China's Commercial Health Insurance Market Surges to CNY 500 Billion in 2016 Amid Policy Tailwinds and Rising Demand

Policy and Market Tailwinds: Commercial Health Insurance Holds Immense Potential.

The insurance industry is in a phase of rapid development. Statistical data from the China Insurance Regulatory Commission (CIRC) for January to November 2016 shows that during this period, the gross written premiums for property insurance reached RMB 829.369 billion, a year-on-year increase of 9.76%; premium income for life insurance companies amounted to RMB 2,057.109 billion, a year-on-year increase of 38.61%. The total gross written premiums reached RMB 2.89 trillion, representing a year-on-year growth of 28.88%.

Health insurance refers to a type of insurance under which insurers provide benefit payments for losses resulting from health-related causes, through mechanisms such as critical illness insurance, medical insurance, disability income loss insurance, and long-term care insurance. It is an independent line of business within the life and health insurance sector. Amid the robust growth of the insurance market, both premium income and benefit payout levels in health insurance have risen accordingly.

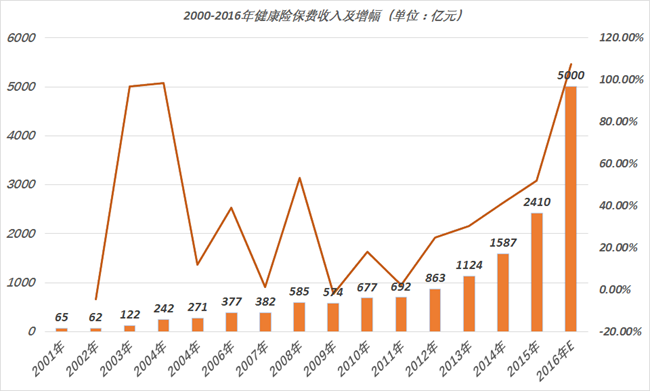

According to a research report by Ping An Securities, the compound annual growth rate of China’s health insurance premium income reached 118.4% during the ten-year period from 2006 to 2015. Based on the insurance density development targets outlined in the new “Ten National Guidelines,” the scale of China’s health insurance market is projected to reach RMB 1.5 trillion by 2020.

As can also be seen from the table above, the explosive growth of health insurance occurred around 2013, driven by the successive introduction of the “Ten National Guidelines on Insurance.” The “Several Opinions on Accelerating the Development of Modern Insurance Services” called for “building an insurance-based social safety net and improving a multi-tiered social security system.” Commercial insurance is to gradually become the primary provider of personal and family commercial protection plans, a key supplier of enterprise-sponsored pension and health security plans, and an active participant in the market-oriented operation of social insurance.

At the level of health insurance, the “Ten National Measures” propose the development of diversified health insurance services. Insurance companies are encouraged to vigorously develop commercial health insurance products, including various types of medical insurance, critical illness insurance, and disability income loss insurance, ensuring their integration with basic medical insurance. Commercial long-term care insurance shall be developed. Health management services—such as disease prevention, health maintenance, and chronic disease management—integrated with commercial health insurance products shall be provided. Support is extended to insurance institutions participating in the integration of the health service industry chain, exploring the establishment of medical institutions and participation in the reform of public hospitals through equity investment, strategic cooperation, and other means.

On the other hand, demand-side drivers are also a significant factor, owing to demographic shifts and the growing emphasis on health insurance in asset allocation.

According to data released by the Ministry of Civil Affairs, China’s total population reached 1.375 billion by the end of 2015, with an average life expectancy of 76.34 years. Among them, the elderly population aged 60 and above numbered 222 million, accounting for 16.1% of the total population. The population aged 65 and above was 143.86 million, representing 10.5% of the total population. It is projected that around 2030, the proportion of China’s elderly population will rise to one-quarter; by around 2050, it will increase to one-third. Population aging has also driven the development of elderly care, nursing services, and critical illness insurance.

Furthermore, the investment attribute of insurance is becoming increasingly prominent, with many people treating insurance as a method of asset allocation. Market research conducted by Kaiying Asset Management Company indicates that in the context of low interest rates both domestically and internationally, insurance is gaining favor as a stable investment option within asset allocations. Many families and individuals with investment intentions are prioritizing insurance as their primary investment choice. In addition to their investment attributes, various health insurance products designed to meet health needs also offer functions such as health management and critical illness coverage, making them popular among institutional insurance investors.

Meanwhile, some Chinese scholars have defined the middle class as individuals with an annual income exceeding RMB 60,000, based on national income and consumption patterns. A recent study by the Institute of Sociology at the Chinese Academy of Social Sciences suggests that China’s middle class is expanding at a rate of one percentage point per year, accounting for approximately 27%–28% of the country’s population in 2015. The continuous growth of the middle- and high-income groups, coupled with their increasing purchasing power, heightened health awareness, and higher expectations for medical services, has provided potential momentum for the development of high-end medical insurance.

Amid favorable policy winds, demographic shifts, and a reallocation of investment demand, health insurance has ushered in sustained growth.

Still Requires Continued In-Depth Development

From a data perspective, health insurance accounts for only 8% of total premiums in China, compared to 40% in the United States. The annual per capita health insurance premium in the U.S. is $16,800, and in Germany it has exceeded $3,000, whereas in China it is only $116. Internationally, when a country’s economy reaches a certain level of development, its medical and healthcare industry also flourishes. Data from developed countries show that the broad health industry typically accounts for 11% to 15% of national GDP, a scale that cannot be overlooked.

