2023 Medical Devices and Supply Chain White Paper: Over 400 Financing Deals, with Consumer MedTech and Multiple Innovation Segments Showing Resilience Amid Market Headwinds!

2023 was a year of sustained volatility. Global medtech IPOs faced challenges, yet the medical technology industry underwent reshaping under pressure. To cope with the capital winter and tighter IPO scrutiny, domestic innovative medical device companies placed greater emphasis on commercialization. 2023 was also a year when the industry separated the genuine from the spurious. As consensus-driven, certain opportunities dwindled and capital tightened, investors ceased chasing hot trends and instead delved deeper to identify blue-ocean opportunities in niche segments.

Despite the challenges, the medical device market in 2023 still had its highlights. Domestic innovative medical device companies accelerated commercialization, with 56 innovative medical device products approved for market entry, and going global became a key focus; centralized procurement price reductions became more moderate, promoting adjustments in the structure of domestic medical device products; policies on large-scale medical equipment configuration were implemented, relaxing configuration standards and increasing market capacity; breakthroughs in multiple key technologies upstream of the medical device industry pushed domestic substitution into deeper waters; consumer healthcare emerged as an innovation hotspot, with medical technology exploring greater opportunities; material technological innovations became crucial; industrial investors increased funding to empower medical technology innovation; multinational medical device companies intensified their localization efforts. In the long run, domestic enterprises face significant opportunities in prolonged competition. For Chinese-made medical devices, speed is king in the short term, while product strength, platform iteration capabilities, and cost control will determine the future in the long term.

This white paper examines innovation in specific segments of the medical device industry in 2023, drawing on typical innovative initiatives and their outcomes since 2023. It highlights the top 20 innovation cases and provides detailed analyses of the innovation pathways and value of selected cases, aiming to offer reference insights for the industry.

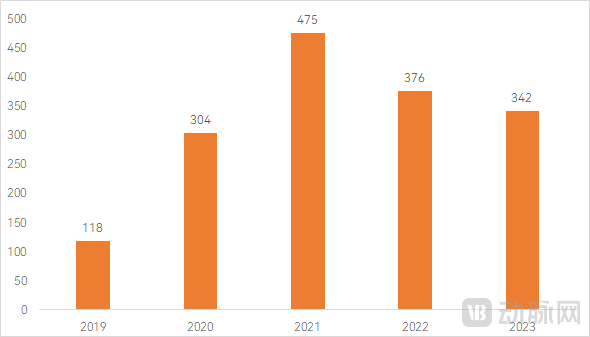

Decline in the Number of Financing and Investment Events for Innovative Medical Devices in 2023As of November 30, 2023, there were 447 financing events in China’s medical device sector, including 104 in the in vitro diagnostics (IVD) field, representing a decline from the 591 financing events recorded in 2022. This downturn in medical device investment and financing aligns with global trends in the healthcare industry. The global healthcare investment sector is currently undergoing its fifth period of volatility, which historically lasts two to three years. Despite the global capital winter, China’s medical device industry still secured over 400 financing deals, underscoring the sector’s resilience. Although there is limited room for valuation growth, leading companies continue to attract funding.

Medical device companies demonstrate stronger resilience.The characteristics of the medical device industry dictate that, compared to biotech companies, medical device firms require smaller capital investments, have shorter R&D cycles, and achieve product commercialization more easily. Coupled with the prevalent multi-pipeline strategy adopted by most companies, innovative medical devices generally demonstrate stronger risk resistance and greater resilience during economic downturns. This implies that enterprises capable of accelerating commercialization and generating positive cash flows possess stronger resilience in down cycles.

The “winter” of the medical device investment and financing market in 2023 was influenced by a combination of multiple factors.From a global perspective, a series of uncertain events have led to a risk-averse contraction in the supply of global capital. In China, the market dividends driven by structural changes in the secondary market for medical innovation investment and financing are gradually diminishing, and the domestic medical device financing sector is entering a new cycle. On the industry front, spurred by supportive policies, innovative forces in China’s medical device sector are surging, with multiple products achieving import substitution. As the rate of domestic substitution rises, cultivating new innovative entities will require time and a certain development cycle.

Number of Private Equity Deals in Innovative Medical Devices from 2019 to November 30, 2023 (Unit: Cases), Excluding In Vitro Diagnostic Events

Diverse Hot Sectors: Capital Unearths Niche “Blue Ocean” Opportunities.Investment in 2023 was distributed across a more diverse range of sectors. In 2022, the top three sectors by funding amount accounted for 34% of the total annual funding; in 2023, the top three sectors represented 24% of the total number of financing deals. Unlike previous years, when medical device investment was primarily concentrated in cardiovascular diseases, surgical robotics, and imaging, 2023 saw the emergence of numerous innovative sectors, such as regenerative materials, microspheres, upstream raw materials, and spatial omics. Investment in the medical device sector in 2023 shifted away from pursuing consensus-driven opportunities with high certainty, focusing instead on deeply cultivating opportunities arising from industrial and technological transformations.

Niche Blue-Ocean Segments Within Popular Major Tracks Are Gaining Attention.Even in popular sectors, the subfields that secured funding in 2023 became more diversified. In the cardiovascular field, financing themes in 2022 included electrophysiology and ventricular assist devices. In 2023, investment focused on intracardiac echocardiography (ICE), tissue-engineered blood vessels, polymer heart valves, and shockwave balloons. The surgical robotics sector also saw the emergence of new subfields in 2023, such as microsurgical robots and modular laparoscopic surgical robots.

Top 12 Distribution of Innovative Medical Device Financing Events in 2022 & 2023

Top 12 Subsector Financing Events in the In Vitro Diagnostics (IVD) Field in 2022 & 2023

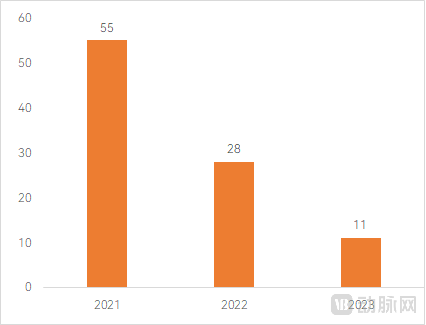

IPO Slowdown Leads to Capital Piling Up in Late-Stage ProjectsThe number of IPOs has shrunk significantly worldwide. In the global market, innovative medical device IPOs are facing headwinds, and health tech IPOs are experiencing their worst year in recent years. In China, the number of IPOs and the amount of funds raised by big health companies in both domestic and overseas capital markets are showing a downward trend. As of November 1, 2023, 11 companies in China have successfully gone public.

