and actively advance equipment leasing initiatives within their respective fields.

Drawbacks of the Traditional Ultrasound Business Model

Data Source: VCBeat

Deliver differentiated and customized holistic solutions, build an ecosystem, and expand value space

Smart ultrasound services cater to a highly diverse clientele, ranging from primary community hospitals to top-tier (Grade 3A) medical centers. Users exhibit varying requirements for system performance and usage scenarios, primarily manifested in cost-effectiveness, operational ease, functional needs, remote support, device performance, customized services, system integration capabilities, data analytics proficiency, stability, and after-sales service.

The ecosystem involves the symbiotic and co-prosperous relationship among multiple stakeholders across the upstream, midstream, and downstream sectors. As a core player, ultrasound enterprises must proactively build such an ecosystem. Ultimately, this enables all parties—including patients, physicians, hospitals, and software/hardware developers—to derive added value from the ecosystem chain, achieving mutual win-win outcomes. By providing differentiated solutions that address the specific needs of medical institutions at various levels, and through flexible software/hardware platforms and standardized interface designs that facilitate future upgrades and personalized customization, companies can solidify their customer base.

Strengthen service-oriented business and establish a new business model of "equipment + software + services"

Currently, ultrasound relies on one-time sales of hardware equipment, making it difficult to achieve sustained profitability through hardware sales alone. The development of smart ultrasound technology is increasingly service-oriented, requiring integration of hardware devices, software platforms, and service support. Therefore, transforming the business model by adopting a new “hardware + software + services” approach is a critical pathway for smart ultrasound companies to achieve sustainable profitability.

Smart ultrasound equipment suppliers should not limit themselves to selling hardware but should also provide comprehensive solutions, including value-added services such as equipment maintenance, software upgrades, education and training, and data management. By integrating with other medical information systems, they can offer better data sharing and analysis. Continuing to provide software platform services and technical support after the sale of hardware enables full lifecycle customer management. This model of generating ongoing service revenue can enhance customer stickiness and repurchase rates.

Patient-Centricity: Uncovering Latent Needs to Proactively Drive Growth

As the highest-tier hospitals in China’s healthcare system, Grade 3A hospitals impose stringent requirements not only on medical service capabilities, research and education standards, and expert teams, but also place significant emphasis on medical equipment with research-support functions. As key bases for medical research, these institutions are particularly drawn to devices that offer statistical analysis and data support. Companies can focus on the clinical needs of Grade 3A hospitals, engage in in-depth technical exchanges and project design, and provide targeted solutions. After meeting market validation standards, they can conduct business demonstrations and replicate their models, thereby rapidly expanding their market share.

Amidst the global surge in high-end medical device development, Carbon Medical has gained deep insights into the clinical needs of frontline physicians in China. Following the launch of its first-generation product, or prototype, the company enabled physicians to gain hands-on experience and continuously optimized functionality and user experience based on their professional recommendations. Since the product’s market debut, Carbon Medical has maintained a rigorous academic approach, learning through clinical collaborations with leading tertiary hospitals in China that serve as teaching and demonstration centers, while vigorously promoting the decentralization and broader adoption of its technologies. This persistent commitment to research and innovation has allowed Carbon Medical to gradually secure a foothold in the urology market.

Enterprises should prioritize patient and clinical needs, establishing scientific research collaborations with tertiary Grade A hospitals. By leveraging these hospitals’ substantial patient volumes and capacity to reach patients, companies can jointly conduct research projects to enhance the scientific value and market competitiveness of smart ultrasound technologies. Providing customized solutions and services—such as professional training, technical support, and software upgrades—can improve equipment utilization and user satisfaction. With a deep understanding of the nuanced needs of tertiary Grade A hospitals and continuous innovation, smart ultrasound enterprises can identify new growth points and competitive advantages within the traditional ultrasound market, thereby achieving significant value creation.

4Enhancing Diagnostic and Therapeutic Efficiency to Facilitate Multi-Disease Research

Rapid detection and diagnosis are fundamental requirements in the medical field. However, traditional ultrasound equipment and medical imaging analysis remain constrained by limitations in manpower, capital investment, and technical maintenance, creating significant barriers to clinical diagnosis and treatment. In contrast, automated and highly precise smart ultrasound technology not only delivers rapid and accurate diagnostic results but also enables in-depth extraction of disease-related information. By developing specialized intelligent analysis models tailored to specific anatomical regions and disease types, this technology enhances the overall standard of diagnosis and treatment.

Rapid and Precise Image Analysis and Diagnosis.By leveraging cutting-edge algorithms such as deep learning, organ contours can be accurately detected, lesion types identified, and severity assessed from ultrasound images within seconds, while generating structured reports containing quantitative metrics such as size and density. This not only improves the efficiency of individual case examinations but also frees up more time for physicians to conduct extensive and in-depth research.

