Rehabilitation Medicine: The Next Investment Hotspot?

Rehabilitation medicine has always been a crucial component of modern healthcare. With the growing influence of international experience in rehabilitation care, coupled with the continuous improvement and opening-up of domestic policies in China, new models and technologies in rehabilitation medicine are emerging rapidly. The market value and potential of the rehabilitation healthcare industry are also expanding steadily. Industrial Securities Research Institute has conducted a comprehensive and in-depth analysis of the current state of rehabilitation medicine both domestically and internationally, and VCBeat has compiled an excerpt from this report.

The report analyzes the three major characteristics of China's rehabilitation medical care at the current stage:

Significant room for growth.

Insufficient supply.

Imperfect mechanisms.

The report suggests that the advantages of rehabilitation medicine in developed countries abroad lie in:

Characteristics of Rehabilitation Medical Service Systems in Developed Countries: A rehabilitation medical service system with a clear structure and well-defined functions; evidence-based, streamlined, and efficient service delivery processes; an insurance payment system grounded in standards and focused on functional outcomes; rehabilitation care teams centered on physiatrists; and emphasis on collaborative synergies involving communities and non-governmental organizations.

U.S. healthcare policies have had a profound and positive impact on the development of rehabilitation medicine.

The report predicts that, driven by the combined forces of policy, capital, and technology in China, the multi-hundred-billion-yuan rehabilitation medical industry is on the verge of taking off:

National policies such as tiered diagnosis and treatment and medical insurance have significantly strengthened support for rehabilitation medicine.

Social Capital and Public Hospitals Partner to Establish Rehabilitation Hospitals, Becoming the Mainstream Win-Win Model: Public Secondary Hospitals Seek Transformation, Operated Under the Management of Public General Hospitals, as Social Capital Floods into the Rehabilitation Medical Sector.

Specialized Rehabilitation Hospitals Possess Inherent Advantages: As Natural Partners of Public Hospitals, They Enhance Bed Turnover Rates and Revenue, Facilitate Health Insurance Cost Containment, and Alleviate Patients’ Financial Burdens. These Specialized Hospitals Boast Strong Profitability, Short Payback Periods, Low Labor Costs, Limited Staff Bargaining Power, and High Standardization, Making Them Easy to Rapidly Replicate and Expand.

Technological Advancement Acts as an Accelerator for the Rehabilitation Medicine Industry: Rehabilitation Robots Are Poised for Significant Growth, Brain-Computer Interface (BCI) Technology Facilitates Disease Recovery, Big Data and Virtual Reality Technologies Are Applied in Rehabilitation Care, and the Digitalization of Rehabilitation Services Is Steadily Advancing.

Below is a summary of the key highlights from the report by VCBeat.

I. Current Status and Market Application Prospects of Rehabilitation Medical Services in China

The report analyzes the importance and value of rehabilitation medicine:Rehabilitation medicine is an integral component of modern medicine’s tripartite framework encompassing prevention, clinical treatment, and rehabilitation. Rehabilitation medicine demonstrates significant application value in general hospitals. For conditions such as fractures, traumatic brain injury, cerebrovascular events, diabetes, cardiovascular diseases, rheumatoid arthritis, cervical spondylosis, and lumbocrural disorders, the integration of rehabilitation medicine more effectively accelerates patient recovery, improves functional outcomes, and significantly reduces disability and mortality rates, thereby playing a prominent role in enhancing overall clinical efficacy.

Rehabilitation medicine demonstrates significant application value in general hospitals. For conditions such as fractures, traumatic brain injury, cerebrovascular events, diabetes, cardiovascular diseases, rheumatoid arthritis, cervical spondylosis, and lumbocrural disorders, the integration of rehabilitation medicine more effectively accelerates patient recovery, improves functional outcomes, and significantly reduces disability and mortality rates, thereby playing a prominent role in enhancing overall clinical efficacy. The report segments the rehabilitation healthcare industry chain:The rehabilitation medical industry chain can be broadly divided into three parts:

The report segments the rehabilitation healthcare industry chain:The rehabilitation medical industry chain can be broadly divided into three parts:

Upstream are rehabilitation equipment and rehabilitation drug manufacturers.

The midstream segment comprises rehabilitation medical institutions, including rehabilitation departments of general hospitals, rehabilitation hospitals, and community rehabilitation centers.

The end users are patients requiring rehabilitation therapy.

The report analyzes the current status of rehabilitation medicine in China:The shifting disease spectrum driven by population aging in China, coupled with the rehabilitation needs arising from high-incidence conditions among the elderly and disability caused by chronic diseases, continues to expand the demand for rehabilitation medical services. Currently, China’s per capita market size for rehabilitation medicine is significantly lower than that of the United States, indicating substantial market potential. However, insufficient supply and an imperfect institutional framework for rehabilitation medical services constrain the development of China’s rehabilitation industry.The report analyzes the population base and market prospects for rehabilitation medical services in China:The demand for rehabilitation medical services in China mainly comes from three groups of people:

The report analyzes the current status of rehabilitation medicine in China:The shifting disease spectrum driven by population aging in China, coupled with the rehabilitation needs arising from high-incidence conditions among the elderly and disability caused by chronic diseases, continues to expand the demand for rehabilitation medical services. Currently, China’s per capita market size for rehabilitation medicine is significantly lower than that of the United States, indicating substantial market potential. However, insufficient supply and an imperfect institutional framework for rehabilitation medical services constrain the development of China’s rehabilitation industry.The report analyzes the population base and market prospects for rehabilitation medical services in China:The demand for rehabilitation medical services in China mainly comes from three groups of people:

First is the elderly population. Hypertension, diabetes, arthritis, cardiovascular and cerebrovascular diseases, and respiratory system diseases, which have high prevalence rates among the elderly, are the primary conditions for rehabilitation treatment. With the deepening aging of China's population, by the end of 2011, the number of people aged 60 and above in China reached approximately 190 million, of whom more than 70 million required rehabilitation services.

Second is the population with disabilities. According to the Sixth National Population Census and the Second National Sample Survey on Persons with Disabilities, by the end of 2010, the number of persons with disabilities in China had reached 85.02 million, among whom more than 50 million had rehabilitation needs;

Third, patients with chronic diseases and individuals in a sub-health state require rehabilitation services. It is projected that by 2030, the prevalence of chronic diseases in China will reach as high as 65.7%, with 80% of these patients needing rehabilitation treatment.

From 1998 to 2008, the incidence rate of diseases among Chinese residents continued to rise over the decade, particularly for chronic conditions such as hypertension, heart disease, and diabetes. According to data from the Fourth National Health Services Survey in 2008, the prevalence of chronic diseases increases with age. The shift in disease patterns driven by population aging, combined with the rehabilitation needs associated with high-incidence conditions among the elderly and disability resulting from chronic diseases, will continue to expand the demand space for the rehabilitation medical industry.