Currently, the population coverage of commercial health insurance in China is less than 1%. Compared with the general level in developed countries, where such insurance accounts for 10% of total medical expenditures, there remains substantial room for growth. In 2015, China’s total national health expenditure exceeded RMB 4 trillion, yet insurance claim payouts amounted to only slightly over RMB 50 billion. Commercial health insurance currently accounts for just 3.5% of total medical expenses. Looking ahead, it is poised to play a more significant role in financing healthcare costs. As healthcare reforms deepen, policy dividends enabling commercial insurers to enter the basic medical services market are gradually being realized. The future market space and development potential for health insurance are enormous, and this promising outlook has sparked strong interest from capital investors.

At the corporate execution level, there are basically three operational models for commercial health insurance in China: first, adopting the life insurance business model by designing products and operations in line with the development strategy of life insurance; second, participating in government-administered programs, such as the New Rural Cooperative Medical Scheme, Basic Medical Insurance for Urban Residents, and Critical Illness Medical Assistance, thereby engaging in social basic medical security; and third, developing a health industry chain model that introduces third-party medical institutions to enhance risk management for health insurance.

Currently, there are only seven companies in China offering professional health insurance services. They are PICC Health, Ping An Health, Hexie Health, Kunlun Health, CPIC-Allianz Health, and the two established last year: Fosun United Health Insurance and Ruihua Health.

From a data perspective, the operational performance of specialized health insurance companies has been unsatisfactory. More than 80% of these companies have loss ratios exceeding 80%, approximately 40% have loss ratios surpassing 100%, and some individual companies have even reached as high as 200%. All specialized health insurance companies with publicly available data are currently operating at a loss.

Industry analysts attribute losses in the health insurance sector to both internal and external factors. On the internal front, there is a mismatch between the supply and demand structures of health insurance products, along with an imbalance in insurance categories: disease insurance accounts for more than half of the market, followed by medical insurance. The structure of long-term and short-term health insurance is unreasonable, creating a supply-demand inversion; furthermore, products lack specificity and exhibit poor market segmentation capabilities. Statistics show that in 2015, China’s elderly population accounted for 16.1%, a figure projected to reach 24.4% by 2030. Chronic diseases already account for 77% of healthy life years lost and 85% of causes of death. The increasingly severe aging population and high incidence of chronic diseases have spurred substantial demand for long-term care insurance. However, long-term care insurance currently holds less than a 1% share of the market, and disability income loss insurance remains nonexistent. Additionally, there are deficiencies in product development, pricing, and risk control capabilities, as well as a low level of specialization in product development. A lack of innovation and serious product homogenization have led to vicious competition within the industry. Both disease insurance and medical insurance businesses are primarily competing for resources among mid-to-low-end customers, driving prices down significantly and shrinking profit margins.

Regarding external factors, the health insurance service chain is relatively long, encompassing social security and healthcare while extending into multiple sectors such as wellness and preventive care, which poses significant challenges for risk management. Health insurance companies typically enter the market by establishing designated partnerships with public hospitals. However, due to their inability to intervene in medical diagnoses to control healthcare costs, it is difficult to manage medical expenses and mitigate moral hazard, resulting in persistently high loss ratios. Meanwhile, integration with the social security system remains a blind spot; the lack of uniformity among local medical insurance IT platforms prevents access to complete and effective information.

Therefore, the promotion of health insurance business should start with optimizing the product mix and developing new products, while exploring collaborations with social security entities, medical service providers, and long-term care institutions across the broader health ecosystem. This approach aims to facilitate more in-depth product development and extend the operational lifecycle of insurance offerings.

“The Road to Health” Is a Long and Arduous Journey

Industry experts state that commercial health insurance is highly specialized and differs significantly from ordinary life insurance in terms of actuarial principles, risk control, and business models. It is essential to leverage professional expertise and actively draw on international experience in data collection and rate setting under a specialized operational framework, thereby achieving genuine product segmentation and risk stratification. Meanwhile, relevant insurance products should be fully integrated with the health risk management industry chain to create a closed-loop system for personal health management that spans from treatment to prevention. This integration will enhance risk control capabilities. In short, insurers offering health insurance can only fundamentally reverse current losses by strengthening their core competitiveness: internally, through continuous improvement in management standards and actuarial techniques; externally, by gaining greater influence over hospital medical expenditures. The future development of health insurance requires policy support to promote the application of medical big data, establish a medical cost-control system linking commercial insurers with social health insurance data, and extend strategic layouts into the broader health industry. As health insurance service capabilities improve, the focus will gradually shift from post-event claims settlement to pre-event health intervention, thereby delivering truly professional health management services.

Industry insiders say that health insurance is on the eve of an explosion. The development of health insurance lies in the reform of the entire supply side and the medical and health system. Because if insurance companies need to integrate many resources, they need the support and coordination of the medical and health system. In the past, insurance companies had no voice in front of public hospitals, but due to the current regionalization of hospital drugs, hospitals are also facing great pressure, and their willingness to cooperate with insurance companies is also strengthening.

From a capital perspective, health insurance lacks the characteristics favored by investors, such as rapid return on investment and high rates of return. The health insurance service chain is long, encompassing multiple sectors including social security, medical healthcare, and wellness care. Its cross-industry nature makes risk control more complex and operational management more challenging. In particular, with the accelerated advancement of the new healthcare reform and the comprehensive rollout of critical illness insurance, there is an even greater need for advanced professional expertise and service capabilities. Moreover, the profitability cycle for health insurance is lengthy, typically spanning ten years or more, which poses a significant test to shareholders’ capital strength, sustained investment capacity, and solvency. Strategically, entities entering this field must be committed to deep cultivation of the health insurance sector, uphold “insurance is fundamentally about protection” as their foundational business principle, remain anchored to a “protection-oriented” approach without deviation, and achieve their own growth and expansion while serving economic and social development.

This article is edited based on Health Point’s “The Eve of the Commercial Health Insurance Boom”

Original Article Link:http://www.healthpoint.cn/archives/52566