Investment Opportunities in Primary Care in 2017 (Part II): Comprehensive Scan of 83 Related Enterprises

In the previous article《Investment Opportunities in Primary Healthcare in 2017 (Part I): Which Industries Benefit from the Rise of Primary Healthcare Services?》In China, VCBeatThis analysis focuses on the opportunities brought to primary healthcare by the promotion of tiered diagnosis and treatment. Seizing policy opportunities, addressing challenges in primary healthcare, and identifying investment prospects are fundamentally driven by the aim of resolving the pain points in this sector.

The emergence of these opportunities is primarily attributable to the following factors.

First, the number of primary healthcare institutions is vast, far exceeding that of hospitals, thereby expanding the customer base for medical industry enterprises by nearly 20-fold compared to hospitals alone. Second, outpatient visits are shifting from tertiary hospitals to primary healthcare institutions, which are poised to meet 70–80% of routine medical service demands in the future, significantly enlarging the market potential. Third, primary healthcare services suffer from inadequate capacity, including deficiencies in both hardware/software infrastructure and the professional competence of medical staff; addressing these pain points presents substantial commercial opportunities. Fourth, there remain market gaps or newly emerging segments within the primary healthcare sector, such as various portable smart medical devices, express delivery services for medical laboratory specimens, and private chain community clinics, representing new blue-ocean markets.