Changes in the Number of IPOs in the Medical Device Sector from 2021 to 2023

IPO Outlook: The BSE’s Quality Improvement and Expansion Hold Promising Prospects

It is anticipated that the landscape of healthcare IPOs in 2024 will continue to be influenced by the broader A-share IPO environment. Furthermore, given the impact of industry policies—such as centralized volume-based procurement and anti-corruption campaigns in the healthcare sector—on for-profit enterprises, coupled with tighter regulations on listings of non-profit entities, the number of healthcare IPOs on the Main Board, STAR Market, and ChiNext in 2024 is likely to decline compared to previous years. Nevertheless, market opportunities will still exist.

The Beijing Stock Exchange Has Become the Main Arena for Innovative SMEs.The Beijing Stock Exchange (BSE) has emerged as a new option for a large number of innovative small and medium-sized enterprises (SMEs). In 2023, the BSE intensified its reform efforts to optimize listing arrangements by refining the implementation standards for the “12-month listing requirement” and allowing qualified high-quality SMEs to conduct initial public offerings (IPOs) and list on the BSE, thereby further facilitating diversified and convenient access to public markets. Currently, under the guidance of the China Securities Regulatory Commission (CSRC), the BSE is accelerating the development of rules and regulations for direct IPOs on the exchange, with more opportunities expected in 2024.

Medical Device Companies Listed on the Beijing Stock Exchange in 2023

Catch-up innovation overseas is nearing its end, while original innovation is on the rise.

Trends in the Review and Approval of Innovative Medical Devices Reflect the Competitive Landscape of Domestic Innovative Medical Devices. At this stage, compared with the global landscape, most domestic innovative medical devices in China are still characterized by catch-up innovation. These products fill gaps in domestically produced offerings and better meet clinical needs through innovative design. As catch-up innovation gradually reaches saturation, innovation in China’s medical device industry will progressively shift toward original innovation.

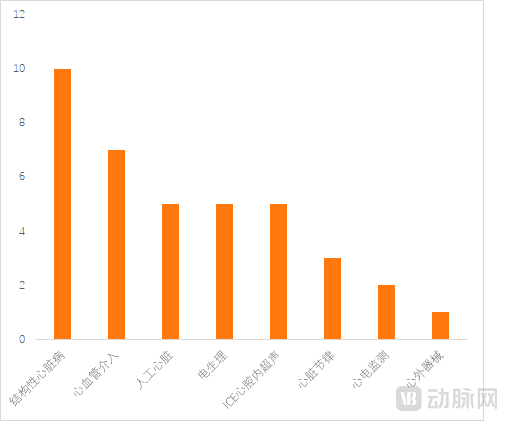

2023 Distribution of the Industrial Landscape for Innovative Medical Devices Entering the Approval List in China

Supportive policies are being continuously introduced, driving the expansion of the medical device industry.

Robust policy support has created a favorable industrial policy environment for the upgrading and development of the medical device industry. In 2022, fiscal interest-subsidized loans for the renewal and upgrading of medical equipment unleashed market demand worth hundreds of billions of yuan. Significant industrial policies were also introduced in 2023.

Relaxation of Approval and Licensing for Large-Scale Medical Equipment. On March 21, 2023, the National Health Commission released the Catalogue for the Administration of Configuration Licenses for Large-Scale Medical Equipment (2023 Edition). Compared with the 2018 catalogue, the number of items under management was reduced from 10 to 6, with Class A items decreasing from 4 to 2 and Class B items from 6 to 4. Notably, Positron Emission Tomography/Magnetic Resonance Imaging systems (PET/MR) were reclassified from Class A to Class B, while X-ray computed tomography scanners with 64 slices or more and magnetic resonance imaging systems of 1.5T or above were removed from the managed items altogether. This revised catalogue further relaxes approval and licensing requirements for large-scale medical equipment, sending a positive signal. The deregulation of procurement for such equipment grants hospitals greater flexibility and promotes the domestic substitution of innovative medical devices and equipment in China.

Changes in the Number of Configuration Permits: Class A: Heavy Ion Radiotherapy Systems (41 new units added, with a planned total of 60 units); High-End Radiotherapy Equipment (76 new units added, with a planned total of 125 units). Class B: PET/CT (860 new units added, with a planned total of 1,667 units; an increase of 377 units under the “13th Five-Year Plan” and an additional 483 units); Laparoscopic Surgical Systems (559 new units added, with a planned total of 819 units; an increase of 154 units under the “13th Five-Year Plan” and an additional 405 units); PET/MR (141 new units added, with a planned total of 210 units; 28 units under the “13th Five-Year Plan” and an additional 113 units). Overall, the planned number of large-scale medical equipment configurations in 2023 exceeded expectations, benefiting domestic medical imaging and surgical robotics companies.

The cardiovascular field, characterized by substantial unmet clinical needs and well-established market education, has long been a focal point for medical technology innovation. As the first therapeutic area to implement centralized volume-based procurement (VBP), the sector has seen industry bubbles squeezed out, fostering a process of elimination that steers development toward a virtuous cycle driven by innovative products. As of November 2023, there were 38 financing events in the cardiovascular sector. In terms of sub-segment distribution, products such as intracardiac echocardiography (ICE) systems, ventricular assist devices (VADs/artificial hearts), polymer heart valves, shockwave balloons, atrial shunts, and bioresorbable stents have attracted the most attention. Although the number of financing deals declined compared to 2022, the depth of innovation has increased, with milestone breakthroughs achieved across multiple sub-segments.

2023 Financing Landscape in Cardiovascular Subspecialties

The Widespread Application of Novel Valve Materials Is Poised to Bring Revolutionary Changes to the TAVR Field。Polymer Valve Technology Has Extremely High Barriers, the primary challenge in research and development lies in material selection. Valve materials must meet multifaceted performance requirements, including fatigue resistance, hemodynamic efficiency, and biocompatibility. For instance, while thickening the valve is a straightforward design approach to enhance fatigue resistance, excessive thickness can impede proper valve opening; balancing these two competing properties presents a significant challenge. Furthermore, as polymer materials are synthetic, impurities arising from chemical synthesis are unavoidable, making the reduction of biological toxicity another major hurdle. Polymer valves also impose distinct requirements on manufacturing processes. Due to high technical barriers, only a few companies worldwide have mastered the core technologies for polymer valve materials.

