After a period of unrestrained growth in 2014 and rapid development in 2015, the digital health sector entered a phase of transformation in 2016. In 2016, the once-omnipotent internet industry faced significant challenges, while a "capital winter" seemed to become the dominant theme in the venture capital and private equity community. The digital health sector also endured this cold spell. Investment enthusiasm remained high in the second quarter (Q2), but began to gradually slow down in the third (Q3) and fourth quarters (Q4). Amidst the cooling investment climate and slightly tighter capital supply, the number of healthcare deals securing funding repeatedly hit record highs, as an increasing number of investment institutions recognized the promising opportunities in digital health.

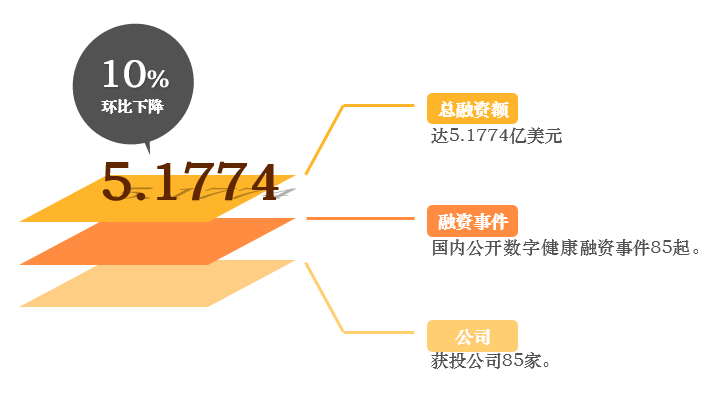

Trading volume rose, while financing amounts saw a slight month-on-month decline; investment enthusiasm in digital health remains strong.

StillEarly StageProject-focused, early-stageThere is a trend of increasing transaction volume for projects.In China, Genomics, Fitness, and Maternal & Infant Care Have Become Key Investment Targets.

The number of investments in the O2O model has declined significantly, while the number of investments in the B2B model has seen a slight increase.

126 investment institutions entered the market, with Oriental Haifu and Matrix Partners China among the most active in this period.Focusing simultaneously on genetic services, chronic disease management, and maternal and child health in both domestic and international markets.

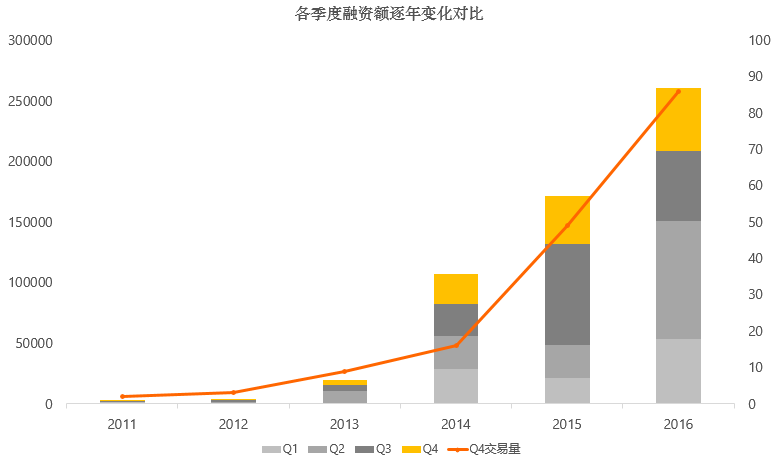

Annual Financing Data ChangesJudging from the transaction volume of investment and financing in recent years, it has maintained a growth trend. Since 2014, digital health entrepreneurship and innovation have begun to explode, and the capital market has continued to inject funds.Q4 2016 financing amounted to $517.74 million, a 33% year-on-year increase and a 10% quarter-on-quarter decrease.Compared with other periods of the year, Q4 is a low season for investment.

