Online Medical Aesthetics: Appearance-Driven Demand Reshapes the Industry, with Minimally Invasive Procedures Emerging as the Next Growth Catalyst | 2016 Annual Review

As 2016 draws to a close, VCBeat’s flagship annual event, the “Top 100 Future Healthcare Companies,” is arriving as scheduled. Prior to the unveiling of the Top 100 list, VCBeat has meticulously curated a series of year-end review features focused on specific healthcare subsectors. These articles are designed to help you quickly gain in-depth insights into the hot healthcare subsectors of 2016, providing a clear overview of the current status of companies, key events, and development trends within each segment.2016 Future Healthcare Top 100 Forum Registration Is Now Open, Registration PointHere!

“Only the good-looking have a youth.” At some point, the term “yanzhi” (facial attractiveness score) suddenly became a buzzword online. A “beauty revolution” has quietly swept in, unleashing the public’s innate desire for beauty to an unprecedented degree. In 2008, photo-editing apps took off; in 2012, mobile beauty applications surged in popularity; in 2014, selfie sticks became all the rage; and in 2016, internet celebrity streamers rose to prominence. From simply enhancing one’s appearance through skincare and photo editing, many people now aspire to become online influencers, hoping to leverage medical aesthetics to better promote and present themselves. As a result, the medical aesthetics industry is poised to seize this new opportunity for growth.

