Japan's Universal Health Insurance System: A Sweet Burden Under the Pressure of an Aging Population

Lessons from Abroad Can Help Polish Our Own Jade. As a neighboring country, Japan has maintained sustained high-speed economic growth for a long time, offering valuable insights for China, particularly in the pharmaceutical industry. Japan’s pharma sector has not only met the domestic population’s healthcare needs but also expanded globally through innovative drugs and advanced technologies, fostering multinational pharmaceutical companies such as Takeda and Daiichi Sankyo. Observing the advancement path of Japanese pharmaceutical enterprises, their innovation capabilities are especially worthy of study for Chinese pharmaceutical companies undergoing transformation.

Huachuang Securities has long maintained a focus on Japan’s biopharmaceutical industry, producing the “Japan Biopharmaceutical Industry Watch” series of reports. VCBeat has obtained exclusive authorization to publish these reports. This article is the first installment, with subsequent issues to be compiled and released in due course.

Key Highlights of This Report

1. Preface.

Japan’s pharmaceutical and biotechnology sector has long been a focal point of our attention and research. Given the similarities in demographic structures and developmental backgrounds, the evolution of Japan’s pharma-biotech industry has provided clear guidance for China’s policy formulation, technological R&D, and model reform. Since 2014, we have continuously tracked its historical development and future trends, documenting our findings in written reports. We also organized two study tours to Japan’s pharmaceutical and biotechnology sector, aiming to gain deeper insights and draw lessons from Japan’s experience through close-range exchanges, thereby adapting these insights for our own use. Today, we are relaunching the “Japan Pharma-Biotech Industry Observation” report series. On one hand, we hope to share the accumulated expertise and reflections from our years of research on Japan; on the other, we believe that, amid the ever-changing political and economic landscapes of both countries—much like Foxconn’s investment in Sharp—the timing is now ripe for investing in Japan. Through our close-up observations, we aim to provide more enterprises and capital investors with first-hand information on Japan, striving to become your primary window into the Japanese pharmaceutical and biotechnology industry.

2. Introduction to Japan’s Pharmaceutical and Biotechnology Industry: The Universal Health Insurance System.

To understand the outcome, one must understand the underlying causes. The Japanese pharmaceutical and biotechnology industry has reached its current state largely due to the critical role played by government policy guidance. In this issue, we will focus on Japan’s world-renowned universal health insurance system to examine how the Japanese government has controlled and regulated the development of the pharmaceutical and biotechnology sector through structural adjustments on the payment side.

3. Tracking the Market Performance of Japan’s Pharmaceutical and Biotechnology Industry: Diverging from the Broader Market with Strong Outperformance.

The Japanese pharmaceutical and biotechnology sector has demonstrated robust market performance, with the TOPIX Pharmaceutical Index maintaining a long-term upward trajectory over the past three decades. In contrast to the “Lost Thirty Years” experienced by the broader TOPIX and the TOPIX Mothers Index, the TOPIX Pharmaceutical Index reached a historic high in 2015 and is currently undergoing consolidation at elevated levels. We have also selected Takeda Pharmaceutical, a well-established manufacturer of conventional chemical drugs, and Tella, a cell therapy startup, to provide a detailed analysis of market investment preferences.

4. Japan Pharmaceutical and Biotech Industry News Brief: China-Japan Cooperation Has Just Begun.

Japanese Government-Business Collaboration Enters China’s Healthcare Services Sector: Chinese Healthcare Consulting Firm Signs Remote Consultation and Overseas Referral Agreement with Minami Tohoku Medical Group, Japan’s Pioneer in Proton Therapy and BNCT Clinical Trials

Main Text

I. Overview of Japan’s Pharmaceutical and Biotechnology Industry: The Universal Health Insurance System

Japan, with its total healthcare expenditure ranking 16th and per capita healthcare spending ranking 19th among OECD member countries, supports a population structure with the highest aging rate globally, while boasting the world’s highest average life expectancy. This highly efficient health insurance system is not only a source of pride for the Japanese people but is also increasingly becoming a burden on them.

