Cross-border Healthcare Enters Platform-driven Development Phase with Capital Yet to Fully Pour In | 2016 Annual Review

As 2016 draws to a close, VCBeat’s flagship annual event, the “Top 100 Future Healthcare Companies List,” is arriving as scheduled. While the selection process is currently in full swing, the excitement extends far beyond this. Prior to the unveiling of the Top 100 list, VCBeat has meticulously curated a series of year-end reviews focused on specific healthcare subsectors. Targeting the hot healthcare niches of 2016, these reviews systematically examine the current state of enterprises, highlight key events, and analyze development trends within each field over the past year, delivering a rich and engaging feast of content for our readers.

In 2011, only 3% of affluent Chinese individuals were aware that they could seek medical treatment abroad in emergencies; by 2014, this figure had surged to 40%. For Chinese people, concern about healthcare ranks second only to housing prices. Social issues stemming from numerous problems within China’s domestic healthcare sector are frequently reported in the media. Meanwhile, advanced technologies and cutting-edge pharmaceuticals available overseas are attracting Chinese citizens. An increasing number of middle-class individuals with the financial means and need have begun to include cross-border healthcare as an option in their health investment portfolios.

In recent years, cross-border healthcare consumption has gradually gained momentum in China. According to incomplete statistics, approximately 3,000 Chinese patients chose to seek medical treatment in the United States in 2015, and this figure is projected to exceed 5,000 in 2016. Market analyses predict that the potential of China’s overseas healthcare market could surpass tens of billions of U.S. dollars over the next decade. Various indicators suggest that the cross-border healthcare industry is now positioned at a pivotal point of rapid growth.

The internet is continuously transforming our lifestyles, harnessing the power of connectivity to drive change. At its core, China’s healthcare sector is grappling with a mismatch between supply and demand. By leveraging the connective nature of the internet to link China’s healthcare needs with global resources, cross-border healthcare emerges as a viable solution. The changes brought about by the internet are often explosive and unpredictable. Therefore, we have decided to thoroughly examine the origins and development of cross-border healthcare to determine whether the “Internet + Cross-Border Healthcare” model is truly feasible.

This report examines the healthcare landscape in destination countries for cross-border medical services, analyzes the current status of four categories of medical services, and reviews three types of cross-border healthcare service providers: traditional medical institutions, representative offices of foreign hospitals in China, and internet-based cross-border healthcare platforms. (A total of 49 companies are included in the statistical scope of this report, with continuous updates ongoing.)

List of Cross-Border Healthcare Enterprises

Macro-Environmental Analysis of Cross-Border Healthcare

What Is Cross-Border Healthcare?

“Cross-border healthcare,” traditionally referred to as “seeking medical treatment abroad” and also known as medical tourism, refers to individuals traveling to foreign countries to access more suitable healthcare services due to the excessive cost or inadequacy of medical services in their place of residence. Since the core focus of this form of care lies in the medical treatment itself, with travel organization and management serving merely as a supporting framework—and given that this management model can be replaced by that of professional cross-border healthcare service providers—this report defines such a model as “cross-border healthcare” rather than “medical tourism.”

Based on the information collected from 49 companies, we calculated the proportion of those offering four categories of services:

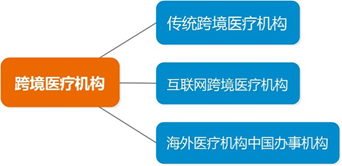

Domestic cross-border medical service providers can be broadly categorized into three types: traditional cross-border medical service agencies, China representative offices of foreign medical institutions, and internet-based cross-border medical service platforms.Among them, traditional cross-border medical service providers entered the market earlier and are more numerous; these established institutions continue to optimize their offline services while also building online platforms.

Another type consists of overseas Chinese representative offices, which are primarily domestic offices established by renowned foreign hospitals or healthcare groups.The final type is the cross-border internet healthcare platform, whose primary model involves establishing an online platform to facilitate cross-border medical care and connect supply with demand.

Why Has Cross-Border Healthcare Emerged?

With the improvement of living standards, growing health demands, rapid development of the internet, and increasing domestic and international information exchange, people have gained a more comprehensive understanding of the disparities in medical resources between China and other countries, bringing cross-border healthcare gradually into the public eye.

According to World Health Organization projections, by 2022, the tourism industry will account for 11% of global GDP, while the health industry will account for 12%, becoming the world’s largest industry. As an organic integration of these two sectors, cross-border healthcare will emerge as a new growth engine for the global economy. Over the past five years, the global medical tourism sector has grown at an average annual rate of 9.9%. Incomplete statistics show that the total global revenue of the medical tourism industry was $40 billion in 2004, rose to $60 billion in 2006, and has currently reached $300 billion. It is projected that by 2017, global medical tourism will generate $678.5 billion in revenue, accounting for 16% of the total global tourism revenue. The substantial economic benefits brought by medical tourism have further accelerated its rapid development worldwide.

Global Medical Tourism Market Output Value Trends

Data source: Publicly available information on the internet, VCBeat

2014In 2014, China’s medical tourism market was valued at RMB 40.8 billion, accounting for less than 1% of the global market. As the world’s largest source market for outbound tourism and the top spender in this sector, China’s outbound tourism expenditure represented 11% of international tourism revenue in 2014. The potential for future growth is substantial, yet existing overseas medical tourism intermediaries still operate under outdated all-inclusive pricing models, which fall far short of meeting the rapidly growing market demand.

2010~2014Market Size of China's Medical Tourism Industry

Data Source: Publicly Available Internet Information, VCBeat

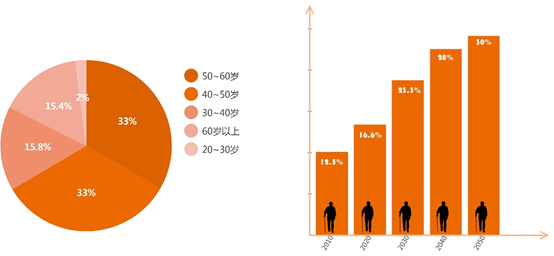

From the demographic structure of individuals seeking cross-border medical services, those aged 40 and above constitute the primary group, accounting for more than 80% of the total. This indicates that as population aging intensifies, the proportion of middle-aged and elderly individuals continues to rise, while their demand for healthcare becomes increasingly strong. Consequently, the customer base for cross-border medical services will continue to expand.

Demographic Profile of Cross-Border Medical PatientsTrend in the Proportion of China’s Population Aged 60 and Above

Data Source: Public Internet Information, VCBeat

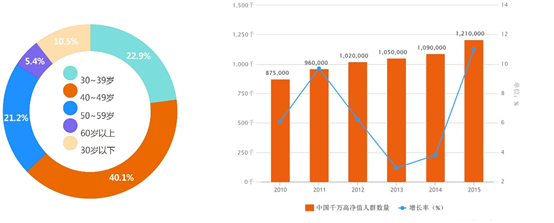

Over the past six years, the number of high-net-worth individuals (HNWIs) in China has continued to grow, showing a fluctuating upward trend. The growth rate of HNWIs with assets exceeding RMB 10 million hit its lowest point in 2013 and peaked in 2015. As the market size of the middle class and the nouveau riche expands, the healthcare industry is upgrading, placing greater emphasis on globalization, experiential services, and personalization. An analysis of the age structure of Chinese HNWIs reveals that individuals aged 40 and above constitute the majority. With their strong purchasing power, they are poised to become the primary demographic for cross-border medical services.