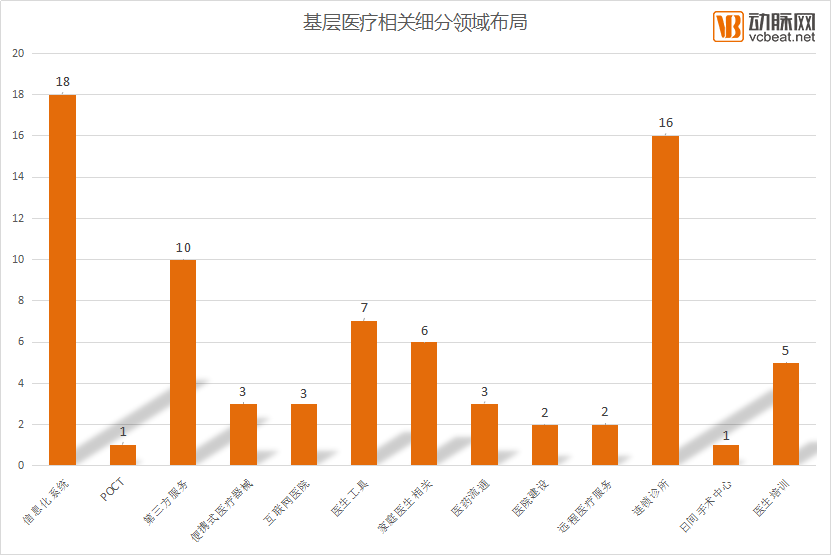

Primary Care-Related Startups

Data source: VCBeat, Eggshell Research Institute database

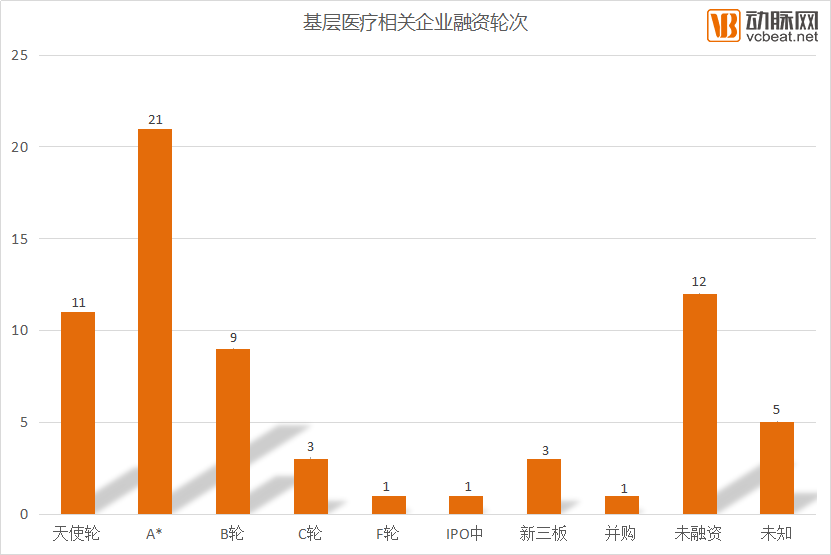

Data source: VCBeat, Eggshell Research Institute Database

VCBeat compiled statistics on 67 startups related to primary healthcare, which are distributed across several major sectors, including healthcare informatics, in vitro diagnostics (IVD), third-party services, pharmaceutical distribution, and chain clinics (some companies have multiple projects). The top three sectors are informatics systems, chain clinics, and third-party services, with 18, 16, and 10 companies, respectively.

Data Source: VCBeat, Eggshell Institute Database

In terms of funding rounds, most primary care-related startups are at the A* and angel stages, while companies that have progressed to Series B and beyond account for one-quarter of the total. Notably, there are 12 unfunded enterprises, ranking second in number. However, these companies are not in their early development stages; rather, they are self-funded by their founders, with the majority achieving remarkable performance.

Information System

In our previous article, we analyzed that the promotion of tiered diagnosis and treatment would significantly benefit companies in the medical informatics sector. This is because primary care institutions have relatively weak service capabilities, creating a strong need for primary care physicians to enhance their professional competencies and skills. The most pressing need in primary care is leveraging new technologies to connect with specialists and higher-level medical institutions, thereby facilitating the learning and professional development of grassroots healthcare personnel.

The growing demand for informatization among primary healthcare institutions has raised the bar for health IT vendors. Hospital Information System (HIS) products must align with the specific needs of these primary care settings, which differ significantly from those of traditional hospitals. Traditional HIS solutions are generally designed to meet the requirements of large, high-tier hospitals. In contrast, primary healthcare institutions focus on providing preventive care, chronic disease management, and treatment of common illnesses for the general population. Their systems require more streamlined functionalities, necessitating that IT vendors develop tailored products to meet these distinct needs.

There is a vast number of primary healthcare institutions. Although cloud-based Hospital Information System (HIS) products have lower unit prices, the sheer volume of primary care facilities—exceeding that of tiered hospitals by several orders of magnitude—results in a larger overall market size. However, promoting these solutions to primary healthcare institutions presents significant challenges, as vendors must extend their distribution channels deeper into local markets and address a more fragmented customer base.

In addition to traditional Hospital Information Systems (HIS), many related software systems should also fall within the business scope of software enterprises, such as Software-as-a-Service (SaaS), physician tools, telemedicine, and tiered diagnosis and treatment systems. By using software to connect primary care physicians with patients and link hospitals at different levels, there is considerable room for growth. However, the number of healthcare informatics companies is currently quite large, with many listed companies participating, making it challenging for startups to develop. Moreover, although there are numerous primary healthcare institutions, their ability to pay is generally limited. Therefore, while opportunities exist, the challenges are significant.

Third-Party Services

In the field of clinical laboratory testing, currently only about 5% of tests are outsourced to third-party laboratories, while 95% of testing services are still performed in hospital laboratories. In contrast, the top three companies in the United States hold a combined market share of over 60%, indicating a high level of market concentration. In developed countries and regions such as Europe, the United States, and Japan, independent laboratories already account for one-third of the clinical testing market. Therefore, there is significant growth potential for the third-party testing market in China.

Taking Dian Diagnostics, a third-party medical testing company listed on the ChiNext board, as an example, its operating revenue in the 2016 semi-annual report reached RMB 1.628 billion, representing a year-on-year growth of 100.19% compared to the same period in 2015, indicating a very rapid growth rate. China’s third-party medical testing industry is still in its early stages of development, with a relatively small overall market size. The compound annual growth rate (CAGR) of the third-party testing market in the coming years is expected to exceed 20%, driving high-speed development.

