Pharmaceutical Sector Leads the Way as 66 Funds Achieve Record-High Exits in 2016

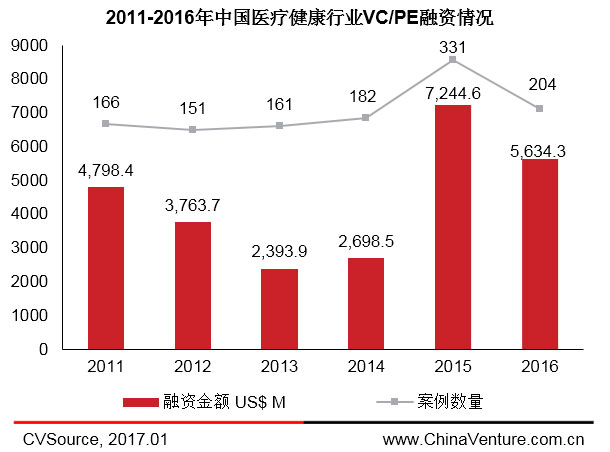

According to statistics from CVSource, a financial data product under China Venture Information (CVInfo), the number of venture capital (VC) and private equity (PE) financing deals in the healthcare sector totaled 204 in 2016, representing a 38.37% decrease from the 331 deals recorded in the previous year. The total financing amount reached USD 5.634 billion, a 22.23% decline compared to USD 7.245 billion in the prior year. However, the average deal size rose to USD 27.62 million, marking a 26.19% increase from USD 21.89 million in the previous year. Overall, both the number of financing deals and the total financing volume experienced a significant decline compared to the previous year, while the average deal size increased. Compared with earlier years, the healthcare financing market in 2016 maintained a relatively stable level of activity; although there was a slight downturn in market conditions, it remained within the range of normal fluctuations. (See Figure 1)

Figure 1 VC/PE Financing in China’s Healthcare Industry, 2011–2016

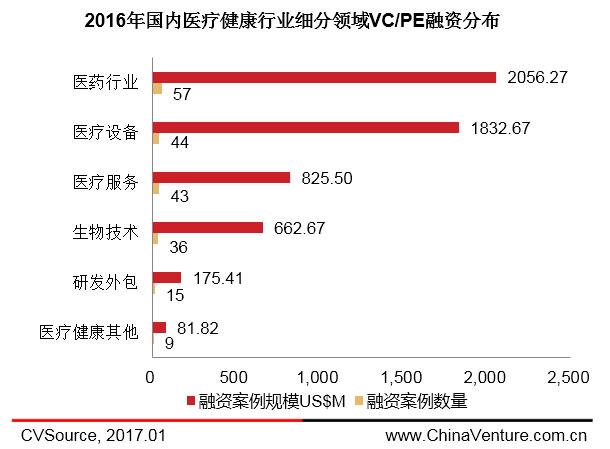

In terms of distribution across sub-sectors, the pharmaceutical industry and the medical device industry ranked first and second in the healthcare sector in 2016, with financing volumes of $2.056 billion and $1.833 billion, respectively. Meanwhile, the number of financing deals in these two sub-sectors also led other areas. In particular, the pharmaceutical industry demonstrated strong and positive growth momentum. In light of the Chinese government’s 2016 initiatives to “vigorously promote the revitalization and development of Traditional Chinese Medicine (TCM), adhere to equal emphasis on both TCM and Western medicine, foster complementary and coordinated development between TCM and Western medicine, and strive to achieve creative transformation and innovative development of TCM health and wellness culture,” as well as to “implement projects for the inheritance and innovation of TCM, advance the modernization of TCM production, and establish Chinese standards and brands,” it is evident that multiple policies continue to safeguard and support the development of the healthcare industry. Although the TCM segment has not yet manifested its prominence at the forefront of the market, these policies have injected new vitality and direction into market development. (See Figure 2)

Figure 2. Distribution of VC/PE Financing by Sub-sector in China’s Healthcare Industry, 2016