Domestic Transcatheter Mitral Valve Interventions Enter a Harvest Period: China’s First Transfemoral Mitral Valve Clip System Receives Market ApprovalThere are more than 20 products in the pipeline for transcatheter edge-to-edge repair (TEER) of the mitral valve in China, making this sector highly competitive. However, companies capable of rapidly completing clinical trials and regulatory registration through exceptional execution and robust technology remain scarce. In 2023, China’s mitral valve industry achieved a major breakthrough: the first domestically developed transfemoral TEER product was approved for market launch. Dejin Medical’s DragonFly™ Transcatheter Mitral Valve Clip System (hereinafter referred to as “DragonFly™”) officially received approval from the National Medical Products Administration (NMPA). Results from the DragonFly-DMR trial demonstrated that the DragonFly™ system offers favorable safety, efficacy, and maneuverability for treating degenerative mitral regurgitation (DMR), providing a better therapeutic option for patients with DMR who are at high surgical risk. The DragonFly™ product features four innovative designs, ensuring safe and controllable clipping, precise and straightforward overall operation, broad anatomical adaptability, and accurate and definitive therapeutic outcomes.

Amid the surge in electrophysiology and structural heart interventions, intracardiac echocardiography remains hot despite the industry winter.ICE financing remained hot in 2023, with five ICE companies securing funding, keeping the number of financing events on par with 2022. Leveraging its clinical advantages, such as high-resolution visualization of cardiac structures and blood flow information, intracardiac echocardiography (ICE) is increasingly being applied in various electrophysiology and structural heart intervention procedures. The clinical application of ICE in 2023 was driven by multiple favorable factors. In terms of reimbursement, intracardiac ultrasound was included in the national medical insurance coverage. Meanwhile, in April 2023, electrophysiology products were included in centralized volume-based procurement across 27 provinces, leading to an increase in the volume of electrophysiology procedures. It is estimated that domestic electrophysiology procedures in China grew by approximately 30%-40% in 2023, correspondingly driving explosive growth in ICE utilization.

Enhanced Treatment Capabilities at Local Hospitals: Innovative Surgical Instruments Reduce Procedural Difficulty and Improve Safety.In contrast to the rapid iteration of innovative products and rising procedural adoption rates in cardiology, cardiac surgery remains synonymous with high difficulty and significant challenges. In recent years, influenced by the pandemic and centralized volume-based procurement, cardiac surgery has accelerated its development, shifting onto a trajectory of robust growth. The most evident manifestation is the surge in surgical volumes: coronary artery bypass grafting (CABG) procedures increased by over 30%, while aortic surgeries exhibited exponential growth. This rapid expansion has been driven by enhanced cardiac surgical care capabilities at local hospitals. Currently, there is an increasingly pronounced trend toward more critically ill patients and greater procedural complexity in cardiac surgery. There is an urgent clinical need for innovative devices that better address pain points during surgeries. Domestic companies are beginning to break through this high technical barrier. In this field, Yuwei Medical, a Chinese innovator, completed two rounds of financing in 2023, with its differentiated innovations gaining recognition from multiple prestigious institutions. Yuwei Medical focuses on the research and development of devices for cardiac surgery and heart failure. Guided by two core principles, the company develops innovative products: leveraging innovative technologies to improve treatment outcomes for critically ill and complex cases from the patient’s perspective, and reducing the learning curve for surgeons while enhancing diagnostic and therapeutic efficiency from the physician’s perspective. Currently, Yuwei Medical’s next-generation cardiac stabilizers, femoral arterial and venous cannulas, and intelligent coronary angiography scoring systems are poised to obtain regulatory approval and enter commercialization, while its pulsatile left ventricular assist system has completed design finalization.

Ophthalmology has become a widely recognized golden track.Over the past three years, the number of financing events in the ophthalmology sector has remained at a high level, with 29 deals recorded in 2021 and 25 in 2022. According to the Arterial Orange database, there were 18 financing events in the ophthalmology sector as of November 30, 2023. Although this figure represents a decline compared to the previous two years, the ophthalmology sector ranked third in terms of total transaction volume across all sectors. Product categories such as intraocular lenses (IOLs), optometry and vision care, minimally invasive glaucoma surgery (MIGS), ophthalmic equipment, and ophthalmic surgical robots have attracted significant attention.

High Import Share + Consumer Attributes Drive the Value of Ophthalmic Devices.Regarding the reasons behind the booming ophthalmology sector, Yan Yi, Managing Director of Shuimu Ventures, stated: Ophthalmology is hailed as the “Golden Eye.” Historically, imported brands have dominated the ophthalmic device market, with import penetration for high-end ophthalmic devices reaching as high as 90%, leaving substantial room for domestic substitution. Second, the manufacturing of ophthalmic devices involves advanced precision engineering, resulting in high industry entry barriers. Ophthalmic medical equipment and high-value medical consumables demand a high degree of precision in optical processing, electromechanical manufacturing, and material synthesis. Consequently, the global market share is currently concentrated among a few large international medical device manufacturers, leading to relatively low competition; many ophthalmic device categories have not yet reached a “red ocean” state of intense rivalry. Third, the optometry and vision care sector possesses strong consumer attributes, making it more resilient to policy uncertainty risks under the backdrop of centralized procurement.

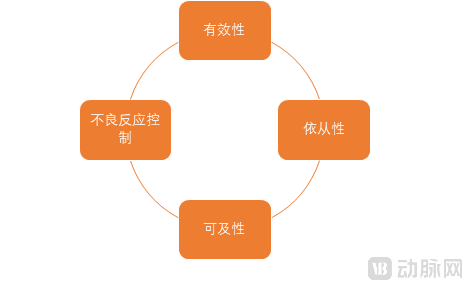

The myopia control market is vast, with various myopia control products coexisting in a complementary manner.Given the large population of myopia patients in China and the strong demand for myopia control, current supply remains insufficient to meet market needs. Yan Yi, Managing Director at Shuimu Ventures, stated that the key to capturing a larger market share for various myopia control products lies in mastering product competitiveness. The four dimensions for evaluating the competitiveness of myopia control products include: efficacy, compliance, affordability, and adverse reaction control. Taking orthokeratology (OK) lenses as an example, they demonstrate outstanding performance in terms of efficacy but fall short compared with defocus spectacle lenses in affordability and compliance. Currently, existing products on the market all have certain shortcomings; therefore, the future landscape of the myopia control market is expected to trend toward the coexistence of multiple product types. Meanwhile, the development of new, consistently effective myopia control products remains a key focus of industry attention.

