Four Key Lessons from the Collapse of Southern Cross Healthcare: A Cautionary Tale for the Global Elderly Care Industry

By Zhang Chunyu

Whether in the United Kingdom or China, for the elderly care industry to develop sustainably and healthily, enterprises must be profitable. However, private elderly care institutions in China are still in the early stages of industrial development. Constrained by various conditions, it is difficult to increase occupancy rates and achieve break-even in a short period. Therefore, whether the government can effectively implement the policy of “integrating and repurposing idle social resources” to address rental cost issues for private elderly care institutions is a key factor determining whether substantial social capital will flow into the elderly care service sector.

Southern Cross Healthcare Group, the UK’s largest elderly care provider with 750 affiliated nursing homes, over 40,000 employees, and management of more than 47,000 beds, staggered through the 2008 economic crisis. Although it struggled on for another three years, it ultimately could not escape the fate of nearing bankruptcy and being sold off.

The United Kingdom entered an aging society at least 50 years earlier than China, with its aging process spanning 80 years. The year 2013 is widely recognized within China’s elderly care industry as its inaugural year, marked by the entry of numerous private enterprises into the sector, signaling the onset of genuine market-oriented operations. In contrast, China’s aging process took only 18 years (1981–1999), and the pace of population aging continues to accelerate. Fortunately, most Western countries entered an aging society before us; their successful experiences offer valuable references, while the challenges they have encountered provide important insights and lessons.

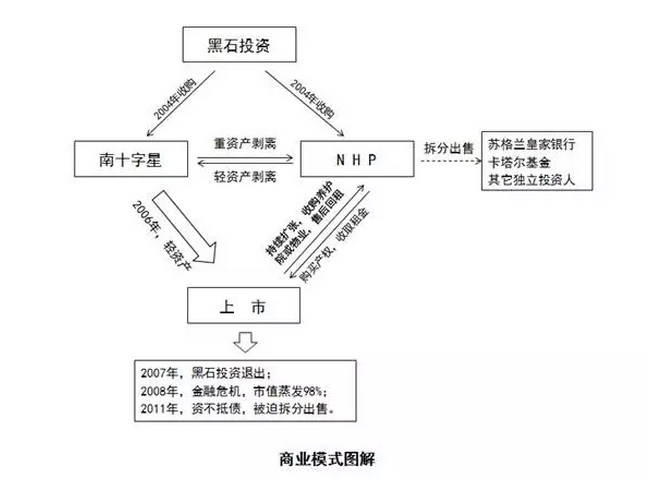

John Morton founded Southern Cross in 1996. Within just six years, by 2002, the company had expanded to 140 chain facilities, ranking as the largest care home group in the UK and the third-largest in Europe. In 2004, the renowned U.S. investment firm The Blackstone Group acquired Southern Cross for £160 million. In the same year, it also acquired NHP (a provider of senior housing real estate and elderly care operations) for £560 million. Subsequently, Blackstone restructured the businesses: it divested Southern Cross’s asset-heavy components, transforming it into an asset-light elderly care operator. Meanwhile, it spun off NHP’s asset-light business (elderly care operation management) to Southern Cross, thereby turning NHP into an asset-heavy senior housing real estate company focused on property leasing and sales, which also included collecting rent paid by Southern Cross.

The two subsidiaries operate independently and maintain separate accounting.

In 2006, Southern Cross Healthcare, which operated 578 chain nursing homes, successfully listed on the London Stock Exchange. After securing financing, the group continued to expand by acquiring other nursing homes or purchasing properties for renovation, then selling the ownership to NHP to generate profits while simultaneously leasing back the sold properties for operation. Leveraging this sale-and-leaseback model, Southern Cross performed strongly in the capital markets, with its market capitalization exceeding £1 billion at one point before 2008.

By July 2007, Blackstone Group had already realized gains exceeding £500 million solely from the appreciation of its stock holdings in the securities market, excluding the profits obtained from selling off all shares upon exit.

The good times did not last long. By early 2011, Southern Cross was severely insolvent and on the verge of bankruptcy, with its market capitalization plunging to £12 million—a 98% drop from its peak value.