Age Structure of China's High-Net-Worth Individuals Number and Growth Rate of China's High-Net-Worth Individuals

Data Source: Public Internet Information, VCBeat

The age structure of individuals seeking cross-border medical care, as well as the core demographic of China’s high-net-worth population, is predominantly composed of those aged 40 and above. As healthcare needs tend to increase with middle age, it is evident that the primary profile of Chinese patients pursuing cross-border medical services consists of individuals with substantial financial capacity and significant healthcare demands.

Disparity in Medical Resources Between China and Abroad: Overall Shortage of Domestic Medical Resources

From the perspective of healthcare systems, those in foreign countries are more robust. China lacks a referral mechanism, causing physicians to devote substantial energy to repeatedly treating common minor ailments; even renowned specialists often find themselves managing routine cases. Domestic hospitals are overcrowded, leading to strained doctor-patient relationships, as the healthcare system prioritizes patient volume over service quality. In developed nations, healthcare systems have reached an advanced stage, with sufficient hospitals and physicians, as well as a scientifically structured tiered referral system. Consequently, these systems not only ensure therapeutic efficacy but also deliver high-quality service.

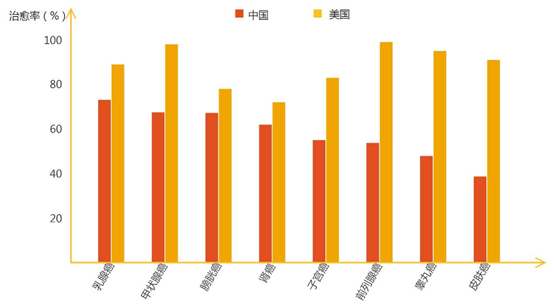

In terms of treatment outcomes, foreign physicians have lower misdiagnosis rates, higher cancer cure rates, and a more comprehensive healthcare-related industry ecosystem. In China, the generally weaker technical proficiency of physicians and a shortage of pathologists have contributed to higher hospital misdiagnosis rates; it is reported that the outpatient misdiagnosis rate in China approaches nearly 40%. An article published in 2008 in an American medical journal cited statistics indicating that the average misdiagnosis rate in the United States ranges from <5% to 15%, with rates in pathology, radiology, and dermatology being <5%.

Comparison of 5-Year Relative Survival Rates for Cancer Between China and the United States

Data source: Publicly available information on the internet, VCBeat

Furthermore, the healthcare industries in developed countries are more mature. The invention and application of advanced medical technologies and instruments originate from these medically advanced nations. Examples include the da Vinci Surgical System, Gamma Knife, X-ray, magnetic resonance imaging (MRI), PET-CT, electrocardiogram (ECG) monitors, cardiac pacemakers, minimally invasive surgery, and organ transplantation. In China, the adoption of these advanced technologies and instruments typically lags behind that of foreign countries by 10 to 20 years or even longer.

Another contributing factor is China’s stringent drug regulations. In the United States, patients can access the latest newly developed anticancer drugs. New anticancer agents, once approved after successful R&D, are typically launched first in the U.S. and European countries before entering the Chinese market. As a result, the market launch of new drugs in China lags behind that in the U.S. by at least three years. Due to overly strict regulatory controls on new drug market entry in China, it is difficult for foreign novel drugs to enter medical institutions through conventional channels.

Policy Orientation: The Government Actively Promotes Medical Tourism

China has also implemented corresponding policies to promote the development of medical tourism, primarily including the relaxation of market access conditions, strengthened planning, layout, and land-use guarantees, and the optimization of investment and financing guidance policies. The State Council’s 2013 “Several Opinions on Promoting the Development of the Health Service Industry” pointed out the need to support the development of health service industry clusters.

National Policies

On February 28, 2013, the State Council officially approved the establishment of the Boao Lecheng International Medical Tourism Pilot Zone in Hainan Province. The plan proposes that the Lecheng project aims to build an emerging industrial park with a focus on medical services, attracting international high-end medical and research institutions to develop tourism-oriented healthcare and rehabilitative care. Meanwhile, it will prioritize health examinations, treatment and rehabilitation for chronic diseases, traditional Chinese medicine wellness and healthcare, cosmetic and plastic surgery, as well as the research, development, and incubation of advanced medical technologies.

During the 12th Five-Year Plan period, Tianhe District in Guangzhou planned to integrate medical and health resources, highlight the distinctive features of medical aesthetic tourism services, attract domestic and international medical institutions to establish operations, and set up a “Hong Kong, Macao, and Taiwan Medical Center.” It also aimed to build the Tianhe Health and Beauty City, aggregating more than 30 well-known domestic and international plastic surgery and beauty brands, as well as Zhongshan Avenue Medical Tourism Street, featuring over 50 high-quality medical institutions.

In June 2008, the Chengdu Municipal People's Government approved the establishment of the "Chengdu International Medical City" in Yongning Town, Wenjiang District. The initial planned construction area covers 18.34 square kilometers, with an additional 13.16 square kilometers reserved for future development. Currently, it has attracted tenants such as the Taiwan Meizhao Health Management Center, Beijing Fuwai Hospital, Sichuan Bayi Rehabilitation Center, U.S. ICT (Chengdu) Oncology Diagnosis and Treatment Center, U.S. WA Regenerative Medicine Center, and West China Hospital National Demonstration Rehabilitation Center.

Representative Local Policies (Shanghai)

In 2010, the Shanghai Medical Tourism Product Development and Promotion Platform, established through multi-party cooperation between Chinese and foreign entities, was officially launched, marking the beginning of Shanghai’s development in medical tourism. In April 2013, the inaugural Shanghai International Healthcare and Medical Tourism Conference and Shanghai International High-End Healthcare Services Exhibition were held. During this event, health authorities explicitly identified the Shanghai International Medical Park and the Shanghai New Hongqiao International Medical Center as two core platforms for developing high-end medical services, including international medical tourism.

Analysis of Healthcare Conditions in Cross-Border Medical Destinations

In China’s cross-border healthcare market, the primary destinations for medical services include the United States, Japan, South Korea, Thailand, Germany, and India. Currently, these destinations are relatively concentrated, with the vast majority possessing distinct characteristics and competitive advantages. For instance, South Korea is the most popular destination for aesthetic medicine and anti-aging treatments; Japan holds a significant advantage in precision health screenings; and the United States is the primary choice for referrals involving critical and severe conditions. Europe and the United States represent the most premium tier of cross-border healthcare destinations, primarily offering treatments characterized by high technological sophistication. Meanwhile, Asian countries attract global clients through specialized, cost-effective services such as medical aesthetics and assisted reproductive technologies. We have categorized the leading medical offerings by destination into four types of medical services and developed a map of cross-border healthcare destinations.

Map of Cross-Border Medical Tourism Destinations

Source: VCBeat Research

Healthcare Service Conditions at the Destination

Destination Medical Pricing: Overall Costs Are Not Exorbitant

Relevant data indicate that approximately 11 million patients worldwide seek cross-border medical services, with an average expenditure of $3,500–$5,000 per person per medical tourism trip. This cost covers all expenses related to medical services, international travel, local transportation at the destination, hospitalization, and other accommodation fees. Furthermore, an examination of medical pricing across various countries reveals that healthcare costs in most nations are not significantly higher than those in China. Using domestic medical expenses in China as a benchmark, average treatment costs in the United States are 3–4 times higher, while those in European countries are only 30% higher (Source: chinaRNA).