Domestic substitution in the ophthalmic equipment sector faces significant challenges, requiring Chinese enterprises to break through on multiple fronts.. Yan Yi, Managing Director of Shuimu Ventures, stated thatFirst, strengthen foundational R&D capabilities and product capabilities.。Domestic enterprises need a flagship product to make a market entry and prove their capabilities when first entering the market; only by achieving parity with or even surpassing imported products in a specific offering can they gain a certain level of market presence.Second, it is necessary to develop a multi-pipeline strategy.In the mid-to-high-end ophthalmic equipment sector, platform-based enterprises hold a distinct advantage; the market capacity for individual products is limited, and their market share is easily surpassed by platform-based competitors. Domestic innovative companies need to adopt a multi-pipeline strategy and possess comprehensive R&D capabilities to compete effectively with multinational corporations (MNCs).Third, leverage localization advantages.Domestic substitution is not achieved overnight; Chinese innovative enterprises need to gradually penetrate the market by fully leveraging their localization advantages. Localization capabilities are reflected in a deep understanding of policies and clinical practices, as well as efficient service response. For instance, while the volume-based procurement (VBP) policy has had a significant impact, it has also created new opportunities for domestic companies, which can capitalize on these policy shifts to increase their market share.Fourth, establish your own clinical, marketing, and sales systems.Domestic innovative enterprises cannot simply replicate the playbook of multinational corporations (MNCs); instead, they must consolidate their own channel resources by cultivating a distributor network or building an in-house sales team.Fifth, adhere to a long-term strategy and avoid engaging in price wars with multinational corporations (MNCs).Past experience has demonstrated that, under the current circumstances, domestic enterprises may not necessarily prevail in price wars. Chinese innovative companies need to identify their products’ unique features based on their actual operational conditions, establish robust clinical, marketing, and sales systems, and win over the market through product advantages.

As of November 30, 2023, there were a total of 21 financing events in the surgical robotics sector. Although the number of financing deals decreased compared to 2022, surgical robotics remains one of the most watched subsectors within the medical device industry, demonstrating strong innovation momentum. Specifically, laparoscopic surgical robotics saw 4 financing events; orthopedic surgical robotics recorded 3; ophthalmic and microsurgical robotics emerged as a standout segment in 2023 with 4 financing events; and despite the impact of Siemens’ exit from the PCI interventional surgical robotics business, vascular interventional surgical robotics still secured 3 financing deals, highlighting the resilience of domestic innovation.

Policy-driven market expansion ushers in a period of installation growth, with domestically produced surgical robots achieving commercial breakthroughs.As the “14th Five-Year Plan” for the allocation of large-scale medical equipment in 2023 was gradually implemented, a new wave of quotas began to be executed, kicking off a fresh round of large-scale equipment procurement across various regions. Meanwhile, the draft guidelines on access standards for the allocation of large-scale medical equipment lowered the thresholds in several areas, including hospital capabilities required for configuring laparoscopic surgical robots, the number of years hospitals have been performing laparoscopic surgeries, clinical application requirements, and physician qualifications. The combined effect of these two policies has unleashed substantial demand for the installation of surgical robots. It is reported that Edge Medical and MicroPort MedBot have both achieved commercial installations.

Da Vinci Surgical Robot’s Localization Efforts Target Second- and Third-Tier Markets.As the number of domestic participants continues to grow and tender procurement processes increasingly favor domestically produced products, the da Vinci Surgical System has begun to accelerate its localization strategy. On June 14, 2023, Intuitive Fosun’s China-produced “Thoracoabdominal Endoscopic Surgical Control System” received market approval, with registration certificate number “Guo Xie Zhu Zhun 20233010800.” On December 1, 2023, the Chinese Government Procurement Network announced that a domestically produced da Vinci system had won a bid at a price of RMB 19.78 million, representing a decrease compared to imported da Vinci systems. An analysis of the distribution of hospitals where da Vinci Surgical Systems were installed in 2023 reveals that second- and third-tier cities have become the primary locations for new installations, indicating that the commercialization strategy of the da Vinci Surgical System is now focused on penetrating hospitals in prefecture-level cities.

New Generation of Joint Surgery Robots Unveiled. On March 8, 2023, orthopedic giant Stryker (NYSE: SYK) unveiled the Mako Total Knee 2.0 robotic system for total knee arthroplasty at the 2023 Annual Meeting of the American Academy of Orthopaedic Surgeons (AAOS). The Mako Total Knee 2.0 is built upon Mako SmartRobotics™ and its three key components: CT-based 3D surgical planning, AccuStop™ haptic technology, and Insightful data analytics. The Mako Total Knee 2.0 also introduces a more intuitive design interface, customizable workflows, and other critical features, including an innovative digital tensioning device that allows surgeons to assess knee stability during total knee arthroplasty (TKA) without the need for additional instruments.

Domestic companies have also launched next-generation joint replacement surgical robots.Taking the Kunwu® Total Orthopedic Surgical Robot launched by BoneSheng Yuanhua Robotics as an example, it is a domestically developed all-in-one system for hip and knee joint surgeries. It offers greater advantages over similar foreign products in terms of design philosophy, system performance, and learning curve. BoneSheng Yuanhua Robotics has independently developed the surgical robotic arm, navigation system, and all associated software, truly filling the gap in China’s high-end medical equipment manufacturing in this field.

Clinical acceptance continues to rise, and the number of orthopedic surgical robots is steadily increasing.In terms of commercialization, orthopedic surgeons and patients in China have gained considerable awareness of the safety, reliability, and distinct advantages of robotic-assisted orthopedic surgery compared to traditional procedures. Acceptance of such robotic systems is rising rapidly, indicating that the market is in a growth phase. With the implementation of centralized procurement policies for high-value orthopedic consumables, patients’ purchasing power has been partially liberated, providing them with greater opportunities to opt for robotic-assisted orthopedic surgeries. Data on the surgical volume of Tinavi’s installed systems show a steady growth trend in 2023. From January to September 2023, the cumulative number of procedures performed using Tinavi’s Tianji robotic system exceeded 16,000 cases, representing a year-on-year increase of over 70%. In recent months, monthly surgical volumes have consistently surpassed 2,000 cases. This development sends positive signals for the commercialization of robotic-assisted orthopedic surgery and boosts industry confidence.

Meanwhile, domestic companies have also launched next-generation surgical robots, achieving better integration of surgical robotics into the entire workflow of orthopedic procedures., the market for orthopedic surgical robots is poised for further expansion. Taking Tuodao Medical as an example, the company has launched an integrated solution of “surgical robot + intraoperative imaging equipment” to address key pain points in orthopedic surgery, such as weak interoperability between surgical robots and intraoperative imaging devices, the need for manual device calibration by physicians, high clinical operational complexity, and prolonged surgical duration. The Hyper-fusion Super-Converged Orthopedic Surgical Robot System by Tuodao Medical features a high degree of automation and ease of use, with one-click registration completed in as fast as 72 seconds. This system reduces robotic preparation steps, delivers high operational precision, enhances clinical consistency and surgical efficiency, and shortens operative time.

