Deepening Healthcare Reform and New Investment Opportunities from Tiered Diagnosis and Treatment: Minsheng Securities Biomedical Industry 2017 Annual Strategy Report (Part II)

This article is part of the 2017 annual strategy report series on the biopharmaceutical industry by Minsheng Securities, and VCBeat has been authorized to republish it.

Highlights of This Issue

Medical resources are concentrated in secondary and tertiary hospitals, while the imbalance in primary care resources has increasingly exacerbated the problems of "difficult and expensive access to medical care." In recent years, the National Health and Family Planning Commission has improved the framework for a new pattern of tiered diagnosis and treatment, creating investment opportunities in sectors such as private healthcare funded by social capital, third-party testing, POCT (point-of-care testing) in vitro diagnostics, healthcare informatization, and rehabilitation.

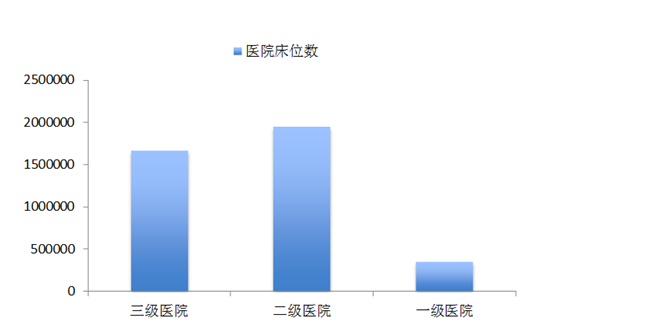

Figure 1: The number of beds in secondary and tertiary hospitals far exceeds that in primary hospitals

Source: China Health Statistics Yearbook 2013, Minsheng Securities Research Institute

In China, due to the shortage of physicians and outdated medical equipment in primary healthcare institutions, most patients bypass community hospitals and clinics after falling ill, seeking care directly at secondary and tertiary hospitals. This has led to severe overcrowding in large hospitals, extreme difficulty in securing appointments, and average consultation times of only a few minutes. Over time, this trend has left primary hospitals nearly deserted, while doctors, patients, and equipment resources increasingly concentrate in tertiary hospitals, creating a vicious cycle.

1. The number of hospital beds in primary hospitals is less than one-quarter of that in secondary and tertiary hospitals

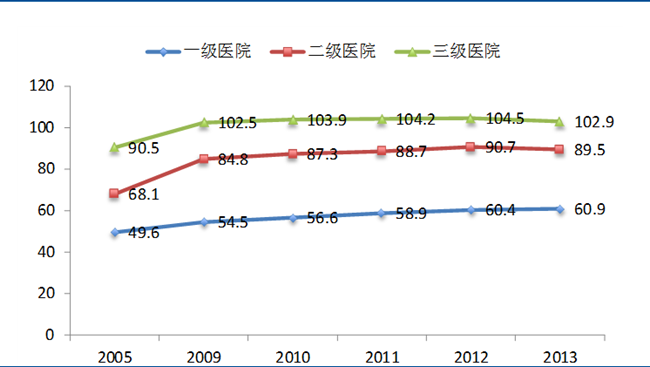

Currently, bed occupancy rates in tertiary hospitals have reached saturation, exceeding 102% annually since 2009, whereas the bed occupancy rate in primary hospitals stands at only around 60%.

Figure 2: Relatively low bed occupancy rate in primary hospitals

Source: China Health Statistics Yearbook 2013, Minsheng Securities Research Institute

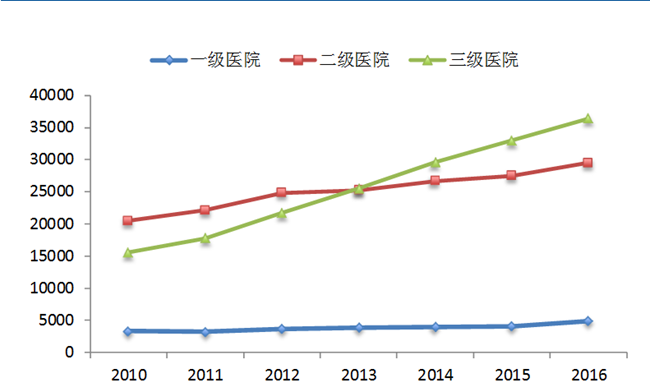

2. The annual number of outpatient visits at tertiary hospitals is six times that of primary hospitals.

Figure 3: Rapid Growth in Patient Visits at Tertiary Hospitals

Source: China Health Statistics Yearbook 2013, Minsheng Securities Research Institute

The number of patient visits at large hospitals has increased year by year. The growth rate of patient visits at tertiary hospitals has been rapid, surpassing that of secondary hospitals in the first quarter of 2013 and reaching 260 million visits. In contrast, the number of patient visits at primary hospitals is significantly lower than that at secondary and tertiary hospitals, never exceeding 50 million visits in any given year.