Continuous Evolution and Model Optimization.Dynamically incorporating feedback from each new case, the system continuously adjusts and optimizes its detection and diagnostic models to deliver more accurate and reliable results. This capability for continuous upgrades will significantly reduce physicians’ workload and provide long-term, robust support for their in-depth research.

Conduct large-sample, multicenter collaborative studies.The vast volume of clinical case data from hospitals migrating to the cloud has made it possible to conduct larger-scale clinical studies with a more comprehensive range of disease types. Physicians can query and correlate this data through intelligent platforms, enabling systematic and comprehensive multi-disease and multi-factor association studies, which hold the promise of yielding pioneering research outcomes.

Deepening the Understanding of Etiology and Optimizing Treatment Regimens.Rich structured case data and in-depth multi-disease research will significantly advance the understanding of the etiology of complex diseases and the design of treatment protocols. This, in turn, will enhance the detection efficacy of intelligent ultrasound systems and improve physicians’ diagnostic capabilities, thereby establishing a virtuous cycle between research and application.

Promote the integration of clinical and basic research. Leveraging the big data and research platforms established by the Smart Ultrasound Cloud Platform can accelerate the translation of basic scientific achievements into clinical applications. For instance, using deep learning to discover new biomarkers in medical images exemplifies how such deep industry-academia-research collaboration will continue to provide fresh insights for healthcare.

As intelligent ultrasound systems continue to evolve and data sharing among major medical institutions expands, large-scale multi-center collaborative research will become more accessible and in-depth. This will effectively push the boundaries of medical research and strengthen the interaction between basic science and clinical practice.

The above is an excerpt from the report. The overall framework of the report is as follows:

Chapter 1 Industry Background: Precise Technological Evolution and Multidimensional Expansion of Application Capabilities

1.1 Fundamental Concepts: The Synergy of Ultrasound in Diagnosis and Therapy

1.2 Development History: The Transformation of Medical Ultrasound Toward Precision and Intelligence

Chapter 2 Market Analysis: Steady Expansion in Scale, Accelerated Rise of Domestic Enterprises

2.1 Market Size: Quantitative Change Drives Qualitative Transformation, Unlocking New Opportunities Through Scale Effects

2.2 Industry Chain: Forging the Foundation, Painting a New Picture of the Industrial Ecosystem

2.2.1 Ultrasound Diagnostic Equipment: Remarkable Progress in Domestic Substitution for Mid- to Low-End Products

2.2.2 Ultrasound Therapy Devices: Slow Progress in Domestic Substitution in the High-End Segment

2.2.3 Demand for Ultrasound Equipment: Diversified User Market and Urgent Need to Expand Specialized Applications

2.3 Drivers: Resonance of Multiple Forces, with Industry Momentum Growing Stronger

2.3.1 Demographic Shifts Unlock Industry Potential

2.3.2 Continued Realization of Policy Dividends for Medical Devices

2.3.3 Significant Growth in Export Demand for Low- to Mid-End Medical Devices

2.3.4 Capital Boosts Local Competitiveness

Chapter 3 Application Innovation: Intelligent Upgrading of Ultrasound, Smart Leadership in Medical Transformation

3.1 Multi-Technology Empowerment: Decoding the Cornerstones of Smart Ultrasound Technology

3.2 Limitless Application Expansion: Uncovering Opportunities in Innovative Fields

3.3 Diverse Scenario Integration, Fruitful Achievements in Smart Ultrasound

3.4 Boundless Potential, Yet a Long and Arduous Path Ahead

Chapter 4 Future Trends: Reshaping the Ultrasound Landscape and Launching Three Strategic Initiatives

4.1 From Traditional Ultrasound to Smart Ultrasound: Domestic Equipment and Consumables Are Gradually Achieving Substitution

4.2 Smart Ultrasound Sparks a New Wave of Commercialization, with Business Models Transitioning Toward Integrated Solutions

4.3 Smart Ultrasound Enhances Diagnostic and Therapeutic Efficiency, Supporting Research on Multiple Diseases

Chapter 5 Corporate Case Studies

5.1 Carbon Medical

5.2 Hebin Intelligence

5.3 XinHuan Technology

Please scan the QR code to add our assistant and obtain the full report. If you have already added the assistant, please initiate a conversation to request it.

Special Acknowledgements (Listed in Order of Research Interviews):

Mr. Zhang Shiping, Chairman of Carbon Medical; Dr. Cheng Dongliang, Co-founder of Hebin Intelligence; Dr. Huang Qi, Co-founder of Hebin Intelligence; and Dr. Zhou Xinhuan, Founder of XinHuan Technology