(I) Overview of the Universal Health Insurance System

Japan’s health insurance system can be divided into three main categories based on the type of insurance organization enrolled: Employees’ Health Insurance for employees of companies, factories, or stores; National Health Insurance for individuals engaged in agriculture, forestry, animal husbandry, and fisheries, as well as sole proprietors and freelancers; and the Late-Stage Elderly Medical Care System for those aged 75 and older.

Enrollees can also be divided into two major categories: the primary insured individuals who pay insurance premiums, and their dependents.

Chart 1 Flowchart of Japan's Health Insurance System

Source: Japan's Ministry of Health, Labour and Welfare; Huachuang Securities

There are three types of insurance organizations involved in the operation of medical insurance: first, employee health insurance organizations for individuals with stable employment; second, regional health insurance organizations covering farmers, foresters, fishermen, self-employed business owners, and freelancers; and third, the Late-Stage Elderly Medical Care Consortium for individuals aged 75 and older.

Chart 2 Status of Various Insurance Organizations

Source: Japan Ministry of Health, Labour and Welfare; Huachuang Securities

Insurance premiums are calculated by multiplying the insured’s standard wage income and standard bonus income by the insurance premium rate (divided into 47 brackets, refer to the quick-calculation table). The insured and the employer each bear half of the premium, which is paid monthly. The insurance premium rate consists of three components: a specific insurance premium rate to support the medical care system for the elderly in later life (uniform across China); a basic insurance premium rate to support the operations of the enrolled insurance organization (formulated by insurance organizations on a regional basis); and a long-term care insurance premium rate paid by insured individuals aged 40–64 who require care services (formulated by the insurance organization).

In 2014, the national average health insurance premium rate under the National Health Insurance Association was 10% (excluding long-term care insurance premiums). Given that the average annual income of Japanese salaried workers in 2013 was approximately ¥240,000, the annual health insurance contribution per household amounted to ¥240,000 × 10%, or about ¥24,000, with individuals bearing half of this cost, i.e., ¥12,000.

Chart 3 Overview of Insurance Premium Rates for Local Branches of the National Health Insurance Association

Source: Japan Health Insurance Association, Huachuang Securities

Note: Excludes the long-term care insurance premiums that individuals aged 40–64 requiring care services are required to pay.

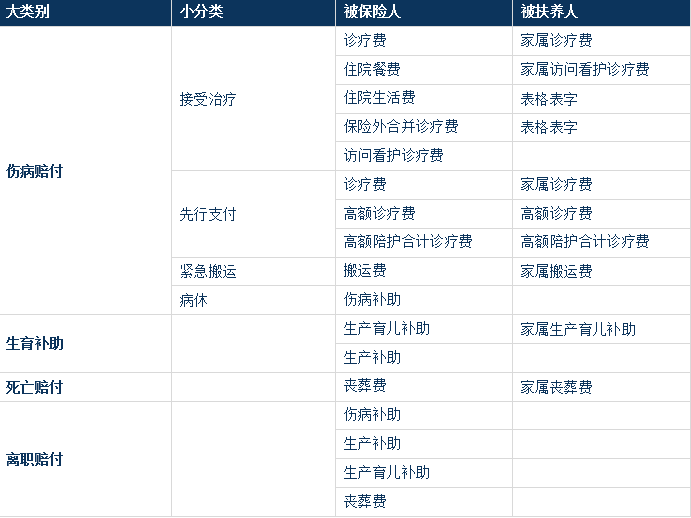

Insurance benefits can be broadly categorized into four types: (1) sickness and injury benefits, (2) maternity benefits, (3) death benefits, and (4) post-employment benefits. The insured individual is entitled to all four categories, while the insured’s family members (i.e., dependents) are eligible for a subset of these benefits.

Regarding reimbursement limits and methods, medical consultation fees are directly deducted at the time of payment according to the following proportions: 70% for individuals under 70 years of age, 80% for those aged 70–74, and 90% for those aged 75 and above. Medical institutions then submit claims for reimbursement to the respective insurance organizations. There is no cap on the reimbursement amount for medical consultation fees; however, a monthly ceiling is imposed on patients’ out-of-pocket expenses. This ensures that patients can access unlimited, state-subsidized medical services within their financial means and under reasonable circumstances.