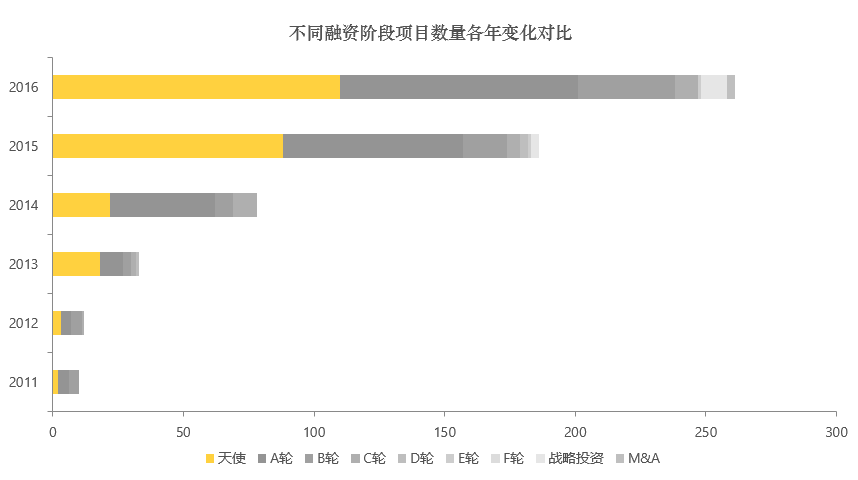

Annual Distribution Changes in Financing StagesAs of the fourth quarter,2016Investment trends in the year remained focused on early-stage projects, totaling201Starting from , the transaction volume of early-stage projects has gradually increased. It is expected that2017The growth in the number of early-stage financing deals will slow down, while the total amount of financing will continue to rise.

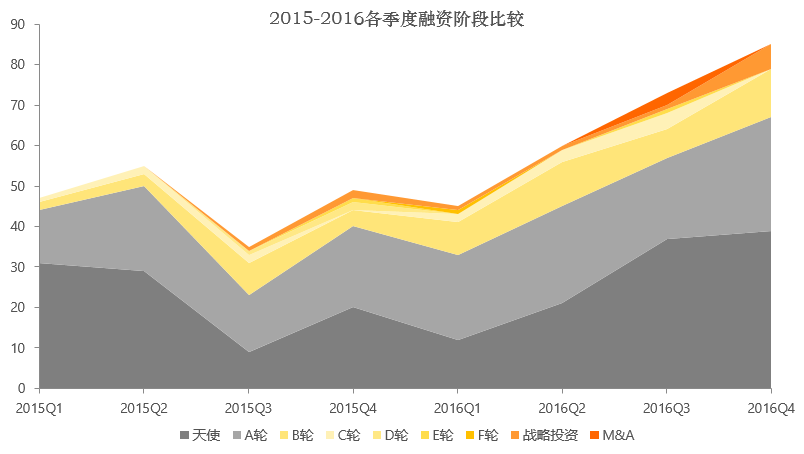

Quarterly Changes in the Distribution of Financing StagesIn 2016, transaction volume rose steadily, peaking in Q4 with 85 financing deals.Transaction volume in Q4 2016 increased by 73.5% year-over-year and by 16.4% quarter-over-quarter.

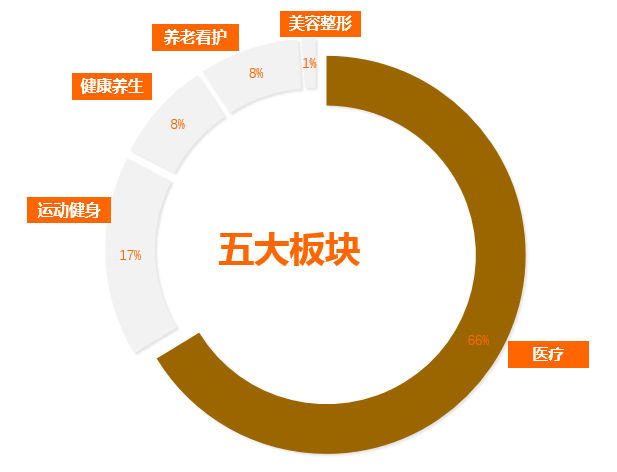

Distribution of the Five Major Segments of Digital HealthMedical projects dominated, with a total of 57 cases, accounting for approximately 66%; sports and health projects ranked second, with 14 cases, representing 17%.Healthcare projects raised $456.44 million, accounting for 61% of the total domestic financing amount this quarter. Among these, genetic services, smart hospitals, and pharmaceuticals were the top-funded sectors, contributing 75% of the total financing for healthcare projects.