Destination Healthcare Services: Comprehensive Services, Streamlined Processes

In fact, the treatment phase of cross-border medical care after traveling abroad is quite straightforward. Once patients secure appointments at U.S. hospitals, their transportation, accommodation, and dining arrangements in the United States are largely similar to those of typical tourist trips. Currently, foreign healthcare institutions place significant emphasis on the Chinese market. Taking the United States as an example, we surveyed 20 renowned U.S. hospitals, all of which have established international departments, with 90% offering Chinese-language services. Late last year, Los Angeles Mayor Eric Garcetti, accompanied by five top-tier international medical centers—Cedars-Sinai Medical Center, Children’s Hospital Los Angeles, City of Hope, UCLA Health, and Keck Medicine of USC—signed a memorandum of cooperation with China Southern Airlines. This partnership launched medical tourism products focused on disease prevention and health check-ups, along with dedicated Chinese-language websites, hotlines, and specialized services for Chinese travelers.

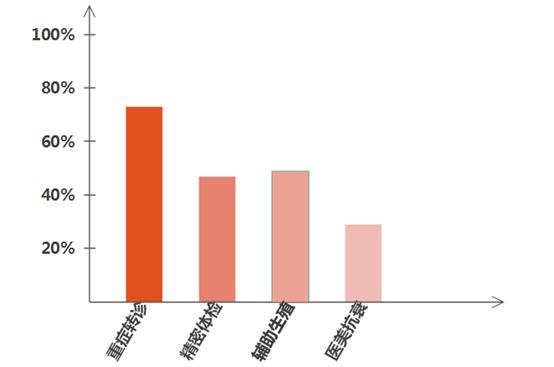

Destination Healthcare Service Types: Highest Proportion of Critical Care Referrals

Based on our statistical data, medical services provided by destination hospitals are categorized into four types: critical care referral, assisted reproduction, precision health checkups, and medical aesthetics and anti-aging. In accordance with the service classifications of domestic cross-border medical institutions, we have calculated the proportion of each of these four service types. Companies offering critical care referral services account for over 70%, those providing precision health checkups and assisted reproduction services exceed 40%, and companies engaged in medical aesthetics and anti-aging services represent nearly 30%. We analyze the underlying reasons as follows: Critical care referral falls under the category of serious medical care, where medical technology remains the most crucial factor in disease treatment. Consequently, many patients still choose to seek treatment in developed countries such as the United States, Germany, or Japan for severe and complex conditions. Given that medical prices in these developed countries are relatively high, profit margins for medical institutions are correspondingly higher.

Proportion of Companies Engaged in Related Businesses

Source: VCBeat

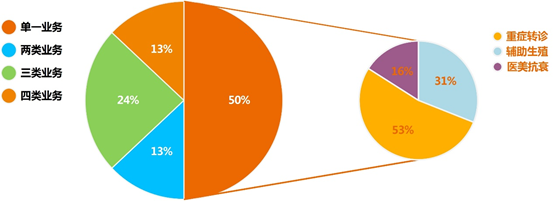

We also compiled statistics on the number of service categories offered by cross-border healthcare institutions. Companies offering a single service accounted for the largest proportion, at 50%. Among those with a single service type, critical care referrals remained the most significant component, representing over 53%; assisted reproductive technology (ART) accounted for 31%, and medical aesthetics and anti-aging services accounted for 16%. The statistics revealed no cross-border healthcare institutions specializing exclusively in precision health checkups. This can be attributed to two main factors: first, domestic residents’ awareness of precision health checkups remains limited, resulting in a relatively small customer base with such demand; second, precision health checkup services are closely linked to other offerings, as companies providing precision health checkups typically also offer critical care referral services.

Source: VCBeat

Critical Care Referral

What Is Critical Care Referral?

Critical Care Referral: This term refers to a healthcare practice in which patients with severe illnesses transfer to medical institutions abroad or in other regions to seek more comprehensive treatment. Conditions covered include tumors, cardiovascular and cerebrovascular diseases, hepatobiliary disorders, diabetes, urological diseases, pediatric conditions, osteoarticular diseases, and neurological disorders.

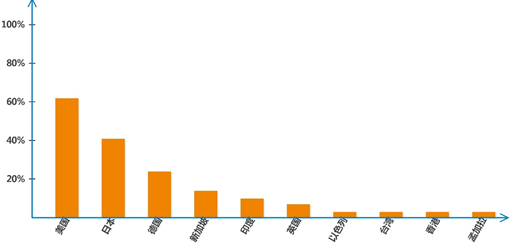

Geographic Distribution of Critical Care Referrals: Countries with High Levels of Medical Care, Such as the United States and Japan

According to the chart showing the proportion of destinations for critical care referrals, it is evident that the primary destinations are the United States, Japan, Germany, Singapore, and others. Among these, the United States and Japan account for the highest shares. Domestic medical institutions tend to collaborate more frequently with advanced healthcare facilities in developed countries. This trend may be attributed to two main factors. First, for critically ill patients, the primary consideration is not cost but rather the level of medical expertise and treatment outcomes, giving the United States and Japan a distinct advantage. Second, Chinese cross-border healthcare providers continue to position themselves primarily in the high-end medical sector; consequently, the hospitals they choose to partner with are predominantly located in developed countries such as the United States and Japan.

Proportion of Companies in Each Country Serving as Destinations for Critical Care Referrals

Data source: VCBeat

Medical Conditions at Critical Care Referral Destinations: High Cancer Survival Rates

Taking the United States as an example for critical care referral destinations, the overall 5-year cancer survival rate in the U.S. is 66%, compared to 31% in China. This significant disparity primarily stems from differences in early diagnosis and early treatment. Additionally, there are variations in the accessibility of comprehensive, multidisciplinary care. It also takes time for advanced medical equipment and therapeutic methods to be introduced into China. Furthermore, while education and collaboration among medical oncology, surgical oncology, and radiation oncology in China are still in their nascent stages, they have shown substantial improvement. Nevertheless, a considerable gap remains compared to advanced international standards. In particular, non-standardized treatment practices are prevalent in small and medium-sized hospitals, contributing to an overall deficiency in the nation’s cancer care capabilities.

A More Detailed Comparison of Treatment Services Between China and the United States: Lung CancerLung cancer is the leading cause of cancer-related mortality in both the United States and China. The latest report released by the American Cancer Society in 2013 indicated that the overall five-year survival rate for lung cancer in the U.S. was 17%. However, due to more effective implementation of early screening programs in the United States, the five-year survival rate for early-stage lung cancer has reached 60% to 80%.

Primary Hospitals for Critical Care Referrals

Source: VCBeat Research

Precision Health Checkup

Precision Health Checkup refers to a comprehensive examination of various body parts using advanced imaging modalities such as CT, MRI, and ultrasound, conducted regularly regardless of the presence or absence of subjective symptoms. The primary objective is cancer screening, followed by the detection of various lifestyle-related diseases. It serves as an important benchmark for assessing one’s recent health status. Targeted organs and systems mainly include the stomach, liver, lungs, intestines, heart, blood pressure, diabetes indicators, prostate, thyroid, uterus, breasts, and ovaries, with a wide variety of specific test items available.