From 1998 to 2008, the incidence rate of diseases among Chinese residents continued to rise over the decade, particularly for chronic conditions such as hypertension, heart disease, and diabetes. According to data from the Fourth National Health Services Survey in 2008, the prevalence of chronic diseases increases with age. The shift in disease patterns driven by population aging, combined with the rehabilitation needs associated with high-incidence conditions among the elderly and disability resulting from chronic diseases, will continue to expand the demand space for the rehabilitation medical industry. China's Rehabilitation Medical Care Is in Its Early Stages, with Huge Market Potential:

China's Rehabilitation Medical Care Is in Its Early Stages, with Huge Market Potential:

According to 2010 statistical data, the total investment in rehabilitation funding for persons with disabilities by disabled persons’ federations at all levels across China amounted to RMB 1.33 billion, accounting for only 0.7% of the total public health expenditure and 0.038% of the GDP for that year. The per capita rehabilitation funding was merely RMB 1.1, and only 33.5% of individuals with disabilities received rehabilitation services. In contrast, based on the U.S. population and healthcare expenditure ratios in 2010, the per capita rehabilitation cost in the United States was USD 452.3 (including long-term care). This highlights a significant gap between China and developed countries, underscoring the need for continued increases in related investments in the future.

The “Report on the Development Prospects and Investment Forecast of China’s Rehabilitation Medical Industry” released by Qianzhan Industry Research Institute pointed out that in 2014, the total number of communities across China with established community rehabilitation stations reached 219,000, representing a year-on-year growth of only 2.34%, indicating substantial room for future expansion.

The report projects the market size and growth rate in China for the coming years:

The report projects the market size and growth rate in China for the coming years:

In 2013, the domestic rehabilitation medical market size in China was only RMB 20 billion (RMB 15 per capita), far lower than that of the United States at USD 100 billion (approximately USD 80 per capita).

Based on the level that basically meets China’s rehabilitation needs, the scale of China’s rehabilitation medical industry is projected to reach RMB 103.8 billion by 2023.

The projected compound annual growth rate (CAGR) is no less than 18%.

Summary: This report presents data analysis on key indicators, including demographic foundations, chronic disease incidence, healthcare expenditure, per capita rehabilitation costs, and the number of community rehabilitation centers. It outlines the current state of rehabilitation medicine in China and, through market analysis, forecasts its development trends in the coming years.China's rehabilitation medical care currently faces two major issues: insufficient supply and an imperfect system.1) Supply shortages primarily encompass four aspects:

Summary: This report presents data analysis on key indicators, including demographic foundations, chronic disease incidence, healthcare expenditure, per capita rehabilitation costs, and the number of community rehabilitation centers. It outlines the current state of rehabilitation medicine in China and, through market analysis, forecasts its development trends in the coming years.China's rehabilitation medical care currently faces two major issues: insufficient supply and an imperfect system.1) Supply shortages primarily encompass four aspects:

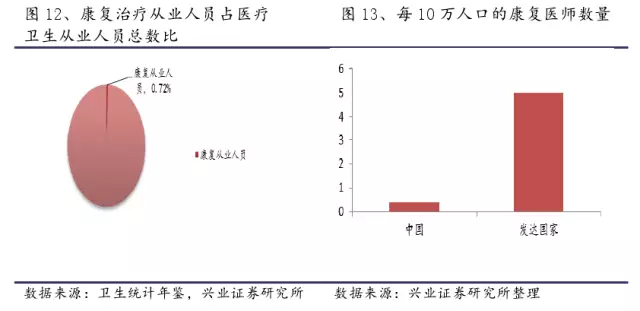

Shortage of Rehabilitation Professionals: Currently, the ratio of rehabilitation physicians to the general population in China is approximately 0.4 per 100,000 people, whereas in developed countries this figure reaches 5 per 100,000—a 12.5-fold difference. According to the requirements of the Ministry of Health, China’s secondary and tertiary hospitals collectively require 58,000 rehabilitation physicians and 116,000 therapists, while community-based comprehensive rehabilitation services need 902,000 personnel. This demand is more than ten times the current rehabilitation workforce, indicating a substantial talent gap.

Severe Shortage of Rehabilitation Medical Institutions: According to 2012 data from the National Health and Family Planning Commission, China currently has only 322 rehabilitation hospitals, with 206 in urban areas and 116 in rural areas. This means that more than half of the over 600 cities nationwide still lack specialized rehabilitation hospitals.

Low Proportion of Rehabilitation Medical Beds: According to data from the National Health and Family Planning Commission, in 2012, the number of rehabilitation medicine beds in China (including those in specialized rehabilitation hospitals and rehabilitation departments of general hospitals) accounted for only about 1.75% of the total number of beds in medical institutions, representing a very small proportion.

Insufficient and Outdated Rehabilitation Equipment: In mainland China, 51% of general hospitals in provincial capital cities have inadequate rehabilitation training spaces, 49.6% have outdated rehabilitation equipment, and there is a lack of modern rehabilitation management software systems, failing to meet the requirements for rehabilitation therapy and patient needs.

2) The imperfections in the system and mechanisms of rehabilitation medical services mainly include three aspects:

Untimely Early Intervention in Rehabilitation Medicine: So-called early rehabilitation refers to the initiation of functional rehabilitation 48 hours after disease onset, provided that the patient’s vital signs are stable and consciousness is clear. Early intervention in rehabilitation is a hallmark of rehabilitation departments in general hospitals, serving as the foundation for their survival and development, as well as a fundamental measure to ensure therapeutic efficacy. In the United States, emergency medical structures have been established to deliver early bedside rehabilitation services. However, due to insufficient rehabilitation awareness among clinicians in China and the influence of economic interests, rehabilitation consultation requests are often not issued in a timely manner. This causes patients to miss the optimal window for rehabilitative intervention, resulting in poor coordination between early rehabilitation training and clinical treatment. Furthermore, patients are not transferred promptly to rehabilitation departments after the acute phase has passed. Consequently, rehabilitation medicine departments primarily admit patients in the late stages of disease, thereby exacerbating the pressure on rehabilitation medical services.

Poor Two-Way Referral in Rehabilitation Medicine: Common manifestations include prolonged rehabilitation hospital stays and low bed turnover rates in general hospitals. Departments of Rehabilitation Medicine in comprehensive hospitals often operate under excessive load, making it difficult to transfer out hospitalized patients who remain longer than necessary, while a large number of early-stage patients fail to receive timely rehabilitation medical services.

High Costs of Rehabilitation Medical Services and the Need for Improved Health Insurance Policies: First, basic health insurance primarily covers pharmaceutical expenses, leaving patients to bear the cost of rehabilitation assistive devices, which constitute a significant proportion of total payments. Second, most rehabilitation therapy items are not included in the scope of basic medical insurance reimbursement, and certain payment mechanisms fail to align with the clinical needs of rehabilitation medicine. Third, restrictions on designated hospitals and settlement methods for insurance reimbursements hinder patient referrals. Fourth, reimbursement policies, average length of stay, and per-patient costs for specialized rehabilitation hospitals are implemented according to the standards for general hospitals, forcing many rehabilitation patients to be discharged before full recovery or to interrupt treatment and seek rehospitalization after a period.