Chart 4 Types of Insurance Claims

Source: Japan’s Ministry of Health, Labour and Welfare; Huachuang Securities

When individuals make payments at medical institutions, they are only required to cover a portion of the costs based on their age, with cost-sharing ratios ranging from 10% to 30%. In 2011, the out-of-pocket share accounted for approximately 12% of total healthcare expenditures. Although Japan’s total healthcare spending has risen year after year, the absolute amount borne by individuals has remained stable between ¥270 billion and ¥290 billion since 2003. This indicates that the Japanese government has made concerted efforts to curb the growth of out-of-pocket expenses, thereby alleviating the financial burden of healthcare access for the public.

Chart 5 The Ratio of Individual Burden to State Burden

Source: Huachuang Securities

Compared with the relatively low out-of-pocket expenses borne by individuals, the proportion of public funding in total healthcare expenditures has been rising year by year, reaching 38.4% in 2011. Meanwhile, in 2011, insurance premiums accounted for approximately 48.6% of total healthcare costs. This demonstrates that Japan’s comprehensive and convenient universal health insurance system is built on the dual pillars of substantial premium revenues and strong government support, neither of which can be dispensed with.

Figure 6 Out-of-Pocket Payments and Government Spending in Total Healthcare Expenditure

Source: Japan’s Ministry of Health, Labour and Welfare; Huachuang Securities

To address the mounting fiscal pressure caused by deepening population aging and to ensure that older adults have equitable access to appropriate medical services, the Japanese government abolished the Elderly Health Care System in 2008 and formally implemented the Late-Stage Elderly Medical Care System. Under the previous Elderly Health Care System, elderly individuals received additional medical benefits while remaining enrolled in their existing health insurance organizations. In contrast, the Late-Stage Elderly Medical Care System requires eligible individuals to automatically withdraw from their current health insurance plans upon reaching the age threshold of 75 and mandatorily join regional Late-Stage Elderly Medical Care Federations. Furthermore, the method for paying insurance premiums was changed to automatic deductions from pensions, among other adjustments.

Chart 7 Outline of the Late-Stage Elderly Medical System

Source: Japan's Ministry of Health, Labour and Welfare; Huachuang Securities

When the system was formally implemented in 2008, approximately 13 million eligible individuals were transferred from various health insurance organizations to the Health Insurance System for Late-Stage Elderly People (Kouki-Koureisha), with per capita medical expenses amounting to around RMB 46,200 that year. By 2012, the number of insured persons under the Late-Stage Elderly Medical Care System had reached 15 million, and per capita medical expenses had climbed to RMB 54,100. The simultaneous increase in both volume and cost inevitably exerted significant financial pressure on the health insurance system. In 2007, expenditures under the elderly healthcare system accounted for 30.1% of total medical costs for that year. After the transition to the Late-Stage Elderly Medical Care System in 2008, this proportion rose sharply, reaching 31.8% in 2011.

Chart 8 2008-2012Insured Persons and Premiums under the Late-Stage Elderly Medical Care System

Source: Ministry of Health, Labour and Welfare of Japan; Huachuang Securities

Chart 9 2007-2011Proportion of the Medical System for the Elderly in the Later Years

(II) Challenges Facing the Universal Health Insurance System

As previously mentioned, 40% of the costs for the Late-Stage Elderly Medical Care System are borne by various insurance organizations. To cover the increasingly high support payments for this system, 1,061 out of 1,431 industry-based health insurance societies incurred deficits in 2012, accounting for approximately 74%, with the total deficit reaching 26.6 billion yuan. Meanwhile, the National Health Insurance organizations, comprising 1,717 entities, recorded a deficit of approximately 17.8 billion yuan in 2011.

Chart 10 2008-2011Deficit Situation of the National Health Insurance Organization

The enrollment rate of the National Health Insurance Organization dropped to its lowest point in 2009, at 88.01%. This was primarily due to the transfer of all insured individuals aged 75 and older—a group with relatively high enrollment rates—following the establishment of the Late-Stage Elderly Medical Care System in late 2008. Meanwhile, despite the implementation of various premium reduction measures by the National Health Insurance Organization to boost enrollment, the rate reached only 89.31% in 2011, remaining below 90%, largely owing to economic downturn and increased insurance premiums. Furthermore, when calculated on a household basis, the enrollment rate for the National Health Insurance Organization was below 80%.