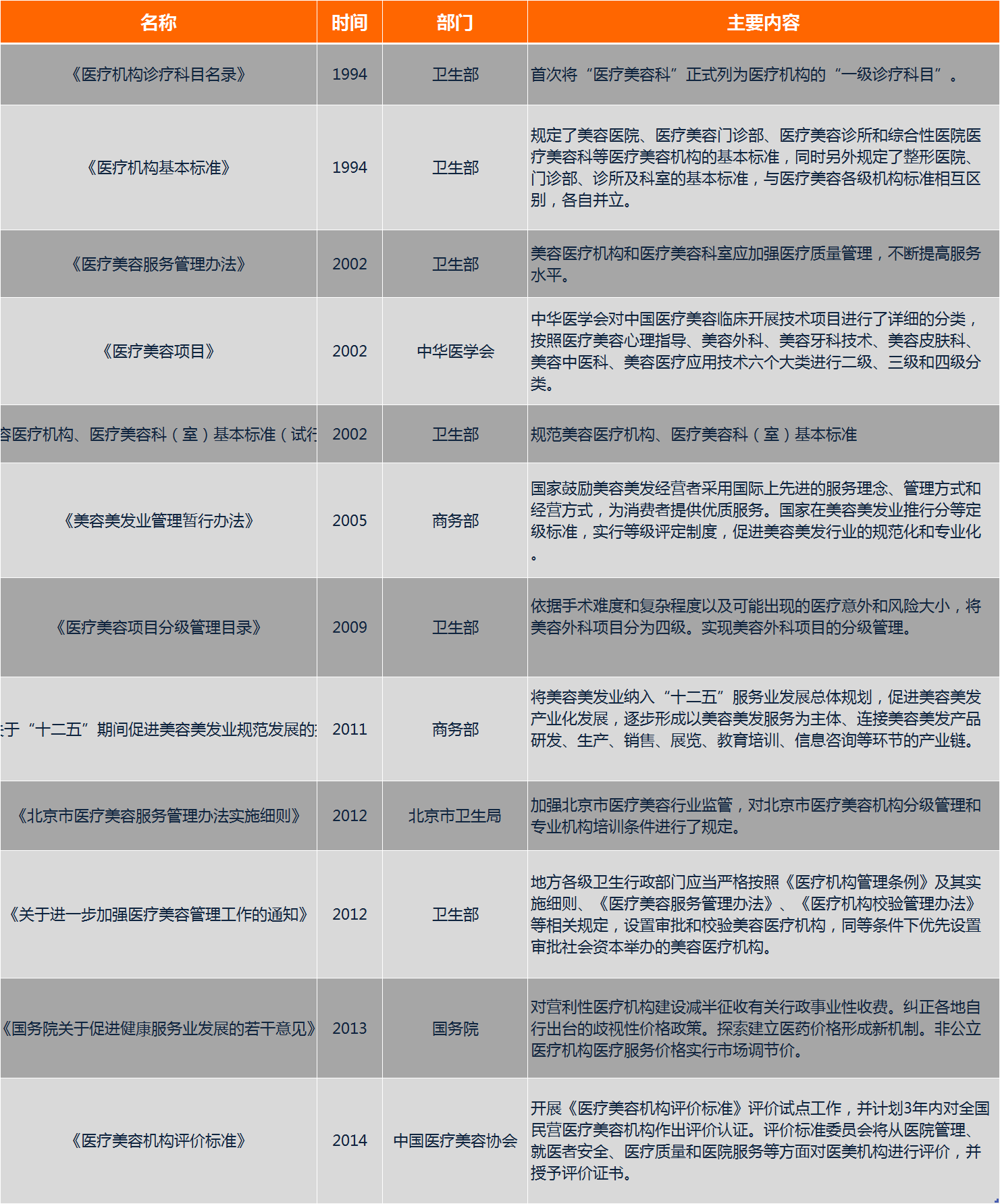

China’s medical aesthetics industry began in the 1980s. Following the reform and opening-up policy, some public hospitals established outpatient aesthetic clinics, while private aesthetic institutions also started to emerge across China. Foreign aesthetic concepts, advanced technologies, cosmetic materials, and operational management philosophies were gradually introduced into China. With the explosive rise of contemporary cultural elements such as short-form videos, internet celebrities, influencers, live streamers, and social media feeds like WeChat Moments, the “beauty revolution” has continuously stimulated consumer demand for medical aesthetic services, driving exponential growth in the number of medical aesthetic institutions.

Currently, the medical aesthetics market accounts for approximately 4.6% of South Korea’s total GDP, whereas China’s medical aesthetics industry is still in its early stages, characterized by a fragmented and disorganized landscape despite its substantial market size. Data shows that the domestic medical aesthetics industry reached RMB 400 billion in 2015, with the industry’s growth rate expected to exceed 15%–20% in 2016.

Demand for aesthetic appeal is driving transformation across the medical aesthetics industry chain, while the rapid development of mobile internet technologies and social e-commerce has accelerated this process. Since last year, the “Internet + Medical Aesthetics” sector has attracted unprecedented attention from investors. Tech industry leaders have begun entering the medical aesthetics market, existing internet-based medical aesthetics platforms have secured frequent rounds of financing, and traditional medical aesthetics institutions are transitioning into online platforms. Amidst this surge in “Internet + Medical Aesthetics,” medical aesthetics apps have sprung up like mushrooms after rain. This new productive force may inject fresh vitality into an industry characterized by uneven development.

VCBeat conducted a comprehensive review of 58 domestic online medical aesthetics startups, detailing their names, locations, founding dates, and financing histories, with data current as of November 2016.

![_{1DUA%UB]1(M%_6VUG2I0G.png](https://cdn.vcbeat.top/upload/image/23/7d/f7/6d/60e41a0cca48e630c234f565d26eaaed.png "1479887686434474.png") 、

、

Data Source: VCBeat, Eggshell Research Institute Database

In March 2016, the medical aesthetics O2O platform So-Young officially announced on March 14 that it had completed its Series C financing round. The amount raised in this round was $50 million, with investors including Youyipin and Tencent’s “Double Hundred” Plan. Following this financing, So-Young will position itself as a connector within the entire medical aesthetics industry, linking consumers, medical aesthetics institutions, physicians, insurance and financial institutions, and pharmaceutical and equipment manufacturers.

In March 2016, the medical aesthetics platform “Meidaila” announced that it had completed a $12 million Series B financing round at the end of the previous year. The round was led by IDG Capital and Ping An Ventures, with existing investor Gaorong Capital participating as a follow-on investor. The funds will be primarily allocated to the development of its e-commerce segment.

In March 2016, Meili Shenqi, an O2O platform for the medical aesthetics community, secured tens of millions of U.S. dollars in Series B financing from Sky View. The funds will be primarily used to build doctor brands on the platform, upgrade core product technologies, promote the brand, and launch a range of medical aesthetic products.