Summary: The report analyzes the deficiencies in China’s rehabilitation healthcare sector across four dimensions: staffing, medical institutions, hospital beds, and medical equipment. It also addresses issues within the service mechanism, including untimely early intervention, inefficient two-way referral systems, persistently high costs, and insurance policy challenges. In doing so, it indirectly highlights key breakthrough points and critical links in the development of rehabilitation healthcare, offering profound guidance on how to effectively enter and navigate this market.

II. Current Status and Characteristics of Rehabilitation Medicine Development Abroad

The report provides a detailed explanation of the five major characteristics of rehabilitation medical service systems in developed countries:1) A rehabilitation medical service system with a clear structure and well-defined functionsA well-established three-tier rehabilitation medical network is a common model in the rehabilitation healthcare systems of developed countries and regions:

The three-tier rehabilitation medical service system in the United States is broadly categorized into Acute Rehabilitation facilities, Post-Acute Care (PAC) facilities, and Long-Term Care (LTC) facilities.

The UK’s three-tier rehabilitation medical service system comprises emergency hospitals (initial consultation), specialized rehabilitation hospitals funded through government procurement (inpatient rehabilitation), and community-based rehabilitation. A function evaluation–based rehabilitation pathway is established across these three tiers, thereby forming an integrated rehabilitation medical consortium with vertical connectivity.

In the Hong Kong Special Administrative Region of China, the rehabilitation medical service system is also divided into three tiers: 1) regional hospitals; 2) rehabilitation hospitals/centers; and 3) community-based rehabilitation services (day hospitals or specialist outpatient clinics). In addition, long-term care hospitals (including infirmaries and custodial care facilities) provide lifelong care services.

2) Evidence-based, smooth, and efficient rehabilitation medical service processesThe reference value of referral processes in developed countries mainly lies in two aspects:

2) Evidence-based, smooth, and efficient rehabilitation medical service processesThe reference value of referral processes in developed countries mainly lies in two aspects:

First is the proactive concept of front-loading rehabilitation. In the United States, early rehabilitation intervention is manifested as bedside rehabilitation during the acute phase, which is implemented by non-rehabilitation departments in acute care hospitals, providing patients with moderate-intensity rehabilitation therapy at an early stage. In the United Kingdom, clinical departments maintain close communication with rehabilitation departments to ensure that the latter are promptly informed of patients’ conditions, thereby facilitating early initiation of rehabilitation treatment.

Second, streamlined triage and referral pathways. In the United States, upon admission of patients in the acute phase, attending physicians initiate rehabilitation treatment based on assessments using standardized functional independence measures and the patient’s tolerance level. Once the patient’s condition stabilizes, they are promptly triaged and referred to acute rehabilitation units, subacute rehabilitation wards, specialized skilled nursing facilities, or long-term care institutions. Patients who can recover without inpatient rehabilitation services may also be discharged as soon as possible to home- and community-based settings.

3) A standards-based, function-oriented health insurance payment systemThe development and improvement of the U.S. rehabilitation medical service system are inseparable from the guiding role of the health insurance payment system. The U.S. health insurance payment system is a prospective payment system based on the Uniform Data System for Medical Rehabilitation (UDSMR), using the Function Independence Measure (FIM) as an assessment tool, and relying on a series of FIM-Function Related Groups (FIM-FRGs). The FIM-FRGs offer two key insights:

3) A standards-based, function-oriented health insurance payment systemThe development and improvement of the U.S. rehabilitation medical service system are inseparable from the guiding role of the health insurance payment system. The U.S. health insurance payment system is a prospective payment system based on the Uniform Data System for Medical Rehabilitation (UDSMR), using the Function Independence Measure (FIM) as an assessment tool, and relying on a series of FIM-Function Related Groups (FIM-FRGs). The FIM-FRGs offer two key insights:

First, scientifically established health insurance payment standards. FRGs categorize patients based on standardized criteria, then assess the level of functional impairment, age, and comorbidity severity for each group using independent functional assessment scales, and finally calculate the standard rehabilitation costs.

Second, reimbursement is contingent upon tangible functional improvements in patients. This incentivizes hospitals to prioritize functional recovery, thereby guiding the development and refinement of rehabilitation medical institutions to meet patients’ diverse needs across varying levels of care and treatment stages, and facilitating timely, proactive, and seamless patient referrals.

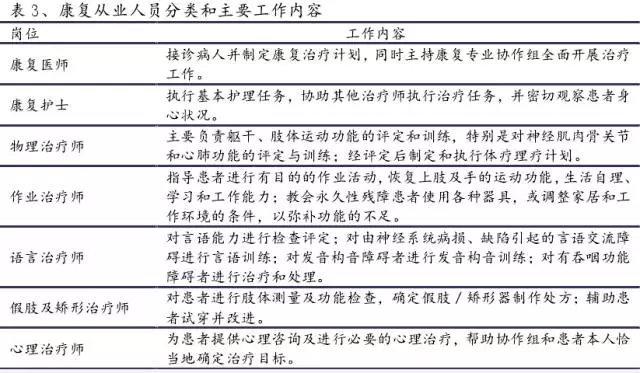

4) Rehabilitation Medical Service Team Centered on Rehabilitation PhysiciansIn regions with well-developed rehabilitation medical services, the basic unit of service delivery is a multidisciplinary rehabilitation team characterized by interprofessional collaboration:

The rehabilitation medical service team in the United States consists of physiatrists (PD), physical therapists (PT), occupational therapists (OT), speech-language pathologists (ST), swallowing therapists, psychotherapists, social workers, and nurses. As the central leader, the physiatrist (PD) is responsible for coordinating the entire team, developing treatment plans, and ensuring their implementation.

In the UK, even the most basic community-based rehabilitation is delivered by multidisciplinary teams. The POT model, centered on a community rehabilitation manager and comprising health, nursing, and social care professionals, provides specialized rehabilitation services for patients with residual impairments following physical or neurological conditions.

5) Prioritize the collaborative synergy between communities and non-governmental organizationsSocial workers are often seen in well-established rehabilitation medical service teams:

In Hong Kong, volunteerism is highly prevalent; in 1997 alone, over 2,000 patients participated in self-help groups, while more than 100 professionals and nearly 600 members of the general public served as volunteers.

In the United States, in addition to specialized rehabilitation physicians, a social worker is typically assigned to rehabilitation medicine wards to handle post-discharge matters for patients. If a patient requires transfer to a rehabilitation center after discharge, the social worker facilitates timely coordination.

In the UK POT team, social workers or discharge coordinators also play a key role.

Summary: The above report summarizes the five key priorities of rehabilitation medical service systems in developed countries such as the United States and the United Kingdom, offering valuable references for the development of China’s rehabilitation healthcare sector. How to develop a distinct model tailored to China’s context—by building upon the experiences of developed nations, fostering collaborative efforts, and integrating resources—is a critical issue that the entire industry must contemplate.

