$25 Billion Basic Pension Fund Set to Enter Market Post-Chinese New Year: Prospectus Filed

I. What is Basic Old-Age Insurance?

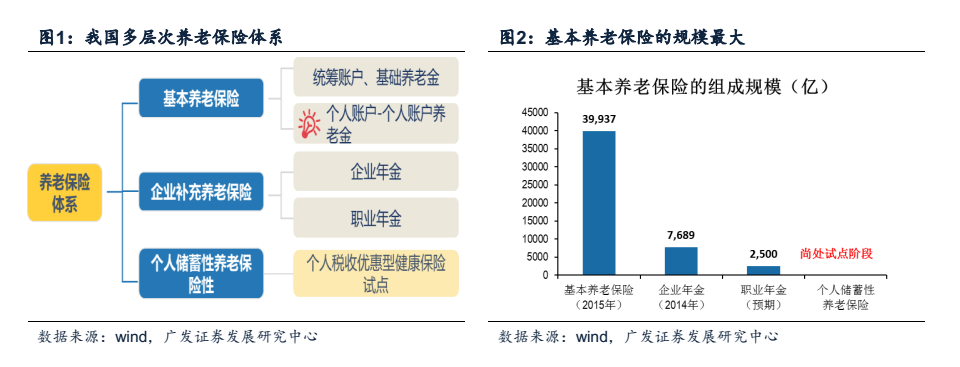

1.1 Basic Old-Age Insurance is the most important component of China's old-age insurance system

Basic old-age insurance is the most important component of China's multi-tiered old-age insurance system. China's multi-tiered old-ageThe insurance system comprises three pillars: basic old-age insurance, enterprise supplementary old-age insurance (enterprise annuities and occupational annuities), and individual savings-based old-age insurance.

Among these, the basic old-age insurance has been progressively refined and constitutes the most critical component of China’s three-pillar pension system. By 2015, the cumulative surplus of China’s basic old-age insurance fund approached RMB 4 trillion. Enterprise-supplementary old-age insurance started relatively late and remains modest in scale, primarily comprising enterprise annuities and occupational annuities. Specifically, enterprise annuities reached RMB 768.9 billion in 2014, while occupational annuities were established starting in 2014 and require an additional two to three years to achieve full funding, with a projected capital size of RMB 250 billion. Combined, enterprise and occupational annuities total approximately RMB 1 trillion, merely one-quarter the scale of basic old-age insurance. Personal savings-based old-age insurance is currently still in the pilot phase.

1.2 Basic Pension Insurance Is Distinct from the Social Security Fund

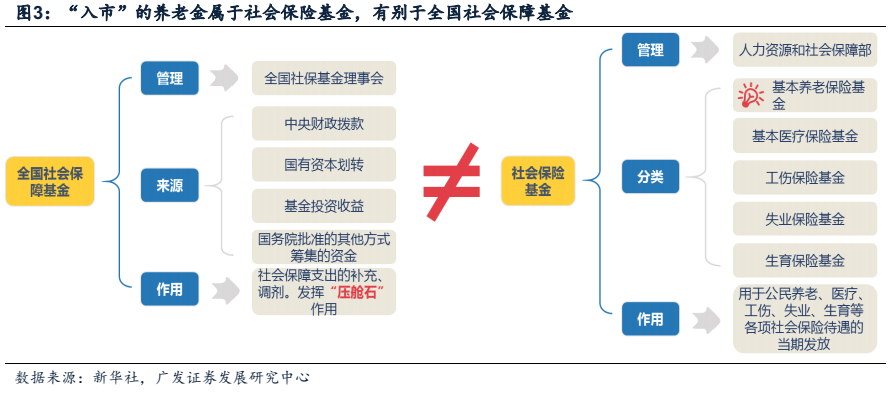

Basic old-age insurance is one of the five social insurance funds in China. China's social insurance funds are administered by human resourcesManaged uniformly by the Ministry of Human Resources and Social Security, it primarily comprises five funds: pension, medical, work-related injury, unemployment, and maternity. Its main purpose is to ensure that citizens receive material assistance in circumstances such as old age, illness, work-related injuries, unemployment, and childbirth.

