Baidu Enters Internet Insurance: Strategic Partnership with Allianz and Implications for Internet Healthcare

This article continues from:What Does an Insurance License Mean for Internet Healthcare? (II) How Difficult Is It to Apply for a Life Insurance License

Part III: Internet Insurance and Related Internet Healthcare Projects

Breaking News: On November 25, Baidu announced a deep strategic partnership with Allianz SE, Europe’s largest insurer based in Germany, to jointly establish an internet insurance company that will conduct online insurance business across China. With this move, the three tech giants known as BAT have once again converged, engaging in fierce competition for the highly explosive insurance market. It is easy to anticipate that competition in the internet insurance sector will intensify significantly, with successive waves of heightened rivalry expected. Thus, the most compelling developments are yet to come.

What is internet insurance? Internet insurance is generally defined as the operational activities wherein insurance companies or insurance intermediaries provide product and service information to customers via the internet, enabling online insurance operations such as application, underwriting, risk assessment, policy administration, and claims settlement, thereby completing the online sales and servicing of insurance products, and facilitating electronic payment of insurance-related fees through third-party institutions. In fact, it is not difficult to see from this description that, simply put, so-called internet insurance refers to the online sale of insurance and the completion of after-sales service processes.

Selling insurance online is not a new phenomenon. As early as 2000, Taikang Life Online, an insurance e-commerce company centered on internet-based operations, was established. Subsequently, insurance industry giants such as Ping An Insurance, China Pacific Insurance, New China Life Insurance, and China Life Insurance have all set up independently operated e-commerce subsidiaries.

The Much-Touted Internet Insurance License: Zero Breakthrough Yet for Life Insurance Licenses

In September 2013, ZhongAn Online P&C Insurance received approval from the China Insurance Regulatory Commission (CIRC) to commence operations, obtaining China’s first professional license for internet insurance. In July 2015, the Interim Measures for the Supervision and Administration of Internet Insurance Business were officially issued, regulating insurance institutions conducting internet insurance business through self-operated online platforms and third-party online platforms. These measures clearly defined the entities eligible to operate in internet insurance, including insurance institutions, self-operated online platforms, third-party online platforms, and professional insurance intermediaries. ZhongAn’s license does not imply that ZhongAn Online P&C Insurance represents an entirely new and unique business model; rather, it should be viewed more as a restricted license. This means that while other established insurance giants can conduct both traditional offline and internet-based businesses, ZhongAn Online is permitted to operate only online.

ZhongAn Insurance was jointly established by three industry titans: Jack Ma, Ma Mingzhe, and Pony Ma. It is important to note that ZhongAn Online currently holds only a property insurance license; its application for a life insurance license is still under regulatory review, with no final decision yet reached. On October 21, 2015, JD.com signed a strategic cooperation framework agreement with the Sichuan Provincial Government and submitted an application to regulators for an internet insurance license, specifically for property insurance. If approved, this would become the fifth internet insurance license in the industry. The other three internet insurance licenses were granted to YiAn Property Insurance (approved in June 2015), Anxin Insurance (approved in July 2015), and Taikang Online Property Insurance (approved in July 2015). However, all five internet insurance licenses, including JD.com’s pending application, are for property insurance only; the sector remains devoid of any pure-play internet life insurance companies.

Therefore, at present, internet insurance companies are mainly divided into two categories. One category consists of established insurers with existing licenses that are re-expanding their online insurance sales businesses; for example, Taikang Life Insurance provides users with one-stop direct online insurance services through its official website, Taikang Online. The other category comprises companies that operate exclusively via online channels and are required to obtain a new specialized license for internet insurance operations.

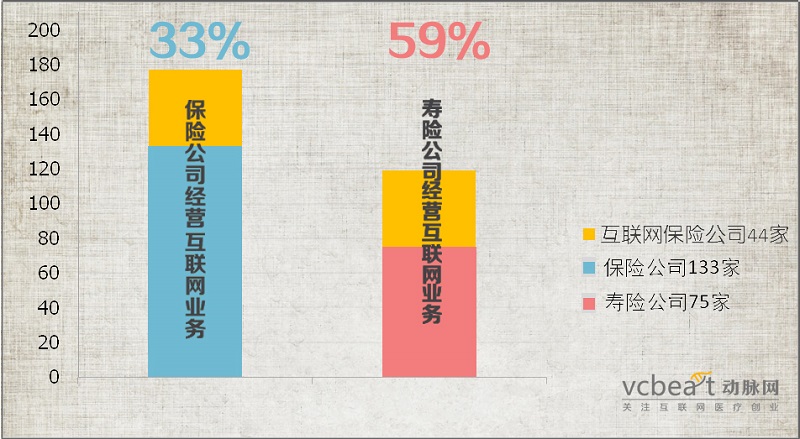

The "Report on the Development of the Internet Insurance Industry" released by the Insurance Association of China in 2014 showed that property and life insurance companies conducting internet insurance business accounted for 45% of the 133 insurance companies, including 44 life insurance companies and 16 property insurance companies.

The current market size of online health insurance premiums is only RMB 660 million.