In April 2016, Yuemei.com announced that it had completed its RMB 110 million Series B financing round in December of the previous year. The round was led by SAIF Partners, with follow-on investment from Ceyuan Ventures, the investor in its Series A round. Xiang Xiaoqin, founder and CEO of Yuemei.com, also announced plans to launch offline physical stores.

In June 2016, Langzi Shares issued an announcement proposing to acquire target assets including a 63.49% equity interest in Sichuan Milan Baiyu Medical Aesthetic Hospital Co., Ltd. and a 70% equity interest in Shenzhen Milan Baiyu Medical Aesthetic Outpatient Department Co., Ltd., at a transfer price of RMB 327.2 million.

In July 2016, Suning Universal issued an announcement stating its intention to pay RMB 104 million in cash to acquire an 80% equity stake in Shanghai Yiermei Ganghua Medical Aesthetic Hospital Co., Ltd., thereby entering the medical aesthetics industry.

In August 2016, the Gengmei app held a strategic press conference in Beijing to announce its Series C financing round. Investors in this round included CHJ Jewellery Group, Suning Universal, Tencent, China Securities Co., Ltd., Fosun Pharma, and Legend Capital, with the total funding amounting to RMB 345 million. Moving forward, Gengmei will further refine its online-to-offline (O2O) closed-loop ecosystem and expand into financial services by offering value-added products such as medical aesthetics-related insurance and installment payment plans to its users.

Data source: Charted by VCBeat

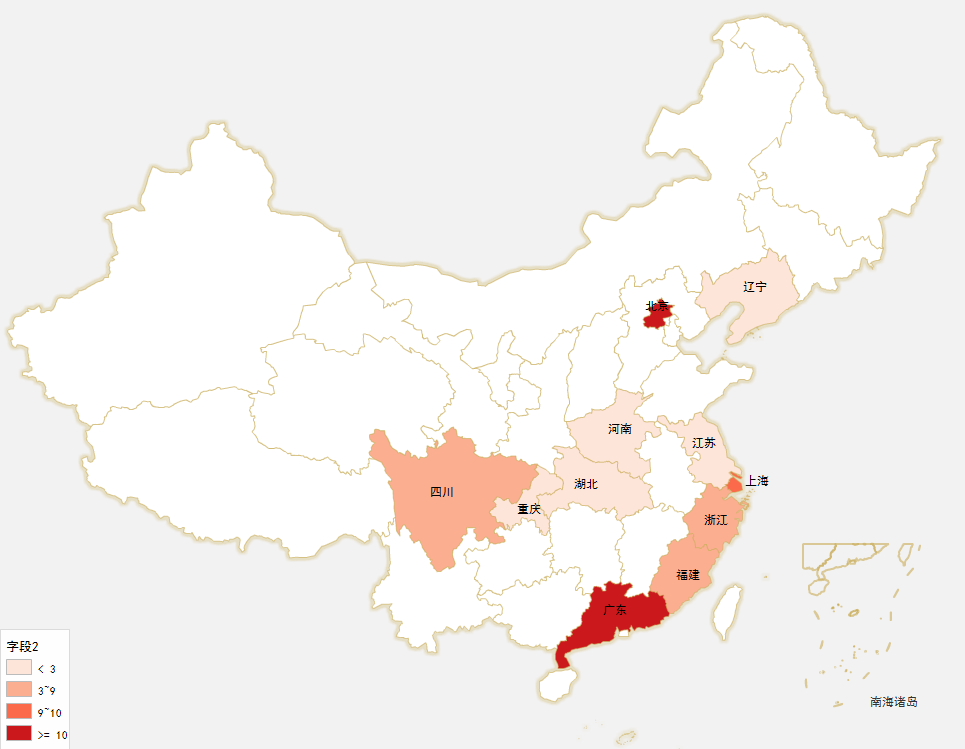

Geographic Distribution of Online Medical Aesthetics Companies

Beijing, Shanghai, and Guangzhou remain the regions with the most vibrant growth in medical aesthetics startups, while entrepreneurial activities are also thriving in certain areas known for producing many beauties. According to Gengmei’s released"2016 Gengmei Medical Aesthetics White Paper"Data shows that the regions with the highest demand for aesthetic enhancement are Beijing, Shanghai, and Chongqing. Additionally, provinces known for producing beauties, such as Sichuan (Chengdu) and Hunan, also exhibit robust demand for medical aesthetics. This pattern largely aligns with the distribution of startups, indicating that the geographic distribution of medical aesthetic ventures is driven by the dual factors of the entrepreneurial environment and market demand for medical aesthetic services.