Chart 11 2003-2011National Health Insurance Organization Enrollment Rate by Year

Meanwhile, unlike employee health insurance, which requires stable employment as a condition for enrollment, National Health Insurance—primarily targeting self-employed individuals and those engaged in agriculture, forestry, animal husbandry, and fisheries—has gradually become a haven for the unemployed and freelancers, influenced by the economic downturn in recent years. In 2011, the unemployed accounted for 42.6% of enrollees, four times the proportion in 1961. The share of employees, predominantly in non-regular employment, rose from 13.9% to 35.8%, while the proportion of workers in agriculture, forestry, animal husbandry, and fisheries declined from 44.7% to 2.8%, and that of self-employed individuals dropped from 24.2% to 14.5%.

Figure 12 Composition of National Health Insurance Personnel

(3) Impact of the Universal Health Insurance System on the Government and the Industry

In summary, universal health insurance is not only a hallmark of Japan’s healthcare system but has increasingly become a “sweet burden” for its government and citizens. To curb healthcare expenditures, the Japanese government has implemented a series of measures, including establishing an independent health insurance system for the elderly, regularly reducing drug prices, and actively promoting the use of generic drugs. These efforts aim to carve out a viable path amid the dual pressures of population aging and declining birthrates, exerting profound influence and directional impact on Japan’s entire pharmaceutical and biotechnology industry. For further details, please continue to follow our series of reports.

II. Tracking the Market Performance of Japan’s Pharmaceutical and Biotechnology Industry

(I) Overall Performance of the Pharmaceutical and Biotechnology Industry

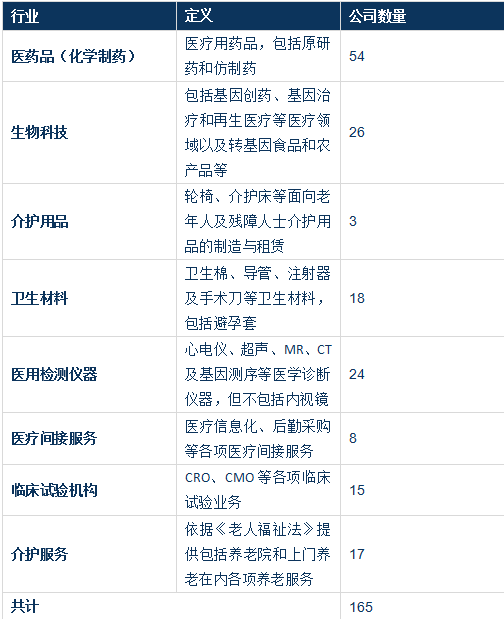

Japan’s pharmaceutical and biotechnology industry can be categorized into eight major segments: pharmaceuticals (chemical drugs), biotechnology, long-term care products, hygiene materials, medical diagnostic equipment, indirect medical services, clinical trial organizations, and long-term care services. Under Japan’s Medical Care Act, all medical institutions must maintain a non-profit status; therefore, hospitals and clinics in Japan do not meet the listing requirements for public offerings. However, long-term care service companies that provide elderly care or rehabilitation services are eligible for listing.

Figure13Classification of Japan’s Pharmaceutical and Biotechnology Industry and Number of Listed Companies (as of the end of 2013)

Source: Huachuang Securities

To examine the market performance of Japan’s pharmaceutical and biotechnology industry over the past 30 years, we selected the TOPIX Pharmaceuticals Index, compiled by the Tokyo Stock Exchange (TSE), Japan’s largest securities exchange, as a representative benchmark. We also analyzed the performance trends of the TOPIX Pharmaceuticals Index relative to the TOPIX (Tokyo Stock Price Index) and the TSE Mothers Index from May 1, 1986, to the present.