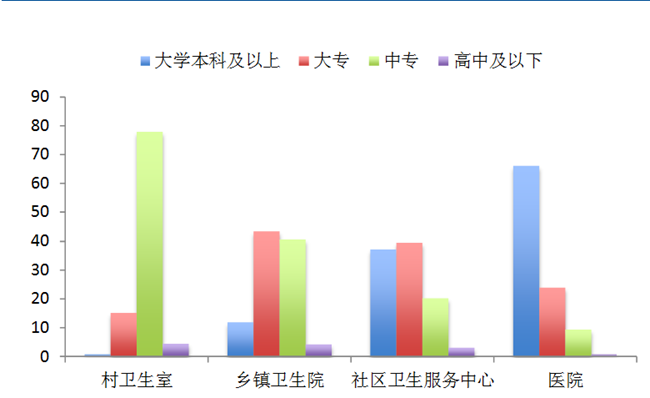

3. Physicians at primary healthcare institutions generally have relatively low educational attainment

The healthcare services industry is characterized by high entry barriers and advanced technical requirements. However, primary care hospitals still lag significantly behind large tertiary hospitals in terms of compensation, established staffing quotas (bianzhi), service environment, and career development opportunities, making it difficult for them to attract highly educated and high-caliber talent.

Figure 4: Physicians at primary healthcare institutions generally have relatively low educational qualifications.

Source: China Health Statistics Yearbook 2013, Minsheng Securities Research Institute

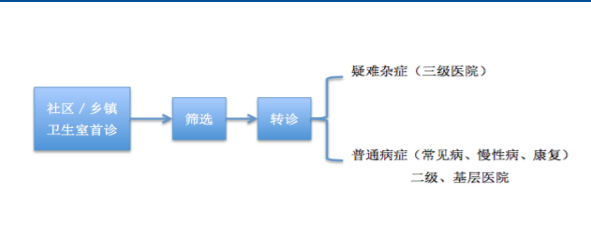

Uneven distribution of medical resources is a major cause of “difficulty in accessing medical care.” The inability to implement “triage between acute and chronic conditions” has led to patient overcrowding in large hospitals, preventing those with genuine needs from receiving appropriate treatment and resulting in diminishing marginal returns on medical resources. Additionally, the imperfection of cross-regional reimbursement platforms and low reimbursement rates are another key factor contributing to the “high cost of medical care.” Therefore, the effective solution to address both “difficulty in accessing medical care” and “high cost of medical care” is to implement a tiered diagnosis and treatment system.

Figure 5: Schematic Diagram of Tiered Diagnosis and Treatment

Source: Compiled by Minsheng Securities Research Institute

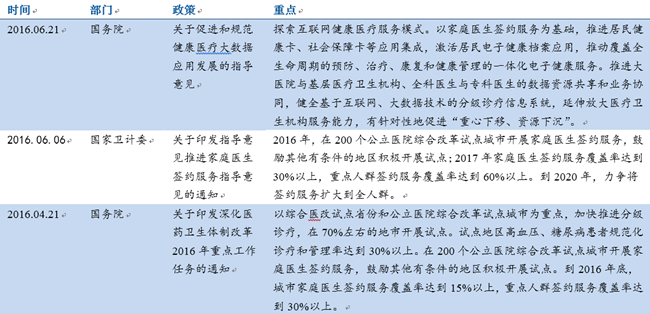

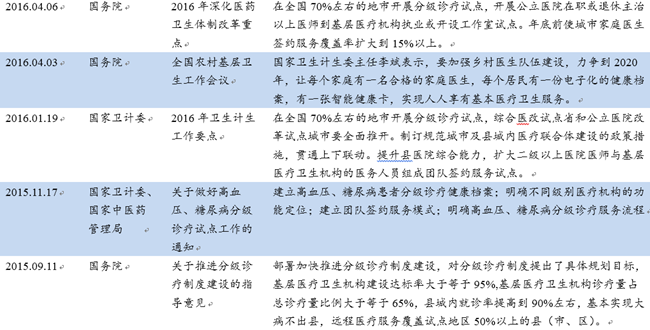

Figure 6: A Review of the Tiered Diagnosis and Treatment Policy

Source: Website of the National Health and Family Planning Commission, Minsheng Securities Research Institute