Data source: VCBeat, Eggshell Research Institute database

Online Medical Aesthetics Financing Overview

Among the 58 companies we analyzed, 27 secured financing. Of these, six did not disclose their funding amounts. The total capital raised by the remaining 22 medical aesthetics startups with disclosed figures amounted to USD 196.13 million, of which USD 146.99 million was raised in 2016, accounting for 75% of the total.

Data Source: VCBeat, Eggshell Research Institute Database

China’s online medical aesthetics industry is dominated by angel-round investments, which account for 52% of total cases. Investment in this sector exhibits a trend wherein later funding rounds correspond to larger individual investment amounts. In 2016, So-Young and Gengmei raised $50 million and $52.27 million, respectively, collectively representing 70% of the total financing in China’s online medical aesthetics sector that year, signaling the emergence of unicorns in the industry.

Data source: VCBeat, VCBeat Research Institute Database

Online Medical Aesthetics Collaboration Overview

Statistics show that China’s online medical aesthetics industry has established extensive collaborations with medical aesthetics institutions, practitioners, and informatics systems. Over 60% of online medical aesthetics companies partner with medical aesthetics institutions. This trend is largely attributable to the industry’s strong service orientation and relatively weak academic foundation. Furthermore, as most players in the online medical aesthetics sector are positioned downstream in the value chain—focusing on the consumer end—they have formed fewer partnerships with medical aesthetics device manufacturers and raw material suppliers, resulting in a rather homogeneous development model.

Data source: VCBeat, VBInsight database

Overview of Online Medical Aesthetic Products

Currently, China’s online medical aesthetics market is dominated by mobile applications and related product services, with apps accounting for 50% of the offerings in this sector. The primary consumers are individuals born in the 1980s and 1990s, a demographic accustomed to obtaining information via mobile devices over extended periods. An analysis of product types and partner institutions reveals that the current online medical aesthetics industry suffers from limited product diversity and significant homogenization, focusing predominantly on information and intermediary services.

Data source: VCBeat, Eggshell Research Institute Database

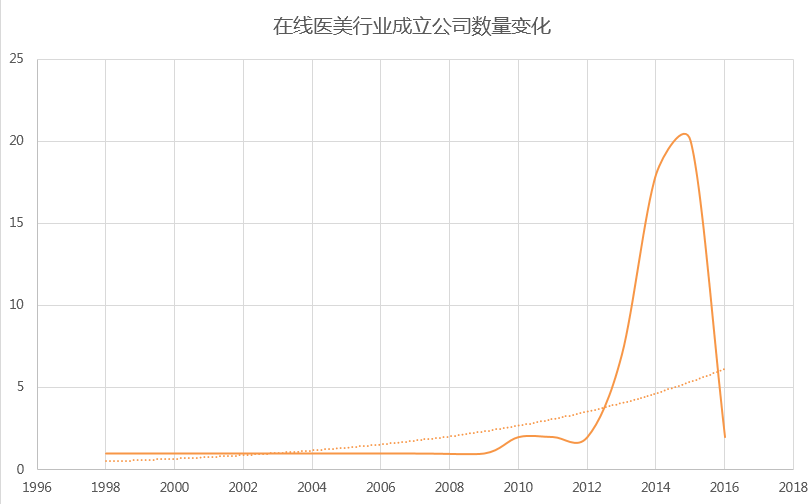

The Development History of Online Medical Aesthetics

Some companies in the online medical aesthetics industry were established relatively early. These entities originally operated as traditional medical aesthetics institutions before transitioning to the online model. Starting in 2012, the number of startups in the online medical aesthetics sector surged, reaching a peak in 2015. During the price wars of 2015, a small minority of these startups emerged successfully amidst the wave of transformation, while the majority failed and withdrew from the turbulent market. These companies were overly optimistic about market prospects and sentiment during their initial planning stages. They failed to adequately account for operational costs, capital turnover costs, and return on investment cycles. Their rash entry into the market often resulted in broken capital chains shortly after establishment or after only a brief period of operation, forcing them to announce transfers and exit at a loss. In 2016, as a "capital winter" set in, both investors and entrepreneurs became more rational, ceasing their blind rush into the volatile medical aesthetics sector.