From the overall business structure of life insurance companies, online health insurance accounted for a very small proportion of only 0.6% among various types of internet life insurance in the first three quarters of 2015, with its annualized premium volume reaching merely RMB 660 million. As for the agency sales parties, they ultimately earn commissions from premiums. If calculated at a commission rate of 20%, the total commission income generated by online health insurance sales in 2015 was approximately RMB 132 million.

As it stands, small and medium-sized life insurers are the primary players in internet-based operations, capturing 82% of the online life insurance market share with RMB 29 billion in premiums. Meanwhile, foreign-funded life insurers account for 15% of the online life insurance market share, representing a significant increase compared to their premium share through traditional channels.

If internet-based insurance business has seen significant growth, the number of insurance sales agents should logically have decreased. However, according to data released by the China Insurance Regulatory Commission (CIRC) for the third quarter of 2015, the number of insurance sales agents actually increased rather than decreased. In the third quarter, life insurance companies had 3.92 million marketing agents, an increase of 1.16 million compared to the same period last year, representing a year-on-year growth of 42%.

Drawing a parallel with the apparel industry, which has seen robust e-commerce growth, online apparel sales accounted for 1.8% of total industry sales in 2008, rising to over 20% four years later in 2012. If the share of internet-based health insurance could similarly reach 20%, it would represent a seven- to eight-fold increase. However, after excluding the portions captured by insurers’ proprietary online channels and other types of online sales platforms, this remaining share still seems insufficient for the many internet healthcare companies aiming to ultimately monetize through insurance sales. The market remains too small, fundamentally because the current scale of commercial health insurance is limited. Can breakthroughs in marketing models substantially enhance the appeal of commercial health insurance to consumers? It is unlikely that improvements solely in sales processes and claims handling will bring about qualitative change.

By-Health, an Active Participant in Internet Healthcare, Applies for a Mutual Insurance License

In the first half of 2015, mutual insurance has already become a hot topic in this year’s insurance market. It is reported that nearly 20 institutions are queuing up to apply for mutual insurance licenses. Among them are Ant Financial and Tianhong Asset Management, both affiliated with Alibaba Group, which are applying for mutual life insurance licenses.

Notably, in June 2015, four companies listed on the ChiNext board—Xinguodu, By-Health, Tengbang International, and Bohui Innovation—simultaneously announced their participation in the establishment of a mutual life insurance company, Trust Mutual Life Insurance. With the exception of Bohui Innovation, which contributed RMB 45 million, the other three companies each invested RMB 50 million, accounting for 5% of the initial operating capital of the mutual life insurance company respectively. Founded in 1995, By-Health operates in the nutrition and health industry and is the first enterprise in China’s healthcare sector to receive an AAA credit rating. Between 2014 and 2015, By-Health invested in and acquired stakes in numerous internet healthcare startups, covering areas such as mobile health management, smart hardware, and genetic testing. It is evident that By-Health is attempting to unlock value through health intervention services, ultimately extending into the life insurance sector.

Mutual Insurance Company refers to an unlisted insurance company that has no stockholders. A mutual insurance company is a legal entity established by all insured individuals, with the operational objective of providing low-cost insurance products to policyholders rather than pursuing profits. In essence, a mutual insurance company is a legal organization founded and jointly owned by policyholders based on the principle of mutual protection, operating insurance business for the benefit of the policyholders themselves. Unlike joint-stock insurance companies, the vast majority of profits generated by a mutual insurance company are returned to policyholders, thereby enabling insurance consumers to minimize costs while maximizing coverage.

In other words, the insurance company itself does not seek profit, operating purely to serve policyholders. This may sound familiar: the free-to-user model has long prevailed in the internet startup sector, and now the insurance industry is also embracing it? However, it is important to note that mutual insurance companies and joint-stock insurance companies can convert into one another. Furthermore, a logic worth considering is that mutual insurers often offer more favorable policy terms, which helps attract consumers to purchase coverage. Although premiums are more competitive, one type of expense remains unavoidable: claims payouts. As an operational cost for mutual insurers, these claims expenses are effectively transferred to healthcare product and service providers. If the entire chain—from healthcare products and services to insurance payment—operates under the same organization, the ultimate implication is that the premiums collected from insured consumers ultimately pay for that same organization’s medical products and services.

Which internet healthcare startups have ties to insurance companies?

Many internet healthcare companies regard commercial health insurance as the most viable path to profitability. In fact, for insurance companies, “Internet + Healthcare” also represents a new trend in the development of the health insurance industry. Based on news reports of collaborations between internet healthcare companies and insurers, we have listed several internet enterprises and their respective partners below. It is believed that many other companies have established private partnerships with insurers; however, due to limited public information, those not publicly disclosed are temporarily excluded from this list. Furthermore, many projects are indirectly affiliated with insurance companies because their investors have stakes in insurance firms or brokerage agencies. The chart below, compiled by VCBeat, lists startups that currently have direct or indirect financial ties to insurance companies.

Furthermore, many projects are indirectly affiliated with insurance companies because their investors have stakes in insurance firms or brokerage agencies. The chart below, compiled by VCBeat, lists startups that currently have direct or indirect financial ties to insurance companies.