Ophthalmology & Microsurgical Robots Emerge as a Powerful Force.Traditional microsurgery relies on optical systems and precision surgical instruments, requiring the surgical field to be magnified 5 to 40 times under optical instrumentation for manual operation. Microsurgical procedures typically involve the anastomosis of lymphatic vessels, blood vessels, or nerves measuring 0.3–0.8 mm in diameter, addressing substantial unmet clinical needs across multiple specialties, including otolaryngology, lymphatic surgery, neurosurgery, and plastic surgery. Robotic-assisted microsurgery systems reduce tremor, enabling surgeons to perform highly complex and challenging procedures with greater ease and enhancing their ability to repair delicate anatomical structures.

Fundus surgery robots are the primary products of interest for domestic companies, with R&D in China keeping pace with global advancements.Among the many retinal surgery robot R&D teams worldwide, Xianwei Medical’s team was the first in China to engage in the development of retinal surgery robots. Unlike single-arm retinal surgery robots, Xianwei Medical’s ophthalmic surgical robot has evolved into a dual-arm system, enabling surgeons to explore more complex and challenging surgical procedures.

Consumer healthcare is on the rise, with surgical robots achieving cost reduction and efficiency improvement.China has substantial demand for dental implants, with significant room for growth in the penetration rate of surgical robots. According to data from Frost & Sullivan, China performed approximately 1.873 million dental implant procedures in 2021, among which robot-assisted dental implant surgeries accounted for only about 200 cases. The penetration rate of robot-assisted dental implant surgeries in the Chinese market remains low.

Chinese Companies Are Deploying Next-Generation Dental Implant Surgical RobotsFengzhun Robotics, a subsidiary of Meiya Medical—a well-known domestic brand in dental implantology—collaborated with South China University of Technology to develop its first-generation prototype in 2020. The company completed clinical trials involving 130 human subjects in 2022 and has obtained regulatory approval. As a subsidiary of a dental implant chain group, Fengzhun Robotics possesses deep insights into clinical needs. Its robotic system can perform approximately 80% of surgical procedures in dental implant treatment, including complex cases such as half-mouth or full-mouth edentulism and severe alveolar bone deficiency. Procedures that previously required highly experienced specialists can now be easily accomplished using the robot. In addition, Meiya Medical Group’s self-developed product portfolio includes dental implants, abutments, accessories, and related consumables such as personalized bars and screws for implantology. Regulatory approvals for most of these products are expected by 2024.

According to statistics from VCBeat, there were 16 publicly disclosed financing events in the field of biomaterials and regenerative medicine in 2023, with multiple funding rounds highlighting that this sector is currently a hot investment trend. In 2023, several innovative biomaterial and regenerative medicine products were also approved in China. Areas such as high-end tissue repair membranes, advanced hemostatic materials, tissue engineering, and regenerative materials for medical aesthetics have attracted significant attention.

Tissue-Engineered Artificial Blood Vessels: Domestic Products Poised to Break Through the Challenges of Standardized Mass Production.Traditional ePTFE artificial vascular grafts with a 6-mm inner diameter, manufactured by companies such as Gore, Bard, and Maquet, have been used for nearly 50 years in applications including arteriovenous access for chronic renal failure, lower extremity arterial bypass, and vascular replacement for lower extremity arterial trauma. However, persistent issues of low patency rates and susceptibility to infection have severely compromised clinical outcomes. In particular, there is a global shortage of artificial vascular grafts with an inner diameter of 3.5–4 mm suitable for coronary artery bypass grafting (CABG), forcing patients to rely on autologous vessels, which leads to numerous clinical complications. Tissue engineering technology offers a novel approach for the in vitro cultivation of artificial blood vessels: seed cells are seeded onto tubular biomaterial scaffolds to construct tissue-engineered vessels with morphology and performance resembling those of human vessels in vitro, during which the biomaterial gradually degrades. After implantation, host cells, including endothelial cells and vascular smooth muscle cells, remodel the vessel wall within a certain period, forming neointima consistent with native arteries. This significantly improves vascular patency and resistance to infection, demonstrating substantial potential to replace traditional ePTFE grafts.

Humacyte, a US-based company, is a global leader in tissue-engineered vascular grafts. Its product became the first to receive Regenerative Medicine Advanced Therapy (RMAT) designation from the FDA in 2017. In June 2022, without obtaining full FDA approval for marketing authorization, the U.S. Department of Defense authorized the FDA to permit its “emergency use” on the battlefield in Ukraine. Real-world follow-up results have surpassed those observed in Phase III clinical trials. On December 12, 2023, Humacyte submitted its first Biologics License Application (BLA) to the FDA for the indication of traumatic lower-extremity arterial injuries. Meanwhile, on April 11, 2023, Humacyte completed enrollment in its Phase III clinical trial evaluating vascular access for hemodialysis in patients with chronic renal failure, and coronary artery bypass grafting clinical trials are scheduled to commence in 2024.

Himai Medical Technology (Suzhou) Co., Ltd., a domestic enterprise, benchmarks itself against Humacyte. Its core product pipeline consists of tissue-engineered blood vessels with inner diameters of 6 mm and 3.5 mm, respectively. Indications include vascular access for hemodialysis in chronic renal failure, lower extremity arterial trauma (including combat injuries), lower extremity atherosclerotic bypass surgery, and coronary artery bypass grafting. With 18 years of R&D accumulation in this field, Himai Medical has developed standardized in vitro cultured human allogeneic small-diameter tissue-engineered blood vessels. Its products are poised to enter the clinical research stage. The company has been granted six Chinese invention patents and has filed multiple PCT patent applications.

China’s neurointerventional and peripheral interventional markets remain in the early stages of development. A total of 12 financing deals were completed across these two sectors, with five in neurointervention and seven in peripheral intervention. In the past, the high certainty associated with neurointerventional and peripheral interventional fields attracted a large influx of domestic companies, leading to intense competition. The growth in procedural volumes has failed to keep pace with the rapid market launch of numerous similar products. Nevertheless, the neurointerventional and peripheral interventional device markets still hold substantial growth potential.

Volume-Based Procurement Drives Growth in Neurointerventional Procedure Volumes, with Highly Differentiated Products Breaking Through Homogenization.In the neurointerventional market, as stroke treatment continues to penetrate primary care levels, China has established over a thousand stroke centers of varying tiers, leading to a rapid increase in the number of physicians qualified to perform neurointerventional procedures. Given that neurointervention is still in its early-to-mid development stage with a relatively low procedural base, and driven by years of patient education, continuous penetration among physicians and hospitals, and the high prevalence of cerebrovascular diseases in China, the volume of neurointerventional procedures is expected to maintain stable and reasonable growth in the future. Companies with diversified product portfolios and strongly differentiated innovative products are poised to capture greater market share and gain recognition from capital markets. In the secondary market, Sino Medical has strategically differentiated itself by focusing on the niche area of neurointerventional stenosis management. With the domestic launch of its exclusive intracranial drug-eluting stent, the company’s neurointerventional business has achieved substantial progress.