There were seven active vertical segments in Q4 2016.

Top 10 Subsectors by Highest Transaction VolumeThe total financing amount of the top 10 sub-sectors accounted for 87.7% of the total financing.The gene services sector attracted the highest investment amount, with Novogene securing the largest single funding round this quarter, completing a RMB 500 million Series B financing in November.In terms of average transaction value, the pharmaceutical sector saw relatively high financing amounts, primarily driven by Dingdang Kuaiyao’s RMB 300 million Series A funding round completed in December.

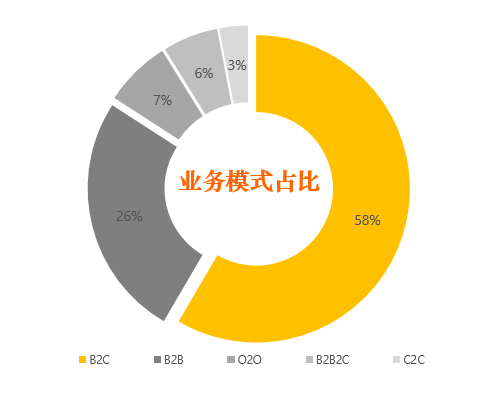

Business Model DistributionThere are four main business models, with B2C projects accounting for 58%. The target populations include patients, consumers, children, the elderly, and women.The number of B2B projects has seen a significant year-on-year increase. While competition in the consumer market continues to intensify, the business sector remains a growth market, with capital investment in this area steadily strengthening.

Product Form Distribution

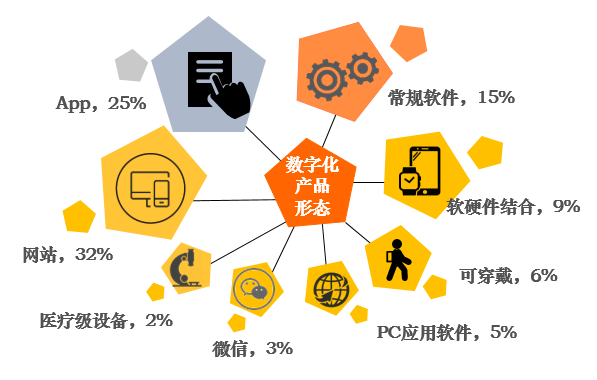

This quarter, the funded projects encompassed eight product forms, primarily websites and mobile platformsAppas the main focus.Conventional software primarily consists of healthcare information systems.In the field of smart hardware, the integration of software and hardware has become the mainstream direction of development.

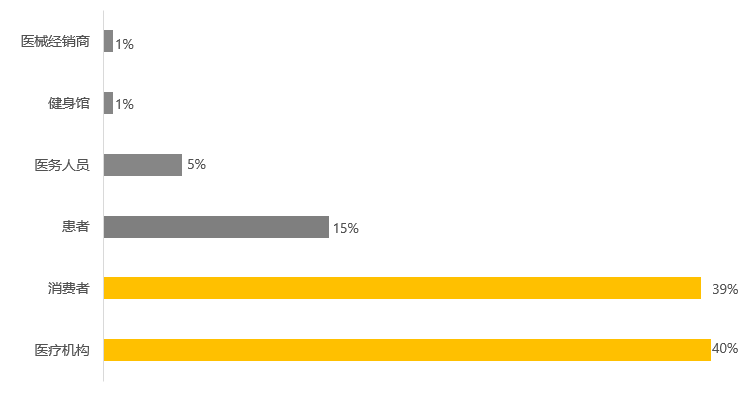

Service Population DistributionService recipients are categorized into six major user segments, with consumers and medical institutions emerging as the primary target groups for strategic deployment this quarter.Consumer-facing sectors are dominated by consumer-grade digital health, encompassing areas such as maternal and child care, health management, elderly care, medical aesthetics, and oral health.The target audience primarily consists of healthcare institutions in the field of medical informatics, followed by those in genetic services.

