Minsheng Securities 2017 Annual Strategy Report (Part I): Pharmaceutical Sector Rebounds from Cyclical Trough with Accelerating Growth

This article is Minsheng Securities’ 2017 annual strategy report on the pharmaceutical and biotechnology sector. VCBeat has been authorized to republish it and will subsequently release a series of categorized reports. Stay tuned for more updates.

Highlights of This Issue

In the first half of 2016, revenue in the pharmaceutical industry increased by 1.23 percentage points year-on-year, indicating a clear trend of recovery. We believe that the negative impacts on the industry are gradually easing. Long-term drivers such as population aging and consumption upgrading remain unchanged. Meanwhile, healthcare expenditure currently accounts for approximately 6% of GDP, which is still relatively low. With accelerated medical insurance reforms and the emergence of new technologies, the industry continues to offer broad prospects for growth.

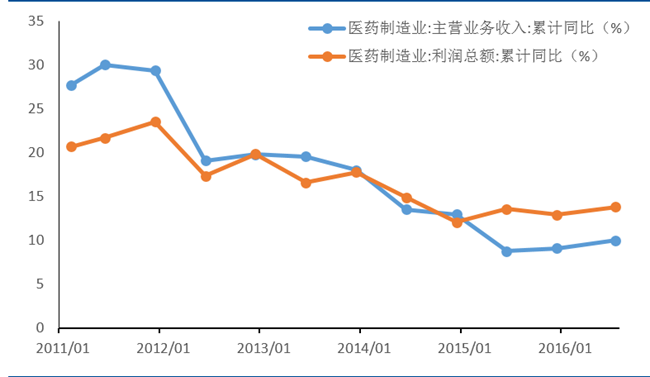

According to data from the Ministry of Industry and Information Technology (MIIT), from January to June 2016, pharmaceutical industrial enterprises above designated size achieved main business revenue of RMB 1.363565 trillion, a year-on-year increase of 10.14%, representing a 1.23 percentage point rise compared to the same period last year. The total profit amounted to RMB 144.967 billion, up 14.61% year on year, an increase of 1.76 percentage points over the same period in the previous year. In comparison with data from the National Bureau of Statistics through July this year, the main business revenue of the pharmaceutical manufacturing industry grew by 10.0% year on year, while profit growth reached 13.8%. The overall growth rate of the pharmaceutical industry shows a clear trend of recovery compared to the same period last year.

Figure 1: Changes in Revenue and Profit Growth Rates of the Pharmaceutical Industry, 2011–H1 2016

Source: National Bureau of Statistics, Minsheng Securities Research Institute

Overall, the pharmaceutical industry exhibited a clear trend of recovery in growth during the first half of the year, performing better than the general expectations of both the industry and the market. We attribute this primarily to the diminishing impact of normalized healthcare insurance cost containment measures on the sector. Furthermore, as drug procurement bidding processes remain incomplete in most provinces and municipalities, the impact of price reductions and other factors on the industry has remained limited. Meanwhile, since 2015, the overall profit growth rate of the industry has outpaced its revenue growth rate, which we believe is mainly driven by declining costs of traditional Chinese medicine raw materials and manufacturers’ effective cost control.

Looking ahead to future industry trends, in the short term, with 2017 as the key milestone referenced in healthcare reform policies, medical insurance cost containment and the cap limiting pharmaceutical expenditure to 30% of total medical costs remain the policy factors exerting the greatest impact on the industry. The imminent implementation of a new round of drug procurement bidding will also have a significant effect; therefore, industry growth will continue to face substantial pressure in the near term. From a medium- to long-term perspective, however, we believe there is no cause for pessimism. Driven by population aging and economic growth, domestic demand for healthcare services remains robust. Currently, healthcare expenditure accounts for only 5–6% of China’s GDP, still well below the 10%+ levels seen in major countries worldwide, indicating ample room for future industry expansion.

In the first half of 2016, the main business revenue of all pharmaceutical sub-sectors maintained a growth rate of over 6%. The fastest growth in main business revenue was seen in traditional Chinese medicine (TCM) decoction pieces and medical instruments and equipment, which have outperformed the industry average growth rate for three consecutive years. Under the influence of policies such as zero markup on drugs and control of the drug proportion, these two sub-sectors benefited the most significantly. The most notable improvement was observed in proprietary Chinese medicines, with the growth rate increasing by 3 percentage points compared to the same period in 2015. The year-on-year growth rate declined for pharmaceutical manufacturing equipment and sanitary materials, with pharmaceutical manufacturing equipment decreasing by 1.3 percentage points, making it the worst-performing sub-sector.