The National Social Security Fund is China's national social security reserve fund. China's social security fund is managed by the NationalManaged centrally by the National Council for Social Security Fund, its sources include: central fiscal budget appropriations, transfers of state-owned capital, investment returns from the fund, and funds raised through other methods approved by the State Council. Its primary role is to supplement and adjust social security expenditures, such as pension insurance, during the peak period of population aging, thereby serving as the “ballast stone” of the social insurance system.

II. Motivations for Investing Basic Pension Insurance in the Capital Market: Enhancing Return Levels & Alleviating the “Empty Account” Gap

2.1 Enhancing the Return on Investment of Pension Insurance Funds

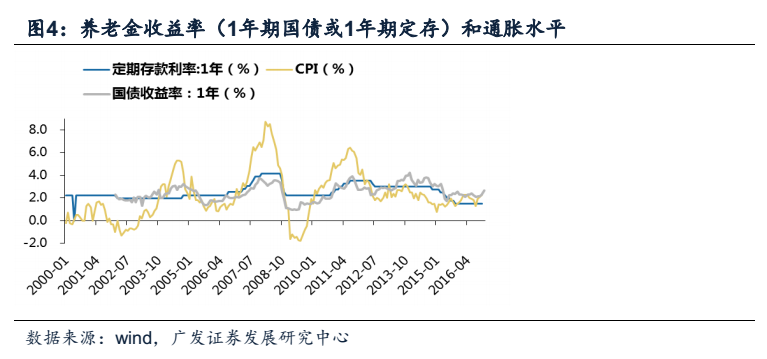

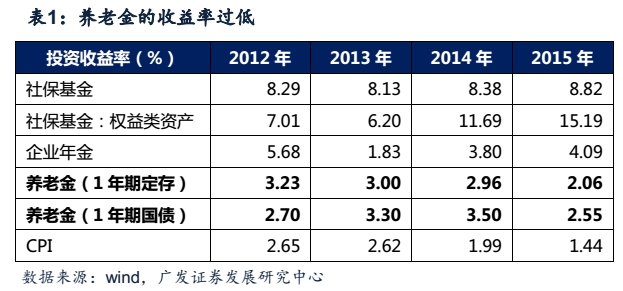

The returns on the pension insurance fund are basically in line with inflation. According to the "State Council's Decision on Establishing a UnifiedThe Decision on Establishing a Unified Basic Old-Age Insurance System for Enterprise Employees stipulates that, after reserving an amount equivalent to two months’ payment expenditures, the fund balance shall be entirely used to purchase national bonds and deposited into special accounts, with strict prohibition against investment in other financial or commercial ventures. Based on this, we approximate that the return rate of pension funds is roughly equivalent to the one-year fixed deposit interest rate (or the one-year government bond yield). As shown in the figure below, on an annual average basis, the return rate of pension funds has basically kept pace with inflation; however, in certain years, pension returns have significantly underperformed inflation. Due to limited investment channels, it is difficult for pension funds to achieve preservation and appreciation of value.