As can be seen, the TOPIX index started at around 1,300 points in May 1986. Having weathered the economic bubble of the late 1980s, the dot-com bubble of the early 2000s, the financial crisis of 2008, and Abenomics in 2015, the index has experienced significant volatility. It once climbed to a peak near 2,900 points, but closed at 1,320.19 points on May 13, 2016, representing a discount of more than 50% from its highest level. This trajectory is a true reflection of Japan’s “Lost Thirty Years.” Meanwhile, the TSE Mothers Index, representing Japan’s growth enterprise market, was officially launched in late 1999. Driven by the pre-2006 internet boom, it reached a high of 2,800.68 points. However, as many representative internet companies delisted due to operational issues, the index plummeted to a low of 269.41 points, losing 90% of its value. It only began a gradual recovery after Shinzo Abe returned to power in 2013, closing at 1,207.02 points on May 13, 2016. In contrast, the performance of the TSE Pharmaceutical Products Industry Index has been remarkable. Starting at around 1,000 points on May 1, 1986, it dipped to approximately 800 points in mid-1995. Since entering the 21st century, it has risen steadily, reaching phase highs of 2,000 and 2,300 points. From 2011 onward, it maintained an upward trend, hitting a peak of 2,900 points in 2015. Currently, it is consolidating at a high level around 2,600 points, closing at 2,653.96 points on May 13, 2016. Compared to the TOPIX and the TSE Mothers Index, the premium rates of the TSE Pharmaceutical Products Industry Index are 101.03% and 119.88%, respectively.

Meanwhile, we also examined the comparison of price-to-earnings (P/E) and price-to-book (P/B) ratios between the pharmaceutical industry and the overall market. For companies listed on the TSE First Section, the aggregate P/E and P/B ratios for the pharmaceutical industry were 34.1x and 2.2x, respectively, whereas those for the entire market were only 16.1x and 1.1x, meaning the former was more than double the latter. For companies listed on the TSE Second Section, the aggregate P/E and P/B ratios for the pharmaceutical industry were 104.6x and 1.2x, respectively, compared to just 15.5x and 0.9x for the overall market, indicating an even more pronounced disparity in P/E ratios. Additionally, since companies listed on the TSE Mothers market are permitted to report negative profits, we compared only their P/B ratios; the P/B ratio for the pharmaceutical industry was approximately 1.6 times that of the overall market. These figures collectively demonstrate strong investor enthusiasm for the pharmaceutical industry.

Chart14Trends in the Pharmaceutical Industry Index, TOPIX, and the Tokyo Stock Exchange Mothers Index

Source: Huachuang Securities

Chart15Comparison of P/E and P/B Ratios: Pharmaceutical Industry vs. Overall Market

Source: Huachuang Securities

(II) Representative Listed Companies

A Single Leaf Reveals the Coming of Autumn: We selected two representative pharmaceutical companies to examine their stock price trends and operational performance. One is Takeda Pharmaceutical Company Limited, a centuries-old global giant in chemical pharmaceuticals that is actively pursuing transformation; the other is Tella, Inc., which focuses on tumor immunotherapy and whose dendritic cell (DC) vaccine technology and applications are at the forefront globally. Takeda’s P/E and P/B ratios stand at 43.40x and 1.96x, respectively, while Tella’s are -14.54x and 9.21x, respectively.

Figure16The company's developed tumor DC vaccine has cumulatively conducted a total of treatments10100Example (as of2015year-end)

Source: Company website, Huachuang Securities

1. Takeda Pharmaceutical Company Limited

Founded in 1781, Takeda Pharmaceutical Company initially built its business on pharmaceutical sales. After more than 230 years of development, it has become Japan’s largest and the world’s 13th-largest multinational pharmaceutical company (2013, PHARMACEUTICAL EXECUTIVE). Although Takeda has launched blockbuster drugs such as lansoprazole, leuprorelin, and candesartan, its growth has slowed in recent years due to multiple factors, including patent expirations, increasing difficulties in small-molecule drug R&D, and Japanese government controls on pharmaceutical expenditures. In response to these challenges, Takeda is intensifying its R&D investments to identify the next blockbuster drug, while simultaneously expanding into biopharmaceuticals and emerging markets through overseas mergers and acquisitions and the appointment of a foreign CEO. Whether this traditional pharmaceutical giant can regain its former glory remains to be seen.