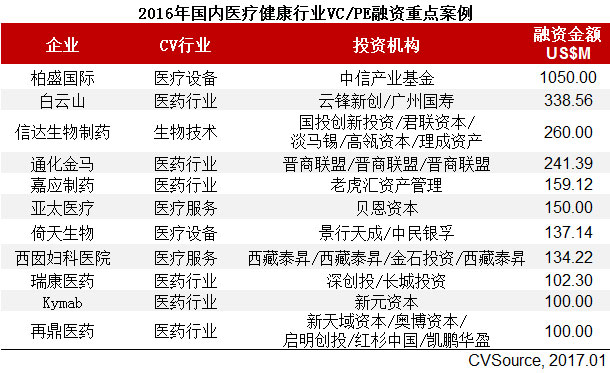

In terms of specific financing cases in China’s healthcare industry in 2016, Biosensors International Group led by a wide margin with a total financing amount of $1.05 billion. On April 19, 2016, CITIC Private Equity Funds Management Co., Ltd. successfully completed the privatization acquisition of Biosensors International Group Ltd. (SGX-ST: B20), a Singapore-listed company and the world’s fourth-largest manufacturer of coronary stents, through funds under its management. The total transaction consideration amounted to $1.05 billion. CITIC Private Equity is a specialized investment subsidiary of CITIC Group Corporation and CITIC Securities Co., Ltd., established in June 2008 with the approval of the National Development and Reform Commission. It benefits from comprehensive support from CITIC’s integrated financial services platform and industrial network. This substantial investment by CITIC Private Equity in Biosensors International reflects the confidence of mature and rational investors in the medical device sector, which is rapidly evolving alongside technological advancements, thereby injecting new vitality into the entire healthcare market.

Meanwhile, among companies that raised over $100 million, the pharmaceutical industry continues to hold a significant position, with six financing cases recorded. The largest fundraising was by Guangzhou Baiyunshan Pharmaceutical Holdings Co., Ltd. (600332.SH), which raised a total of RMB 7,885,807,628.44 (approximately $339 million). After deducting issuance expenses of RMB 22,361,100.11, the net proceeds amounted to RMB 7,863,446,528.33. Specifically, Guangzhou China Life Urban Development Industrial Investment Enterprise (Limited Partnership), a fund under Guangzhou China Life Urban Development Industrial Investment Consulting Enterprise (Limited Partnership), subscribed for 73,313,783 shares at RMB 1,727,272,727.48; Shanghai Yunfeng Xinchuang Equity Investment Center (Limited Partnership), a fund under Shanghai Yunfeng Xinchuang Investment Management Co., Ltd., subscribed for 21,222,410 shares at RMB 499,999,979.60. In the VC/PE financing market, the pharmaceutical sector is indeed experiencing robust growth, driven by the overall virtuous cycle and development of the market, as well as favorable policy support.

Furthermore, among the VC/PE financing cases this year, there has been a phenomenon where four or more relatively mature venture capital or private equity firms compete for investment in the same company. In the case of Innovent Biologics in the biotechnology sector, investors included SDIC Innovation Investment, Legend Capital, Temasek, Hillhouse Capital, and Licheng Asset Management. A similar pattern was observed in the case of Xi’nan Gynecological Hospital, with investors including Tibet Taisheng, Jinshi Investment, and others. Zai Lab also attracted investment from multiple institutions. This phenomenon highlights the rational competitive stance of investors in the market. The fact that these investee companies have garnered favor and recognition from multiple institutions is precisely due to their stable and balanced growth momentum, which overall indicates that the market is becoming increasingly mature and stable. (See Table 1)