A total of 126 investment firms participated in digital health project investments, representing a 46.5% increase compared to Q3. Additionally, nine individual investors participated in digital health investments during Q4.There are five active investment institutions, namely Orient Hifu, Matrix Partners China, Puhua Capital, CMB International, and Chongshan Capital, with their participation focused on the early to mid-stages.

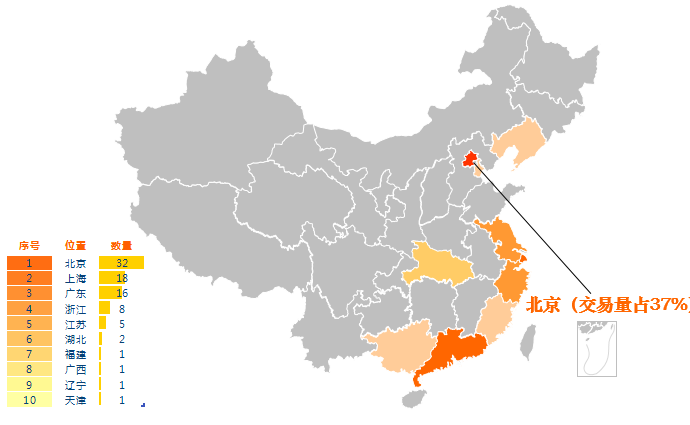

Distribution of Active RegionsIn terms of transaction volume, Beijing continues to lead with 32 deals.

Top 10 Investment and Financing DealsThe top ten deals in Q4 2016 accounted for approximately 63% of the total financing amount.Of these, five transactions occurred in the field of genetic services, while the remaining deals were distributed across smart hospitals, pharmaceuticals, rare diseases, maternal and infant care, and fitness.

Geographic Distribution of Overseas Funded ProjectsThis quarter, 101 investment deals were recorded in mainstream domestic and international healthcare markets, with total financing reaching $2.18 billion.

A comparison of the distribution of investment rounds for funded projects in China and the United States reveals that U.S. funded projects are relatively evenly distributed across early and mid-stage rounds, whereas Chinese funded projects are primarily concentrated in the early stage.

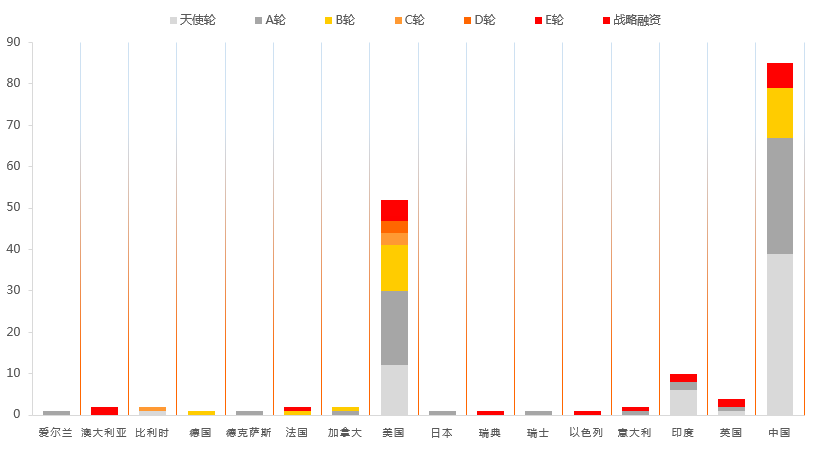

The most active regions for investment in the medical and healthcare sector abroad are the United States, India, and the United Kingdom.

