Three Key Sectors Set to Benefit Most from China's Thriving Digital Healthcare Landscape

Federico Sferrazz, Digital Marketing Manager at Daxue Consulting, offers insights into healthcare digitalization in China, explaining in an article how technological advancements—particularly mobile technology—can help alleviate the country’s healthcare challenges. VCBeat (WeChat ID: vcbeat) has compiled and translated his perspectives.

China’s digital technology market is largely dominated by a triad of mobile technology, social media, and e-commerce. In contrast, the healthcare industry appears less “modern,” with its level of digitalization consistently lagging behind. While new technologies indeed pose significant challenges to the healthcare sector, they also herald substantial opportunities—namely, the ability to treat patients through innovative and personalized approaches.

Today, Chinese consumers are embracing digital technology at a remarkably rapid pace, profoundly influencing the behaviors and lifestyles of the new generation of consumers. The healthcare industry is also accelerating its pace of innovation. In the first half of 2016, private investment in the digital health sector reached $1.4 billion, surpassing the total investment for the entire year of 2015. Below, we will elaborate in detail on how new technologies will help address China’s healthcare challenges.

Overview of the Internet Healthcare Market

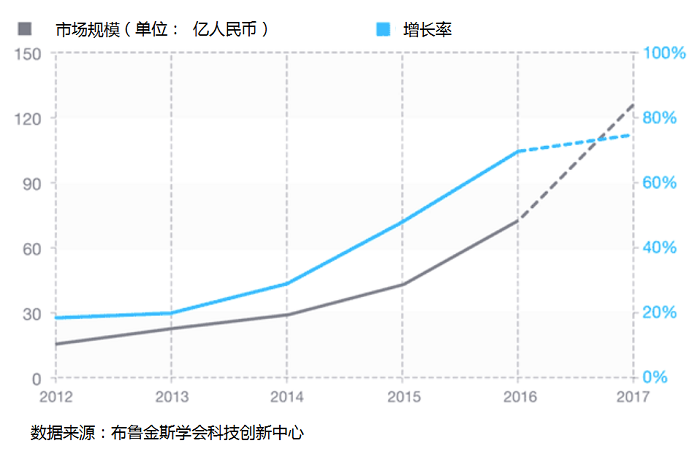

Mobile health (mHealth) technology has garnered global attention, and in China, it is poised to become the most significant technological breakthrough of the new year. In 2016, the scale of China’s mHealth market was approximately RMB 7 billion; it is projected to exceed RMB 10 billion in 2017, representing a forecasted growth rate of 74.5%. The number of mHealth applications has surged over the past five years, attracting numerous startups and investors. However, thus far, most of these apps remain limited to basic functionalities, with self-diagnosis and medical examination products accounting for only 8%, and medical information retrieval products comprising merely 6%. Although mobile health applications are still in their early stages of development, they are highly likely to play a pivotal role in the market in the near future.

Mobile Healthcare Market Trends

Three Key Focus Areas of Mobile Health

Quality: The validity of shared medical information will be emphasized. In other words, as the level of informatization brought about by mobile healthcare increases, so do the quality requirements for medical information. For example, electronic prescriptions can help reduce errors in the healthcare process (such as redundant examinations) and improve the accuracy of medication and treatment. If the electronic prescription system is comprehensively improved, patients can avoid unnecessary expenses while receiving efficient treatment.

Accessibility: In China, patients sometimes struggle to access appropriate medical care, while mobile health offers services that are easy to disseminate, tailored, and readily accessible. Patients in remote communities can receive preliminary diagnoses via telemedicine video consultations; the most active segment of healthcare consumers—patients aged 25 to 34—almost unanimously praise the benefits of internet-based healthcare.

Cost Savings: An interesting phenomenon has been observed—among users of mobile health applications, more than 26% have a monthly income below RMB 2,000. This trend may be attributed to this demographic’s greater tendency to use symptom-checking apps for self-diagnosis, thereby avoiding medical consultation fees and conducting preliminary research before seeing a doctor.

Application Area 1: Digital Insurance Market

Although China’s insurance industry has a history spanning several centuries, a formal insurance system did not truly emerge until 1980, with the sector’s most significant surge occurring over the past decade. Today, China is the world’s third-largest insurance market, and with the advent of digital technologies, the industry is heading in an entirely new direction.

Digital insurance services represent the integration of traditional insurance practices with emerging technologies. By leveraging digital distribution, big data, and blockchain technology, this sector has experienced sustained growth over the past five years. Utilizing these tools, the insurance industry has rapidly expanded, continuously launching insurance products tailored to diverse needs. According to data from the Insurance Association of China, the digital insurance market in China reached RMB 81.6 billion in the first half of 2015, marking a year-on-year increase of 260%. It is projected that by 2020, the digital insurance market will account for 24% of the entire insurance sector, equivalent to RMB 912 billion.