Figure 2: Comparison of Revenue Growth Rates Across Pharmaceutical Sub-sectors (2014–2016 H1)

Source: Ministry of Industry and Information Technology, Minsheng Securities Research Institute

In terms of profitability across sub-sectors, the fastest growth was seen in bulk chemical pharmaceuticals and medical instruments and equipment. The growth in bulk pharmaceuticals was primarily driven by the rise in vitamin prices since late last year. While traditional Chinese medicine (TCM) patent medicines experienced an acceleration in revenue growth, their profit growth remained lackluster, likely due to the recent increase in prices of TCM herbal materials. Pharmaceutical equipment manufacturing was the only sub-sector to report negative profit growth, marking its second consecutive year of decline, mainly attributable to shrinking market demand following the peak period for compliance with the new Good Manufacturing Practice (GMP) certification requirements.

Figure 3: Comparison of Revenue Growth Rates Across Pharmaceutical Sub-sectors, 2014–H1 2016

Source: Ministry of Industry and Information Technology, Minsheng Securities Research Institute

From a cross-sector comparison of various sub-industries, it is recommended to focus on the traditional Chinese medicine (TCM) decoction pieces and medical device sectors, which benefit from healthcare reform policies.TCM decoction pieces are excluded from the drug revenue ratio and are not subject to the zero-markup policy; therefore, they are expected to maintain robust growth in the hospital market. The government has recently introduced multiple supportive policies for traditional Chinese medicine (TCM), indicating a positive outlook for the sector’s future development. Consequently, the TCM decoction pieces and formula granule industries will remain highly prosperous. Meanwhile, national quality control standards for TCM raw materials and decoction pieces are being progressively strengthened, which will drive low-quality manufacturers out of the market and increase industry concentration, benefiting leading enterprises. Medical devices have significantly benefited from healthcare reform policies. Under constraints on the drug revenue ratio, hospitals are increasing non-pharmaceutical revenue streams, such as diagnostic tests and examinations, thereby continuously stimulating sales growth of medical devices and consumables. Additionally, the medical device sector is bolstered by favorable factors including policies supporting domestically produced medical equipment and the expansion of primary healthcare markets under the tiered diagnosis and treatment system.

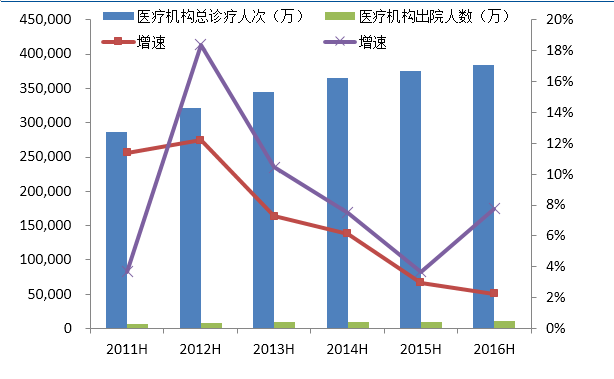

1. Number of patient visits.According to the newly released data from the National Health and Family Planning Commission, the total number of outpatient and emergency visits at medical and health institutions across China reached 3.85 billion in the first half of 2016, a year-on-year increase of 2.3%, with the growth rate declining by 0.7 percentage points compared to the same period last year. However, the slowdown in the overall growth of visits was primarily driven by a 0.9% year-on-year decrease in visits to primary care medical institutions. In contrast, hospitals recorded 1.57 billion visits, representing a 6.1% year-on-year increase and an acceleration of 0.2 percentage points in growth rate. The significantly stronger growth in hospital visits compared to primary care facilities indicates that urban and rural residents still prefer seeking treatment at large hospitals, underscoring that the implementation of tiered diagnosis and treatment remains a long and arduous task.

2. Number of Discharged Patients.From January to June 2016, the number of discharges from medical and health institutions across China reached 108.785 million, a year-on-year increase of 7.8%, with the growth rate rising by 4.1 percentage points. Among these, hospitals accounted for 83.793 million discharges, a year-on-year increase of 8.6%, with the growth rate rising by 2.7 percentage points; primary care medical and health institutions saw a year-on-year increase of 4.5%. The growth rate in hospitalizations exceeded that of outpatient visits, which is partly related to current efforts to control the proportion of pharmaceutical costs. Since the drug cost ratio for inpatients is lower than that for outpatients, hospitals are incentivized to increase the proportion of inpatient admissions.