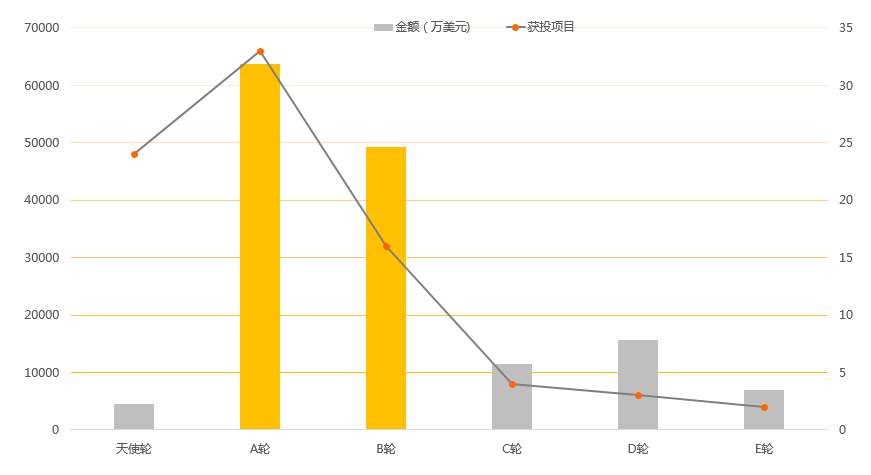

Distribution of Funding Rounds for Overseas Invested ProjectsIn Q4, overseas investment deals in the healthcare sector were predominantly Series A and Series B rounds, totaling 49 transactions and accounting for 59.8% of the total number of investments (excluding strategic investments).

Excluding the angel round, the average funding amount for all other rounds exceeded $10 million, with Series D recording the highest average at $52 million.

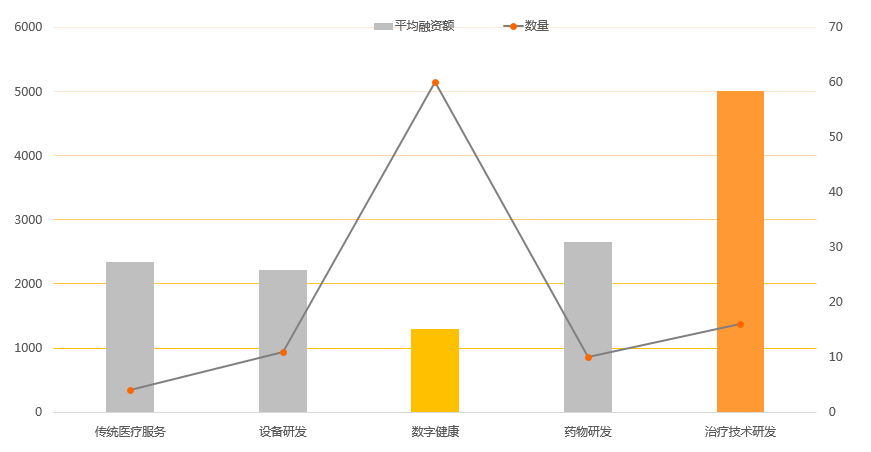

Distribution of Investment Areas in Overseas Medical and Healthcare ProjectsThere were 60 financing events in the digital health sector, accounting for 59.4% of the total number of transactions. However, as digital health companies predominantly operate under an asset-light model, the total financing amount in this sector was lower than that in the traditional healthcare sector.

The average financing amount in the field of therapeutic technology R&D stands at $50 million, with frontier medical technologies remaining highly sought after by capital.

Top 7 Subsectors in the International Digital Health MarketQ4: Overseas digital health funding accounted for 35.7% of total healthcare funding.

The health management sector recorded 11 transactions, with a total transaction value of $176 million, making it the sub-sector with both the highest number of deals and the largest amount of investment.

Genetic services, chronic disease management, and maternal and child health are the areas of simultaneous focus both domestically and internationally in Q4.

