China's Pharmacy Retail Chains Reach 55% Penetration, Pivoting Toward Professional Health Services

Driven by policy and capital, the pharmacy retail sector is undergoing significant transformation; seizing this trend is undoubtedly a key driver for maintaining a competitive edge amid change.

Over the past decade, the retail pharmacy sector has undergone a wave of consolidation characterized by larger players acquiring smaller ones. Recently, this trend has reached an inflection point, as independent pharmacies and small chains form alliances, acting as a pause in the rapid march toward higher retail chain penetration. Beyond changes in scale, significant shifts have also occurred at the operational level: pharmacy services are gradually transitioning from simple product sales to service-oriented and even health management-focused models. Scale is no longer the sole competitive advantage for retail pharmacies.

"Land Grabbing"

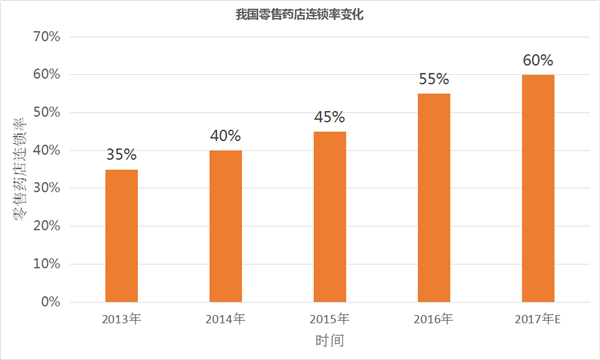

Relevant data indicate that the chain store penetration rate of retail pharmacies in China has reached approximately 55%, hitting a record high.

In fact, prior to 2013, the chain affiliation rate of retail pharmacies in China was very low, with the market dominated by local small chains and independent pharmacies, and there was no prevailing concept of industry consolidation or mergers and acquisitions. However, when some pharmacy chains listed on the securities market that year, investors recognized retail pharmacies as a “prime” investment target. In the following years, fueled by capital injection, the chain affiliation rate of retail pharmacies rose significantly, achieving an average annual growth rate of over 5%. (The overall growth rate in the total number of pharmacies was slower than the increase in the chain affiliation rate, indicating that the rise in chain affiliation was driven primarily by mergers and acquisitions within the industry.)

Taking 2015 as an example, statistical data released by the China Food and Drug Administration (CFDA) showed that at the end of the year, there were 4,981 retail pharmacy chains in China, with 204,000 chain stores. The number of independent pharmacies stood at 243,000, resulting in a chain rate of 45.5%. Meanwhile, the number of newly added pharmacies reached 13,200, representing a growth rate of 3.04%, which was lower than the growth rate of the chain rate.

We should also note that there is an upper limit to the increase in the chain affiliation rate of retail pharmacies, which observers estimate to be around 70%. The specific rationale is that raising the chain affiliation rate comes at the cost of depleting the accumulated capital reserves of acquiring enterprises; this path cannot be extended indefinitely. Moreover, a higher chain affiliation rate introduces managerial challenges, potentially leading to a situation where the organization becomes too large and unwieldy to manage effectively.

However, there is still significant room for improvement in the chain store rate of retail pharmacies in China. Taking the U.S. market as an example, the retail pharmacy chain rate is approximately 75%, nearly 20 percentage points higher than that of China. Meanwhile, the U.S. market exhibits relatively high concentration, with three major pharmacy chains—CVS, Walgreens, and Rite Aid—accounting for over 75% of the pharmaceutical retail market share and operating more than 40,000 stores combined. In contrast, the top ten retail pharmacy chains in China hold a relatively low market share, and their number of stores is insufficient to achieve nationwide coverage.

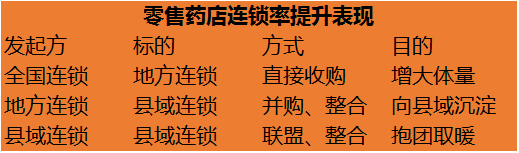

In the absence of significant new store construction, the rise in the chain rate of retail pharmacies is primarily driven by mergers and acquisitions. Several listed companies have followed this path; Yixintang, Yifeng Pharmacy, Laobaixing Pharmacy, Guoda Drugstore, and Shuyu Civilian Pharmacy have all raised funds from the secondary market to finance M&A activities (notably, Yixintang aims to accelerate its expansion, with its store count expected to surpass 4,000 in the short term).