Data Source: VCBeat, VCBeat Database

As the tide of “Internet + Medical Aesthetics” rises, traditional sales and marketing channels in the medical aesthetics industry have become more transparent and open. The inherent structural flexibility of the industry has significantly increased, with consumers taking a proactive role and exercising consumer sovereignty. To meet consumer demands, companies must offer products and services that are more affordable, delivered faster, and of higher quality. “The customer is king” is no longer just a concept for terminal services but a guiding principle across the entire design, production, and sales chain. Therefore, breaking down information barriers between B2B and B2C sectors and strengthening the interaction between the core industrial chain and consumers are key to the strategic layout of “Internet + Medical Aesthetics.”

Online Medical Aesthetics Industry Chain

Online medical aesthetics primarily focuses on the mid-to-downstream segments of the industry, where the majority of transaction volumes occur. In the traditional medical aesthetics supply chain, medical devices and raw materials pass through multiple distributor layers, resulting in low efficiency and high costs. The ex-factory price is often several times lower than the final retail price, which invisibly inflates the end pricing of medical aesthetic products. On the other hand, traditional chain medical aesthetics clinics typically acquire customers through broad marketing channels such as SEO, television advertisements, and outdoor advertising. The customer acquisition cost for such marketing strategies can reach approximately RMB 6,000 per client. As these costs are ultimately passed on to consumers, they are reflected in product prices. Small-scale institutions often cannot sustain such high marketing expenses; instead, they rely mainly on maintaining existing customer bases or outsourcing sales to small marketing teams. While these institutions have relatively lower marketing costs, outpatient-type medical aesthetics clinics are often of uneven quality, with some lacking proper business licenses and failing to guarantee the professional competence of their physicians.

The “Internet + Medical Aesthetics” model has transformed traditional customer acquisition channels. However, current online medical aesthetics products are primarily focused on the interface between patients and medical aesthetics institutions, while also partnering with insurance companies and financial institutions to offer services such as installment payment plans and medical aesthetics insurance. There is limited engagement with the upstream segment of the medical aesthetics industry, particularly in the procurement of equipment and materials by medical aesthetics institutions. Moreover, no products have yet emerged that specifically target physician training to enhance professional competence. Online medical aesthetics platforms remain largely at the stage of resource integration and information optimization, with no comprehensive solution currently available that can effectively link and coordinate the entire medical aesthetics industry chain.

Source: VCBeat

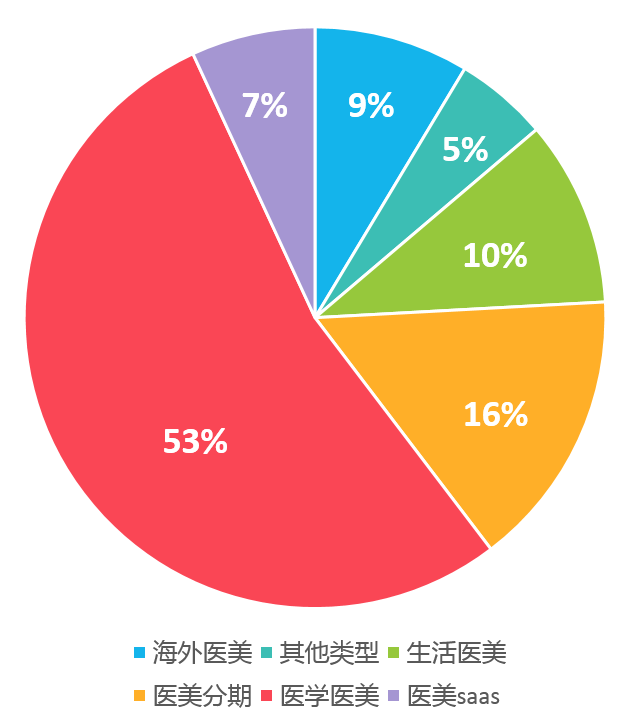

Online Aesthetic Medicine Product Matrix

Online medical aesthetic products vary in their focus. Therefore, we have categorized them based on their primary orientations into five main types: medical-grade aesthetics, non-surgical aesthetics, aesthetic insurance and financial services, overseas medical aesthetics, and aesthetic SaaS. Based on the final form of these products, we have mapped out a product matrix for the online medical aesthetics industry. The target markets are primarily divided into the domestic (Chinese) market and overseas markets. Sub-sectors can be differentiated by the degree of medical relevance. Currently, online medical aesthetic products are dominated by these six categories; the product types are relatively homogeneous, with a strong emphasis on service-driven models, resulting in low industry barriers to entry.