Table 1 Key VC/PE Financing Cases in China’s Healthcare Industry in 2016

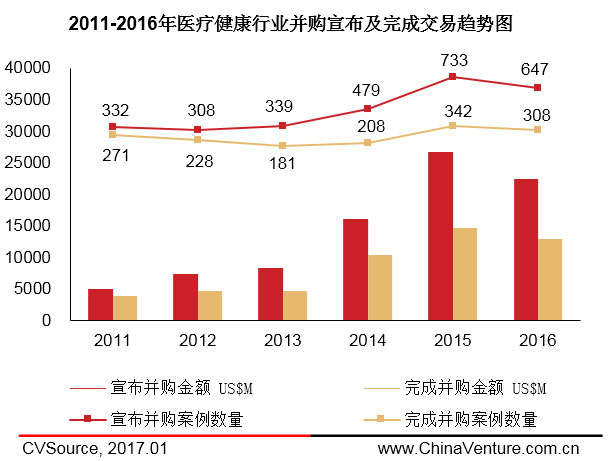

According to statistics from CVSource, a financial data product under Zero2IPO Research, the number of announced mergers and acquisitions (M&A) deals in the healthcare sector reached 647 in 2016, with a disclosed transaction value of $22.399 billion. Compared with the same industry in 2015, the number of announced M&A deals decreased by 11.73%, and the disclosed transaction amount dropped by 15.99%. In 2016, the number of completed M&A transactions in the same industry totaled 308, with a disclosed transaction value of $12.961 billion. Year-on-year, the number of completed cases declined by 9.94%, and the total transaction value decreased by 11.62%. Overall, although the healthcare M&A market experienced a slight slowdown in 2016 compared to the previous year, it generally surpassed earlier years across various indicators, indicating that the M&A market is in a process of steady and balanced development. (See Figure 3)

Figure 3: Trends in Announced and Completed M&A Transactions in the Healthcare Industry, 2011–2016

From specific cases, the most notable is Beijing Jialin Pharmaceutical Co., Ltd., which ranked first with a transaction amount of $1.272 billion. On December 12, 2015, Beijing Jialin Pharmaceutical Co., Ltd. proposed an asset swap with Xinjiang Tianshan Wool Textile Co., Ltd. (000813.SZ). On August 18, 2016, all assets of Jialin Pharmaceutical were injected into Tianshan Textile, completing the back-door listing transaction. Next, Tongjitang Medicine, ranking third with a transaction amount of $931 million, also successfully completed a back-door listing. On February 12, 2015, Xinjiang Hops Co., Ltd. (600090.SH) proposed to acquire 100% equity of Tongjitang Medicine Co., Ltd. held by Hubei Tongjitang Investment Holding Co., Ltd., Shenzhen Shengshi Jianjin Equity Investment Partnership (Limited Partnership), and others through share issuance and cash payment. On May 17, 2016, the back-door listing transaction was completed. After this change, Hops held 100% equity in Tongjitang Medicine. Back-door listings in the M&A market are on par with traditional acquisitions, highlighting the broad prospects and immense potential of the healthcare industry.

Meanwhile, the two companies that went public via reverse mergers are also part of the pharmaceutical industry. The transaction volume and number in this subsector accounted for a significant share of the entire healthcare industry in 2016, driving the development of the industry as a whole.

Also noteworthy is the segment on cross-border M&A transactions. For instance, BPL, which ranked second in transaction value, is a global blood products company with a comprehensive industry chain and is among the top ten blood products manufacturers worldwide. Originally a national blood products research institution under the UK Department of Health, BPL boasts substantial R&D expertise and a complete product portfolio. In May 2016, BPL was fully acquired by Tiancheng International, a joint venture established by the controlling shareholders of Shanghai RAAS Blood Products Co., Ltd. (002252.SZ), among others. This transaction reflects the market’s emphasis on biotechnology R&D and its optimistic outlook for future growth. Cross-border transactions were also highlighted in relevant government initiatives and policies in 2016. The government continued to encourage private investment in healthcare facilities to alleviate the burden on public hospitals and relaxed restrictions on foreign investment. Meanwhile, to meet growing domestic demand, the government encouraged Chinese enterprises to strengthen overseas investments in the healthcare sectors of countries such as Israel, the United States, and Australia, thereby acquiring advanced technologies, specialized expertise, and premium brand value from foreign companies to better cater to the needs of the domestic market. (See Table 2)

