Fitbit: Pioneering the Wearables Market with Health Data at Its Core – A Strategic Review and Outlook Amid Market Volatility

As the new year begins, everything takes on a fresh look. The end of the Spring Festival holiday marks our official entry into the busy schedule of 2017. Looking back on 2016, we witnessed frequent turbulence in the internet healthcare industry, the continuous surge of artificial intelligence, a rush of capital into the genomics sector, and tightening policies for pharmaceutical e-commerce...

Although the market we can observe is merely the tip of the iceberg of the entire healthcare and wellness industry, these small signs reveal broader trends. VCBeat will identify benchmarks and leaders from these dynamic sectors, review their development over the past year, and analyze and forecast their strategies for 2017, hoping to provide valuable insights for investors, observers, thinkers, and practitioners in the industry.

A few years ago, analysts were predicting that wearables would become a major market sweeping through the tech industry, with rapid growth across the entire sector and individual companies. However, recent data show that the performance of the wearable market has fallen far short of earlier expectations. In December 2016, IDC, a renowned global market research and consulting firm, released survey results indicating that the wearable market’s growth rate was only 3.3% in the third quarter of 2016 compared with the same period in 2015, disappointing many who had been bullish on the market. Even Jawbone, the pioneer brand in wearables, is struggling to survive, grappling with financial problems and worldwide layoffs, and is now seeking acquisition.

Fitbit also finds itself in a rather awkward position. According to data from S&P, Fitbit’s stock price plummeted by 75% in 2016. When announcing its third-quarter results for 2016, Fitbit even projected that its year-over-year growth rate for the fourth quarter would be merely 2%–5%. The company was compelled to publicly acknowledge: “We are indeed growing and profitable, but our growth pace is significantly slower than anticipated.” Meanwhile, it stated that it is enhancing product quality and deepening its integration into the healthcare ecosystem, aiming to leverage its brand equity to unlock additional revenue streams. Here, VCBeat (WeChat ID: vcbeat) takes stock of Fitbit’s actions over the past year or so, clarifies the logic behind its sequential moves, and offers brief predictions on its potential new initiatives.

Four New Products: Enhanced Features and Fashion-Forward Design

Fitbit released four fitness tracker models in 2016: the Blaze, Alta, Charge 2, and Fitbit Flex 2. Among these new products, the Blaze marked Fitbit’s first foray into everyday smartwatches, while the Flex 2 was its first waterproof wearable device capable of tracking swimming activities. One of Fitbit’s most competitive features is undoubtedly continuous heart rate monitoring, which it implements more elegantly than even its biggest competitor, the Apple Watch. In the 2016 lineup, this feature is available on both the Blaze and the Charge 2.

Some analysts argue that Fitbit has long held a leading position in the wearable device market. To maintain its industry forefront, the company has continuously invested in product research and development. However, sales have clearly not been strong enough to offset these R&D investments, leading to an inevitable decline in profits, which is also a significant factor behind the drop in its stock price.

From left to right: Flex 2, Charge 2, Alta, Blaze

From a product design perspective, Fitbit has moved closer to fashion accessories. For instance, the Blaze, launched at CES in early 2016, was positioned as a stylish fitness watch. Its Apple-inspired aesthetic conveyed this message to the general public, seemingly demonstrating that “we can achieve strong design appeal even without collaborating with fashion brands like Tory Burch” (the two companies had previously partnered in 2014 to release wearable accessories). The Alta, another model marketed for its fashionable style, has been described by some reviewers as Fitbit’s most visually appealing product to date, further underscoring its fashion-oriented strategy. All four wearable devices released that year featured interchangeable bands, allowing users to switch up their look depending on the occasion—a clear reflection of Fitbit’s effort to enhance the fashion appeal of its products.