III. Analysis of the Development Trends of China’s Rehabilitation Medical Industry from the Perspectives of Policy, Capital, and Technology

1) National policies have significantly increased support for rehabilitation medicineIn recent years, national policies such as tiered diagnosis and treatment and medical insurance have significantly strengthened their support for rehabilitation medicine. In 2009, the central government’s landmark healthcare reform document, “Opinions of the Central Committee of the Communist Party of China and the State Council on Deepening the Reform of the Medical and Healthcare System,” explicitly stated that China’s healthcare system should emphasize the “integration of prevention, treatment, and rehabilitation.” In 2011, the Ministry of Health’s document, “Notice on Launching Pilot Programs to Establish and Improve the Rehabilitation Medical Service System,” further specified the establishment of a three-tiered rehabilitation medical service system under the tiered diagnosis and treatment framework (acute phase: general hospitals; rehabilitation phase: rehabilitation hospitals; long-term follow-up phase: community hospitals).

In 2010, the Ministry of Health’s document “Notice on Including Certain Medical Rehabilitation Services in the Scope of Basic Medical Insurance Coverage” explicitly included nine major rehabilitation treatment services within the scope of medical insurance reimbursement.

In 2010, the Ministry of Health’s document “Notice on Including Certain Medical Rehabilitation Services in the Scope of Basic Medical Insurance Coverage” explicitly included nine major rehabilitation treatment services within the scope of medical insurance reimbursement.

2) Introducing Social Capital: Great Potential in the Rehabilitation Medical Industry

2) Introducing Social Capital: Great Potential in the Rehabilitation Medical Industry

At the national level, there is encouragement for social capital to invest in healthcare. Considering private capital’s preference for addressing gaps in the medical system and its advantage in establishing specialized hospitals, the rehabilitation medicine sector is poised to witness a surge in investment. With increasing policy support from the government, rehabilitation medicine has gradually emerged as a new growth frontier in healthcare services.

Social capital invests in rehabilitation healthcare through flexible and diverse approaches, primarily including establishing new facilities, acquiring existing ones, and entrusting the management of rehabilitation hospitals. Among these, collaboration between social capital and public hospitals to jointly establish rehabilitation hospitals has emerged as the mainstream win-win model. This co-construction model requires lower investment compared to building new general hospitals, shortens the payback period, and offers a high cost-performance ratio.

Rehabilitation hospitals have become favored by social capital due to their unique advantages. Unlike general hospitals, which demand exceptionally high standards across all operational elements, rehabilitation hospitals offer benefits such as lower talent requirements, strong profitability, shorter payback periods, high standardization, and ease of replication and expansion. Meanwhile, integrating rehabilitation hospitals with public hospitals helps alleviate the persistent challenges of difficult and costly access to care within the public healthcare system, thereby creating favorable opportunities for private investment.

3) Technological Advancements Are the Accelerator for the Development of the Rehabilitation Medical IndustryRehabilitation Robots

China has a large base of individuals with physical disabilities, and the number continues to rise. According to the total population from the Sixth National Population Census and the Second National Sample Survey on Persons with Disabilities, the total number of persons with various types of disabilities in China reached 85.02 million by the end of 2010, accounting for approximately 6.2% of the national population. Among them, 24.72 million had physical disabilities, representing 29.07% of the total disabled population—the largest proportion among all disability categories.

There is an insufficient supply of rehabilitation training services for individuals with physical disabilities, resulting in a significant gap between service availability and patient needs. According to statistics from the China Disabled Persons’ Federation, by the end of 2014, there were 6,914 rehabilitation institutions nationwide, of which 2,181 provided rehabilitation training for physical disabilities. A total of 367,000 individuals with physical disabilities received rehabilitation training across China. However, given that the population of individuals with physical disabilities in China exceeds 24 million, there remains a substantial shortfall in the supply of rehabilitation equipment relative to clinical demand. Traditional manual therapy or simple medical devices can no longer meet patients’ rehabilitation needs, thereby driving increased demand for limb rehabilitation devices such as rehabilitation robots. Rehabilitation robots can reduce the need for human caregiving assistance while more effectively facilitating patient recovery. More importantly, demand for medical rehabilitation robots is relatively inelastic among patients, the elderly, and young children—collectively referred to as the “vulnerable populations”—indicating promising future market potential in this segment.

Brain-Computer Interface (BCI) Technology

Brain-Computer Interface (BCI) Technology

Since Berger and colleagues proposed the concept of “reading thoughts” in 1929, brain–computer interface (BCI) technology has advanced rapidly in recent decades, driven by progress in brain signal research, growing recognition of the spatiotemporal ubiquity of neuroplasticity, developments in real-time acquisition and analysis systems for brain signals, and increasing societal demand.

A Brain-Computer Interface (BCI) is a computer system that enables interaction between humans and the external environment, thereby displaying or executing desired behaviors, without the involvement of normal efferent pathways such as peripheral nerves and muscles. In a sense, BCI serves as a rehabilitation training device applicable to the rehabilitation process of various diseases. It facilitates recovery primarily through two mechanisms: first, by substituting multiple functions for severely paralyzed patients through interaction with the environment; and second, by promoting neuroplasticity to achieve functional compensation, ultimately reducing disability and improving patients' quality of life.

The main operational steps of brain-computer interfaces are: 1) Signal Acquisition: Acquiring signals and removing noise, with the most reliable method currently being the collection of human electroencephalogram (EEG) signals; 2) Signal Processing: Converting signals into a specific format; 3) Feature Extraction and Classification: Identifying specific signals, which is the most difficult and challenging step; 4) Control Interface: Translating relevant features into commands and operations.

Big Data and Virtual Reality (VR) Technology

Big Data and Virtual Reality (VR) Technology

The Precision Rehabilitation Medical System integrates modern information science technologies—such as the Internet of Medical Things (IoMT), telemedicine, and big data-driven intelligent decision engines—with intelligent network platforms, building upon traditional medical concepts. It utilizes embedded wearable devices to sense and monitor human vital signs, collect and provide feedback on rehabilitation-related data, and issue medical intervention instructions and treatment plans. During the diagnosis and treatment process, the system employs a big data intelligent decision engine to analyze, mine, mathematically simulate, and perform image analysis, thereby acquiring and transmitting information for diagnostic purposes, assessing disease risks, conducting intelligent judgments and decision-making, and presenting and providing intervention measures. Digital precision rehabilitation medicine is an expert system established through high-tech means, representing an extension and amplification of human wisdom in the field of medicine via machines and artificial intelligence.

Virtual reality (VR) is a technology that generates virtual effects targeting human sensory perception. It has been widely applied in the field of rehabilitation medicine, demonstrating significant therapeutic efficacy in cognitive rehabilitation for conditions such as attention deficit, spatial perception disorders, and memory impairment; in the rehabilitation of patients with emotional disorders—including anxiety, depression, and phobias—as well as other mental illnesses; and in motor rehabilitation for impairments such as poor balance and coordination.