Figure 7: Establish and improve the guarantee mechanism for tiered diagnosis and treatment

Source: Chinese Government Website, Minsheng Securities Research Institute

1. Promote the family (general practitioner) doctor contract service

In June 2016, the State Council issued the “Guiding Opinions on Advancing Family Doctor Contract Services,” proposing the implementation of family doctor contract services in 200 pilot cities for comprehensive public hospital reform. By 2017, the family doctor contract coverage rate was to reach over 30%, with coverage of key populations exceeding 60%. By 2020, efforts were to be made to extend coverage to the entire population. Through contracting with family doctors, patients would receive initial consultations from them, and patient triage would be conducted based on their professional services. This approach aims to alleviate irrational healthcare-seeking behavior and overcrowding at large hospitals, thereby shifting the focus of medical and health services downward.

Figure 8: The number of general practitioners increased in 2013

Source: China Health Statistical Yearbook, Minsheng Securities Research Institute

2. Strengthen the development of healthcare talent at the primary level and enhance primary healthcare service capacity

The State Council has proposed enhancing the service capacity of primary healthcare institutions through government provision or purchase of services. Specific measures include: reasonably determining the varieties and quantities of medicines equipped and used by primary healthcare institutions; strengthening the medical service capabilities of township health centers in areas such as emergency care, routine surgeries below Level II hospitals, normal deliveries, screening for high-risk pregnant and postpartum women, and pediatrics; integrating existing resources from hospitals at Level II and above, such as inspection and testing facilities and sterile supply centers, and making them accessible to primary-level institutions; and exploring the establishment of independent regional medical laboratory testing institutions, pathological diagnosis centers, medical imaging examination centers, sterile supply centers, and blood purification centers to achieve regional resource sharing.

Figure 9: The tiered diagnosis and treatment system focuses on strengthening primary healthcare infrastructure

Source: The Chinese Government Website, Minsheng Securities Research Institute

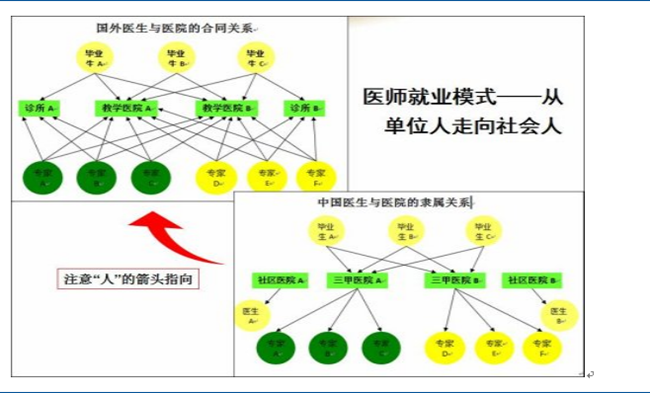

3. Encouraging the new employment mechanism of “multi-site practice,” with “physician groups” continuing to expand

Public hospitals boast robust, high-caliber medical teams and experienced specialists, which is one of the reasons why large hospitals are often overcrowded. Encouraging physicians to practice at multiple sites, including consultations at primary care institutions and private hospitals, can help divert a portion of patients and alleviate the pressure on public hospitals. Moreover, this approach has positive implications for enhancing the technical proficiency of primary healthcare and supporting the development of private medical institutions.

Figure 10: Comparison of Medical Practice Models Between China and Other Countries

Source: Medlive News, Minsheng Securities Research Institute

In the “Guiding Opinions,” the State Council proposed encouraging physicians from urban hospitals at the secondary level and above to engage in multi-site practice at primary healthcare institutions, or to provide regular outpatient and mobile clinic services, through measures such as forming medical consortia, establishing paired assistance programs, and implementing multi-site physician practice policies, thereby enhancing service capacity at the grassroots level.

Physician groups are a practice model originating from developed countries, referring to alliances or organizations formed by multiple physicians who practice collectively and share profits and losses. The team effect can help build a certain level of renown and establish specialized research teams, thereby improving the efficiency of medical services. In the traditional healthcare environment, the value of physicians’ clinical expertise has been underestimated, leading to increasingly strained doctor-patient relationships. Within physician groups, doctors are not “institutional employees” tied to hospitals but rather “independent practitioners,” with their personal value linked to patient welfare. This arrangement enhances physicians’ motivation to provide high-quality care and can, to some extent, alleviate doctor-patient conflicts. As policies become more liberalized and public demand for medical services grows increasingly diverse, the development prospects for physician groups will continue to improve.