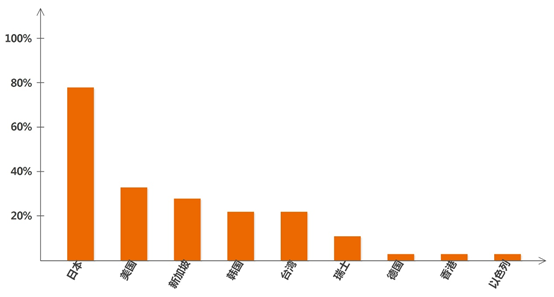

Based on the distribution chart of destinations for precision health checkups, it is evident that Japan is the primary destination. The top four destinations are, in order: Japan, the United States, Singapore, and South Korea. We analyze the reasons behind this trend as follows: First, these developed countries possess advanced medical capabilities. For instance, Japan established its determination and practical measures for nationwide cancer prevention and control as early as thirty years ago, creating a world-leading system for cancer prevention and treatment. Japan is currently the most advanced country in the world in this field. Second, Japan, Singapore, and South Korea are all Asian countries, offering geographical proximity to China. Finally, 100% of the companies offering precision health checkup services also provide referral services for critical illnesses, with the United States and Japan being the primary destinations for such referrals. This fact further explains the observed phenomenon.

Proportion of Companies by Country for Precision Health Checkup Destinations

Source: VCBeat

Precision health checkups are primarily sought in Japan, with 80% of companies offering medical examination services there. In Japan, approximately 80% of cancers are detected at an early stage, and 80% of these patients can be cured. In contrast, in China, more than 80% of cancer cases are diagnosed at mid-to-late stages, and 80% of patients cannot be cured.

Japan’s life expectancy ranks among the highest in the world, and its society is aging at an accelerating pace. The number of deaths caused by malignant diseases, namely cancer (approximately 340,000 cancer-related deaths in 2008), has been increasing. In response, Japan enacted the Basic Act on Cancer Control in 2007 to promote cancer prevention and early detection, advance equitable access to cancer treatment, and foster cancer research. Through screening, Japan can detect cancers smaller than 5 mm, leaving cancer cells nowhere to hide. By contrast, world-class cancer screening typically identifies tumors larger than 15 mm, while in China, instrumental detection generally reveals mid- to late-stage cancers measuring several centimeters or more.

Japanese health checkups recognize that while diagnostic equipment is important, physicians play a dominant role. Doctors conduct detailed inquiries into family medical history, medication history, and general health status, taking a proactive approach throughout the examination process to ensure greater rigor. Through multi-tiered comprehensive assessments covering various indicators—including brain function, blood parameters, visceral organs, and bone health—expert teams provide detailed diagnostic interpretations based on the collected data, enabling examinees to gain a thorough understanding of their physical condition. Additionally, authoritative specialists from various fields offer targeted recommendations and guidance on potential health issues, advising individuals on how to achieve and maintain optimal health. Furthermore, such meticulous examinations facilitate the early detection of major diseases, including cancer, allowing for timely and effective treatment.

Major Hospitals for Precision Health Checkups

Source: VCBeat Research

Assisted Reproductive Technology

Assisted Reproductive Technology (ART) is an abbreviation for Human Assisted Reproductive Technology. It refers to techniques that employ medical interventions to help infertile couples achieve pregnancy, including two main categories: Artificial Insemination (AI) and In Vitro Fertilization and Embryo Transfer (IVF-ET), along with their derived technologies.

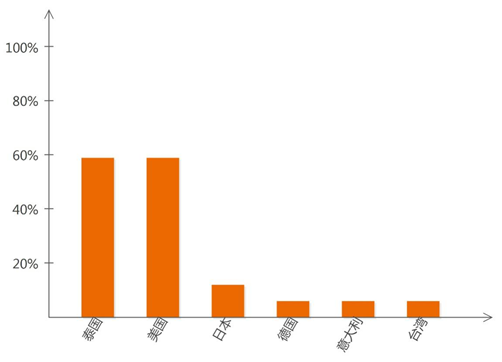

The primary destinations for assisted reproductive technology (ART) are Thailand and the United States, with nearly 60% of companies offering ART services directing patients to these two countries. While both nations have well-developed ART industries, the United States maintains a technological edge over Thailand. However, Thailand holds a significant advantage in terms of cost. Patients with higher technical requirements and greater spending capacity tend to choose the United States, whereas those with moderate financial means seeking high cost-effectiveness often opt for Thailand.

Proportion of Companies by Country for Assisted Reproductive Technology Destinations

Source: VCBeat

Thailand’s IVF success rate is second only to that of the United States and significantly higher than the current level in China, with a success rate of approximately 50%–60%. Thai IVF hospitals have a long history; numerous high-tech hospitals, such as BNH Hospital, Jetanin Hospital, Bangkok International Centre (BIC), and Bangkok Hospital, provide technical and medical assurances for successful IVF outcomes. Moreover, the cost of IVF in Thailand ranges from approximately RMB 70,000 to 90,000, which is basically on par with domestic prices in China and thus more readily accepted by the general public.

Aesthetic Anti-Aging

Medical aesthetics refers to the repair and reshaping of a person’s facial appearance and the morphology of various body parts through surgical procedures, pharmaceuticals, medical devices, and other traumatic or invasive medical techniques. Anti-aging refers to interventions that inhibit or delay the body’s aging process, promote overall health, and help maintain optimal cognitive and physical function within the lifespan determined by genetic factors.

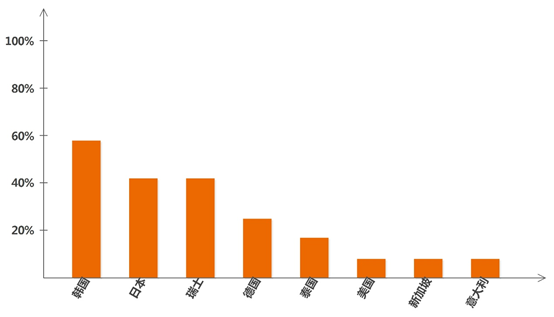

The primary destinations for medical aesthetic anti-aging treatments are South Korea, Japan, Switzerland, and Germany. Among these, South Korea and Japan are the main hubs for general medical aesthetic procedures, while Switzerland and Germany specialize in anti-aging treatments. First, South Korea, Japan, Switzerland, and Germany are all countries with advanced medical aesthetic technologies. Second, the core consumer base of China’s medical aesthetics market consists of individuals under the age of 35, who account for 88% of the market share, whereas customers aged 35 and above represent only 12%. In contrast, in European and American markets, consumers aged 35 and above constitute the majority, accounting for 81.5% of total cases. Therefore, European and American consumers primarily seek anti-aging treatments, while East Asian consumers exhibit more diverse preferences. This has resulted in a market distribution where general medical aesthetic procedures are dominated by South Korea and Japan, while anti-aging treatments are led by Europe and the United States.

Proportion of Companies by Country for Medical Aesthetics Anti-Aging Destinations

Data Source: VCBeat

Taking South Korea, which accounts for the largest share, as an example of a destination for medical aesthetic anti-aging treatments, it is the country with the highest penetration rate of medical aesthetics globally. With a population of less than 50 million, South Korea performs nearly one million cosmetic procedures annually, ranking among the top five countries worldwide in terms of the total number of cosmetic procedures performed. Furthermore, South Korea leads the world with a rate of 13.5 cosmetic surgeries per 1,000 people. There are 2,000 registered plastic surgeons in South Korea, where the threshold for becoming a cosmetic surgeon is relatively high, resulting in a generally high level of technical expertise. Becoming a registered cosmetic and plastic surgeon requires six years of specialized medical education, one year of internet-based technical training, and four years of specialized skills training, during which candidates must pass up to five major assessments. The entire training process typically spans 12 to 14 years.