Steady Progress in the Informatization of Rehabilitation Medicine

Steady Progress in the Informatization of Rehabilitation Medicine

With the advancement of internet technology, the referral process for rehabilitation patients from clinical care to rehabilitation will become fully digitalized, enabling information sharing among various medical institutions and facilitating seamless referrals across tertiary rehabilitation hospitals. The Tier-3 Rehabilitation Network Construction Project centers on modern rehabilitation technologies and integrates rehabilitation medical resources through a physical extension encompassing tertiary hospitals, secondary hospitals, community health service centers, and community health service stations. Its objective is to establish a digital diagnosis and treatment system for rehabilitation within healthcare institutions at all levels in the region, develop a unified rehabilitation data platform, achieve digitization and sharing of rehabilitation information, and create an ecosystem where patients can access convenient, high-quality remote rehabilitation services, including diagnosis, treatment, referrals, and education.

On April 27, 2015, the signing and launch ceremony for China’s first digital rehabilitation hospital was held at the Sichuan Provincial Rehabilitation Hospital (Sichuan Bayi Rehabilitation Center), thereby initiating the construction of a three-tier rehabilitation network covering the entire province of Sichuan. Subsequently, other provinces, municipalities, and regions, including Shanghai, also entered the initial phase of actively developing their own three-tier rehabilitation networks.

Summary: The report outlines policies, capital investment, and new technologies in rehabilitation medicine, reflecting an increasingly clear trajectory for its future development. Driven by the combined forces of policy support, capital influx, and technological advancement, China’s rehabilitation medical industry, with a market value in the hundreds of billions, is poised for takeoff, offering broad prospects.

Summary: The report outlines policies, capital investment, and new technologies in rehabilitation medicine, reflecting an increasingly clear trajectory for its future development. Driven by the combined forces of policy support, capital influx, and technological advancement, China’s rehabilitation medical industry, with a market value in the hundreds of billions, is poised for takeoff, offering broad prospects.

IV. Overview of Listed Companies at Home and Abroad

1) Overseas Listed CompaniesUpstream Medical DevicesReWalk RoboticsReWalk Robotics, an Israeli provider of exoskeleton systems, went public on the NASDAQ in September 2014. The company manufactures wearable powered exoskeleton devices that help individuals with paraplegia regain mobility. ReWalk received CE marking for the European market in 2012, and in June 2014, its exoskeleton product became the first and only exoskeleton to receive approval from the U.S. Food and Drug Administration (FDA).The company offers two products: ReWalk Personal and ReWalk Rehabilitation. The former is primarily designed for use in home, work, or social settings, enabling users to stand, walk, and climb stairs through sensors and monitors. The latter is intended for clinical rehabilitation, providing physical therapy for paralyzed patients by alleviating limb pain and muscle spasticity caused by paralysis, assisting bowel function, and accelerating metabolism. Stroke and cerebral palsy patients are also target populations for ReWalk’s future expansion.ReWalk products are priced between $69,500 and $85,000. This price point has somewhat limited acceptance among patients and the elderly, as well as the size of the addressable market. However, with economies of scale driving down prices, along with increased government subsidies and broader insurance coverage, ReWalk is likely to gain wider acceptance among patients and the elderly in the future. Ekso Bionics Holdings, Inc.Ekso Bionics was listed on the NASDAQ OTC market in the United States in 2014 and currently has a market capitalization of $94.7 million. Previously known as Berkeley Bionics, the company is engaged in the design and manufacture of exoskeletons aimed at enhancing human performance. It has collaborated with the military for over a decade and began researching solutions to assist individuals with lower-body paralysis in 2012. The exoskeletons or wearable robotic devices designed, developed, and marketed by the company have a wide range of applications across the medical, military, and industrial sectors. Its bionic robotic exoskeletons for rehabilitation are targeted at patients who have suffered strokes, sustained spinal cord injuries, or have other neurological disorders. Ekso’s devices are priced at over $100,000, and the company plans to further reduce prices in the future.

Ekso Bionics Holdings, Inc.Ekso Bionics was listed on the NASDAQ OTC market in the United States in 2014 and currently has a market capitalization of $94.7 million. Previously known as Berkeley Bionics, the company is engaged in the design and manufacture of exoskeletons aimed at enhancing human performance. It has collaborated with the military for over a decade and began researching solutions to assist individuals with lower-body paralysis in 2012. The exoskeletons or wearable robotic devices designed, developed, and marketed by the company have a wide range of applications across the medical, military, and industrial sectors. Its bionic robotic exoskeletons for rehabilitation are targeted at patients who have suffered strokes, sustained spinal cord injuries, or have other neurological disorders. Ekso’s devices are priced at over $100,000, and the company plans to further reduce prices in the future. Downstream Medical InstitutionsHealthSouth CorporationThe company was founded in Birmingham, Alabama, in 1984, had its initial public offering (IPO) on the NASDAQ in 1986, and transferred its listing to the New York Stock Exchange (NYSE) in 1988. As the largest chain of rehabilitation hospitals in the United States, the company employs 34,700 people and provides post-acute rehabilitation care services across 34 U.S. states, with a current market capitalization of $3.2 billion. In recent years, the company has continued to acquire rehabilitation hospitals while expanding into related business areas such as outpatient rehabilitation, home health care, and hospice care. Specifically, the company acquired Walton Rehabilitation Hospital in 2013; in December 2014, it acquired Encompass, the fourth-largest home health care provider in the United States, thereby entering the home health care and hospice care sectors; and in October 2015, it acquired Reliant, gaining ownership of 11 independently operated rehabilitation hospitals (with a total of 902 beds located in Texas, Massachusetts, and Ohio). As the company’s scale has continued to expand, its stock price has surged sixfold over the past four years.

Downstream Medical InstitutionsHealthSouth CorporationThe company was founded in Birmingham, Alabama, in 1984, had its initial public offering (IPO) on the NASDAQ in 1986, and transferred its listing to the New York Stock Exchange (NYSE) in 1988. As the largest chain of rehabilitation hospitals in the United States, the company employs 34,700 people and provides post-acute rehabilitation care services across 34 U.S. states, with a current market capitalization of $3.2 billion. In recent years, the company has continued to acquire rehabilitation hospitals while expanding into related business areas such as outpatient rehabilitation, home health care, and hospice care. Specifically, the company acquired Walton Rehabilitation Hospital in 2013; in December 2014, it acquired Encompass, the fourth-largest home health care provider in the United States, thereby entering the home health care and hospice care sectors; and in October 2015, it acquired Reliant, gaining ownership of 11 independently operated rehabilitation hospitals (with a total of 902 beds located in Texas, Massachusetts, and Ohio). As the company’s scale has continued to expand, its stock price has surged sixfold over the past four years. The company’s business is primarily divided into two segments: Inpatient Rehabilitation and Home Health and Hospice. The Inpatient Rehabilitation segment further comprises inpatient and outpatient rehabilitation services. According to the 2015 annual report, the company generated $3.12 billion in revenue in 2015, representing a 31.2% year-over-year increase, with a net profit of $180 million. Inpatient services accounted for the largest share of revenue at 81%, followed by home health care at 15%, while outpatient rehabilitation and hospice care contributed 3% and 1%, respectively.

