Top 5 Internet Healthcare Acquisition Segments in 2015: A Prospectus Overview

VCBeat Research Institute Gu Beini Xu Lei

Earlier, the FDA approved Capsule’sSmartLinx Vitals PlusProduct, a monitoring system that connects hospitals and patients via mobile devices. The French company, which was acquired by Qualcomm last month, has also received FDA 510(k) clearance as requested, allowing it to be used as a Class II medical device. The total transaction amount remains undisclosed, but according toQualcomm LifeThe company explained that this transaction would significantly expand Qualcomm Medical’s business scope, extending its operations from purely home-based care to remote monitoring both inside and outside hospitals.

Accenture Consulting recently pointed out: by 2018,Healthcare EntrepreneurshipMergers and acquisitions (M&A) among companies will account for 8% of the total value in the healthcare system, a significant increase from less than 1% in 2014. This conclusion is drawn from a recent research report by Accenture, which analyzed 1,500 recorded transactions between 2006 and 2015. The year 2015 was an exceptionally active period for global corporate M&A activity; according to data from Dealogic, the total value of M&A transactions so far this year has reached $4.9 trillion, setting a new historical record and surpassing the previous high of $4.6 trillion set in 2007. Research institutions have stated that there were approximately 217 mergers and acquisitions in the internet healthcare sector in 2015, nearly double the number in 2014.

VCBeat now provides a quick overview of the major global M&A transactions in the internet healthcare sector from Q1 to Q4 2015, totaling 43 deals. See the table below for details.

An examination of the 2015 acquisition deals reveals several noteworthy characteristics:

1. Acquisition projects targeting healthcare institutions were the most numerous

Nearly half of the target customer base for the acquired companies’ core businesses is concentrated in medical institutions, i.e., healthcare service providers, with a few projects also serving pharmaceutical companies or health insurance departments. The next largest segment comprises businesses targeting general consumers, numbering 14 companies. This is followed by six companies focused on patients. When categorized by business model as either B2B or B2C, there are 22 B2B-oriented companies and 21 B2C-oriented ones, representing an almost even split.

2. Mobile Fitness Sector Seeks Capital Exit Strategies

In terms of the specific sub-sectors that attracted acquirers, 2015 saw a large number of mobile fitness apps being acquired. When combined with smart hardware for mobile fitness, this sector recorded the highest number of M&A transactions. In 2015, Fitbit, a leading brand in fitness trackers, successfully completed its IPO and received highly positive market feedback, reaching a valuation of $6.5 billion. Meanwhile, Misfit, a competitor with similar products but a lower market share, was ultimately acquired by the renowned watch brand Fossil for $260 million—a 25-fold difference in valuation. This highlights the vast gap between the market leader and the runner-up. Additionally, many prominent fitness apps were sold to sports equipment companies or gym chains. It appears that the wave of capital exits for mobile fitness startups in the mainstream North American market has already peaked.

Telemedicine and medical data analytics companies emerged as the two most popular acquisition targets, tied for second place. Most acquirers of telemedicine projects were established industry leaders already in the top tier, with one case each involving acquisitions by traditional healthcare providers and chain pharmacies. Meanwhile, activity in the data analytics sector focused primarily on operational and clinical data analysis solutions tailored to healthcare providers.

Five companies focused on cost-containment initiatives to reduce healthcare insurance expenditures were acquired, making this another hotspot sector; such projects often leverage data analytics technologies to achieve their goals. Additionally, four smart hardware products were acquired.

3. Diversification of Acquirers

From the perspective of the business relationship between acquirers and acquirees, projects in niche sectors were most frequently acquired by internet/IT companies with broader business scopes or larger scales, accounting for 21 transactions, or exactly half of the total. Meanwhile, established players in traditional sectors—such as traditional sports apparel brands, fitness clubs, professional consulting firms serving healthcare institutions, and pharmaceutical companies—also emerged as significant acquirers, involved in 18 transactions. A small number of other projects were acquired by cross-industry tech giants, such as IBM and Qualcomm.