Table 2 Major M&A Cases in the Healthcare Industry in 2016

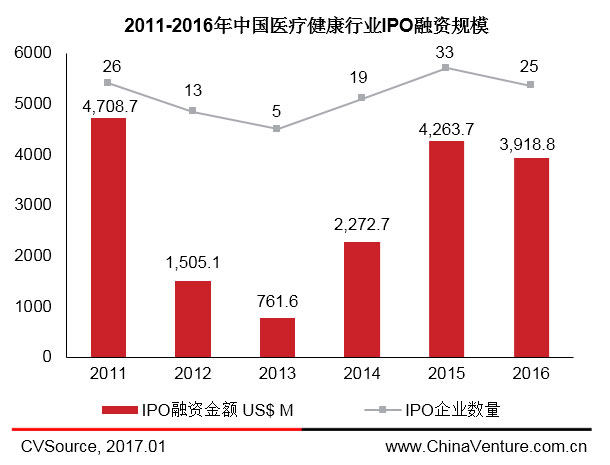

In 2016, there were 25 initial public offerings (IPOs) in the healthcare sector, with total fundraising amounting to USD 3.919 billion. The number of financing cases decreased by 24.24% compared to 33 cases in 2015, while the total fundraising volume declined by 8% from USD 4.264 billion in 2015. (See Figure 4)

Figure 4 IPO Financing Scale of China's Healthcare Industry, 2011–2016

As shown in the table below, there were seven companies in the healthcare industry that raised over USD 100 million through initial public offerings (IPOs) in 2016. Among them, three were listed on the Hong Kong Stock Exchange: China Resources Pharmaceutical (03320.HK), Ruici Healthcare (01526.HK), and Kanghua Medical (03689.HK). One company was listed on the Shanghai Stock Exchange: Buchang Pharmaceuticals (603858.SH). Two companies were listed on the Shenzhen Stock Exchange: Asymchem Laboratories (002821.SZ) and Betta Pharmaceuticals (300558.SZ), with the latter listed on the ChiNext board. The remaining company was BeiGene (BGNE.NASDAQ), listed on the NASDAQ stock exchange in the United States. From a subsector perspective, among these seven key IPO cases, one belonged to biotechnology, two to healthcare services, and four to the pharmaceutical industry. Within the pharmaceutical sector, China Resources Pharmaceutical’s (03320.HK) IPO raised USD 1.803 billion, a figure significantly higher than those of the other IPOs. (See Table 3)

Table 3 IPO Financing Cases in the Healthcare Industry in 2016

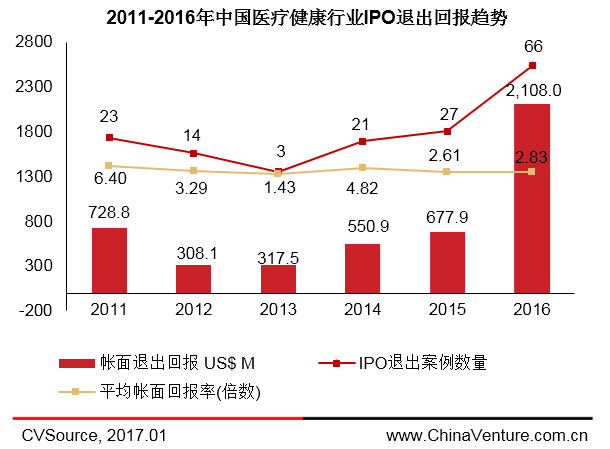

According to CVSource, in 2016, a total of 66 institutional funds achieved exits in the healthcare sector, with an average book return multiple of 2.83x. Compared with 2015, both the number of institutional funds involved and the book exit returns saw significant increases, reaching a six-year high. Although the average book return multiple increased slightly, the change was marginal. (See Figure 5)

Figure 5. Trends in IPO Exit Returns in the Healthcare Industry, 2011–2016

Source: CVSource Research Institute,Author: He Liu