The company’s business is primarily divided into two segments: Inpatient Rehabilitation and Home Health and Hospice. The Inpatient Rehabilitation segment further comprises inpatient and outpatient rehabilitation services. According to the 2015 annual report, the company generated $3.12 billion in revenue in 2015, representing a 31.2% year-over-year increase, with a net profit of $180 million. Inpatient services accounted for the largest share of revenue at 81%, followed by home health care at 15%, while outpatient rehabilitation and hospice care contributed 3% and 1%, respectively. In the area of inpatient rehabilitation, the company currently operates 121 hospitals with a total of 8,404 beds. In 2015, it recorded approximately 580,000 outpatient visits and discharged around 150,000 cured patients. The company’s rehabilitation hospitals provide comprehensive and professional diagnostic services, as well as high-quality, cost-effective nursing care. Ninety-two percent of the hospital’s patients are referred from acute-care hospitals, with the majority requiring inpatient rehabilitation due to impaired mobility caused by conditions such as stroke, hip fractures, or neurological disorders. The rehabilitation team consists of physiatrists, nurses, and skilled physical therapists and speech-language pathologists, who help patients restore physiological and cognitive functions.In the fields of home healthcare and hospice care, the company currently maintains 186 home health locations and 27 hospice facilities. Encompass, acquired by the company at the end of 2014, is the fourth-largest Medicare-certified home healthcare provider in the United States. Following the acquisition, the company gradually transferred the majority of its previously operated home healthcare agencies to Encompass. As of November 2015, 44 home health agencies and three hospice facilities across seven states had been transitioned to operate under Encompass. Encompass’s home health and hospice facilities are widely distributed across 23 U.S. states. Patients admitted to its home health agencies are typically referred after acute treatment or inpatient rehabilitation, while its hospice facilities primarily serve terminally ill patients and their families, providing pain relief, symptom management, and emotional support.