Expanding into Two Major Markets Outside the United States

In the Chinese market, healthy lifestyles and fitness trends are on the rise, and fitness trackers are becoming increasingly familiar to Chinese consumers, although they have not yet entered the mainstream market. In 2016, Fitbit’s sales in the Asia-Pacific region were sluggish, and it faced competition from other affordable wearable fitness products. Apart from the Flex 2, a relatively affordable device priced at $99, Fitbit lacked overall price competitiveness that year. In April 2016, Fitbit announced a strategic online retail partnership with Tmall, signaling its intent to further penetrate the Chinese market, which boasts hundreds of millions of consumers. Tmall also stated its goal to help Fitbit attract 10 million fans in Asia. In May, Tmall hosted a Fitbit Super Brand Day to launch the collaboration, with Founder and CEO James Park making a personal appearance in Hangzhou. Both parties jointly announced their commitment to promoting national fitness and helping Chinese consumers achieve their health and fitness goals.

In China, in addition to Tmall, the domestic health management company Miao Health and its parent company, Sanpower Group”Its retail stores (including Leye Communications and Hongtu Brookstone, among others) also sell Fitbit products.

Fitbit Is Actively Expanding Its Presence in the Chinese Market

In August last year, Fitbit opened a new office in Dublin, Ireland, creating 100 new jobs. This new office now serves as the headquarters for the Europe, Middle East, and Africa (EMEA) markets, aiming to expand its presence in these regions. The platform currently supports five European languages, and Fitbit’s market share in Europe has been rapidly growing. For instance, during the second quarters of 2015 and 2016, Fitbit’s year-over-year revenue growth rate in the European market reached 150%. Fitbit seized the right moment and leveraged Dublin’s highly skilled workforce to establish its new headquarters, using international market expansion as a strategy to boost sales.

3 Acquisitions, with a Focus on Wearable Software

In the face of a sluggish market for sports wearables, Fitbit’s most typical response has been to acquire other smart hardware companies in an effort to strengthen its position through consolidation. Although the effectiveness of this strategy remains to be seen, Fitbit embarked on an aggressive acquisition spree in 2016: in May, it acquired the mobile payment company Coin; by year-end, it purchased Pebble, the pioneer of smartwatches that had fallen on hard times, for $40 million, acquiring only its software division and intellectual property rights; and early this year, it announced the acquisition of the software division of Vector Watch, a European fashionable smartwatch brand. Late last year, Fitbit nearly acquired Jawbone, which was struggling to survive amid the bleak wearable market conditions. Fitbit had been anticipating Jawbone’s bankruptcy and even proactively offered to waive previous infringement compensation claims against Jawbone to initiate acquisition negotiations. However, the deal ultimately fell through due to a failure to agree on the purchase price. Even Fitbit CEO James Park stated in an interview that acquisitions and technological integration are a key priority for Fitbit at this stage.

A closer look at Fitbit’s acquisitions reveals that smart wearable software is a key component. Last March, market research firm Argus Insights released a survey on user satisfaction with activity-tracking wearables and their companion apps. The results showed that Fitbit users were pleased with the hardware but less satisfied with the app (whereas Jawbone saw the opposite trend). This indirectly reflects that, as Fitbit continuously upgraded its product generations, its companion app failed to keep pace. It now appears that the company is seeking to enhance its software capabilities by acquiring software technologies from other firms.

Imagine if Fitbit integrated Coin’s standalone e-card mobile payment technology, allowing users to make purchases simply by wearing a Fitbit tracker. With the acquisitions of Pebble and Vector, Fitbit is further enhancing its software capabilities. These moves suggest that Fitbit aims to add more features, seemingly positioning itself to compete with Apple. However, its CEO has stated that feature enhancements will be implemented gradually, criticizing Apple for offering “too many features, leaving users overwhelmed.”

Extensive Business Collaboration

Fitbit has completed a substantial number of research and commercial projects over the past year or so. From these business collaborations, several key needs of Fitbit can be summarized: first, to enhance product functionality; second, to increase data accumulation; and third, to conduct brand marketing through diverse channels and expand market influence.