Analysis of China's Cross-Border Healthcare Industry

In the cross-border healthcare industry structure, patients constitute the demand side. Their methods for accessing cross-border healthcare information fall primarily into three categories: channel-based, advertising-based, and online platform-based. Channel-based approaches mainly leverage healthcare-related channels such as hospitals, physicians, and other patients. Advertising-based approaches rely on broad marketing channels, including search engine optimization (SEO), television advertisements, and outdoor advertising. Online platform-based approaches facilitate direct communication with physicians and hospitals via digital platforms, influencing user decision-making through platform promotion, physician recommendations, and patient feedback.

Within the cross-border healthcare industry structure, cross-border healthcare service providers occupy an intermediary position, primarily comprising traditional cross-border healthcare institutions, internet-based cross-border healthcare platforms, and overseas hospital representative offices. Domestic cross-border healthcare service providers exhibit a high degree of privatization, generally characterized by high-quality services and premium pricing.

In the cross-border healthcare industry structure, medical institutions in destination countries operate on the service supply side. Major healthcare destinations include the United States, Japan, South Korea, Thailand, Germany, and India. These destinations fall into two categories: one comprising the United States, Japan, and Europe, which leverage advantages in advanced technology and high-quality services; the other including South Korea, Thailand, Singapore, India, and Malaysia, which distinguish themselves through specialized offerings and cost-effectiveness.

Source: VCBeat Research

From a horizontal perspective analyzing the demand side, intermediary side, and service side of the cross-border healthcare industry, destination medical institutions on the service side operate under relatively standardized regulatory frameworks, with a comparatively concentrated industrial landscape. Profits are primarily concentrated upstream, particularly among top-ranked medical institutions with strong reputations, which enjoy higher profit margins. However, in the medium to long term, there is greater potential for integration and enhancement from the demand side to the intermediary side, making this segment likely to become the main battleground for competition among various stakeholders. From a vertical extension perspective of the overall industrial structure, the cross-border healthcare industry is beginning to integrate with sectors such as financial insurance, tourism services, and legal services. As a cross-sectoral industry, cross-border healthcare offers broad market dimensions, providing a larger platform for value realization for more participants.

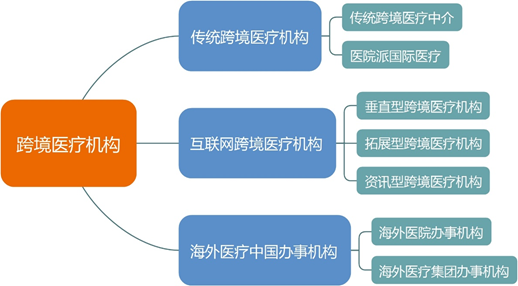

Current Status of the Domestic Cross-Border Healthcare Industry

In China's current cross-border healthcare market via the Internet, service providers are mainly divided into three major categories: traditional cross-border healthcare institutions, Chinese offices of overseas cross-border healthcare providers, and internet-based cross-border healthcare institutions.

Source: VCBeat Research

Overall, traditional cross-border medical institutions occupy the vast majority of the market. However, internet-based cross-border medical platforms and China offices of overseas cross-border healthcare providers remain vital components of the domestic cross-border healthcare sector. As internet platforms gradually become key channels for patient acquisition, they will increasingly shape the competitive landscape of the cross-border healthcare industry. Leveraging domestic hospital resources and advanced medical technologies from abroad, China offices of overseas cross-border healthcare providers have established precise patient acquisition pathways.

Source: VCBeat Research

In January 2016, Wanda Group invested RMB 15 billion to launch its cross-border healthcare business and signed a cooperation agreement with the UK-based International Hospital Group in Beijing.

In March 2016, Xiekang Changrong, a well-established cross-border medical institution, secured RMB 20 million in Series A financing for its Cancer Radar project and planned to establish three early cancer screening centers in first-tier cities within the year.

In March 2016, Jiuyi 160 launched its international medical services, featuring a direct-connect model focused on collaborations with overseas governments.

In April 2016, Yi'an Health, a cross-border medical service platform based on precision medicine, completed its RMB 17 million angel financing round led by Western Capital.

In June 2016, the international medical services segment of Huiyi Online was launched. On June 15, Huiyi Online signed a cooperation agreement with relevant South Korean institutions in Beijing, announcing that several renowned hospitals would gradually join the Huiyi Online platform.

In July 2016, 360 Health officially launched a new overseas medical initiative—“360 Global Quality Medicines”—partnering with top private hospitals in India to provide comprehensive treatment services in India for domestic hepatitis C patients.

In September 2016, Chunyu International, a cross-border internet healthcare platform, completed its Series A and Series A+ financing rounds, with successive investments from Shanheng Capital and Huayao Capital. The total amount raised exceeded RMB 50 million.

In 2006, China’s first private health travel service agency, Mingshi Youxiang, was established, marking the emergence of the initial form of cross-border healthcare. During this phase, the primary business focus was on health tourism and medical wellness. In 2008, Hope Ark, specializing in the Japanese medical sector, was founded. Targeting patients with severe conditions, it brought serious cross-border medical services—such as critical care referrals and precision health screenings—into public view. In 2011, Starnow, dedicated to serious cross-border healthcare, was established to cater primarily to high-net-worth individuals with health needs. From then on, cross-border healthcare entered a high-end, niche, club-style development stage.

Among the 44 cross-border medical service providers we surveyed, 17 were traditional cross-border medical institutions, accounting for 38.6%—the largest proportion among such providers. These institutions entered the market earlier and are relatively more numerous.

Based on the different developmental trajectories of traditional cross-border healthcare, we further categorize it into two types: traditional medical intermediaries and hospital-affiliated international medical services.

Transformation of Traditional Medical Intermediaries: A Case Study of Shengnuo YijiaEstablished in April 2011 with a registered capital of RMB 20.88 million and headquartered in Beijing, Shengnuo Yijia is a leading provider of overseas medical treatment services in China. It was the first domestic referral agency to establish official partnerships with high-quality hospitals abroad. Since its inception, it has obtained authorizations from prestigious hospitals in multiple countries, including the United States, the United Kingdom, and Germany. In 2012, it signed a strategic agreement with Haodf.com, entering the field of online cross-border healthcare.

Hospitals are expanding into international medical services, as exemplified by New Journey Meijia International Healthcare. Originally founded in Houston’s Texas Medical Center in the United States in 2012, Meijia Overseas Healthcare was formally established in Shanghai, China, in 2013. This September, New Journey Hospital Group acquired a controlling stake in Meijia Overseas Healthcare and rebranded it as New Journey Meijia International Healthcare.

Leveraging the nationwide hospital network of New Journey Hospital Group, which includes central medical centers such as Beijing New Journey Cancer Hospital and regional medical centers such as Luoyang Dongfang Hospital and CITIC Central Hospital, New Journey Meijia focuses primarily on oncology. With early prevention as its foundation and personalized treatment plans at its core, it offers a range of international medical services, including overseas health check-ups, cancer screening, remote consultations, international case discussions for complex diseases, green-channel access to global healthcare facilities, and patient accompaniment. Furthermore, by integrating with the group’s domestic hospital network, it facilitates the local implementation and follow-up care of overseas treatment plans in China, providing a one-stop solution for cross-border medical care.