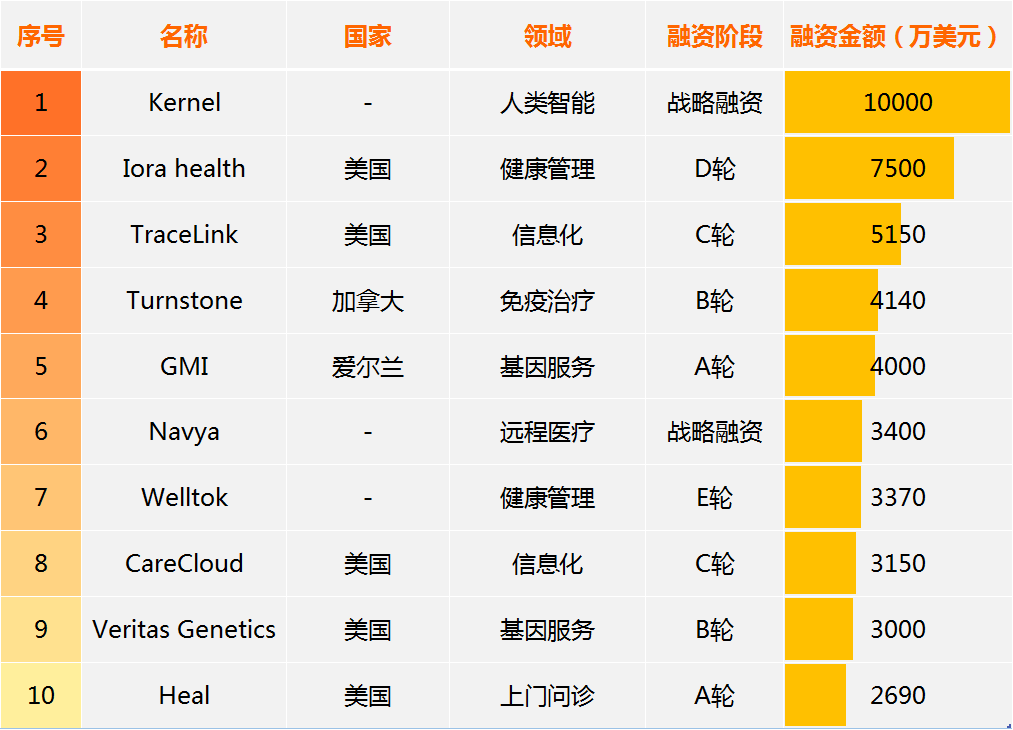

Top 10 Most Funded Digital Health Projects AbroadIn Q4, the digital health project with the highest funding amount was Kernel. Among the top 10, there were two projects each in the fields of health management, medical informatization, and genetic services.

Copyright Notice

This report is produced by VCBeat. All text, images, and tables contained herein are protected by applicable trademark and copyright laws. Portions of the text and data have been sourced from publicly available information, with ownership retained by the original authors. No organization or individual may reproduce or distribute this report in any form without prior written permission from our company. Any unauthorized commercial use of this report shall constitute a violation of the Copyright Law of the People's Republic of China, other relevant laws and regulations, and applicable international conventions.

Disclaimer

This research report is based on information that VCBeat considers reliable and currently publicly available. VCBeat strives to, but does not guarantee, the accuracy and completeness of such information. Due to limitations in research methodologies, sample sizes, and the scope of data collection, the data presented herein only reflects the basic conditions of the surveyed population during the survey period and serves solely for the current research purposes, providing a general reference for the market and clients. Furthermore, VCBeat does not guarantee that the views or statements contained in this report will remain unchanged. At different times, VCBeat may issue reports with data, opinions, and projections inconsistent with those contained herein.

VCBeat does not consider recipients of this report as its clients by virtue of their receipt thereof. This report is distributed only where permitted by applicable laws and regulations and solely for informational purposes; it does not constitute any form of advertising. Under no circumstances shall the information contained herein or the opinions expressed be construed as investment advice to any person. Where permitted by law, VCBeat and its affiliates may hold equity interests in the companies mentioned in this report and may provide or seek to provide capital raising, financial advisory, or other related services to such companies.