In the area of inpatient rehabilitation, the company currently operates 121 hospitals with a total of 8,404 beds. In 2015, it recorded approximately 580,000 outpatient visits and discharged around 150,000 cured patients. The company’s rehabilitation hospitals provide comprehensive and professional diagnostic services, as well as high-quality, cost-effective nursing care. Ninety-two percent of the hospital’s patients are referred from acute-care hospitals, with the majority requiring inpatient rehabilitation due to impaired mobility caused by conditions such as stroke, hip fractures, or neurological disorders. The rehabilitation team consists of physiatrists, nurses, and skilled physical therapists and speech-language pathologists, who help patients restore physiological and cognitive functions.In the fields of home healthcare and hospice care, the company currently maintains 186 home health locations and 27 hospice facilities. Encompass, acquired by the company at the end of 2014, is the fourth-largest Medicare-certified home healthcare provider in the United States. Following the acquisition, the company gradually transferred the majority of its previously operated home healthcare agencies to Encompass. As of November 2015, 44 home health agencies and three hospice facilities across seven states had been transitioned to operate under Encompass. Encompass’s home health and hospice facilities are widely distributed across 23 U.S. states. Patients admitted to its home health agencies are typically referred after acute treatment or inpatient rehabilitation, while its hospice facilities primarily serve terminally ill patients and their families, providing pain relief, symptom management, and emotional support. 2) Relevant Listed Companies in ChinaUpstream Medical Devices**Tofflon**On May 27, 2015, the company announced that it would invest RMB 35 million to subscribe for 4.375 million shares of Shanghai Nuocheng Electric Co., Ltd., accounting for 14.77% of Nuocheng Electric’s share capital, thereby becoming its second-largest shareholder. Nuocheng Electric projected net profits of RMB 9 million, RMB 15 million, and RMB 23 million for the years 2015, 2016, and 2017, respectively.Established in 1997, Nuocheng Electric’s main products include electroencephalographs (EEG), electromyographs (EMG), evoked potential instruments, and intraoperative neuromonitoring systems, among other electrophysiological and rehabilitation series products. It is a “little giant” in the niche sector of electrophysiology and rehabilitation technology. While electrophysiological equipment is standard in hospitals, its development had been relatively slow. However, with the integration of sensors, data transmission and analysis technologies, and internet technology, modalities such as electrocardiography (ECG), EEG, and EMG have garnered increased attention, and the application of electrophysiological rehabilitation has expanded significantly.Leveraging its technical advantages in hardware equipment and software development for electrophysiological rehabilitation systems, Nuocheng Electric has led or participated in the construction of tertiary rehabilitation network projects in certain areas of Shanghai. Currently, the Xuhui District Tertiary Rehabilitation Network Construction Project, jointly promoted and implemented by Nuocheng Electric and Shanghai Sixth People’s Hospital, has completed the establishment of a tertiary rehabilitation network. This network uses Shanghai Sixth People’s Hospital, the Xuhui District Health and Family Planning Commission, two secondary hospitals in Xuhui District, and ten community hospitals as demonstration sites.**Maidong Medical**The company was listed on the National Equities Exchange and Quotations (NEEQ) on November 12, 2015. In 2014, the company reported operating revenue of RMB 10.599 million and net profit attributable to shareholders of RMB 514,000. Its main products for sale include ventilators, rehabilitation products, and nursing care products, which are primarily marketed to secondary distributors and healthcare institutions such as hospitals and nursing homes. Rehabilitation products mainly include motion feedback training systems and cervical/lumbar traction devices. The motion feedback training system is a series of products launched by MediTouch from Israel, designed for active rehabilitation exercise training and functional assessment of multiple joints and the trunk. The product line includes HandTutor (finger and wrist trainer), ArmTutor (elbow and shoulder trainer), LegTutor (knee and hip trainer), and 3D-Tutor (full-body multi-joint trainer). B'POSTURE™ by Qudubang is a leading health product in the B+ series from Bachmann Health Products Co., Ltd. It is a medical device designed to address and treat various spinal pathologies caused by spinal imbalance and instability, helping to restore the physiological curvature of the spine.Downstream Medical Institutions**Hunan Development**The company has adopted a cooperation model with Xiangya Hospital that involves no equity investment or shareholding. By branding the Bo’ai Rehabilitation Hospital under the “Xiangya” name, it leverages Xiangya Hospital’s strong brand influence and medical expertise for comprehensive collaboration. This arrangement gives Xiangya Bo’ai Hospital an advantage in accessing patient resources from Xiangya Hospital. Under the premise of shared referral resources, Xiangya Bo’ai Rehabilitation Hospital pays Xiangya Hospital fees for brand usage, technology licensing, and multi-site practice privileges. The two parties cooperate through fixed fees for brand naming and technical support, with further negotiations on the cooperation model to take place once the number of beds exceeds a certain threshold. The rehabilitation hospital serves 8,600 patient visits annually, with approximately one-third of these patients initially estimated to be referrals from general hospitals such as Xiangya.By connecting with general hospitals to secure a steady patient source, the rehabilitation hospital ensures its survival during the start-up phase, which is crucial. Currently, part of the property used by the operating Xiangya Bo’ai Rehabilitation Hospital is leased, with a total investment of RMB 130 million. Based on the committed net profit, the initial investment cost is low, and the payback period is short. Changsha Bo’ai Rehabilitation Hospital is a Grade III specialized rehabilitation hospital with 420 beds. It officially began operations in the second half of 2012, achieved over RMB 100 million in revenue and reached break-even by 2014. Dean Zhou Jianglin committed to net profits of no less than RMB 16 million, RMB 18 million, and RMB 20 million for 2015, 2016, and 2017, respectively. Dean Zhou Jianglin’s resources in the rehabilitation industry, the mature model of cooperation with general hospitals, and the background resources of state-controlled holdings constitute the unique advantages of the “Xiangya Model,” serving as a strong guarantee for the successful promotion of its chain layout across Hunan Province. Rehabilitation hospitals in Xiangxi and Changde are expected to open within the year, with plans to complete coverage at the prefecture-level city level in Hunan within three to five years.**Aoyang Technology**In November 2015, the company released a private placement plan to raise a total of RMB 960 million for project investments, with the actual controller subscribing to RMB 100 million. Of this amount, RMB 260 million will be used for the construction of Gangcheng Rehabilitation Hospital and a chain of rehabilitation hospitals. Gangcheng Rehabilitation Hospital will construct a 10-story building according to Grade II rehabilitation hospital standards, housing departments for orthopedic and joint rehabilitation, neurological stroke rehabilitation, spinal cord injury rehabilitation, among others. Its clinical services cover post-stroke sequelae, post-operative care for traumatic brain injury and brain tumors, various orthopedic surgeries, multiple trauma, childhood disabilities, neck/shoulder/waist/leg pain, myasthenia gravis, Parkinson’s disease, and chronic internal medicine conditions in the elderly, catering to all age groups and specialties. The planned approved bed capacity is 300, with a total construction area of approximately 20,000 square meters. Upon completion, the project will become one of the most professional specialized rehabilitation hospitals in East China.The rehabilitation hospital chain project leverages the company’s leading advantages in operation, technology, and talent within rehabilitation healthcare. It selects economically developed areas lacking professional rehabilitation hospitals in East China to co-establish rehabilitation medical departments with local hospitals. In this model, partner hospitals provide facilities and medical staff, while the company assists in department management through equipment support, technical support, trusteeship, and other cooperative modes. Revenue is distributed between the parties according to agreed proportions.Over the next three years, the company plans to cooperate with 30–50 hospitals to initially establish a rehabilitation medical network covering East China. The total planned investment for the rehabilitation hospital chain is RMB 120 million, funding 30 chain operation centers with an average investment of RMB 4 million per center, primarily for the purchase of rehabilitation treatment equipment. The annual revenue per bed is estimated at RMB 140,000–150,000. As this is an asset-light investment model, both gross and net profit margins are expected to be high, with gross margins reaching up to approximately 40% and net margins up to approximately 20%. Based on the company’s current assumption of 50 beds per chain center, totaling 1,500 beds, the project is expected to generate an annual net profit of RMB 42–45 million for the company.**Hejia Shares**In April 2015, the company signed a “Strategic Cooperation Agreement” with Zhengzhou People’s Hospital Medical Management Co., Ltd. regarding the investment and establishment of for-profit rehabilitation hospitals, with Zhengzhou Medical Management Company holding a 20% equity stake in the rehabilitation hospitals. Both parties will use the invested rehabilitation hospitals as cooperation bases for long-term, in-depth collaboration in hospital management, talent training, and technical exchange and development. The key departments of the rehabilitation hospitals are Neurological Rehabilitation and Orthopedic Trauma Rehabilitation, aiming to position them as leaders in high-end chain rehabilitation healthcare.**Huabang Health**The company’s layout in the medical services sector is based on rehabilitation healthcare, developing towards specialized rehabilitation. In July 2015, it acquired Rhein Hospital in Germany. This acquisition introduces advanced German rehabilitation concepts and experience to the domestic market, accumulating experience for the company’s expansion in the rehabilitation field. Furthermore, it may replicate the Rhein Hospital model in first-tier cities to establish high-end rehabilitation centers, meeting the growing rehabilitation demands of the domestic high-net-worth population.**Guolong Medical**The company was listed on the New Third Board in November 2014 and operates as a general hospital specializing in orthopedics and obstetrics/gynecology. Currently, Guolong Medical has established branch hospitals including Yinchuan Guolong Hospital, subsidiary Wuzhong Guolong Hospital, and Shanghai Guolong Hospital. In April 2015, the company announced the introduction of relevant domestic and foreign institutional investors through capital increase and share expansion, including PreferUS Healthcare and Legend Holdings, adding the dual wings of “capital + technology” to its development. Legend Holdings has long been renowned in China’s capital circle, owning two venture capital firms: Hony Capital and Joy Capital. Additionally, the introduced technical partner, PreferUS, is a well-known American rehabilitation medical institution with over 100 famous American doctors spanning orthopedics, minimally invasive surgery, spine, and rehabilitation disciplines, with successful international outpatient clinics located around the world.