It is understandable for elderly care operation and management companies to adopt an asset-light model, successfully go public, and continue to expand, with their stock prices soaring all the way. If the dimension of time is ignored in the short term, the business model led by Blackstone Group is undoubtedly successful. However, this success must be based on two important prerequisites.

First, the macroeconomic environment is booming, primarily driven by the sustained appreciation of real estate.Because Southern Cross acquired new care homes or properties through financing and loans, it sold them under the premise of guaranteeing stable rental income for NHP or other investors (with a 2.5% annual increase) while the properties themselves had potential for appreciation. Once hit by an economic crisis like that of 2008, the bursting of the real estate bubble caused the properties purchased by Southern Cross to sharply depreciate and become unsellable, leading to an immediate break in cash flow. To make matters worse, the rent increased annually; in 2011, Southern Cross Group's payable rent reached £250 million, exceeding 25% of its annual revenue.

Second, we must rely on the steady increase in occupancy rates; before 2008, the Group’s occupancy rate remained stable at approximately 92%.In the aftermath of the economic crisis, the UK central government significantly reduced public expenditure and encouraged elderly individuals to adopt more cost-effective home-based care models. As government payments or subsidies accounted for as much as 70% of the group’s client base, the average occupancy rate declined to 84%, exacerbating operational deficits and insolvency. Ultimately, the company was broken up and sold off under government direction, marking the exit of this once-preeminent eldercare giant from the historical stage.

Therefore, the author believes that the external factor leading to the collapse of the UK's Southern Cross Healthcare Group was the 2008 financial crisis, while the internal factor was its high-risk business model.

Insight 1

Capital is a double-edged sword. Leveraging its power enables rapid breakthroughs and market expansion. Yet how can one strike a balance between maximizing the commercial returns sought by capital and the inherently low-margin, welfare-oriented nature of the elderly care industry? After achieving an investment return of more than fourfold within three years, Blackstone Group gracefully exited the market. While one must admire its sophisticated operational strategies as an investor, along with its precise timing for market entry and exit, the business model it spearheaded did not withstand the test of time.

Insight 2

The more concentrated the customer base, the higher the commercial risk. For Southern Cross Care, the government is its largest client. Unlike competitors such as Bupa, which began strategically positioning themselves early on and have continuously developed the out-of-pocket payment market, Southern Cross Care has not done so to the same extent. Consequently, reductions in government fiscal spending and shifts in policy direction have a very limited impact on elderly care institutions that serve a predominantly self-paying clientele.

Insight 3

The primary costs in the elderly care service industry stem from two sources: labor and rent (public elderly care institutions are excluded from this discussion). Labor constitutes a variable cost, while rent is a fixed cost. From an operational perspective, Southern Cross’s rental costs exceed 25% of its revenue, requiring an occupancy rate of no less than 90% to achieve profitability, thereby imposing significant operational pressure.

Whether in the UK or China, for the elderly care industry to develop sustainably and healthily, enterprises must be profitable. However, private elderly care institutions in China are still in the early stages of industrial development, and various constraints make it difficult to increase occupancy rates and achieve break-even in the short term. Therefore, whether the government can effectively implement the policy of “integrating and repurposing idle social resources” to address rental costs for private elderly care institutions is a key factor determining whether substantial social capital will flow into the elderly care service sector.

Insight 4

An examination of the leading corporate groups in the UK’s elderly care sector reveals that they all follow a path characterized by branding, chain operations, large-scale expansion, and specialization, with each managing more than 200 facilities. For instance, Four Seasons Health Care operates a chain of 500 facilities, Bupa has 310, and HC-One has 241. Therefore, the author boldly predicts that within the next 15 years, China will certainly see the emergence of large-scale elderly care operators managing more than 1,000 facilities. However, it will require considerable patience to determine which company will become the industry’s first unicorn.

Author: Zhang Chunyu,Graduated with an MBA from the University of Sheffield, UK。Having resided in the United Kingdom for many years, I have over a decade of experience in the elderly care and broader health industries, with extensive involvement in industry research, market observation, and practical operational management of elderly care services. I am currently a co-founder of Meridian (Beijing) International Elderly Care Services Co., Ltd.