Source: National Health and Family Planning Commission, Minsheng Securities Research Institute

Figure 5: Changes in the Growth Rates of Hospital Visits and Discharges, 2011–H1 2016

Source: National Health and Family Planning Commission, Minsheng Securities Research Institute

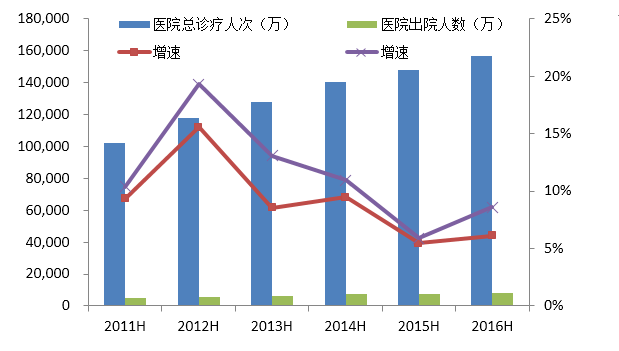

3. Rapid growth in private medical services.From January to June 2016, private hospitals recorded a total of 190 million patient visits, representing an 18.5% year-on-year increase. The number of discharges from private hospitals reached 12.296 million, a 25.0% year-on-year increase. Private hospitals have maintained a rapid growth rate in diagnostic and treatment services, significantly outpacing the growth of public hospitals, which reflects the positive development trend of the current private medical service sector. Currently, private medical providers account for approximately 5% of total patient visits and 11% of hospital discharges. Although these proportions remain relatively low, with the substantial influx of social capital, private hospitals will continue to strengthen their service capabilities and brand influence, leading to a steady rise in their share of service volume. We are strongly bullish on the development of private medical services.

Figure 6: Changes in the Growth Rate of Hospital Visits and Discharges, 2011–H1 2016

Source: National Health and Family Planning Commission, Minsheng Securities Research Institute

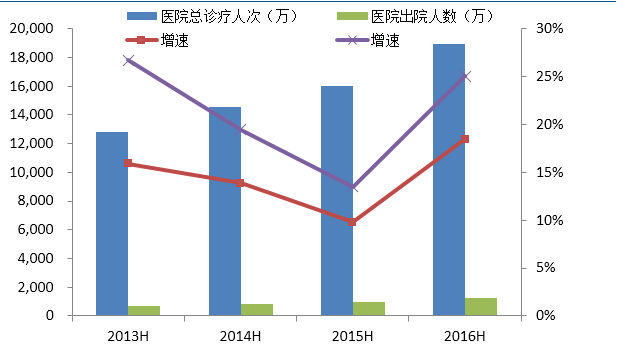

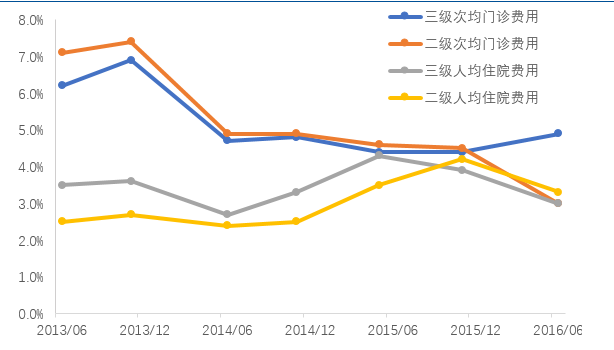

4. Steady growth in average medical expenditure per visit.From January to June 2016, the average outpatient visit cost at tertiary public hospitals across China was RMB 289.6, a year-on-year increase of 4.9%; the average outpatient visit cost at secondary public hospitals was RMB 188.2, a year-on-year increase of 3.0%. The average inpatient cost per capita at tertiary public hospitals was RMB 12,901.2, up 4.9% year on year; the average inpatient cost per capita at secondary public hospitals was RMB 5,535.8, also up 4.9% year on year. Average medical costs have maintained steady growth. Outpatient visit costs, heavily influenced by cost-containment measures due to the high proportion of pharmaceutical expenditures, have shown a downward trend in recent years. Currently, costs at tertiary hospitals have basically stabilized, whereas secondary hospitals continue to face significant pressure owing to their higher pharmaceutical expenditure ratios. Average inpatient costs have remained largely stable and have been minimally affected by cost-containment policies.

Figure 7: Changes in Outpatient and Inpatient Costs at Secondary and Tertiary Hospitals, 2013–2016

Source: National Health and Family Planning Commission, Minsheng Securities Research Institute