The third-party medical laboratory testing model, which includes regional clinical laboratories, has proven highly successful abroad. Under this model, hospitals retain only emergency testing services, while outsourcing all non-emergency tests to third-party service providers. This approach offers several advantages:1. It reduces government fiscal expenditure by eliminating the need for each hospital to duplicate purchases of medical equipment.2. It enables regional resource sharing, allowing test orders and results to be mutually recognized across all hospitals within the same city. This avoids redundant testing for the same parameters, thereby saving on medical insurance expenditures and facilitating patient access to care.3. It allows primary care institutions, particularly those serving rural populations, to transport specimens requiring analysis to centralized regional clinical laboratories via cold-chain logistics. This alleviates the burden of overcrowding at large hospitals and improves patient satisfaction.4. By consolidating laboratory departments through medical consortium models, county-level hospitals significantly enhance their professional capabilities. The range of available test items can increase from approximately 300 to around 1,000, also boosting hospital revenue.5. With independent accounting, clinical laboratories achieve greater economic efficiency, leading to a substantial increase in the income of laboratory physicians.

In addition to third-party laboratory testing, the third-party services sector also includes numerous third-party medical imaging institutions. Due to their ease of standardization, high replicability, and suitability for remote operations, these institutions are significantly driven by technological advancements. They represent a highly viable business model in primary healthcare delivery, offering strong profitability and growth potential. The National Health and Family Planning Commission (NHFPC) previously issued the Basic Standards and Management Specifications for Medical Imaging Diagnostic Centers (Trial), which encourages the development of third-party medical imaging diagnostic centers. On the basis of supporting private capital participation, the policy promotes chain-based and group-oriented development and prioritizes approval for establishment.

Revenue data from China’s Tier 3A hospitals show that general medical imaging accounts for approximately 20% of total hospital revenue, with a growth rate surpassing that of pharmaceuticals. If imaging services can be decentralized from hospitals, regional imaging centers will have substantial room for growth. Data collected by third-party medical imaging centers must be integrated between primary healthcare institutions and higher-level hospitals to maximize its value, thereby creating opportunities for IT enterprises in cloud-based data transmission.

In the realm of third-party services, it is still relatively easy to identify new market gaps. For instance, KuaiYiJian, a company listed in our table, provides cold-chain transportation services for laboratory specimens from primary healthcare institutions to third-party testing centers. This remains a novel market opportunity, enabling the company to achieve rapid growth.

Chain Clinics

Community clinics are small in scale and numerous, offering convenient access to medical care for residents. However, the lack of standardized management and the low proficiency of physicians have led to a deficit in public trust, which constitutes the core challenge in the national push for tiered diagnosis and treatment. In contrast, chain clinics win over patients through standardized management and high-quality clinical environments.

Chain clinics currently follow two distinct development models. One comprises premium chain clinics targeting mid-to-high-end clients, such as United Family Healthcare, Jiahui Health, and Zhuozheng Medical. The other consists of mid-range chain clinics that significantly outperform the fragmented model of traditional solo private practices, such as Zhengguangxing, Dr. Lv, and Baihuiji.

Over the next five years, community healthcare revenue is projected to reach RMB 360 billion, with a growth rate as high as 23%. Chain community clinics will serve as pioneers in the private community healthcare sector. Private chain clinics will undertake a significant portion of primary care services, with their value increasingly recognized and gradually attracting attention from capital markets and internet companies. In first- and second-tier cities, chain clinics are most likely to become the fastest-growing primary healthcare institutions, while in other regions, community healthcare facilities and township health rooms will remain the main providers of medical services.