Source: VCBeat

In 2016, among various online medical aesthetics products, medical-grade medical aesthetics platforms stood out, accounting for over 50% of the total. Medical aesthetics installment services accounted for 16%, lifestyle medical aesthetics for 10%, overseas medical aesthetics for 9%, and medical aesthetics SaaS for 7%. The overall trend was upward, with particularly significant year-on-year growth observed in medical-grade medical aesthetics platforms, medical aesthetics installment services, and lifestyle medical aesthetics.

Data Source: VCBeat, VCBeat Database

Medical Aesthetics Platforms to Build Proprietary Brands, with Offline Store Expansion Becoming a Trend

The development models of medical-grade aesthetic medicine platforms are primarily divided into two types: community-based aesthetic e-commerce and cloud clinics. The current development model for community-based aesthetic e-commerce mainly adopts a "community + e-commerce platform + expert consultation" framework. In terms of content, it focuses on three aspects: UGC (User-Generated Content), OGC (Occupationally-Generated Content), and PGC (Professionally-Generated Content), which correspond to user-shared experiences, popular science education, and expert explanations, respectively. Its revenue streams primarily revolve around the e-commerce platform, aiming to stabilize platform growth, enhance user stickiness, and improve monetization capabilities by creating a closed loop of "user → content → cosmetic consumption → content → user."

However, the quality and credibility of user-generated content (UGC) on community-based medical aesthetics e-commerce platforms are currently poor. These platforms are also plagued by a vast number of fake accounts and paid shills. Furthermore, unlike high-frequency consumption sectors such as dining and transportation, the medical aesthetics industry does not share these characteristics. Additionally, community-based e-commerce platforms lack neutrality, making it difficult to form objective evaluations of medical aesthetics institutions. For community-based medical aesthetics e-commerce platforms, followers represent the highest-quality target consumers. To monetize this follower base, the key lies in fostering a sense of community engagement, establishing interaction between physicians and target consumers, and enhancing topic relevance within the community, thereby driving the creation of high-quality UGC.

The medical aesthetics cloud clinic model is primarily represented by So-Young, Gengmei, and Yuemei. These three platforms initially operated as community-based medical aesthetics e-commerce sites before transitioning to the cloud clinic model. The fundamental business model involves medical aesthetics APP platforms signing agreements with offline clinics or hospitals across various regions, as well as contracting with high-quality plastic surgeons. The offline clinics provide patient referrals, facilities, equipment, management, and services, and then share revenue with the physicians. Supported by national policies on multi-site practice, this model offers certain growth potential while ensuring the quality of medical aesthetics practitioners.

Typical Community-Based Medical Aesthetics E-Commerce App Architecture

Source: Charted by VCBeat

Overseas Medical Aesthetics Market Holds Significant Potential, with White-Collar Workers Emerging as Core Consumers

In 2009, the South Korean government officially legalized medical tourism. With strong governmental support, the medical tourism industry has experienced rapid growth. According to a Yonhap News Agency report on November 21, statistical data released by the Korea Tourism Organization on the same day showed that the number of foreign visitors to South Korea had surpassed the 15 million mark this year as of November 21. Among them, Chinese tourists reached 7 million, accounting for nearly half of the total number of visitors, representing a sharp year-on-year increase of 40%.

Relevant data indicate that plastic surgery and anti-aging treatments account for a significant proportion—60%—of healthcare spending by mainland Chinese consumers in overseas medical markets. While the primary clientele for overseas medical services has traditionally been high-net-worth individuals, advancements in aesthetic medicine technology and the development of minimally invasive and non-surgical cosmetic procedures are gradually expanding the consumer base from a niche segment to the general public, with urban white-collar workers emerging as the core consumer group.

