Two-Decade Investment Trends in 17 U.S. Disease-Specific Therapeutic Areas (1999–2015)

This report is republished by VCBeat with authorization from Yuanxu Capital. The author is Zhang Xing, Partner at Yuanxu Investment (WeChat ID: AlwaysForTruth). Yuanxu Investment is dedicated to assisting Chinese investment firms and industrial capital in establishing their presence in the U.S. biopharmaceutical and healthcare sector.

Most new technology prototypes in the U.S. healthcare sector originate from research institutions, while the further development of these prototypes into medical products relies primarily on startups. Compared to the IT industry, healthcare startups are capital-intensive ventures; even at the seed stage, they require tens of millions of dollars in investment to get off the ground. Consequently, venture capital investment trends in the healthcare sector largely determine which new drugs and medical devices will emerge in the future market.

This article presents a statistical analysis of investment trends by U.S. venture capital firms across various disease areas from 1999 to 2015. Based on the organs affected by diseases, I have categorized venture capital investments into 17 distinct fields for individual analysis. Many companies develop products for multiple diseases simultaneously, and a single disease often affects multiple organs. Consequently, the same company may appear in the statistics for multiple disease categories. Diseases are classified according to the primary organ they affect.

Overall, venture capital investment is concentrated in five major disease areas: cardiovascular diseases, neurological disorders, immune system diseases (including tumor immunology), skeletal diseases, and endocrine/pancreatic diseases (such as diabetes). In recent years, orphan diseases (defined in China as conditions affecting fewer than 200,000 patients nationwide) have also become a hotspot for investment, driving funding into previously less popular areas such as hematologic disorders.

Cardiovascular Diseases. Cardiac disease treatment technologies have long been a key focus of healthcare venture capital investment. However, since 2008, venture capital funding for medical devices has declined significantly, leading to a corresponding decrease in total investment in the cardiology sector.

2. Neurological Disorders. Investment focuses on Alzheimer’s disease, Parkinson’s disease, and depression. Adjunctive therapies leveraging IT technologies, such as software and gaming, have also attracted significant investment.

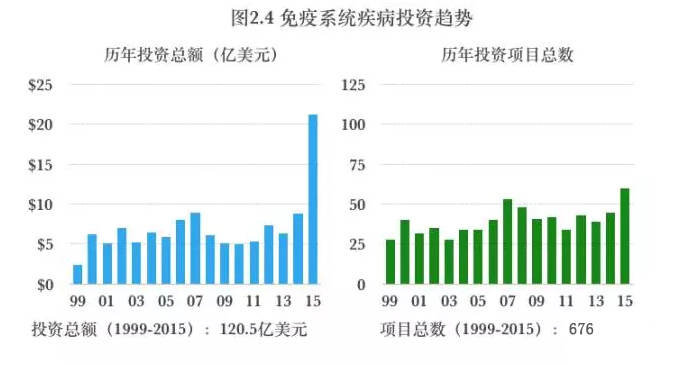

3. Immune System Diseases. Investment focuses on tumor immunology, inflammation, autoimmune disorders, and novel vaccines.

4. Skeletal System Disorders. Venture capital flooded into orthopedic surgical products between 2005 and 2007. After 2008, as the medical device sector cooled overall, venture capital investment in this area gradually declined.

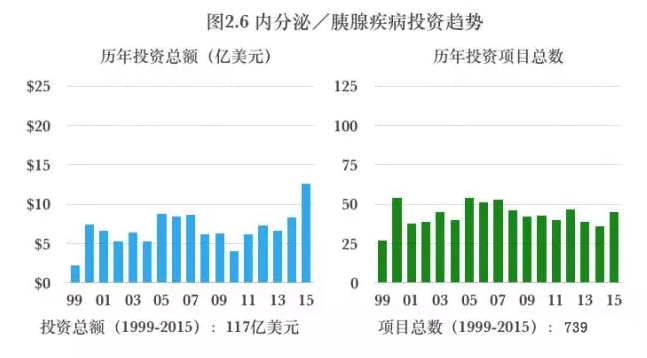

5. Endocrine/Pancreatic Diseases. Investment priorities focus on diabetes-related product technologies, particularly pharmaceuticals for type 2 diabetes. Cell therapies for type 1 diabetes are also a key area of investment interest.