A major factor driving the growth of China’s mobile healthcare market is the demand for private insurance beyond public insurance schemes. Data from Ernst & Young (EY) indicates that 93% of respondents were dissatisfied with their existing insurance coverage, and among them, 33% lacked savings to cope with critical illnesses. Government measures to lower regulatory barriers and introduce tax incentives have further created favorable opportunities for the development of digital insurance.

Application Area 2: Pharmaceutical Market

China is the world’s second-largest pharmaceutical market. The market is projected to grow from $108 billion in 2015 to $167 billion in 2020, representing a compound annual growth rate of 9.1%. Pharmaceutical sales recently accounted for 17% of total healthcare expenditure, averaging $78 per capita, with essential medicines comprising 64% of these sales. The pharmaceutical industry—encompassing chemically synthesized drugs, traditional Chinese medicine, medical devices and instruments, healthcare supplies, packaging materials, and pharmaceutical machinery—has become one of China’s leading sectors.

In 2016, approximately 50% of the industry’s revenue came from prescription drugs, most of which had been launched in the preceding five years, with the elderly population constituting the primary consumer base. However, China’s over-the-counter (OTC) drug market also demonstrated significant growth. According to data from the China Non-Prescription Medication Association, this market has been growing at an annual rate of approximately 17%, outpacing the rest of the Asia-Pacific region. Market research firm Espicom estimates that China will become the world’s largest OTC market by 2020.

China’s current demographic landscape inevitably drives further growth in medication demand, positioning the country to potentially become the world’s largest producer and exporter of active pharmaceutical ingredients (APIs), especially given that China already accounts for 40% of global API production. As the government progressively promotes pharmaceutical research and development, China’s pharmaceutical industry is poised for further innovation, fostering collaboration between major domestic and international pharmaceutical companies. With the advancement of the pharmaceutical sector, digital health technologies will be increasingly utilized to enhance medication adherence, support clinical trials, and facilitate market research.

Application Area 3: Pharmaceutical E-commerce

![C]WVK96[}OZ8Q]3RHF)R@5E.png](https://cdn.vcbeat.top/upload/image/09/02/06/05/1486371952423143.png)

As policies have gradually eased, pharmaceutical e-commerce has entered a development phase. Although the industry is still in its early stages, its growth rate lags behind that of products with already mature trading markets. The number of online pharmacies grew from 28 in 2011 to 387 in 2016, largely benefiting from the increasing prevalence of online shopping and mobile technology. Meanwhile, China’s online pharmaceutical sector has become increasingly prosperous, with sales rising from RMB 1.6 billion in 2012 to over RMB 10 billion in 2015. The liberalization of online prescription drug sales has clearly opened new entry points into the pharmaceutical market for many e-commerce platforms, and as regulatory policies continue to evolve, more competitors are expected to enter this market.

Here, the development of pharmaceutical e-commerce faces two major challenges. On one hand, policies allowing medical insurance to cover online medication purchases are a significant driver for online drug sales; however, due to the lack of uniformity in social security systems across China, sales volumes vary considerably. On the other hand, since the online sale of prescription drugs cannot be decoupled from the hospitals that issue the prescriptions, penetrating the upstream supply chain has become critical.

On the day when online pharmaceutical sales leap from the tens of billions to the 150 billion level, online drug sales will account for 10% of the entire pharmaceutical market, thereby entering a brand-new stage of development. Based on this optimistic forecast, China’s pharmaceutical e-commerce market is projected to reach nearly RMB 400 billion in sales revenue by 2020.

Conclusion

Mobile health holds the potential to reform healthcare delivery and improve the quality of medical care. Advances in telecommunications, the ubiquity of smartphones and mobile devices, and the continuous optimization of IT infrastructure are all driving healthcare toward greater efficiency and lower costs. However, challenges such as policy regulation, health insurance systems, and the integration of healthcare services remain critical issues that must be addressed in the application of mobile technologies to healthcare.

China’s healthcare demands and prospects are continually evolving. Over the past few decades, the country has made significant progress in improving population health, particularly in epidemiology; however, chronic non-communicable diseases such as cardiovascular and cerebrovascular disorders and diabetes have emerged as new challenges, necessitating reforms in healthcare delivery. The value of mobile health is thus becoming evident, as it can transform our approach to addressing these issues and effectively alleviate pressures on the healthcare system. Nevertheless, to fully realize its potential, digital technologies must be widely piloted and adopted across the healthcare sector.