Medical Aesthetics SaaS: Penetrating the Consumer Market from the Business Side, or Establishing a Risk-Based Pricing System

As the internet has evolved, the value of data has gradually come to light. In the past, medical aesthetic institutions relied excessively on pay-per-click platforms such as Baidu, employing overly simplistic marketing strategies and lacking strategic direction, which resulted in actual costs outweighing returns. In response, a SaaS-plus-business-opportunity model tailored specifically to the medical aesthetics industry has emerged.

The development path of medical aesthetics SaaS companies involves integrating B-side resources before acquiring C-side users. The business model of medical aesthetics SaaS generates revenue through annual subscription fees and lead-generation fees, serving large chain institutions, large standalone clinics, and small-to-medium-sized outpatient facilities. Characterized by strong neutrality, the platform supports onboarding for all ecosystem partners in the industry. This approach enables access to comprehensive, industry-wide data and creates significant business opportunities for medical aesthetics institutions. Furthermore, the medical aesthetics data held by these SaaS companies can not only serve the institutions themselves but also be integrated with financial institutions to establish risk-based pricing systems for medical aesthetics installment payment plans.

The Lifestyle Integration of Medical Aesthetics: Non-Surgical Procedures May Become the New Growth Engine

"Lifestyle-grade medical aesthetics," also known as "non-surgical medical aesthetics," refers to a novel concept that replaces traditional surgical procedures with various non-invasive medical techniques—such as laser therapy, radiofrequency, injectable fillers, biotechnology, and chemical peels—to achieve skin tightening and wrinkle reduction, facial micro-contouring, facial rejuvenation, body slimming and contouring, and the treatment of skin conditions.

As medical aesthetics gains increasing acceptance in China, the proportion of non-surgical aesthetic procedures within the industry has been rising year by year. Furthermore, with the rapid advancement of biotechnology and medical aesthetic devices utilizing sound, light, and electrical energy, physicians can now address many challenges without invasive surgery.

Data indicates that Taiwan has over 1,000 minimally invasive aesthetic medicine institutions. In South Korea, which is renowned for its expertise in surgical cosmetic procedures, medical aesthetic clinics commonly feature dedicated departments for minimally invasive treatments. Characterized by the ideal consumer attribute of “high frequency and high price,” minimally invasive aesthetic medicine facilitates the establishment of quantitative evaluation systems. Meanwhile, the model of “high frequency and low price” grants it greater elasticity during the industry’s explosive growth. As technology, capital, and industrial resources rapidly converge, the accessibility and cost-effectiveness of minimally invasive aesthetic medicine will improve significantly. This model is poised to become the next major growth engine in the medical aesthetics industry.

Internet Finance Giants to Become the Biggest Threat to Medical Aesthetics Installment Plans

Following the internet’s penetration into the medical aesthetics industry, financialization has accelerated, giving rise to installment-based consumer finance services for medical aesthetic procedures. On one hand, payment caps on online platforms prevent full upfront payment for certain surgical treatments; on the other hand, some consumers cannot afford the total cost of plastic surgery in a single payment. Consequently, installment products for plastic and cosmetic surgeries have emerged. These services provide consumers with options such as prepayment, installment plans, and consumer credit, while generating financial returns for service providers.

As a niche segment of consumer finance, medical aesthetics installment plans account for only the tip of the iceberg in the medical aesthetics industry. However, as an emerging model within this sector, they exhibit significant growth potential. With the medical aesthetics O2O market approaching saturation, both Putian-affiliated providers and financial institutions have keenly recognized the business opportunities presented by medical aesthetics installment financing.

From the perspective of traffic acquisition, medical aesthetics platforms are more targeted toward niche markets; however, installment payment services heavily rely on financial strength, operational efficiency, and risk control capabilities—areas where financial institutions hold a significant advantage. Start-up medical aesthetics platforms lack such experience and strengths. Therefore, collaboration between the two parties to leverage each other’s complementary strengths is virtually the only viable path forward.