In the primary market, Nuanyang Medical completed a financing round worth tens of millions of RMB in 2023. This round was led by Yunsheng Investment, with participation from Jiangsu High-Tech Investment Group, Nantong Xinyuan Investment, and existing shareholders Yijing Capital and Daotong Investment. Nuanyang Medical’s core product is a flow diverter with high R&D barriers. In the field of aneurysm treatment, flow diverters represent a new generation of therapy following coil embolization and stent-assisted coil embolization. The YonFlow® flow-diverting stent system, independently developed by Nuanyang Medical, allows for recapture and redeployment after the stent has been fully released from the microcatheter, enabling timely position adjustments. It also features excellent pushability and maneuverability, and is compatible with various microcatheters sized 0.021 inches and above, addressing the issue of universal compatibility with ancillary devices. Special surface treatments and tip design enhance the safety profile of the stent. This flagship product passed the innovative medical device review by the National Medical Products Administration (NMPA) in January 2023, entering the “green channel” for innovative medical devices, and is expected to obtain regulatory approval in 2024.

In 2023, there were 86 financing events in the in vitro diagnostics (IVD) sector, representing a decline from 2022 and indicating reduced investment enthusiasm. In recent years, the implementation of national and regional centralized procurement has been reshaping the IVD industry landscape. The hospital entry prices for traditional IVD products have dropped significantly, ushering in an era of slim margins. On one hand, policy, technological, and market dynamics are driving intense competition within the IVD industry; on the other hand, advancements in various innovative technologies in the IVD field are bringing new hope for industry development.

From the perspective of financing热度, niche sectors such as flow fluorescence, mass spectrometry, new gene sequencing technologies, upstream raw materials, tumor NGS, AD diagnosis, and spatial omics continue to attract significant attention. Excluding the COVID-19 testing market, IVD remains the largest sub-sector within medical devices and continues to maintain robust industry growth. New therapeutic approaches—including novel disease prevention (such as AD screening), personalized treatment, precision medicine, and dynamic monitoring—urgently require the application of new diagnostic technologies. The IVD market remains substantial, particularly as IVD technologies penetrate primary healthcare settings, unlocking immense potential for incremental market growth.

Dr. Song Yanqun, Vice President of the Innovation Business Division at Haoyue Capital, who specializes in the IVD and life sciences sectors, believes that 2023 was a year for the in vitro diagnostics (IVD) industry to digest inventory and valuation bubbles in the post-pandemic era. With more than 60 domestically listed IVD companies, intensifying competition within the industry is reaching a critical point of differentiation. To secure a position in the market, companies can break through in three key areas: deeply exploring differentiated clinical application scenarios based on precision medicine; increasing revenue while reducing costs by diligently building commercial systems and cultivating the market; and expanding into overseas markets to seize opportunities in emerging markets.

In 2023, numerous new opportunities also emerged, with differentiated innovative projects and hard-tech projects featuring domestic substitution attributes attracting the most attention. In the hard-tech sector, focus has been placed on the domestic substitution of core products and key bottleneck technologies; for instance, the gene sequencer field still saw multiple large-scale financing rounds. In the realm of differentiated innovation, both technological innovation and application scenario innovation are worthy of attention.

Commercialization of Early Cancer Screening Advances Through Exploration; New Horizon’s Path to Profitability Boosts Industry Confidence.Currently, the early cancer screening industry is in the initial stage of commercialization. The penetration rate of early cancer screening remains low, but end-user demand continues to grow driven by consumption upgrades and supportive policies. From concept to implementation, New Horizon Health’s diversified commercial explorations have opened up new avenues for high growth within China’s domestic industry. At present, the commercial deployment of early cancer screening products primarily takes two forms: IVD (In Vitro Diagnostic products) and LDT (Laboratory Developed Tests). The IVD model requires large-scale prospective clinical trials and NMPA certification; while this entails high regulatory barriers for compliance, it offers broad commercial prospects by targeting asymptomatic high-risk populations. In contrast, LDTs have relatively lower entry thresholds, but their market is confined to clinical settings, serving only hospitalized patients, thereby facing significant challenges.

NewHorizon Health Builds a New Business Ecosystem by Expanding into Out-of-Hospital Markets and Consumer Healthcare.In exploring the commercialization pathway for early cancer screening, New Horizon Health has delivered results that exceeded expectations. Its flagship early-screening product, Colotect, is the first molecular diagnostic test for early cancer screening approved by China’s National Medical Products Administration (NMPA). Since launching its first product, New Horizon Health has insisted on conducting large-scale prospective clinical validation for every cancer screening product it develops. According to the product review report published on the NMPA website, Colotect demonstrates a sensitivity of 95.5% and a negative predictive value of 99.6% for colorectal cancer, enabling effective screening among asymptomatic, high-risk individuals aged 40 to 74 years.

New Horizon Health is a benchmark enterprise in China’s early cancer screening sector. Its marketed products and R&D pipeline cover high-incidence cancers in China, including colorectal, gastric, cervical, liver, and nasopharyngeal cancers. In late 2023, the company jointly launched the clinical study of the PANDA cohort project for pan-cancer early screening and diagnosis with the Health Science Center of Peking University, initiating large-scale enrollment. The company’s marketed products—ColoClear, PuPuGuan, and YouYouGuan—benefit from robust regulatory barriers and are experiencing rapid market expansion. As of the 2023 interim report, New Horizon Health achieved triple-digit revenue growth for three consecutive years, turned profitable, and recorded its first recurring profit over the trailing twelve months. According to New Horizon’s Double 11 disclosure, ColoClear had completed over 880,000 tests by November 10, 2023, generating revenue exceeding RMB 1 billion.

In 2023, the minimally invasive surgery sector completed 13 financing rounds, with capital primarily concentrated in endoscopy and energy-based device products. Driven by the converging trends of minimally invasive techniques, precision, and digital-intelligent transformation, the minimally invasive surgery market is poised for sustained high-speed growth. As the sector enters a phase of high-quality development, leading domestic enterprises capable of providing integrated solutions will occupy the high end of the value chain. Regarding the development of domestic companies, Chinese firms have initially achieved import substitution; however, their per-unit market share remains to be improved. Compared with multinational corporations (MNCs), domestic leaders still lag in terms of product diversification, scale, and advanced functionalities.