Since 2011, driven by the internet wave, healthcare has gradually achieved the optimization and reallocation of patient-centric medical resources. Multi-site practice for physicians has been progressively liberalized, and patients’ perspectives on seeking medical care have steadily shifted. With the internet’s penetration into the overseas healthcare sector, this market continues to evolve: from traditional referral programs that sent Chinese patients to foreign medical institutions, to increasingly popular medical services in recent years such as cosmetic procedures and health check-ups, as well as overseas remote consultations enabled by advances in hardware technology. The overseas healthcare market has quietly opened up many new opportunities.

On July 22, 2015, Chunyu International Medical officially commenced operations, providing patients with services such as international remote consultation, critical care treatment, assisted reproduction, and overseas health examinations. As one of the strategic shareholders of Chunyu International, Chunyu Doctor, the leading brand in mobile healthcare, has consistently provided strong support to Chunyu International in areas including data resources, customer acquisition, and professional expertise. This marked the entry of internet-based cross-border medical institutions into a phase of platform-oriented development.

Based on their distinct roles within the industry, we categorize internet-based cross-border medical institutions into three types: vertical cross-border medical institutions, expansion-oriented cross-border medical institutions, and information-based cross-border medical institutions.

Vertical cross-border healthcare institutions are exemplified by Chunyu International. Chunyu International clearly positions itself not as an intermediary agency or an overseas hospital entity, but as an internet-based service platform that aggregates global healthcare industry resources. It focuses on the “Internet + Overseas Healthcare Service Platform” model, aggregating all overseas healthcare suppliers—similar to how hotels and airlines are aggregated—including hospitals, medical aesthetics clinics, health examination centers, dental clinics, and more. By integrating information and suppliers online, delivering services offline, and finally transitioning to online private physicians, it completes a closed-loop transaction process.

Expanded Cross-Border Medical Institutions: The Case of WeDoctorWeDoctor Group, founded in 2010 by Liao Jieyuan and his team, is positioned as a large-scale internet healthcare service platform. It provides the public with online appointment registration, medical guidance and triage, in-consultation payment, health consultations, and health management services. On its website, WeDoctor’s overseas medical treatment program is categorized under premium healthcare; however, it actually integrates third-party international medical service providers such as Hanxiang Medical and Aojia Yueyang Medical.

Information-based cross-border medical institutions are exemplified by Fuzhen Wang. Fuzhen Wang is a website under FUZHEN LIMITED, which launched its trial version in September 2014. It is a professional Chinese-language web search engine for the latest medical achievements and an international medical information platform, tailored to meet the needs of domestic patients with critical illnesses by providing access to overseas medical resources (including databases of doctors and hospitals). The platform also outsources the operation of its cross-border medical services to third parties, while generating revenue from international hospitals based on their rankings in the United States and other countries.

Since 2014, renowned U.S. medical institutions such as the Mayo Clinic and Cleveland Clinic have successively established representative offices in Beijing or set up referral channels with domestic hospitals, promoting their areas of expertise—including cancer treatment, pediatric diseases, and hematologic disorders—to attract a large number of patients, thereby fostering exchanges between the domestic and international medical communities.

Based on the differing attributes of the parent companies, we categorize China-based offices of overseas cross-border healthcare providers into two types: representative offices of overseas hospitals and representative offices of overseas healthcare groups.

Taking Shangtai International Medical as an example, overseas hospital representative offices serve as international referral liaisons in China for institutions such as Bumrungrad International Hospital in Thailand. They specialize in providing pre-treatment consultations for IVF in Thailand, guidance through IVF treatment protocols, and lifestyle support services during the course of treatment in Thailand.

Taking Haiyiyu as an example of overseas medical groups’ representative offices, California Health Technology Group established the Haiyiyu U.S. Satellite Clinic Alliance in China in 2015, aiming to serve Chinese patients with U.S. medical services by providing better localized access. The Haiyiyu™ U.S. Medical Platform collaborates with Chinese medical institutions to establish satellite clinics, integrating online and offline services to offer Chinese patients “Internet+”-based Sino-U.S. joint outpatient consultations, specialist video consultations, multidisciplinary video consultations, and facilitated medical travel to the United States, including services for critical care cases. Haiyiyu primarily leverages its network of 30 partnered satellite clinics as customer acquisition channels.

Cross-border healthcare in China emerged in the early 21st century. From 2000 to 2010, it was in a phase of initial exploration, driven by individual patient needs, focused solely on treatment, developing spontaneously, with unclear supply-and-demand dynamics. From 2011 to 2014, it entered an incipient stage characterized by exclusive clubs, led by healthcare service providers that attracted patients through medical technologies and resources; this period featured autonomous development, with treatment remaining the primary focus while services such as precision health screenings gained visibility. After 2014, the sector entered a platform-based development stage. Leveraging rapid advancements in information technology and global integration, communication between domestic and international healthcare markets became more frequent, and online medical resources were increasingly integrated into the cross-border healthcare industry, fostering scaled-up growth.

Taking Cedars-Sinai Medical Center in Los Angeles, USA, as an example, the number of Chinese patients seeking cross-border medical services at Cedars-Sinai has been gradually increasing since 2012. Starting in 2015, Cedars-Sinai entered the Chinese market to explore opportunities in cross-border healthcare, initially collaborating with traditional cross-border medical intermediaries. In April this year, it joined the internet-based cross-border healthcare platform “Chunyu International” to jointly develop cross-border medical services. In 2015, more than 30 Chinese patients received treatment at Cedars-Sinai; however, within just the first few months of 2016, over 100 Chinese patients had already undergone cross-border treatment at Cedars-Sinai Medical Center.

Since 2014, capital has shown a strong preference for the cross-border healthcare market. Many cross-border healthcare companies have attracted significant investor interest. In June 2014, Sequoia Capital completed its Series A investment in Beijing Shengnuoyijia Hospital Management Co., Ltd., entering the high-end transnational healthcare market. In April 2016, Yi’an Health, a cross-border healthcare service platform, announced that it had secured RMB 17 million in angel financing led by Western Capital. In August 2016, Huayao Capital officially completed its investment in Chunyu International, the leading brand in China’s internet-based cross-border healthcare sector, thereby entering the field of internet-enabled cross-border healthcare.

Selected Invested Companies in the Cross-Border Healthcare Market

Data source: VCBeat

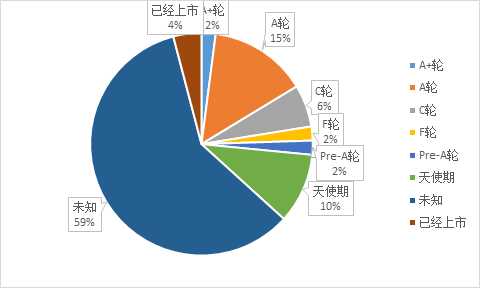

Among the 49 companies included in our statistics, 29 (59%) had either not raised financing or had not disclosed their financing status. A total of 20 companies had financing records, comprising five at the angel round, one at the Pre-A round, seven at the Series A round, one at the Series A+ round, three at the Series C round, one at the Series F round, and two that were publicly listed. Furthermore, among the 15 companies that had raised funding beyond the angel round or were publicly listed, eight were not exclusively focused on the cross-border healthcare vertical; instead, they had expanded into the cross-border healthcare sector from the online healthcare domain.