Below is a detailed overview of acquisitions with transaction values exceeding RMB 100 million (publicly disclosed transaction amounts):

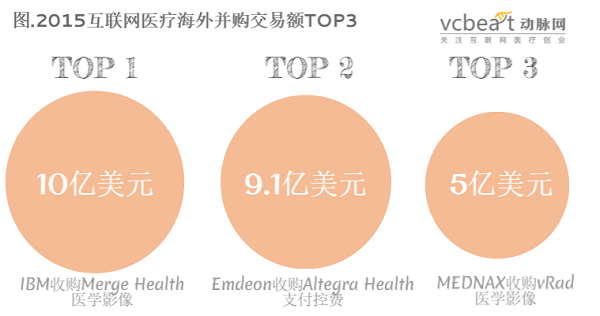

Topping the list of M&A transactions is IBM’s $1 billion acquisition of Merge Healthcare, a provider of medical imaging equipment. Headquartered in Armonk, New York, Merge Healthcare states that its technology is used by more than 7,500 healthcare sites across the United States. IBM plans to integrate Merge Healthcare’s technology into its Watson supercomputing business through this acquisition. Prior to this deal, IBM had already acquired two startupsPhytelandExplorys, with the aim of enhancing its Watson Health Cloud project. Meanwhile, in July this year, IBM announced a strategic partnership with CVS, the largest drug retailer in the United States.

The second place isEmdeonSpent $910 million to acquire a company that develops analytics tools for payers and most providersAltegra HealthCompany. Emdeon is a provider of healthcare software and technology services. By integrating Altegra Health’s risk adjustment and quality analytics technologies with its own revenue cycle management (RCM) methodologies and payment tools, Emdeon will better and more accurately guide healthcare organizations into a new era of transaction-based insurance and value-based medical billing.

Then there isMEDNAXAcquired a virtual imaging company for $500 million.vRadvRad is a global telemedicine company and the largest radiology medical services provider in the United States, with over 450 radiology specialists. Its proprietary software, data, and clinical practices enable physicians to rapidly and securely transmit patient imaging and medical history to appropriate specialists, thereby enhancing the speed and accuracy of clinical diagnoses while reducing costs. Currently, vRad’s physicians and operational platform serve more than 2,000 hospitals, generating over seven million diagnostic reports annually. Among vRad’s 450 radiology specialists, 75% are chief physicians with more than nine years of subspecialty radiology practice following board certification. Additionally, vRad operates a top-tier imaging service platform and holds 14 patents.

Notably, two of the three largest transactions by valueAll projects focus on the field of medical imaging.

Following closely behind are sports equipment manufacturersUnder ArmourSpending $475 million on a nutritional data tracking platformMyFitnessPalAcquired under its umbrella. MyFitnessPal had previously announced that the platform’s registered users had surpassed 80 million. Under Armour aims to leverage MyFitnessPal to forge stronger connections with athletes, build greater brand loyalty, and promote a healthier, more active lifestyle. Of course, all of this is ultimately aimed at selling more athletic shoes and apparel.

The Fifth Major Acquisition WasPremierCloud-based data analytics platform acquired for $400 millionCECity. Like Premier, CECity is also focused on performance management and improvement, value-based payment reporting, and professional education. Both companies share the same clear goal: to provide higher-quality, more cost-effective healthcare services to hospitals and other medical institutions.

No. 6 isHuron ConsultingAcquisitionStuder Group$325 million, Studer Group can provide users with healthcare consulting services.

Next isCardinal HealthThe company acquired an acute care coordination and bundled payment program management firm for $290 million.NaviHealth.

Next is the watch manufacturerFossil GroupAcquired fitness tracker manufacturer Misfit for $260 million. Founded in 2011, Misfit has raised a total of $63 million across three funding rounds to date, with investors including Xiaomi, GGV Capital, JD.com, Horizons Ventures, Founders Fund, Khosla Ventures, and Norwest Venture Partners. Fossil aims to integrate Misfit’s technology into products that more closely resemble traditional watches by next year, rather than limiting itself to developing rubber-cased fitness devices. The company plans to continue offering Misfit’s own product line.

Then, Adidas acquired fitness app developer Runtastic for $240 million. Given that Runtastic currently has 70 million active users, this acquisition will help Adidas enhance the competitiveness of its products in the wearable smart device sector.

Finally, Quality Systems acquired the mobile electronic health record company Healthfusion for $165 million, and QSI stated that it would make an additional $25 million in equivalent investment if Healthfusion performed well before March 2016.

Other M&A transactions with significant amounts and disclosed figures include:

1. Under Armour acquired fitness community and app developer Endomondo for $85 million, a move expected to help the U.S. sports brand sell more athletic gear.

2. Citadel Group Acquired Healthcare Software Provider PJA Solutions for $45 Million. PJA is a healthcare software service provider, primarily offering clinical healthcare solutions, clinical diagnosis and treatment software, and integrated management systems.

3. Teladoc Acquired Telemedicine Provider Stat Health Services for $35 Million; the latter, a telemedicine company similar to Teladoc, primarily offers patients 24/7 remote medical consultation services. The acquisition is expected to significantly enhance Teladoc’s telemedicine capabilities.

4. Arcadia Healthcare Solutions Acquired Sage Technologies, a Professional Business Intelligence (BI) Services Provider, for $28 Million.