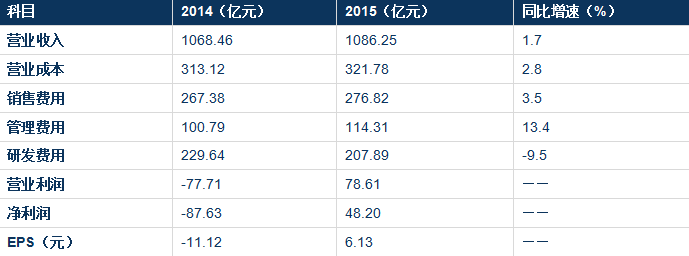

Takeda reported operating revenue and net profit of JPY 108.625 billion and JPY 4.82 billion, respectively, in 2015. Operating revenue increased by 1.7% year-on-year, while the gross profit margin remained at approximately 70%. Net profit turned from loss to profit, driven by a decrease in the R&D expense ratio from 21.49% to 19.19% and a significant reduction in other operating expenses. Among these, the company’s current key development areas—gastrointestinal drugs and central nervous system (CNS) drugs—contributed revenues of JPY 17.892 billion and JPY 3.42 billion, respectively, representing year-on-year growth of 23.6% and 37.3%. These segments are expected to remain the primary drivers of the company’s performance growth in the future. In contrast, although oncology drugs, another key focus area, generated JPY 20.218 billion in revenue last year, the year-on-year growth rate was only 1.0%, indicating an urgent need for the company to identify new blockbuster products in this field. From a geographic sales perspective, the United States and emerging markets continued to be the main contributors to the company’s revenue growth, with year-on-year increases of 12.4% and 4.8%, respectively. Notably, China’s sales revenue reached JPY 7.47 billion, growing by 8.0% year-on-year, making it the leading driver within emerging markets. Meanwhile, Takeda’s operating revenue in Japan has been declining annually; although drug sales revenue amounted to JPY 32.55 billion in 2015, the year-on-year growth rate was -3.3%.

Figure172014-2015 Corporate Financial Summary

Source: Company announcements, Huachuang Securities

Chart18Sales Revenue from the Company’s Key Focus Areas, 2014–2015

Source: Company announcements, Huachuang Securities

2. Tella Inc.

Founded in 2004 and listed on the Tokyo Stock Exchange Mothers market, the company is an emerging startup that focuses on cell therapy and regenerative medicine. It is dedicated to the research and development of immunocellular therapies for cancer, while also providing its proprietary technologies to medical institutions as a core business pillar. By the end of 2015, the company’s dendritic cell immunotherapy (DC vaccine) had been adopted by 37 medical institutions across Japan, treating 10,100 cancer patients, with pancreatic cancer patients constituting the largest group at approximately 2,000 cases. Generally, the average survival time for pancreatic cancer patients from diagnosis to death is only one year. Therefore, the company set the post-treatment observation period for pancreatic cancer patients at 1–1.5 years. Notably, the longest-surviving patient treated by the company has remained healthy for over three years post-surgery.

Chart19The tumor DC vaccine developed by the company has cumulatively conducted a total of10100Example (as of2015End of Year)

The core competitiveness of the company’s dendritic cell (DC) vaccine stems from its patented technologies for culturing WT1 cancer antigens and DC cells. WT1, initially identified as the oncogene responsible for Wilms’ tumor in pediatric renal cancer, has since been confirmed to be widely expressed in solid tumors such as pancreatic, lung, and colorectal cancers, as well as in hematologic malignancies like leukemia. In the National Institutes of Health’s (NIH) evaluation and ranking of 75 cancer antigens to date, WT1 received an exceptionally high score, establishing it as one of the most suitable cancer antigens for tumor vaccines. Furthermore, the maturation of DC cells is a critical factor in the application of DC vaccines. The company’s technology, originally sourced from the Institute of Medical Science at the University of Tokyo and subsequently refined through multiple improvements, achieves a clinical-grade DC cell concentration as high as 1×10⁷/cm³—more than ten times that of comparable technologies in the United States.

Chart20The company holds a patented WT1 cancer antigen, which exhibits an extremely high detection rate across nearly all solid tumors and hematologic malignancies.