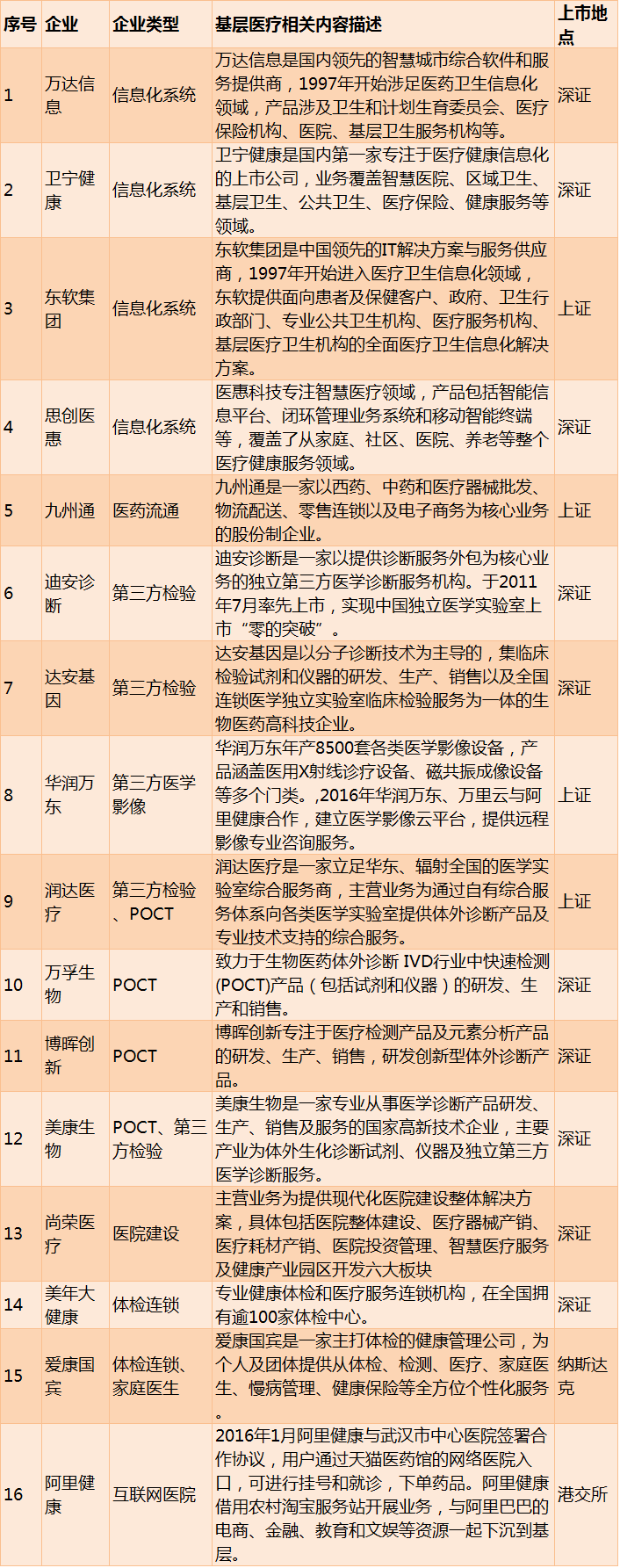

Listed Companies in Primary Healthcare

Data Source: VCBeat, VBInsight Database

The primary healthcare market boasts a substantial capacity of RMB 450 billion. This lucrative segment is attracting not only startups but also publicly listed companies, which are eager to capitalize on this opportunity. Among the 16 listed companies we analyzed, in addition to those focusing on health information systems and third-party services, several operate in the point-of-care testing (POCT) sector. POCT currently represents both the most advanced concepts and technologies in laboratory medicine and the “appropriate” medical testing techniques and methods well-suited for China’s primary healthcare settings. It stands as one of the most dynamic fields within biotechnology, biomedical engineering, and related disciplines.