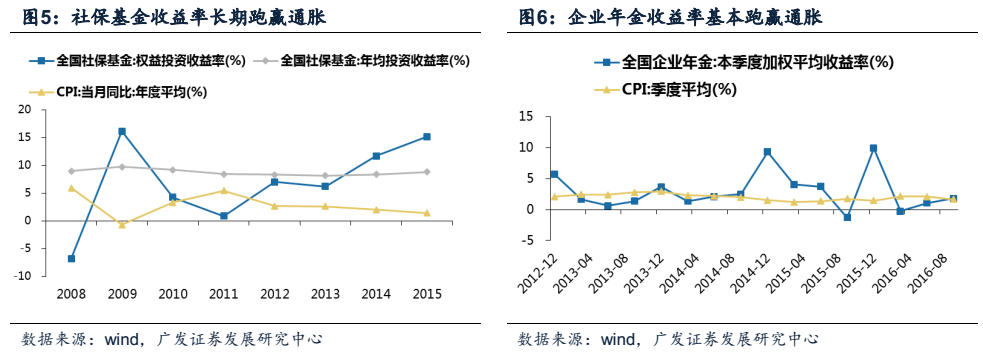

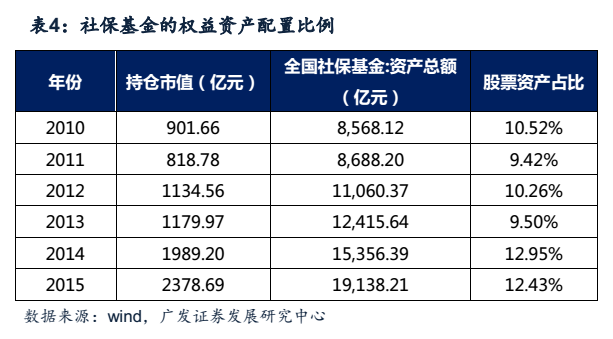

However, the returns of the social security fund and enterprise annuities have significantly outpaced inflation. The average annual investment return rate of the National Social Security FundThe long-term return has remained above 8%, with the long-term average return on equity assets standing at 6.81% (if the impact of the 2008 stock market crash is excluded, the long-term average from 2009 to 2015 was 8.75%). The investment returns of the National Social Security Fund have significantly outpaced the Consumer Price Index (CPI). From 2012 to the third quarter of 2016, the average return rate of enterprise annuities was 2.94%, slightly higher than the average CPI during the same period.of 2.01%.

Compared with the social security fund and enterprise annuity, the return level of pension funds has remained at a low level for a long time, due to investment channelschannels are constrained, making it difficult to even achieve the basic objective of preserving and increasing value. By broadening the investment channels for pension funds and entrusting their management to the National Council for Social Security Fund (NCSSF), allowing pension funds to enter the capital market can enhance returns and achieve capital preservation and appreciation.

2.2 Addressing the “Empty Account” Deficit in Individual Accounts

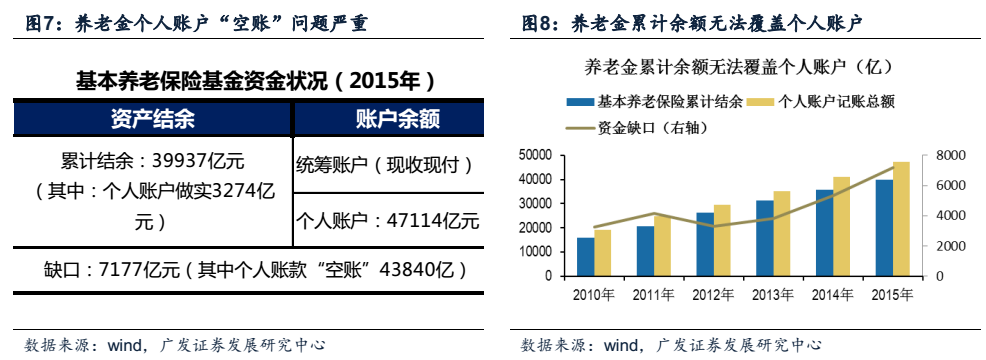

Under the “empty account” problem, cumulative surpluses have long been unable to cover individual accounts. China’s basic old-age insurance adoptsThe model combining social pooling and individual accounts includes both a pay-as-you-go social pooling component (with contributions equal to 20% of the wage base) and a funded individual account component (with contributions equal to 8% of the wage base). Due to historical legacy issues and population aging, the social pooling component has been insufficient to cover current pension expenditures, leading to substantial misappropriation of funds from individual accounts and resulting in severe “empty accounts” in the individual account system.

The funding gap in basic old-age insurance continues to widen, increasing the pressure to preserve and enhance the value of accumulated pension fund surpluses.According to statistics, by 2015, the scale of individual pension accounts had reached RMB 4.71 trillion, while the cumulative surplus of pension funds was only RMB 3.99 trillion. Even if this entire surplus were allocated to individual accounts, there would still be a funding gap exceeding RMB 700 billion, and this gap is widening year by year.