2) Relevant Listed Companies in ChinaUpstream Medical Devices**Tofflon**On May 27, 2015, the company announced that it would invest RMB 35 million to subscribe for 4.375 million shares of Shanghai Nuocheng Electric Co., Ltd., accounting for 14.77% of Nuocheng Electric’s share capital, thereby becoming its second-largest shareholder. Nuocheng Electric projected net profits of RMB 9 million, RMB 15 million, and RMB 23 million for the years 2015, 2016, and 2017, respectively.Established in 1997, Nuocheng Electric’s main products include electroencephalographs (EEG), electromyographs (EMG), evoked potential instruments, and intraoperative neuromonitoring systems, among other electrophysiological and rehabilitation series products. It is a “little giant” in the niche sector of electrophysiology and rehabilitation technology. While electrophysiological equipment is standard in hospitals, its development had been relatively slow. However, with the integration of sensors, data transmission and analysis technologies, and internet technology, modalities such as electrocardiography (ECG), EEG, and EMG have garnered increased attention, and the application of electrophysiological rehabilitation has expanded significantly.Leveraging its technical advantages in hardware equipment and software development for electrophysiological rehabilitation systems, Nuocheng Electric has led or participated in the construction of tertiary rehabilitation network projects in certain areas of Shanghai. Currently, the Xuhui District Tertiary Rehabilitation Network Construction Project, jointly promoted and implemented by Nuocheng Electric and Shanghai Sixth People’s Hospital, has completed the establishment of a tertiary rehabilitation network. This network uses Shanghai Sixth People’s Hospital, the Xuhui District Health and Family Planning Commission, two secondary hospitals in Xuhui District, and ten community hospitals as demonstration sites.**Maidong Medical**The company was listed on the National Equities Exchange and Quotations (NEEQ) on November 12, 2015. In 2014, the company reported operating revenue of RMB 10.599 million and net profit attributable to shareholders of RMB 514,000. Its main products for sale include ventilators, rehabilitation products, and nursing care products, which are primarily marketed to secondary distributors and healthcare institutions such as hospitals and nursing homes. Rehabilitation products mainly include motion feedback training systems and cervical/lumbar traction devices. The motion feedback training system is a series of products launched by MediTouch from Israel, designed for active rehabilitation exercise training and functional assessment of multiple joints and the trunk. The product line includes HandTutor (finger and wrist trainer), ArmTutor (elbow and shoulder trainer), LegTutor (knee and hip trainer), and 3D-Tutor (full-body multi-joint trainer). B'POSTURE™ by Qudubang is a leading health product in the B+ series from Bachmann Health Products Co., Ltd. It is a medical device designed to address and treat various spinal pathologies caused by spinal imbalance and instability, helping to restore the physiological curvature of the spine.Downstream Medical Institutions**Hunan Development**The company has adopted a cooperation model with Xiangya Hospital that involves no equity investment or shareholding. By branding the Bo’ai Rehabilitation Hospital under the “Xiangya” name, it leverages Xiangya Hospital’s strong brand influence and medical expertise for comprehensive collaboration. This arrangement gives Xiangya Bo’ai Hospital an advantage in accessing patient resources from Xiangya Hospital. Under the premise of shared referral resources, Xiangya Bo’ai Rehabilitation Hospital pays Xiangya Hospital fees for brand usage, technology licensing, and multi-site practice privileges. The two parties cooperate through fixed fees for brand naming and technical support, with further negotiations on the cooperation model to take place once the number of beds exceeds a certain threshold. The rehabilitation hospital serves 8,600 patient visits annually, with approximately one-third of these patients initially estimated to be referrals from general hospitals such as Xiangya.By connecting with general hospitals to secure a steady patient source, the rehabilitation hospital ensures its survival during the start-up phase, which is crucial. Currently, part of the property used by the operating Xiangya Bo’ai Rehabilitation Hospital is leased, with a total investment of RMB 130 million. Based on the committed net profit, the initial investment cost is low, and the payback period is short. Changsha Bo’ai Rehabilitation Hospital is a Grade III specialized rehabilitation hospital with 420 beds. It officially began operations in the second half of 2012, achieved over RMB 100 million in revenue and reached break-even by 2014. Dean Zhou Jianglin committed to net profits of no less than RMB 16 million, RMB 18 million, and RMB 20 million for 2015, 2016, and 2017, respectively. Dean Zhou Jianglin’s resources in the rehabilitation industry, the mature model of cooperation with general hospitals, and the background resources of state-controlled holdings constitute the unique advantages of the “Xiangya Model,” serving as a strong guarantee for the successful promotion of its chain layout across Hunan Province. Rehabilitation hospitals in Xiangxi and Changde are expected to open within the year, with plans to complete coverage at the prefecture-level city level in Hunan within three to five years.**Aoyang Technology**In November 2015, the company released a private placement plan to raise a total of RMB 960 million for project investments, with the actual controller subscribing to RMB 100 million. Of this amount, RMB 260 million will be used for the construction of Gangcheng Rehabilitation Hospital and a chain of rehabilitation hospitals. Gangcheng Rehabilitation Hospital will construct a 10-story building according to Grade II rehabilitation hospital standards, housing departments for orthopedic and joint rehabilitation, neurological stroke rehabilitation, spinal cord injury rehabilitation, among others. Its clinical services cover post-stroke sequelae, post-operative care for traumatic brain injury and brain tumors, various orthopedic surgeries, multiple trauma, childhood disabilities, neck/shoulder/waist/leg pain, myasthenia gravis, Parkinson’s disease, and chronic internal medicine conditions in the elderly, catering to all age groups and specialties. The planned approved bed capacity is 300, with a total construction area of approximately 20,000 square meters. Upon completion, the project will become one of the most professional specialized rehabilitation hospitals in East China.The rehabilitation hospital chain project leverages the company’s leading advantages in operation, technology, and talent within rehabilitation healthcare. It selects economically developed areas lacking professional rehabilitation hospitals in East China to co-establish rehabilitation medical departments with local hospitals. In this model, partner hospitals provide facilities and medical staff, while the company assists in department management through equipment support, technical support, trusteeship, and other cooperative modes. Revenue is distributed between the parties according to agreed proportions.Over the next three years, the company plans to cooperate with 30–50 hospitals to initially establish a rehabilitation medical network covering East China. The total planned investment for the rehabilitation hospital chain is RMB 120 million, funding 30 chain operation centers with an average investment of RMB 4 million per center, primarily for the purchase of rehabilitation treatment equipment. The annual revenue per bed is estimated at RMB 140,000–150,000. As this is an asset-light investment model, both gross and net profit margins are expected to be high, with gross margins reaching up to approximately 40% and net margins up to approximately 20%. Based on the company’s current assumption of 50 beds per chain center, totaling 1,500 beds, the project is expected to generate an annual net profit of RMB 42–45 million for the company.**Hejia Shares**In April 2015, the company signed a “Strategic Cooperation Agreement” with Zhengzhou People’s Hospital Medical Management Co., Ltd. regarding the investment and establishment of for-profit rehabilitation hospitals, with Zhengzhou Medical Management Company holding a 20% equity stake in the rehabilitation hospitals. Both parties will use the invested rehabilitation hospitals as cooperation bases for long-term, in-depth collaboration in hospital management, talent training, and technical exchange and development. The key departments of the rehabilitation hospitals are Neurological Rehabilitation and Orthopedic Trauma Rehabilitation, aiming to position them as leaders in high-end chain rehabilitation healthcare.**Huabang Health**The company’s layout in the medical services sector is based on rehabilitation healthcare, developing towards specialized rehabilitation. In July 2015, it acquired Rhein Hospital in Germany. This acquisition introduces advanced German rehabilitation concepts and experience to the domestic market, accumulating experience for the company’s expansion in the rehabilitation field. Furthermore, it may replicate the Rhein Hospital model in first-tier cities to establish high-end rehabilitation centers, meeting the growing rehabilitation demands of the domestic high-net-worth population.**Guolong Medical**The company was listed on the New Third Board in November 2014 and operates as a general hospital specializing in orthopedics and obstetrics/gynecology. Currently, Guolong Medical has established branch hospitals including Yinchuan Guolong Hospital, subsidiary Wuzhong Guolong Hospital, and Shanghai Guolong Hospital. In April 2015, the company announced the introduction of relevant domestic and foreign institutional investors through capital increase and share expansion, including PreferUS Healthcare and Legend Holdings, adding the dual wings of “capital + technology” to its development. Legend Holdings has long been renowned in China’s capital circle, owning two venture capital firms: Hony Capital and Joy Capital. Additionally, the introduced technical partner, PreferUS, is a well-known American rehabilitation medical institution with over 100 famous American doctors spanning orthopedics, minimally invasive surgery, spine, and rehabilitation disciplines, with successful international outpatient clinics located around the world.