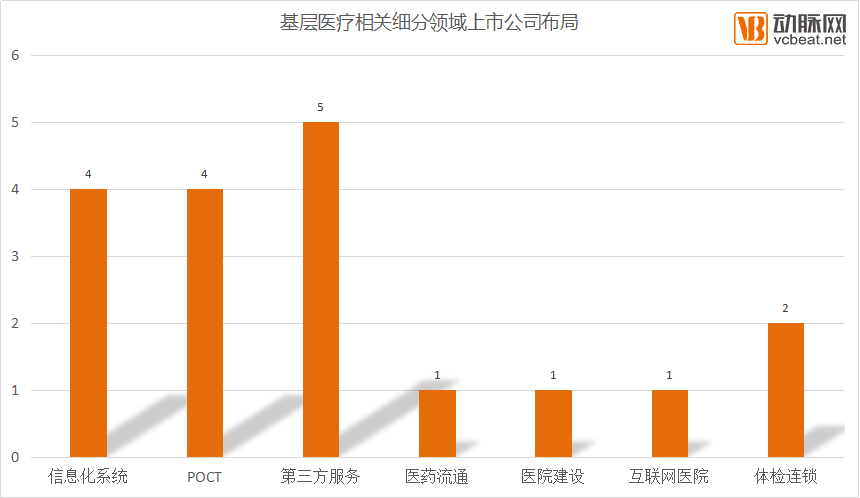

Data Source: VCBeat, Eggshell Research Institute Database

China’s primary healthcare institutions suffer from a shortage of medical resources, low levels of equipment configuration, and relatively low diagnostic and treatment technical capabilities, particularly in vast rural grassroots areas. In contrast, Point-of-Care Testing (POCT) can perform nearly all tests conducted in clinical laboratories. POCT instruments are miniaturized and automated, with simple and convenient operation that allows even healthcare workers or patients to use them. This eliminates the cumbersome process of specimen collection and delivery, while providing timely and accurate results, making POCT highly suitable for primary healthcare settings.

In 2015, the market size of in vitro diagnostics (IVD) in China reached RMB 30 billion, while the point-of-care testing (POCT) market stood at RMB 5 billion. After excluding imported brands, the market share available for domestic brands was approximately RMB 2 billion. Domestic POCT companies, represented by Wondfo, are poised to seize greater development opportunities in the primary healthcare market.

Addressing Pain Points Creates Investment Opportunities

For a long time, the perceived bottleneck of healthcare reform has been the weakness of primary care institutions. The state has invested substantial human, material, and financial resources in an effort to establish a healthcare system characterized by initial consultations at the primary level, two-way referrals, and tiered diagnosis and treatment. However, the outcomes have been less than satisfactory.

However, no matter how daunting the challenges facing healthcare reform may be, there is no room for retreat; the issues plaguing primary care institutions are an insurmountable hurdle that must be addressed. Resolving these problems and achieving tiered diagnosis and treatment represent the opportunities presented by the market. How can we improve the service quality of primary care physicians? How can we standardize clinical protocols? How can we enhance mutual trust between doctors and patients? These are all significant challenges confronting primary care institutions.

Challenges and opportunities coexist: this is the new opportunity that primary healthcare in 2017 has brought to the market.

Primary HealthcareUnderstanding Primary Healthcare Here

Focusing on Reporting the Industrial Transformation Brought by New Technologies Empowering Primary Healthcare

Welcome to scan the QR code to follow the WeChat account of Primary Care Health. For reprints on websites, official accounts, etc., please contact liu.zy@vcbeat.top for authorization.

Copyright Statement

This report is produced by VCBeat. All text, images, and tables contained herein are protected by applicable trademark and copyright laws. Portions of the text and data have been sourced from publicly available information, with ownership retained by the original authors. No organization or individual may reproduce or distribute this report in any form without prior written permission from our company. Any unauthorized commercial use of this report shall constitute a violation of the Copyright Law of the People's Republic of China, other relevant laws and regulations, and applicable international conventions.

Disclaimer

This research report is based on information that VCBeat considers reliable and currently publicly available. VCBeat strives to, but does not guarantee, the accuracy and completeness of such information. Due to limitations in research methodologies, sample sizes, and the scope of data collection, the data presented herein only reflects the basic conditions of the surveyed population during the survey period. It is intended solely for the current research purposes and serves as a basic reference for the market and clients. Furthermore, VCBeat does not guarantee that the opinions or statements contained herein will remain unchanged. At different times, VCBeat may issue reports with information, opinions, and projections inconsistent with those contained in this report.

VCBeat does not consider recipients of this report as its clients by virtue of their receipt thereof. This report is distributed only where permitted by applicable laws and regulations and solely for informational purposes; it shall not be construed as advertising in any manner. Under no circumstances shall the information contained herein or the opinions expressed constitute investment advice to any person. Where permitted by law, VCBeat and its affiliated entities may hold equity interests in the companies mentioned in this report and may provide or seek to provide financing, financial advisory, or other related services to such companies.

If you are an entrepreneur in the primary healthcare sector, please feel free to contact the author of this article, Liu Zongyu (WeChat ID: q19930797). Entrepreneurs and investors in the primary healthcare field may also contact Yan Jingjing from the Investment Department of VCBeat (WeChat ID: 13717606110).