Furthermore, the catalytic role of industry capital should not be overlooked. For instance, Tasly has invested in regional pharmacy leaders such as Gansu Zhongyou and Shandong Lijian. Direct investments by pharmaceutical companies’ big health funds into leading regional pharmacy chains indicate that pharmaceutical manufacturers are actively participating in the M&A and consolidation of retail pharmacies, aiming to achieve synergy between industrial capital and foster in-depth cooperation at the business level.

Meanwhile, independent pharmacies are also weighing the trade-offs between being acquired and forming alliances. This is particularly true for certain county-level pharmacy chains (with fewer than 100 stores and annual sales revenue not exceeding RMB 500 million). These chains cover towns and rural areas that large pharmacy retailers cannot reach, making them attractive acquisition targets for regional leaders. However, being incorporated into a large group means losing control, so many county-level leaders have chosen to form alliances by establishing joint pharmacy chain groups. This approach offers several benefits: first, it provides an indirect means of resisting takeovers; second, it grants stronger bargaining power against pharmaceutical manufacturers and drug distribution companies.

A Subtle Shift in Business Model

Amidst the race for market expansion, pharmacies are also diversifying their services, driven by pharmaceutical policies and shifting consumer demand. Large and medium-sized chain pharmacies, in particular, are prioritizing functional evolution alongside scale expansion, gradually developing models such as pharmaceutical care services, medication delivery, chronic disease management, specialty pharmacies, and health benefit management.

Taking pharmaceutical care services as an example, under the new GSP standards, retail pharmacies are basically equipped with licensed pharmacists who can provide prescription verification and medication advice, thereby enhancing the pharmacies’ capacity to deliver pharmaceutical care services.

The elimination of the “drug-revenue-subsidized healthcare” model, the separation of prescribing from dispensing, and the outflow of prescriptions have all brought significant benefits to the retail pharmacy sector. In terms of market size, the distribution ratio between hospital and retail channels in China’s previously RMB 1.4 trillion pharmaceutical market was highly imbalanced, with the total retail market amounting to less than RMB 350 billion. As the drug revenue share declines, the spillover market will exceed RMB 100 billion. How retail pharmacies can absorb this market—through what mechanisms and whether they are capable of doing so—is driving a functional transformation in their business operations.

The first to emerge were hospital-adjacent pharmacies and specialized pharmacies. Following the separation of prescribing and dispensing, some retail pharmacies shifted their focus to the hospital pharmacy market and secured priority access to prescriptions through strong collaborative relationships with hospitals, thereby becoming beneficiaries of this policy shift. It should be noted that this cooperation model exists only during the transitional phase of separating prescribing from dispensing; hospital-adjacent pharmacies often maintain dependencies or interest-based ties with hospitals, making their experience difficult to replicate on a large scale. Specialized pharmacies are similar in that they both reap the benefits of the separation of prescribing and dispensing and seek breakthroughs in functional systems.

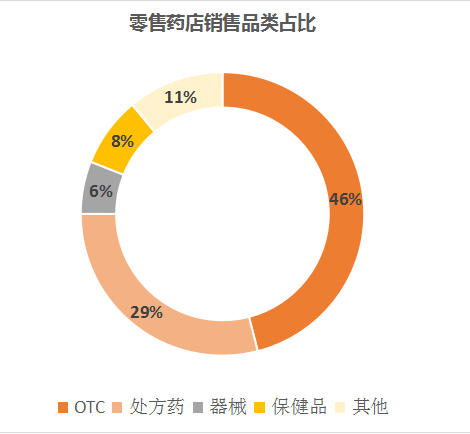

It is also important to note the shifts in consumer demand. Previously, pharmacies primarily focused on over-the-counter (OTC) drugs, complemented by sales of health supplements and medical device-related products; however, this landscape is now changing.

Adjustments in the product mix of pharmacy sales are reflected in the increasing volume of non-pharmaceutical products, including health supplements, maternal and infant products, medical devices, and herbal decoction pieces, with the most significant growth observed in medical devices and maternal and infant products. Medical devices primarily focus on chronic disease monitoring and rehabilitation, covering areas such as diabetes and blood glucose management, while maternal and infant products include prenatal care, infant formula, and baby supplies. These changes are mainly driven by shifts in demographic structure and residents’ health status, such as population aging; the latter is directly related to the expansion of pharmacy service scopes.

Overall, as pharmaceutical reforms gradually enter deeper waters, the landscape of pharmaceutical retail is undergoing gradual changes, with structural adjustments in sales categories and service models, and the industry is facing a turning point.

