Yijietong: The 'Second Medical Insurance Card' – Unlocking the Vast Potential Behind RMB 80 Million in Health Insurance Assets

80 millionHealth Insurance Funds,30,000Employee.

It took the Chongqing-based startup Yijietong more than a year to achieve this scale of management, which represents only a tiny fraction of the vast health insurance industry.

In the view of Jian Guangping, General Manager of Yijietong, managing this RMB 80 million health insurance fund merely opens a window. In the future, this window will evolve into a door, beyond which lies a vast realm of possibilities connecting insurance companies, enterprises, and medical institutions.

Creating Value by Addressing Industry Pain Points

Jian Guangping has served at China Life for many years, and few know the Chongqing health insurance market better than he does.

“Policyholders and insured individuals seek timely and rapid claims settlement, along with greater choice and convenient payment processing, while insurance companies aim to strictly monitor the flow of funds,” said Jian Guangping. For large-scale insurers, meeting these demands is technically feasible but cost-prohibitive, which creates an ideal opportunity for third-party service providers.

“Our team has a combined 90 years of experience in the insurance industry, giving us firsthand insight into its pain points.” As a result, Jian Guangping and his colleagues founded Yijietong, a third-party service platform for health insurance. The platform’s core business model is to provide one-stop solutions for health insurance, ensuring the rational use of funds while improving both capital efficiency and benefit payout levels.

Through Yijietong, insured employees no longer need to make out-of-pocket payments when incurring expenses at contracted medical institutions, pharmacies, online pharmacies, health examination centers, and rehabilitation centers; instead, transactions are settled directly, significantly enhancing convenience. Additionally, Yijietong allows affiliated individuals, such as family members of the insured, to utilize their benefits for health-related expenditures, thereby further improving the utilization efficiency of health insurance funds.

“Previously, there was significant idle capital in the supplementary medical insurance accounts (a policy-supported category within health insurance) provided by enterprises to their employees. Now, insured individuals are willing to use this system, ensuring that health funds are truly directed toward meeting healthcare needs,” said Jian Guangping. By connecting this critical node, Yijietong has not only enhanced the user experience and utilization efficiency of health insurance products but also improved customer satisfaction for insurance companies, thereby creating value for policyholders, insured individuals, and insurers alike.

Currently, Yijietong has partnered with China Life Insurance Company in Chongqing and multiple other companies that provide supplemental medical insurance to their employees, focusing on the utilization and management of insurance funds. The scale of managed individuals is approximately 30,000, with annual managed funds reaching RMB 80 million.

Second Medical Insurance Card

“Yijietong currently offers a card, and its model essentially provides insured individuals with a second ‘medical insurance card,’” said Jian Guangping. He noted that the Yijietong Card holds advantages over the standard medical insurance card in terms of claims calculation, applicable scenarios, and target consumer segments.

Yijietong Insurance Service Card Sample

He calculated that supplementary medical insurance could account for approximately 2% of employees’ wages. Based on this estimate, the comprehensive rollout of such insurance would create a substantial market opportunity. Against the backdrop of a funding gap in basic medical insurance and escalating employee health needs, supplementary insurance is experiencing rapid growth.

Jian Guangping stated that similar businesses in China are actually just in their nascent stages, with substantial room for development. On a positive note, health needs are gaining increasing attention from enterprises, and the government is providing incentives, such as tax benefits, to companies that purchase supplementary medical insurance.

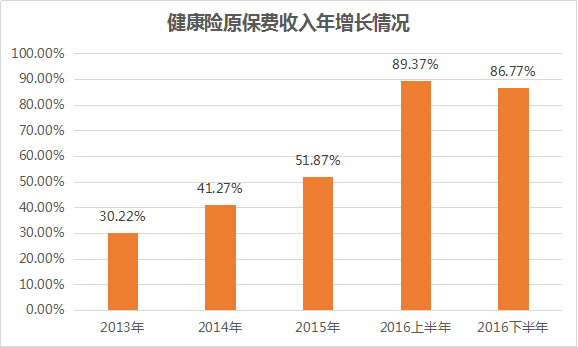

Statistical data also corroborates this point. According to statistics from the China Insurance Regulatory Commission (CIRC), from January to November 2016, the original insurance premium income of national health insurance business reached RMB 384.18 billion, a year-on-year increase of 73.08%.

Source: Caixin Health Point

The “13th Five-Year Plan for Deepening the Reform of the Medical and Healthcare System,” recently issued by the State Council, also proposes to diversify health insurance products, vigorously develop consumer-oriented health insurance, promote the development of various types of health insurance, formulate and improve relevant preferential policies such as fiscal and tax incentives, and support the accelerated development of commercial health insurance.

Unlimited Space Behind the 80 Million

Managing RMB 80 million in health insurance funds is merely the beginning—indeed, a very modest one.

In Jian Guangping’s view, health insurance, as a supplement to medical insurance, is not an end in itself. The third-party services provided by Yijietong can attract policyholders to utilize such services; driven by incentives such as enhanced employee benefits and tax subsidy policies, enterprises will also accelerate their adoption of this business model. Meanwhile, through calculations performed via the Yijietong system, insurance companies can reduce their underwriting costs and save time.

“In fact, the market we are currently targeting is still dominated by existing funds. Supplementary medical insurance actually exists within insurance companies in the form of fund management. After expanding service providers and accounting methods, insurance companies are also happy to cooperate with us.” In Jian Guangping’s view, after being revitalized by the Yijietong third-party service platform, a win-win situation for all participants in the chain has been formed.

Within a framework of win-win cooperation, Yijietong is increasingly focused on leveraging health insurance as a gateway to connect with a broader future. Jian Guangping plans to gradually integrate more insurance companies, insured enterprises, and health services into the Yijietong ecosystem, while simultaneously deepening its existing business model and enhancing brand influence. In particular, by onboarding more product and service providers from the broader health sector, Yijietong aims to become the preferred partner for platform-based enterprises seeking to enter the big health industry. In this process, insurance companies will be more willing to provide customized group insurance products for Yijietong. Yijietong itself will also participate in insurance product design, claims settlement, and the customization of health services, thereby establishing its own market influence and voice.

Yang Yang, Operations Director at Yijietong, revealed that 2015 was a year for laying the foundation for the company. In 2016, it established systematic frameworks and accumulated experience in products and services. The year 2017 marked a critical phase in its development, during which the company would engage in an in-depth exploration of service models to establish standards for third-party health insurance service platforms.

“Only with a solid foundation can there be opportunities for strategic expansion,” said General Manager Jian Guangping, adding that Yijietong will expand beyond Chongqing to other regions this year.