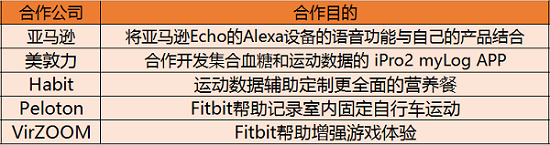

To enhance product functionality, Fitbit partnered with Amazon to deepen its voice capabilities by integrating Amazon Echo’s voice assistance features into all of Fitbit’s fitness tracking devices. This integration enables users to interact with their Fitbit devices through Alexa-enabled Amazon Echo devices, where Alexa translates user intents into machine language and commands understandable by Fitbit devices. Additionally, users can enjoy a hands-free experience by directly accessing their fitness data via voice commands.

To meet the growing need for data accumulation, Fitbit partnered with Medtronic to develop the iPro2 myLog app, which integrates data from blood glucose monitoring devices and activity trackers. The aim is to allow patients with diabetes to intuitively visualize the correlation between their physical activity levels and their condition, while also enabling the collection of more comprehensive user data.

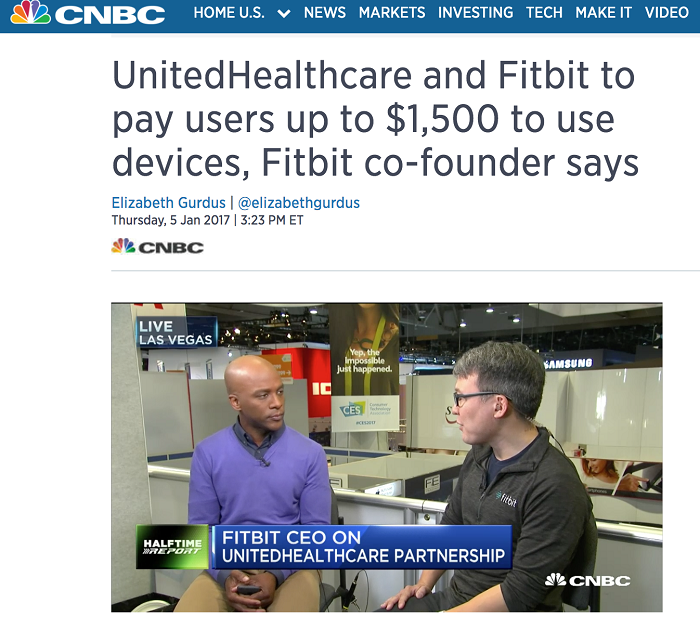

To strengthen its brand marketing efforts, Fitbit has partnered with Habit (a personalized nutrition company based on genetic data), Peloton (an indoor stationary bike manufacturer), and VirZOOM (a VR fitness gaming company) to launch a project called “New Works with Fitbit.” This initiative employs various innovative formats to engage consumers and allow them to experience the health-oriented brand culture advocated by Fitbit. Specifically, Habit leverages Fitbit’s data to help users create more comprehensive personalized meal plans; Fitbit enables users to monitor their workout metrics while cycling on Peloton equipment; and integrating Fitbit enhances the gaming experience when playing VirZOOM titles. Additionally, the company is collaborating with UnitedHealthcare on a wellness program called “Motion,” which rewards participants with bonuses for achieving their health goals—an innovative measure designed to incentivize physical activity.

Partnering with UnitedHealthcare on a Fitness Incentive Program, Users Can Earn Up to $1,500

Combining the aforementioned three demands with Fitbit’s recent lackluster sales performance, one conclusion can be drawn: Fitbit is striving to find a breakthrough in profitability. On one hand, it aims to win over users by upgrading product experience; on the other, it continues to intensify data accumulation to identify potential revenue models; meanwhile, it is launching initiatives to attract consumers and boost sales.

New Direction: Professional Medical Devices

In numerous interview statements, Fitbit has expressed strong interest in the specialized medical device sector. The CEO himself once stated that regulating medical devices represents “a huge opportunity,” and advocated against drawing an overly rigid distinction between healthcare and fitness, urging instead that the two be integrated to spark greater innovation and unlock new opportunities. Fitbit is not merely paying lip service to this vision; it is actively pursuing exploratory initiatives in professionalization.