Speculations on Future Models

Based on the aforementioned analysis, new business models will emerge in the pharmaceutical retail sector, with the integration of medical consultations, chronic disease management, and professional services becoming central. Related health management entry points and synergies with internet healthcare may evolve as derivative business formats.

First is the consultation service. VCBeat (WeChat: vcbeat) previously reported that the Chengdu Municipal Food and Drug Administration launched a pilot program for electronic prescriptions among chain pharmacy enterprises across the city. More than 3,000 pharmacies activated consultation services, and over 1,800 participated in the electronic prescription pilot. These pilot pharmacies provide consumers with health consultations, electronic prescription issuance, and verification services. Recently, WeDoctor also announced the achievements of its “Pharmacy + Clinic” initiative. Over the past year, WeDoctor has collaborated with chain pharmacies to introduce Wuzhen Internet Hospital for patient consultations at pharmacy locations, connecting more than 10,000 pharmacies and handling an average of over 20,000 daily consultations. This demonstrates that pharmacies have adopted a proactive attitude toward integrating consultation services, with significant and evident results.

Introducing consultation services into pharmacies offers several benefits: first, it improves service quality; second, it effectively captures the incremental prescription volume generated by consultation services; third, it increases customer traffic and stickiness, while also serving as a supplement to primary healthcare. Examining these points individually, diagnostic and treatment capabilities have long been a weakness for pharmacies. Although they do not hold prescribing authority, customers still seek relatively professional medication guidance and services. Furthermore, remote consultations require relevant diagnostic equipment, and deploying such resources through retail pharmacy channels can enhance utilization and conversion rates. Finally, the incremental customer base and prescription volume that pharmacies gain in this process have become a major incentive for pharmacies to pursue consultation services.

More importantly, with the implementation of the national tiered diagnosis and treatment policy, new requirements have been raised for the utilization of primary healthcare. Similar to primary care clinics and hospitals, pharmacies can also assume part of the functions within the tiered diagnosis and treatment system. Meanwhile, the resources of their affiliated online hospitals can endorse their professionalism, enabling “initial diagnosis at the primary level and rehabilitation at the primary level,” thereby effectively alleviating the pressure on the tiered diagnosis and treatment system.

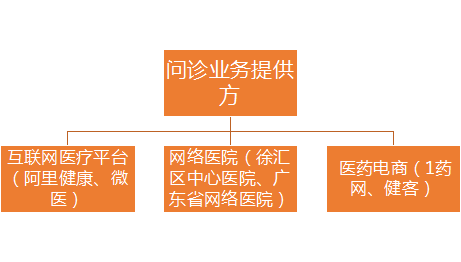

Providers of online consultation services may include internet healthcare platforms (such as AliHealth, WeDoctor, and Haodf), pharmaceutical e-commerce companies (such as 111.com and Jianke), or online hospitals affiliated with Grade-A tertiary hospitals (such as Xuhui District Central Hospital and Guangdong Provincial Online Hospital). Different healthcare resource providers can also drive distinct development trajectories. Potential service offerings—such as appointment scheduling and consultations, electronic prescriptions, follow-up visits, and medication delivery—remain areas to be explored through future collaborations.

Next, it serves as the entry point for health management services. In fact, many companies have already proposed this concept, including Dingdang Kuaiyao, a subsidiary of Renhe Pharmaceutical, with its “Smart Pharmacy” initiative, and Haoyaoshi Pharmacy with its “Health Service Store” model. Both approaches position physical pharmacies as the entry point and carrier for future business operations. From the perspective of pharmaceutical care services provided by pharmacies, serving as an entry point for health management is a natural progression. By establishing user health records and subsequently engaging in full-cycle health management services, pharmacies can not only enhance user stickiness but also achieve a functional closed loop.

What services can health management include? It encompasses a range of offerings such as basic medication services, chronic disease monitoring, personal health records, and personalized medical care. These services can be further expanded into several key segments—“healthcare, pharmaceuticals, and insurance”—to effectively manage residents’ health. Moreover, under the trend of “proactive health,” there will be substantial demand for daily health management. By integrating pharmaceutical care services, retail pharmacies can identify strategic areas for growth.

From a broader perspective, driven by favorable policies, upgrades in the medical and healthcare industry, shifting consumer demands, and the rising trend of proactive health management, retail pharmacies are extending their business models toward service-oriented and medical-focused offerings. While aggressively expanding their market share, pharmacies are also actively seeking new growth drivers, with emerging business models gradually gaining favor from both capital markets and the industry.