Data source: VCBeat

To better illustrate the capital market’s attention to cross-border healthcare, we selected vertical cross-border healthcare institutions with financing records and compiled their financing data.

Note: Bubble size represents the amount of financing.

With Shengnuo Yijia, Wordicon, and Chunyu International—three distinct types of cross-border healthcare providers—securing consecutive investments, both the domestic industry and capital markets have demonstrated growing attention to the demand for high-end transnational medical services. An analysis of funding rounds reveals that all surveyed companies are at stages prior to Series B, indicating that the cross-border healthcare sector is still in its early explosive growth phase. While capital markets are closely monitoring this space, they have not yet fully flooded into it.

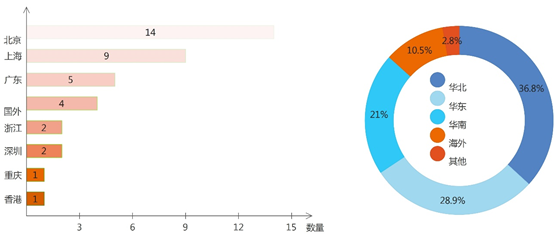

From the 49 cross-border healthcare companies included in our statistics, we excluded those that outsource their cross-border healthcare operations to third parties. These excluded entities, primarily internet companies focused on information services and market expansion, totaled 11. We then analyzed the geographic distribution of the headquarters of the remaining 38 companies.

Data Source: VCBeat

According to our statistics, the geographical distribution of cross-border medical institutions in China is highly unbalanced, with central cities serving as key hubs. Currently, the cross-border healthcare industry is primarily concentrated in the developed eastern regions. Although market coverage has expanded geographically to include central cities in the central and western regions, the vast markets of second- and third-tier cities in these areas remain largely untapped. There is still a lack of channels for product promotion and business expansion, meaning that downward market penetration will take time. At present, China’s cross-border healthcare market is centered around Beijing, Shanghai, and Guangzhou, and can be broadly divided into four major segments: East China, North China, South China, and Overseas. Among these, the North China, East China, and South China markets account for the majority of the share.

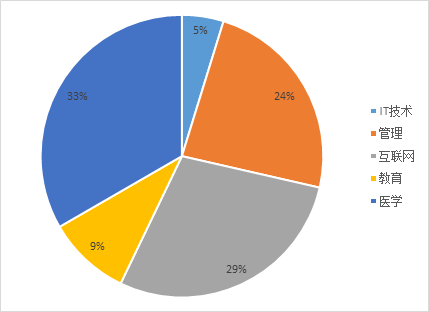

The background and experience of founders largely determine a company’s development direction and business model. Therefore, we analyzed the backgrounds of founders in cross-border healthcare companies. The results show that those with medical backgrounds account for the highest proportion at 33%, followed by internet backgrounds at 29%, traditional management backgrounds at 24%, and education backgrounds at 9%. Although the proportion of founders with medical backgrounds is the highest, it is significantly lower than the overall proportion in healthcare startups. This indicates that cross-border healthcare relies less on specialized expertise and has relatively low technical barriers. Additionally, we found that more than half of the founders in cross-border healthcare have overseas work experience. Their familiarity with overseas medical treatment processes enables them to better optimize services, which provides certain advantages in the cross-border healthcare sector.

Source: VCBeat

Service fees for overseas medical treatment are generally divided into two parts. The first part covers domestic appointment-related costs, including the organization and translation of medical records, expert evaluations, hospital appointments, and visa processing. The second part covers service expenses incurred during the stay in the United States, such as accommodation and meal arrangements, interpretation services accompanying medical treatment, and transportation. Most agencies charge both parts together. Typically, the total service fee ranges from 50,000 to 100,000 yuan, which is difficult for many patients seeking overseas treatment to afford.

Currently, the cost of cross-border medical services in China is gradually returning to rational levels. Many online healthcare companies have entered the cross-border medical sector, leveraging their expertise in internet-based strategies. The brand effect has enabled them to attract customers at lower costs, thereby reducing customer acquisition expenses and, consequently, product prices. Meanwhile, with their participation, the market for cross-border medical service providers is becoming more rational, shifting the focus back to core medical services while reducing ancillary tourism-oriented customized offerings. Taking health check-ups in Japan as an example, prices were previously highly inconsistent, with some packages costing as much as RMB 160,000 to 200,000. After its launch, the Chunyu International platform introduced a Japanese health check-up package priced at RMB 30,000, which was well received by many users. Currently, prices across the entire market are gradually returning to a reasonable range.

In fact, the most challenging aspect of seeking medical treatment abroad is securing appointments before departure, rather than the treatment itself once overseas. Once patients have successfully scheduled appointments at U.S. hospitals, their transportation, accommodation, and dining arrangements in the United States are largely similar to those for typical tourism. The international departments of U.S. hospitals generally provide professional interpreters to assist patients throughout their treatment.

Currently, cross-border medical service providers in China offer largely comprehensive services, with most institutions providing one-stop solutions. These include: medical consultants assisting patients in organizing and translating medical records; coordinating appointments for evaluations by overseas specialists; scheduling medical visits; facilitating visa applications; arranging flight tickets, hotel accommodations, and local transportation; booking local interpreters and patient escorts; assisting with hospital billing and negotiating fee discounts; and providing post-return health management. Cross-border medical institutions effectively handle nearly all procedural aspects, making seeking medical treatment abroad increasingly straightforward.

Horizontal Comparison of Three Types of Institutions

We analyzed the geographic distribution of the selected companies by cross-border healthcare category. Our statistics reveal that traditional cross-border healthcare institutions have a broader geographic footprint, with economically developed regions serving as their primary hubs; their business expansion relies mainly on regional customer word-of-mouth. Internet-based cross-border healthcare institutions are predominantly concentrated in Beijing, Shanghai, Guangzhou, and Shenzhen—key hubs for internet entrepreneurship—where abundant tech talent enables them to leverage digital advantages for business growth. The headquarters of overseas cross-border healthcare institutions are largely located abroad, allowing them to expand their business through institutional reputation and hospital professionalism.

Source: VCBeat

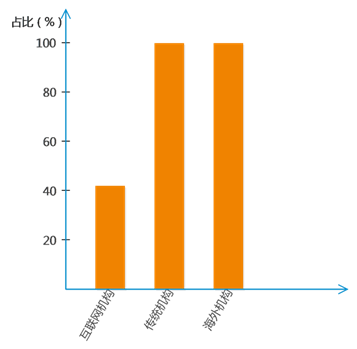

Only 42% of internet-based cross-border healthcare institutions provide offline services, a figure that lags significantly behind traditional cross-border healthcare providers and domestic offices of overseas institutions. One reason is that internet-based cross-border healthcare companies primarily rely on online channels for promotion, as customer acquisition costs for offline channels are relatively high. Another reason is that these companies were generally established later and have not yet developed comprehensive business channels.