2023In 2026, the domestic ultrasonic scalpel market is undergoing a period of transformation.Ultrasonic scalpels account for the largest share within the energy-based device platform and represent the sub-segment with the greatest potential for domestic substitution. Under the DRG (Diagnosis-Related Groups) and DIP (Big Data Diagnosis-Intervention Packet) payment policies, ultrasonic scalpels are encountering a new wave of growth opportunities, while centralized procurement is also reshaping the industry landscape. The ultrasonic scalpel market is characterized by strong growth potential, a low rate of domestic substitution, and a relatively favorable competitive structure. Amidst the pressure of price reductions from centralized procurement, well-prepared Chinese manufacturers are reaping the benefits of rapid volume expansion. However, international mainstream brands still hold a dominant position in the high-end market. Laparoscopic surgeries are primarily performed for tumor resection in surgical oncology; consequently, hospitals conducting these procedures exhibit higher concentration and are generally of higher tiers. Laparoscopic surgical tools used by physicians, particularly laparoscopic staplers and ultrasonic scalpels, directly engage in tissue cutting and suturing. Poor product quality can easily lead to surgical risks, prompting physicians to maintain extremely high quality standards for these instruments and raising the bar for domestic alternatives.

Domestic enterprises need to impress the market with higher quality and innovation.Taking Ansukang as an example, Ansukang has pioneered a new generation of console-free ultrasonic scalpels, integrating traditional components such as the ultrasonic generator, transducer, torque wrench, and control mechanism into a single unit. This innovation achieves a console-free ultrasonic scalpel system, breaking through the traditional design paradigm that has persisted for 30 years. In addition to differentiating itself through innovation to overcome market homogenization, Ansukang has optimized the cutting and hemostatic efficiency and precision of traditional ultrasonic scalpels, making substantial adjustments to address issues related to the efficient use of the blade tip. Regarding shaft stability, the manufacturing quality of the blade tip is subject to multiple stringent controls, ensuring greater stability and earning consistent acclaim in clinical applications.

Chinese Companies Expand from Disposable Ureteroscopes to Multiple Fields.Previously, domestic companies primarily entered the market with disposable flexible ureteroscopes. This was driven by two main factors: first, traditional reusable flexible ureteroscopes have a very high damage rate, leading to significantly increased maintenance costs and extremely high per-procedure costs. In contrast, the per-procedure cost of disposable flexible ureteroscopes is far lower than that of reusable ones, creating substantial clinical demand. Second, due to the long shaft and narrow instrument channel of flexible ureteroscopes, cleaning and disinfection are difficult, posing risks of cross-infection. Disposable flexible ureteroscopes eliminate this risk, offering superior safety. Furthermore, the procurement cost of reusable endoscopes for urology departments in Chinese hospitals can reach hundreds of thousands or even millions of RMB. The high price of reusable endoscopes has left room for the development of domestically produced disposable endoscopes. As the number of market participants increases, companies with stronger comprehensive capabilities are taking the lead in exploring more application scenarios. For example, RayPai Medical has obtained regulatory approvals for multiple products across various departments, including urology, gynecology, hepatobiliary surgery, and gastroenterology, with commercialization gradually underway. Approvals for respiratory, otolaryngology, and orthopedic applications are also expected in the next two years. RayPai Medical is the first company in China to obtain a Class III registration certificate for a disposable cystoscope. It currently holds nearly 50 domestic and international registration certificates and owns more than 80 core patents.

Global Endoscopic Procedure Volumes and Single-Use Penetration Rates

A significant trend in medical device investment in 2023 was a strong focus on sectors with consumer-oriented attributes. Ophthalmology and dentistry have emerged as popular hotspots, giving rise to leading domestic companies. China possesses the ideal conditions for nurturing giants in the hearing aid industry; however, no true industry leader has yet emerged in the domestic hearing care market, either in terms of services or products. While China exports a large volume of low-end hearing aids, high-end products remain heavily reliant on imports. According to data from China Customs, China’s hearing aid exports totaled 14.318 million units in 2022, with the United States, the United Kingdom, the Netherlands, Malaysia, and Japan being the primary export destinations. In the same year, China imported 1.355 million hearing aids, with Denmark, Vietnam, and Singapore serving as the main sources of imports.

The domestic hearing aid market in China represents a blue ocean with substantial potential. However, enterprises that possess strong product capabilities, sufficient production capacity, extensive channel resources, and robust terminal reach remain scarce. In 2023, Boyin Hearing was the only company in China’s specialized hearing sector to secure financing. Boyin hearing aids integrate multiple technological advantages, featuring proprietary algorithms, fitting software, and programmers, which facilitate store-based fittings and enhance user convenience, indicating promising market prospects. The founder of Boyin brings extensive industry experience and broad resources, with comprehensive expertise in the commercialization of hearing aid products, while core team members each have over ten years of accumulation in the hearing aid industry. From 2023 to 2025, Boyin Hearing will complete the registration and mass production of more than ten hearing aid models, fully meeting the usage needs of users across various types and price ranges. In addition to breaking through technical barriers, Boyin Hearing places significant emphasis on service enhancement. The company has successfully established an end-to-end service system integrating prevention, assessment, treatment, and rehabilitation, offering an efficient and convenient one-stop service model to provide users with comprehensive hearing solutions. Amidst the opportunities for import substitution in the medical-grade hearing aid market, Boyin Hearing is expected to leverage this momentum to lead the development of China’s domestic hearing market.

In 2023, six financing deals were completed in the medical imaging sector, with four of them involving upstream core components.

Policy Implementation Drives Rapid Growth in China’s Medical Imaging Market. The implementation of the “Catalogue for Configuration Licensing Management of Large-Scale Medical Equipment (2023)” in March 2023 and the “14th Five-Year Plan for the Configuration of Large-Scale Medical Equipment” in June has removed quota restrictions on configuration licenses for mid-to-high-end CT and MR products. As a result, market demand for mid-to-high-end and ultra-high-end CT systems continues to rise, while the MR market has achieved rapid growth. Market demand for molecular imaging (MI) and radiation therapy (RT) is also expected to be further unleashed. Driven by multiple factors—including the development of National Medical Centers, national/provincial regional medical centers, the “Thousand Counties Project,” county-level sub-centers, nuclear medicine departments, and oncology centers, along with the reform of configuration licensing—the market space is poised for further expansion.