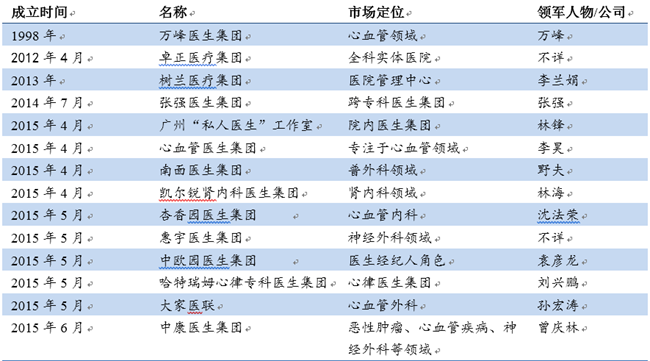

Figure 11: Existing Physician Groups in China

Source: Iyiou.com, Minsheng Securities Research Institute

4. Internet-based third-party platforms supplement communication between doctors and patients

Accelerate the development of national health information infrastructure, establish regional medical and health information platforms, achieve continuous recording of electronic health records (EHRs) and electronic medical records (EMRs), and facilitate information sharing among medical institutions of different levels and types. Enhance telemedicine capabilities, leverage information technology to promote the vertical flow of medical resources, improve the accessibility of high-quality medical resources and the overall efficiency of healthcare services, and encourage secondary and tertiary hospitals to provide remote consultation, remote pathological diagnosis, remote imaging diagnosis, remote electrocardiogram (ECG) diagnosis, remote training, and other services to primary healthcare institutions. Promote the sharing of patient information across regions and institutions. Develop internet-based medical and health services, and fully leverage information technologies such as the internet and big data in supporting tiered diagnosis and treatment.

(III) Investment Opportunities Brought by the Implementation of Tiered Diagnosis and Treatment

1. Private Healthcare: Enhancing Service Quality at Primary Hospitals

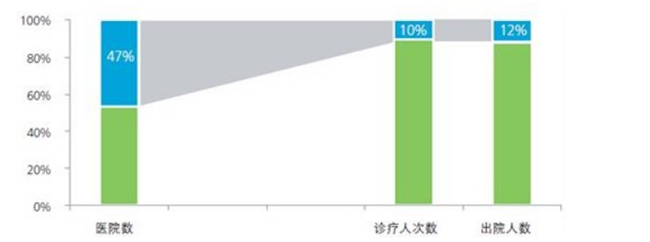

Figure 12: Comparable Numbers of Public and Private Institutions, Significant Disparity in Patient Visits

Source: China Investment Consulting Network, Minsheng Securities Research Institute

Currently, the number of public hospitals is comparable to that of private hospitals; however, the number of patient visits in public hospitals far exceeds those in private hospitals. Under the tiered diagnosis and treatment system, patients are being diverted to primary care institutions, leading to continuous expansion of the primary care market. The contradiction between the growing demand and insufficient supply in the primary care sector has become increasingly prominent. The State Council has proposed further relaxing market access restrictions, controlling the scale of public hospitals, leaving room for privately funded medical services, promoting the flow and sharing of resources, and encouraging physicians from public hospitals to practice in private hospitals. These measures aim to guide social capital to participate in improving primary healthcare services and enhance the operational standards of primary healthcare institutions.

2. Third-Party Testing and Diagnosis: Supplementing the Diagnostic and Treatment Capabilities of Primary Care Hospitals

Initial diagnosis at the primary care level serves as the starting point. It is essential to first enhance the medical service capabilities of primary healthcare institutions, which requires basic testing and imaging facilities to support family physicians in their clinical practice. The return of patients to communities for rehabilitation demands a high-quality community service environment and highly skilled medical personnel, both of which necessitate government support for primary healthcare delivery. Due to the limited service capacity of primary medical institutions, third-party diagnostic services can assist primary care physicians in making diagnoses, thereby improving service capabilities. Furthermore, competition introduced by third-party social capital can help ensure cost-effective services, reduce the cost of medical care, and optimize cost-benefit ratios.

Third-party services are currently in their nascent stage. With the implementation of tiered diagnosis and treatment, the primary care market is increasingly being unlocked, leading to growing demand for high-quality and efficient laboratory testing. Consequently, the development prospects for third-party medical services are becoming increasingly promising. For instance, in the field of third-party laboratory testing, the market size of independent clinical laboratories was approximately RMB 1.3 billion in 2010 and reached RMB 4.76 billion in 2014, representing a compound annual growth rate (CAGR) of 54%.