III. The History of Basic Pension Insurance Entering the Stock Market

3.1 The basic old-age insurance system is gradually improving, and the conditions for entering the market are ripe

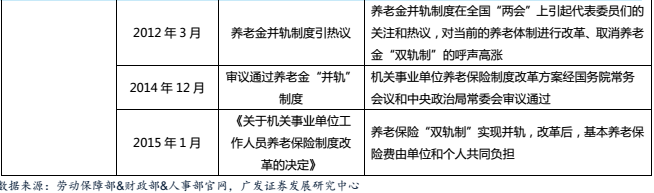

After more than 20 years of development, China’s basic old-age insurance system has been largely perfected. China’s basic old-age insuranceThe system was established in the 1950s, suffered disruption during the Cultural Revolution, entered a recovery phase in the 1970s and 1980s, and began to gradually build and improve the modern old-age insurance system in the 1990s. Since the 1990s, China’s basic old-age insurance system has undergone roughly three major stages: establishing and improving the old-age insurance system for enterprise employees; establishing and improving an integrated urban-rural old-age insurance system; and merging the pension systems for government agencies and public institutions. Currently, apart from the issue of “empty accounts,”Historical issues such as urban-rural integration and the “unification” of pension systems have been resolved, and the objective conditions for the entry of pension insurance funds into the capital marketThe conditions are met.

Note: Pension “empty accounts”—as of 2015, data from the Ministry of Human Resources and Social Security shows that,In individual pension accounts, the recorded balance has reached RMB 4.7 trillion, of which only RMB 330 billion is actually funded—less than one-tenth—resulting in an “empty account” rate exceeding 90%. A notional defined contribution (NDC) system may be adopted in the future, allowing individual accounts to operate on a notional basis with only nominal bookkeeping entries retained (currently under discussion; specific policies have not yet been issued).

3.2 Four Major Stages of Basic Pension Insurance Entering the Stock Market

China’s process of introducing its basic old-age insurance into the capital market began roughly in 2011, undergoing stages of conceptualization, pilot programs, legislation, andImplementation in Four Phases: After Long-Term Preparation, Pension Funds Have Entered the Implementation Phase of Market Entry

(1) Conceptualization Phase (2011–2014): The Research Center of the China Securities Regulatory Commission began proposing basic pension insurance in 2011China’s version of the “401(k) Plan” to channel pension funds into the stock market, advocating for structural adjustments to the pension system to facilitate such investment;

In November 2011, Guo Shuqing, then Chairman of the China Securities Regulatory Commission (CSRC), stated: "If local pension funds in China could be invested in the stock market"Generating returns will greatly benefit individuals, governments, and capital markets.

(2) Pilot Phase (2012–2015): The National Council for Social Security Fund, with the approval of the State Council, separatelyIn 2012 and 2015, it was entrusted to invest in and manage RMB 100 billion each of the accumulated basic old-age insurance funds from Guangdong Province and Shandong Province (disbursed in installments), achieving high investment returns;

(3) Legislative Phase (2015–2016): Primarily clarified the investment scope and operational management of pension insurance funds.Institutions—Investment Scope: The 2015 "Measures for the Administration of Investment of Basic Pension Insurance Funds" expanded the investment scope of basic pension insurance funds, stipulating that the proportion invested in stocks, equity funds, hybrid funds, and equity-oriented pension products shall not exceed 30% of the net asset value of the pension fund;

Operating Agency: The 2016 Regulations on the National Social Security Fund authorized the National Council for Social Security Fund toThe Council operates the basic old-age insurance fund;

(4) Implementation Phase (2016–): In November 2016, four custodian banks for the pension insurance fund were announced (Industrial and Commercial Bank of China(Industrial and Commercial Bank of China, Bank of China, Bank of Communications, and China Merchants Bank); in December 2016, 21 investment management institutions were selected (including 14 fund management companies, 6 insurance companies, and 1 securities company); on January 6, 2016, Guangxi Zhuang Autonomous Region signed a RMB 40 billion entrusted investment contract for pension funds with the National Council for Social Security Fund.

3.3 Guangxi Signs Its First Pension Insurance Investment Contract

Guangxi Officially Signs Pension Fund Investment Contract with the National Council for Social Security Fund, with a Total Scale of RMB 40 Billion. According toAccording to information released on January 6 by the official website of the Ministry of Human Resources and Social Security, the Guangxi Zhuang Autonomous Region has formally signed the “Entrusted Investment Contract for Basic Old-Age Insurance Funds” with the National Council for Social Security Fund. The total amount involved is RMB 40 billion, with RMB 30 billion and RMB 10 billion in entrusted investment funds to be collected and transferred by the end of 2016 and in 2017, respectively. This marks the first provincial-level contract signed since the State Council issued and implemented the “Measures for the Administration of Investment of Basic Old-Age Insurance Funds” on August 17, 2015.