China's Leading Players Push into High-End Ultrasound, Filling the Gap in Domestic ProductionThe domestic ultrasound market exceeds RMB 14 billion, with high-end ultrasound systems priced as high as one million yuan. The high-end ultrasound segment (including cardiac ultrasound and four-dimensional gynecological ultrasound) has long been dominated by multinational corporations, which hold approximately 70% of the market share in this sector. Key technologies such as ultrasound software, complex functionalities, and real-time 3D imaging serve as critical entry barriers to the high-end ultrasound market. For a considerable period, domestically produced medical ultrasound equipment was primarily concentrated in the mid-to-low-end segments, resulting in weak overall competitiveness. In 2023, Chinese manufacturers achieved significant breakthroughs in the high-end ultrasound field. Hisense Medical launched the HD70, a high-end intelligent ultrasound system. The HD70 adopts a new-generation “Wide-Area” ultrasound platform, features a novel GPU architecture, and incorporates completely redesigned hardware, core system pathways, and logical systems. This design realizes a transformation from hardware-based to software-based beamforming, leading to an exponential increase in computational power and processing speed. Consequently, the images exhibit improved full-field uniformity and spatial resolution, substantially enhancing the quality and precision of various advanced imaging functions. The HD70 offers numerous intelligent measurement capabilities, including automatic measurement of carotid intima-media thickness, amniotic fluid index, bladder volume, and cardiac function. A distinctive feature of the Hisense HD70 is its automatic measurement of uterine fibroids, which assists junior physicians in rapidly and automatically measuring multiple uterine fibroids, thereby improving measurement accuracy and further boosting work efficiency.

Microsurgical techniques present high technical barriers, with multiple products still lacking domestic alternatives in China.Microsurgery is a clinical specialty in which China holds distinct advantages and unique characteristics, consistently maintaining a leading position on the international stage. Driven by the trend toward specialization in microsurgery, the volume of microsurgical procedures in China has grown rapidly. Due to the intricate nature of these operations, there are extremely high requirements for the quality, precision, and ease of use of surgical instruments. As the field involves precision manufacturing, it also demands strong capabilities in product design and development, high equipment machining accuracy, process stability, and skilled technical expertise. Consequently, several innovative medical devices for vascular anastomosis and free flap surgery were previously unavailable from domestic manufacturers. As the localization of high-end medical devices enters a more advanced phase, domestic substitution in the high-barrier field of microsurgery has garnered significant attention, with Chinese enterprises gradually filling these gaps. A case in point is Kechuang Medical, a leading domestic player in microsurgery that has deeply cultivated this field for many years. Leveraging its independent innovation technology platform, the company has launched multiple exclusive domestic products. Targeting critical microsurgical procedures such as vascular and nerve anastomosis, Kechuang Medical has introduced microvascular anastomotic devices and absorbable nerve conduits. The microvascular anastomotic device enables rapid and safe anastomosis of blood vessels ranging from 0.8 mm to 4.3 mm, significantly reducing operative time.

The above is an excerpt of the main content of the report. Below are the outstanding innovation case studies of the year. Scan the QR code on the poster to access the full report.

Report Table of Contents:

PART 01: By the Numbers in 2023—The Industry Faces a Moment of Restructuring

1.1 Financing: Global Healthcare Financing Cools Down

1.2 IPO: Global MedTech IPOs Slow Down, BSE Offers New Opportunities

1.3 Policy Trends: Observing Industry Trends from Approval Data

PART 02 Interpretation of Innovative Subsectors in the Medical Device Industry

2.1 Cardiovascular: Rebirth After Centralized Procurement, with Two Major Development Threads Advancing in Parallel

2.2 Ophthalmology: A Vast Consumer Market, the Ophthalmology Sector Remains Attractive

2.3 Fierce Competition in Consumer Healthcare’s Dental and Ophthalmology Sectors, While the Hearing Care Segment Quietly Emerges

2.4 Surgical Robots: Policy-Driven Market Expansion, Orthopedic Segment Sends Positive Signals

2.5 Biomaterials & Regenerative Medicine: The Three Major Directions of Regenerative Materials, Cell Technologies, and Tissue Engineering Will Continue to Drive Incremental Innovation

2.6 Neuro & Peripheral Intervention: Differentiated Products Reap Bountiful Harvests After the Tide Recedes

2.7 In Vitro Diagnostics: The Industry Returns to Normal Development, and Innovative Technologies Enter a Window of Opportunity

2.8 Minimally Invasive Surgery: Entering the Warring States Period

2.9 Medical Imaging: Configuration Certificate Policies Drive Market Growth, with Gradual Breakthroughs in Upstream Core Components

2.10 Microsurgery: High Barriers in Precision Manufacturing, with Multiple Products Still Lacking Domestic Alternatives

2023 Outstanding Cases of Annual Innovation in Medical Devices and Supply Chain

PART 03 Interpretation of Innovative Cases in Medical Devices and Supply Chains in 2023

Tuodao Medical: Pioneers the Orthopedic Hyper-Converged System, Achieving Comprehensive Interoperability of Control and Data Through an Integrated “Robotics + Intraoperative Imaging” Solution

Kechuang Medical: A Leader in Microsurgery, Filling Multiple Gaps in Domestic Products

Hisense: Leading the Ultrasound + AI Technology Revolution, Filling the Gap in High-End Domestic Ultrasound

Dejin Medical: First Domestically Produced Transcatheter Mitral Valve Clip System Approved, Pioneering a New Era in Interventional Therapy for Structural Heart Disease in China

Yuanhua Intelligence: Focused on the R&D and manufacturing of specialized surgical robots; commercialization of the first domestically developed all-in-one system for hip and knee joint replacement

Yuewei Medical: AI-Powered SYNTAX Score Enables Precision Diagnosis and Treatment of Coronary Artery Disease

Ansukang: A New Generation of Console-Free Ultrasonic Scalpel, Breaking Through 30 Years of Traditional Design

RuiPai Medical: A Domestic Unicorn in Endoscopy, Leading the Disposable Endoscope Sector

Haimai Medical: Human Cell-Based "Manufactured" Blood Vessels Break Through the Challenge of Standardized Mass Production in Ex Vivo Tissue-Engineered Vascular Culture

Xianwei Medical: Third-Generation Dual-Arm Fundus Surgical Robot, Assisting Physicians in Performing High-Precision Complex Surgeries

Nuanyang Medical: Original, Independently Developed Technologies Drive Breakthrough Innovations, Leading the Iteration of Neurointerventional Products

New Horizon Health: Leading the Way in Early Cancer Screening, with Core Products Accelerating Volume and Driving Rapid Revenue Growth

Meiya Medical: Precision Navigation Technology Ushers in a New Era of Dental Implant Surgery

Boyin Hearing: Digital Closed-Loop, Building a Full-Lifecycle Hearing Health Ecosystem