3. POCT (Point-of-Care Testing): Broad Application Fields and Promising Prospects

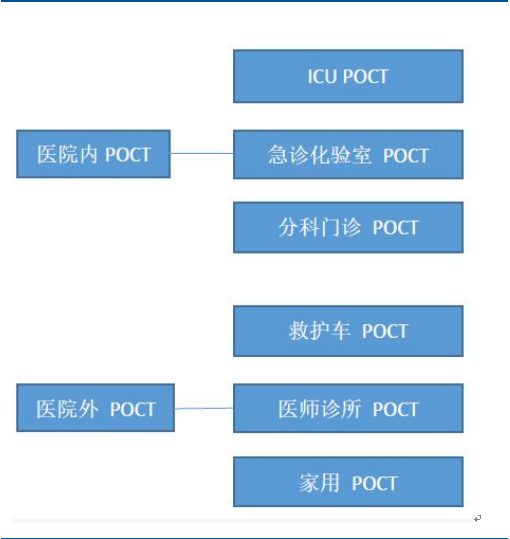

Point-of-Care Testing (POCT) refers to a rapid diagnostic analysis technology performed near the patient’s bedside, enabling testing at the bedside, in hospital wards, or in locations outside the central laboratory. Applications include ambulances, rehabilitation centers, blood banks, home care settings, communities, and rural clinics. Under the tiered diagnosis and treatment system, POCT in vitro diagnostics also boasts broad prospects.

Figure 13: POCT Classification

Source: China Industry Information Network, Minsheng Securities Research Institute

From the perspective of general hospitals, there are currently few POCT products available. However, with the advancement of tiered diagnosis and treatment, patients are increasingly flowing to primary and secondary care institutions. This has led to a reduction in the variety of tests and specimens at large hospitals. Consequently, large-scale automated laboratory testing platforms in these hospitals will gradually be replaced by POCT and regional clinical laboratory centers. POCT can be applied in various settings, including clinical laboratories, ICUs, operating rooms, and emergency departments.

From the perspective of general clinics, as tiered diagnosis and treatment is promoted, the number of patients referred down from tertiary hospitals has increased, leading to a corresponding rise in demand for point-of-care testing (POCT).

From the perspective of community households, the volume of point-of-care testing (POCT) for common and chronic diseases will increase, as chronic disease management and disease prevention will generate certain demand for POCT.

4. Healthcare Informatics: Reducing Costs and Enhancing Efficiency

Internet-based referrals facilitate connectivity among medical institutions of varying levels and categories. For instance, secondary and tertiary hospitals can conduct remote consultations and remote imaging interpretations for patients via internet healthcare services, thereby reducing patients’ time and transportation costs and improving the orderliness of medical care.

Figure 14: Internet + Healthcare

Source: Xinhua News Agency Finance, Minsheng Securities Research Institute

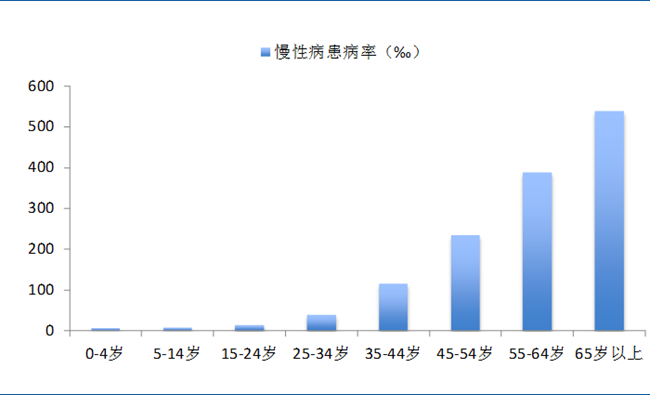

5. Rehabilitation Medicine: Significant Gap, High Demand

In China, individuals aged 60 and above account for more than 10% of the total population. Additionally, there are 85 million people with disabilities and 270 million patients with chronic diseases. Currently, there is a significant shortfall in rehabilitation services in China, making it difficult to meet the growing demand for rehabilitation. In 2012, there were only 322 rehabilitation hospitals in the country. The tiered diagnosis and treatment system requires community and primary healthcare institutions to accept chronic rehabilitation patients referred from tertiary hospitals, which will generate substantial demand for rehabilitation hospitals.

Figure 15: High prevalence of chronic diseases among the elderly

Source: China Health Statistics Yearbook 2013, Minsheng Securities Research Institute