Pension Fund Entrusted Investment Contract.

In 2015, Guangxi’s cumulative pension fund balance was only RMB 45.654 billion, while the amount entrusted to the Social Security Fund for investment management reachedRMB 40 billion (accounting for as high as 87.6% of the entrusted scale) not only reflects the significant pressure on Guangxi’s pension funds to preserve and increase their value, but also sets a precedent for other provinces regarding the investment scale of pension funds (entrusted to the National Social Security Fund). Provinces with relatively small accumulated pension fund balances can increase the proportion of funds under entrusted investment, thereby achieving a substantial scale for pension fund investments.

IV. Estimation of the Total Scale of Basic Pension Insurance Entering the Stock Market: Approaching RMB 250 Billion

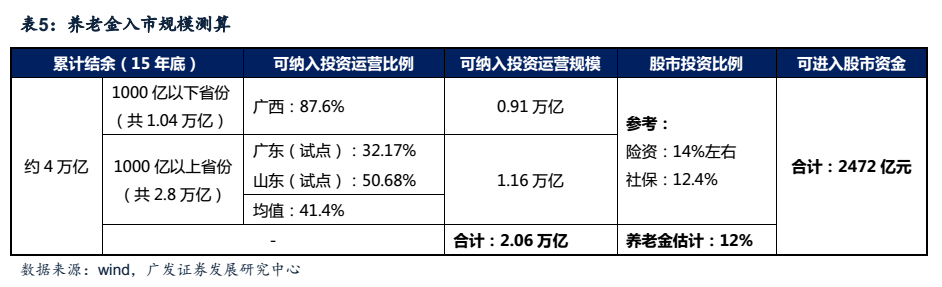

4.1 Pension funds eligible for investment and operational management: approximately RMB 2 trillion

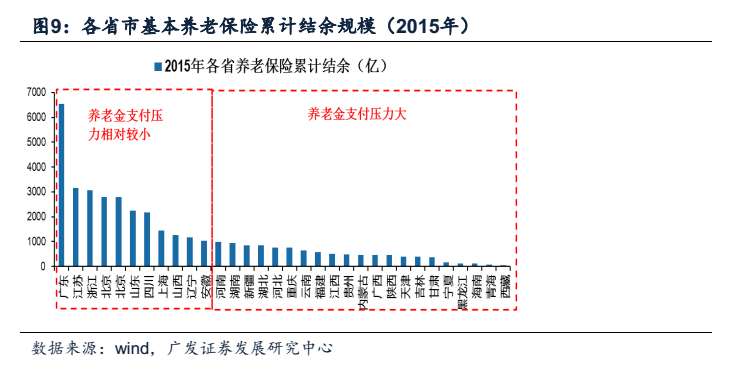

Proportion of pension funds included in investment operations (portion included in investment operations / cumulative surplus) or with cumulative surplusNegative Correlation with Remaining Scale: Provinces with higher cumulative surpluses have a lower proportion of funds included in investment operations, while provinces with lower cumulative surpluses have a higher proportion. Provinces with smaller cumulative surpluses face greater pressure in pension disbursements, making the need for value preservation and appreciation through investment operations more urgent. In contrast, provinces with larger cumulative surpluses experience relatively less pressure in pension disbursements; meanwhile, to ensure fund security, the proportion of pensions included in investment operations tends to be relatively lower.

Provinces with relatively low cumulative pension fund balances (less than RMB 100 billion) have approximately 87.6% of their funds allocated for investment and operational management:Taking Guangxi as an example, the cumulative surplus of pension funds in 2015 was only RMB 45.654 billion, while the amount entrusted to the National Social Security Fund for operation reached RMB 40 billion, accounting for a high proportion of 87.61% (40/45.654 = 87.61%).