The Putian Network Collectively and Proactively Enters the Medical Aesthetics Installment Financing Sector. An investment partner may receive five to six business plans for medical aesthetics installment financing within a single week, with the Putian Network frequently represented behind these ventures. In fact, most medical aesthetics installment platforms have yet to achieve profitability. A core reason for this lies in the high bad debt rate. For entities within the Putian Network, their ownership of physical plastic surgery clinics constitutes their greatest advantage. By maintaining control over the entire cosmetic procedure process, they can better manage bad debt rates while simultaneously boosting sales volume.

If there is any player in the market capable of becoming a unicorn in medical aesthetics installment financing, internet finance giants are the most likely candidates. Although their traffic portals are not exclusively targeted at the medical aesthetics market, they boast a large user base, high user stickiness, and a well-established credit reporting system. Moreover, given the severe homogenization of medical aesthetics apps and the low industry barriers to entry, it is reasonable to speculate that internet finance giants will pose the greatest threat to startups in the medical aesthetics installment financing sector. Another potential contender is medical aesthetics SaaS companies. These firms hold core data of the medical aesthetics industry, and possessing such data creates opportunities to establish risk-based pricing systems. Since risk-based pricing is the core of any installment product, this is a significant advantage. However, a risk-based pricing system cannot be built by medical aesthetics SaaS companies alone simply by virtue of having data; it also requires the participation of financially robust institutions. Therefore, collaborative teams comprising medical aesthetics SaaS providers and financial institutions also have the potential to break through the competitive landscape.

The Standardized Development of the Medical Aesthetics Industry Is an Irresistible Trend

Medical aesthetics is the subsector with the highest rate of private participation in China’s healthcare services industry, with private institutions accounting for approximately 90% of the total. However, these entities are generally small in scale; there are only around 4,000 medical aesthetic institutions nationwide that meet the designated size criteria. A large number of unlicensed clinics continue to operate, resulting in low industry concentration. Furthermore, it is highly prevalent for a significant portion of beauty salons and hairdressing establishments to illegally administer hyaluronic acid injections. Market research by iResearch Group indicates that the primary concern deterring consumers from undergoing cosmetic surgery is fear of safety risks. These patient concerns directly highlight the chaotic landscape of the medical aesthetics industry, characterized by a mix of reputable and dubious providers and a lack of professionalism among practitioners.

Whether it is medical aesthetics insurance, installment payment plans for medical aesthetic procedures, or online medical aesthetic services, these emerging business models all prioritize selecting large-scale, reputable medical aesthetic institutions with proven strength and reliable guarantees. Meanwhile, as the government continues to strengthen regulatory oversight of the medical aesthetics industry, the sector will ultimately move in one direction: standardized development.

Copyright Statement

This report is produced by VCBeat. All text, images, and tables contained herein are protected by applicable trademark and copyright laws. Portions of the text and data have been sourced from publicly available information, with ownership retained by the original authors. No organization or individual may reproduce or distribute this report in any form without prior written permission from our company. Any unauthorized commercial use of this report shall constitute a violation of the Copyright Law of the People's Republic of China, other relevant laws and regulations, and applicable international conventions.

Disclaimer

This research report is based on information that VCBeat considers reliable and currently publicly available. VCBeat strives to, but does not guarantee, the accuracy and completeness of such information. Due to limitations in research methodologies, sample sizes, and the scope of data collection, the data presented herein only reflects the basic conditions of the surveyed population during the survey period. It serves solely for the current research purposes and provides general reference for the market and clients. Furthermore, VCBeat does not guarantee that the opinions or statements contained in this document will remain unchanged. At different times, VCBeat may issue reports with data, opinions, and projections that are inconsistent with those presented in this report.

VCBeat does not consider recipients of this report as its clients merely by virtue of their receipt thereof. This report is distributed only where permitted by applicable laws and regulations, solely for informational purposes, and shall not be construed as advertising in any manner. Under no circumstances shall the information contained herein or the opinions expressed constitute investment advice to any person. Where permitted by law, VCBeat and its affiliated entities may hold equity interests in the companies mentioned in this report and may provide or seek to provide fundraising, financial advisory, or other related services to such companies.

Note: I am Wang Guanglong, an author at VCBeat. If you are an investor interested in online medical aesthetics or an entrepreneur in the online medical aesthetics sector seeking media coverage, please feel free to contact me. We also welcome any leads on relevant companies. WeChat: touchlife1; Email: wang.gl@vcbeat.top