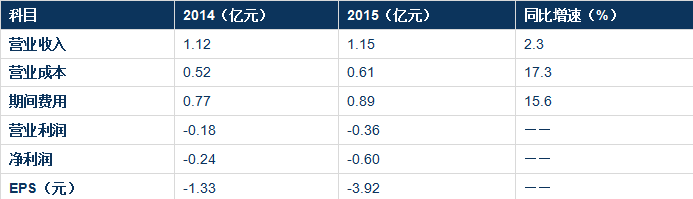

In 2015, the company reported operating revenue of RMB 115 million, a year-on-year increase of 2.3%. However, due to sustained increases in selling expenses and R&D and administrative costs associated with its application to include DC vaccine therapy in the national medical insurance coverage, the company’s net profit stood at a loss of RMB 60 million. Nevertheless, it is projected that following inclusion in the medical insurance scheme, the market potential for the company’s products in pancreatic cancer treatment alone will expand by more than 35-fold. Meanwhile, the company has decided to initiate medical insurance reimbursement applications for lung cancer-related indications in the near term.

Chart212014–2015 Corporate Financial Summary

Source: Company announcements, Huachuang Securities

III. News Flash from Japan’s Pharmaceutical and Biotech Industry

(1) Japanese Government and Business Join Forces to Expand into China’s Healthcare Market

Medical device company Trim, which initially built its business on manufacturing and selling hydrogen-rich water, has announced that its joint venture in Hong Kong plans to raise approximately RMB 100 million within six months. The funds will be used to establish a 200-bed specialized hospital for chronic diseases in Haidian District, Beijing, with diabetes management and hemodialysis among its core services. Additionally, the company intends to develop a chain hospital group across nine cities in China, including Shanghai and Dalian, over the next five to seven years.

The Japanese government plans to designate this new hospital chain group as the primary recipient of Japan’s medical exports and the main service provider for the new hospitals. All physicians and nurses will be dispatched from Japan under the auspices of the Japanese government. Professor Masaki Nakayama’s team from Fukushima Medical University, renowned experts in diabetes treatment, will participate in the operation of the new hospitals. Meanwhile, companies involved in the development of dietary products for diabetes prevention, such as Mitsubishi Corporation, also plan to join this initiative.

Commentary: Trim, the operating entity, lacks experience in managing specialized chronic disease hospitals, and it remains questionable whether the physicians and nurses dispatched by the Japanese side can adapt to China’s healthcare service environment. Nevertheless, as a landmark event marking the entry of Japanese healthcare services into the Chinese market, we will continue to monitor its developments.

(II) Annuo Zhimei Partners with Japan's Minami Tohoku Medical Group to Launch Remote Consultation and Overseas Referral Services

Beijing Annuo Zhimei Health Technology Co., Ltd. has partnered with Meinian Onehealth Healthcare Industry Group and Japan Minami-Tohoku Medical Group to jointly provide early cancer screening and overseas referral services. With over 50 medical service institutions across the three northeastern prefectures of Fukushima, Miyagi, and Aomori, Japan Minami-Tohoku Medical Group covers multiple business areas including healthcare, elderly care, and disability rehabilitation. It is Japan’s first private medical institution to offer proton therapy and currently the only one conducting clinical trials on BNCT (Boron Neutron Capture Therapy).

Over the past eight years of providing proton therapy, the Group has treated 3,468 patients, with head and neck cancer, lung cancer, and esophageal cancer being the top three most frequently treated indications. In the treatment of non-small cell lung cancer (NSCLC), the 2-year local control rates and 2-year survival rates for Stage I patients were 95.7–98.0% and 76.0–87.9%, respectively, while for Stage III patients, the 2-year local control rate and 2-year survival rate were 36.4% and 51.1%, respectively. For esophageal cancer, the 3-year survival rate was 90% for Stage I patients and 55% for Stage II and III patients.

Comment: Proton therapy is currently one of the most advanced radiotherapy modalities for cancer treatment worldwide. Japan has accumulated extensive experience in this field, and we anticipate future collaboration between China and Japan in this area.

Editor’s Note: This article is the first installment of Huachuang Securities’ observation series on Japan’s pharmaceutical and biotechnology industry. We will continue to publish updates for our readers’ benefit. Your attention is greatly appreciated.

Series Report Directory

Phase III: Traditional Chinese Medicine in Japan: Annual Output Value of Only RMB 10 Billion, with Just One Listed Company

Issue 4: Japanese Drug Prices Under Government Control: Strained Health Insurance Reimbursements and Constrained New Drug R&D Pricing