Provinces with substantial cumulative pension fund surpluses (exceeding RMB 100 billion) have allocated approximately 41.4% of these funds for investment and operational management. Taking Guangdong and Shandong as examples, both provinces entrusted RMB 100 billion to the National Council for Social Security Fund (NCSSF) for investment and operational management in 2012 and 2015, respectively. During the pilot period, the proportion of pension funds allocated for investment and operational management was 32.17% (100/310.815 = 32.17%) for Guangdong and 50.68% (100/197.298 = 50.68%) for Shandong, yielding an average of 41.43%.

The scale of pension funds available for investment and operation is approximately RMB 2.06 trillion:

(1) Provinces with cumulative pension fund balances below RMB 100 billion: RMB 1.04 trillion * 87.6% = RMB 0.91 trillion

(2) Provinces with cumulative pension fund balances exceeding RMB 100 billion: RMB 2.8 trillion × 41.4% = RMB 1.16 trillion

4.2 Proportion of Pension Fund Investment in the Stock Market: Approximately 12%

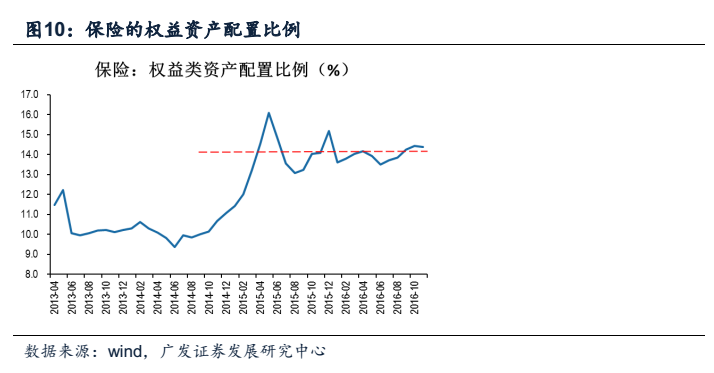

The allocation ratio of equities in pension funds can refer to the data from social security funds and insurance companies, but pensions prioritize capital preservation.have higher requirements and a relatively lower risk appetite. According to calculations, the allocation ratio of equity assets in the National Social Security Fund has been between 12% and 13% over the past two years; meanwhile, the equity asset allocation ratio for insurance capital has fluctuated around 14% since 2016.

Due to the lower risk appetite of pension funds, their allocation ratio to equity assets will be slightly lower than that of social security funds and insurance funds. According to the "BasicThe "Measures for the Administration of Investment of Basic Pension Insurance Funds" stipulate that the proportion of pension funds invested in stocks, equity funds, hybrid funds, and equity-oriented pension products shall not exceed 30% of the net asset value of the pension fund. We believe that the entry of pension funds into the stock market will not immediately reach this upper limit. Referencing historical data from the National Social Security Fund and insurance capital, we estimate that the allocation ratio for pension funds entering the market this time will be around 12%.

4.3 Estimation of Pension Fund Entry into the Stock Market: Nearly RMB 250 Billion

The scale of pension funds entering the stock market may reach 247.2 billion yuan, accounting for 0.45% of the total market capitalization of A-shares, with limited overall impact.

As of the end of 2015, the cumulative surplus of pension funds approached RMB 4 trillion, of which a portion could be entrusted to the National Social Security Fund for investment.The operational scale is approximately RMB 2 trillion. Assuming a 12% allocation ratio of pension funds to the stock market (with an upper limit of 30%), the corresponding investment volume would reach around RMB 250 billion, accounting for 0.45% of the total market capitalization of A-shares, indicating a limited overall impact.

The "Measures for the Administration of Investment of Basic Old-Age Insurance Funds" stipulate that the operation of pension funds shall be conducted by provincial-level governments, which will consolidate local availableInvested pension funds are pooled into provincial-level social security special accounts and uniformly entrusted to pension fund management institutions authorized by the State Council for investment and operation;

The Regulations on the National Social Security Fund stipulate that the National Council for Social Security Fund may operate the basic old-age insurance fund,It is expected that the majority of pension funds entering the market will be channeled through the National Council for Social Security Fund. It is expected that the majority of pension funds entering the market will be channeled through the National Council for Social Security Fund.

This article is excerpted from GF Securities’ “Impact of Pension Funds Entering the Stock Market: Insights from Domestic and International Experience——Special Report on Pension Funds Entering the Stock Market》

Report Authors: Analysts—Chen Jie, Cao Liulong