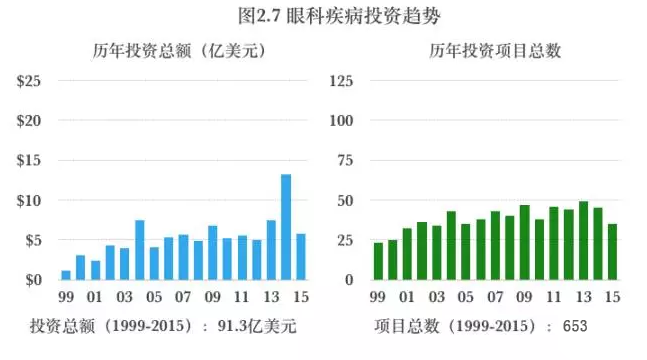

6. Ophthalmic Diseases. Investment in ophthalmic diseases peaked in 2013 and 2014, primarily focusing on areas such as glaucoma and macular degeneration. Starting in 2015, investment levels returned to the average. This shift was driven by two factors: first, investors adopted a wait-and-see approach; second, several ophthalmic pharmaceutical companies raised capital in the secondary market through initial public offerings (IPOs).

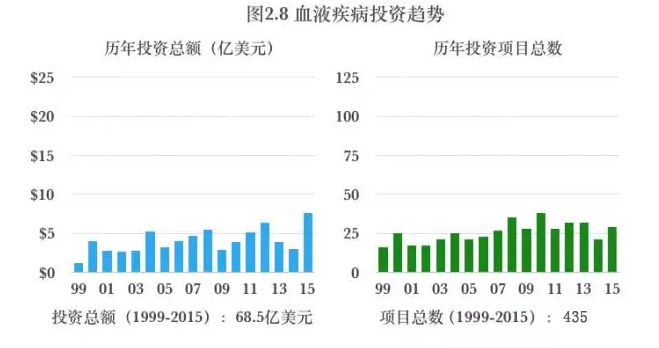

7. Blood Disorders. Orphan diseases have recently become a hot spot for venture capital investment. Against this backdrop, rare hematologic conditions such as hemophilia and paroxysmal nocturnal hemoglobinuria have attracted substantial venture capital funding.

8. Pulmonary Diseases. Medications and devices for asthma have long attracted venture capital investment. In recent years, genetic disorders that impair lung function, such as cystic fibrosis, have also begun to receive substantial venture capital funding.

9. Digestive System Diseases. Investment focus is on inflammatory bowel disease (such as Crohn's disease, ulcerative colitis, etc.), particularly oral medications.

10. Kidney Diseases. Key investment areas include kidney stones, chronic renal failure, acute kidney injury, and renal cell carcinoma.

11. Skin Diseases. Investment focus areas include skin cancer, acne, and aesthetic consumer products.

12. Gastric Diseases. Investment focus is on obesity-related product technologies, particularly products associated with weight loss.

13. Reproductive System Diseases. Investment focus is on drugs, devices, and testing methods for the prevention of preterm birth.

14. Muscular Diseases. Venture capital investment is primarily concentrated on orphan diseases within the spectrum of muscular disorders; additionally, investments targeting rehabilitation medicine are also gaining momentum.

15. Urological Diseases. Historically, urological diseases have attracted little venture capital investment. In recent years, venture capital has begun to focus on conditions such as bladder cancer and benign prostatic hyperplasia.

16. Otologic Diseases. In recent years, attention to otologic diseases has begun to rise, and drugs targeting hearing loss (such as tinnitus) have become a hot spot for investment.

17. Liver Disease. Venture capital investment in liver disease has fluctuated significantly, with non-alcoholic steatohepatitis (NASH)—a condition that can lead to cirrhosis and liver cancer—being the only area to enjoy sustained venture capital interest.

Venture capital investment enthusiasm for a particular disease is jointly influenced by both internal and external factors.

Internal Factors: Primarily basic research in academia. For instance, the role of the immune system in cancer development and treatment has been a focal point in academic circles in recent years, with various studies achieving breakthrough progress. This has attracted substantial venture capital investment to the field of tumor immunology.

External Factors: Primarily government regulatory policies and market entry barriers (such as insurers’ coverage policies). For instance, venture capital investment in cardiology has declined sharply since 2008. This is mainly attributable to significant policy changes by the U.S. FDA in areas such as clinical trials, which have led to a substantial increase in the R&D costs of medical devices; meanwhile, insurance companies have adopted a conservative stance toward covering new devices.