First, it engaged in professional medical scientific research to accumulate research-grade data. In 2016, it participated in two significant studies: one was a collaboration with Cedars-Sinai Medical Center in Los Angeles to observe activity levels among cancer patients, and the other was a partnership with the Dana-Farber/Brigham and Women’s Cancer Center to investigate the correlation between weight loss and reduced breast cancer recurrence rates. Fitbit even established a research repository; last October, it collaborated with Fitabase to create the Fitbit Research Library, which enables users to search for all health studies that have utilized Fitbit products.

Next, we must continue to strengthen sensor manufacturing, further enhancing capabilities for continuous data collection, data accuracy, and data analysis, so that healthcare providers, pharmaceutical companies, insurers, and others can all benefit from Fitbit’s wearable data.

"The Battle of Lin Yuan Has Begun"

On January 30 local time, Fitbit issued a performance warning, stating that the company’s revenue for the fourth quarter of last year missed expectations and unexpectedly posted a loss, andwill lay off 110 employees (6% of the company’s global workforce) toCutting Costs. Following the announcement, the stock price plummeted by nearly 20% intraday, hitting a record low since its IPO. The decline in performance was perhaps anticipated. As the hype around fitness wearables and sensors fades, even wearable pioneers like Fitbit will plunge into crisis unless they identify new profit models and develop effective strategies to continuously attract and retain users.

In addition to the aforementioned extensive collaborative initiatives designed to attract diverse user segments, the company has recognized another imperative strategy for user acquisition and retention. In recent years, Fitbit’s user ecosystem has arguably failed to take shape, relying merely on a model of wearable devices paired with apps offering limited functionality. For instance, long-term users of either iOS or Android find it difficult to transition to a new platform. As application data accumulates within a given ecosystem, switching to a different system entails forfeiting all historical records. This dynamic effectively “locks” users into a single ecosystem.

CEO James Park revealed in an interview from early 2017 that the company wouldLaunch of Fitbit’s Own App Store, with its technological foundation built upon the recently acquired Pebble software. This is almost a definitive signal that Fitbit intends to introduce an “app store model,” directly challenging Apple. The next step is likely the launch of a product capable of rivaling the Apple Watch.Advanced Smartwatch, and gradually incorporate more features into the product.

Park cited two categories of apps that would be integrated into the Fitbit App Store: one comprising various fitness-related applications, and the other consisting of medication reminder apps. What is certain is that Fitbit will implement payment functionality following its acquisition of Coin’s mobile payment technology. Although the company stated at the time that it would not launch payment services within 2016, whether it will introduce them in 2017 remains to be seen.

In addition, Fitbit will continue to considerMergers and Acquisitions,Strengthening Research on Equipment Technologyetc.

Key Events Review

January 2016:

Launched the Blaze product, achieving sales of 1 million units within one month of listing;

Received a class-action lawsuit from consumers regarding inaccurate heart rate monitoring in the Charge HR and Surge products;

Collaborate with Cedars-Sinai Medical Center in Los Angeles to observe the activity levels of cancer patients.

February:

Launched the Alta band, selling 1 million units within one month of its market debut.

March:

Integrate Amazon Echo's voice assistance feature into the product.

April:

Enter into an online retail agreement with Tmall;

Collaborating with the Dana-Farber/Brigham and Women’s Cancer Center to investigate the correlation between weight loss and reduced breast cancer recurrence rates.

May:

Acquired the mobile payment company Coin.

August:

Launch of the Charge 2 and Fitbit Flex 2 products;

Announced the opening of its headquarters for the Europe, Middle East, and Africa (EMEA) markets in Dublin, Ireland.

October:

Co-established the Fitbit Research Library with Fitabase.

December:

Acquired the software division of smartwatch manufacturer Pebble;

Collaborated with Medtronic to develop the iPro2 myLog APP, which integrates blood glucose monitoring data with exercise data.

January 2017:

Acquired the software division of Vector Watch, a smartwatch manufacturing company;

Collaborated with gene-based personalized nutrition company Habit, indoor stationary bike company Peloton, and VR fitness gaming company VirZOOM on the “New Works with Fitbit” project;

Collaborate with UnitedHealthcare on the “Motion” health program.