Data Source: VCBeat

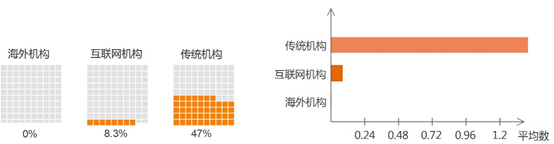

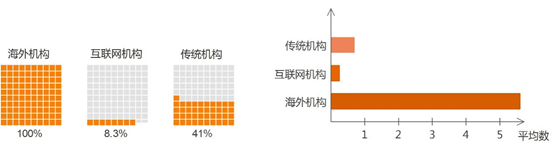

Domestic branches or offices established by cross-border medical institutions primarily serve to facilitate offline customer services and provide post-return medical follow-up care. The presence of such branches reflects the domestic service capacity and scope of these cross-border medical institutions. We analyzed the distribution of service branches (excluding headquarters) set up by three types of cross-border medical institutions in China. Overseas medical institutions with Chinese representative offices have virtually no additional branches elsewhere in China beyond their representative offices. Among internet-based companies, only 8.3% maintain branch offices, whereas nearly 50% of traditional institutions have established branches. Therefore, traditional institutions hold a significant advantage in bridging offline services between the downstream and midstream segments of the industry chain.

Source: VCBeat

Overseas branches established by cross-border healthcare institutions are primarily designed to provide patients with more comprehensive follow-up care services. The presence of such overseas branches reflects the service capabilities and reach of these institutions abroad. We analyzed the overseas branch establishment patterns across three categories of cross-border healthcare institutions. All institutions in the “Overseas” category have branches or representative offices abroad. In contrast, only 8.3% of companies in the “Internet-based” category maintain overseas branches, while over 40% of those in the “Traditional” category do. Furthermore, the average number of overseas branches per cross-border healthcare institution exceeds five. Therefore, overseas institutions hold a distinct advantage in facilitating offline coordination between the midstream and downstream segments of the industry chain.

Source: VCBeat

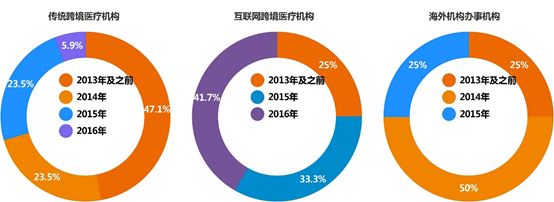

From the perspective of establishment dates, China’s cross-border healthcare industry is relatively young overall. Traditional cross-border healthcare institutions were the earliest to emerge, with nearly 50% founded between 2006 and 2013. In contrast, internet-based cross-border healthcare providers and overseas representative offices started somewhat later, with more than 70% established after 2013. Traditional cross-border healthcare institutions hold certain advantages in reputation building and service process optimization.

Data Source: VCBeat

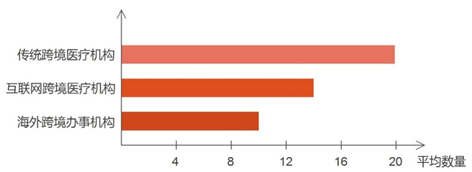

When calculating the number of partner hospitals, companies specializing in the medical aesthetics sector, which have a significant impact on overall figures, were excluded. Due to the substantial influence of extreme values on the data results, both maximum and minimum values were removed to determine the average number of partner hospitals across three types of institutions. The average number of partner hospitals for traditional cross-border healthcare institutions is close to 20; for internet-based cross-border healthcare institutions, it is approximately 14; and for overseas cross-border healthcare institutions, it is around 10. Traditional cross-border healthcare institutions were established earlier and forged connections with high-quality hospitals worldwide at an earlier stage, resulting in a relatively larger number of partner hospitals. Although internet-based cross-border healthcare institutions have a shorter history, their parent internet enterprises have developed rapidly. Furthermore, both traditional and internet-based cross-border healthcare institutions are driven by domestic demand, offering more comprehensive business scopes compared to the domestic offices of overseas cross-border healthcare providers. In contrast, the domestic offices of overseas cross-border healthcare providers leverage foreign medical resources and focus on specific business areas, leading to a relatively smaller number of partner hospitals.

Source: VCBeat

Based on the collected data, we have compiled statistics on the destination countries for three types of institutions. It is evident that traditional and internet-based providers serve a relatively broad range of destinations, whereas overseas-focused providers, being driven by the medical industries in their target markets, offer a more limited selection. Furthermore, the primary destinations for traditional providers are countries such as the United States and Germany, which hold competitive advantages through technological prowess; in contrast, internet-based providers mainly direct patients to countries like Thailand, India, and Singapore, where cost competitiveness is the key advantage.

Data Source: VCBeat

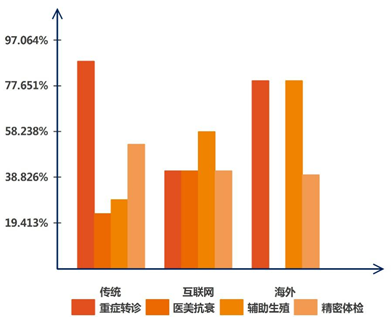

Among traditional cross-border medical institutions, nearly 90% offer critical care referral services, and approximately 50% provide precision health check-up services. Internet-based cross-border medical institutions show a relatively even distribution across the four business types, each accounting for around 40–60%. Overseas cross-border medical facilitation agencies primarily focus on critical care referrals and assisted reproductive technology (ART) services.

Source: VCBeat

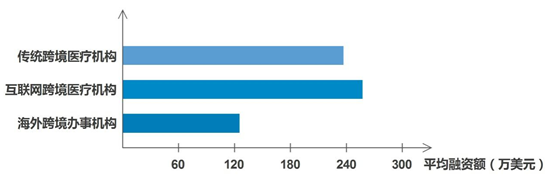

In terms of financing, all three types of cross-border healthcare institutions have gained recognition from the capital market. Traditional cross-border healthcare institutions and internet-based cross-border healthcare institutions have received an average funding amount of approximately $2.4 million, while overseas cross-border healthcare liaison offices have secured an average funding amount of around $1.2 million. Both traditional and internet-based models are driven by domestic demand, feature relatively broad business scopes, and leverage local advantages, making them more attractive to investors.

Data source: VCBeat

Copyright Notice

This report is produced by VCBeat. All text, images, and tables contained herein are protected by applicable trademark and copyright laws. Portions of the text and data have been collected from publicly available sources, with ownership retained by the original authors. No organization or individual may reproduce or distribute this report in any form without the prior written permission of our company. Any unauthorized commercial use of this report shall constitute a violation of the Copyright Law of the People's Republic of China, other relevant laws and regulations, and applicable international conventions.

Disclaimer

This research report is based on information that VCBeat considers reliable and currently publicly available. VCBeat strives to, but does not guarantee, the accuracy and completeness of such information. Due to limitations in research methodologies, sample sizes, and the scope of data collection, the data presented herein only reflect the basic conditions of the surveyed population during the survey period and serve solely for the current research purposes, providing a general reference for the market and clients. Furthermore, VCBeat does not guarantee that the opinions or statements contained in this document will remain unchanged. At different times, VCBeat may issue reports with data, opinions, and projections inconsistent with those presented in this report.

VCBeat does not consider recipients of this report as its clients by virtue of their receipt thereof. This report is distributed solely for informational purposes and only where permitted by applicable laws; it shall not be construed as advertising in any manner. Under no circumstances shall the information contained herein or the opinions expressed constitute investment advice to any person. Where permitted by law, VCBeat and its affiliated entities may hold equity interests in companies mentioned in this report and may provide or seek to provide capital raising, financial advisory, or other related services to such companies.

Note: I am Wang Guanglong, an author at VCBeat. If you are an investor interested in cross-border healthcare, or an entrepreneur in the cross-border healthcare sector seeking media coverage, please feel free to contact me. We also welcome any leads on relevant companies. WeChat: touchlife1; Email: wang.gl@vcbeat.top