Minsheng Securities 2017 Annual Strategy Report (III): The Development Path of China's Retail Pharmacy Sector – M&A Integration and Service Expansion

This article is Minsheng Securities’ 2017 annual strategy report on the pharmaceutical and biotechnology sector. VCBeat has been authorized to republish it and will subsequently release a series of categorized reports. Stay tuned for further updates.

Highlights of This Issue

China’s retail pharmacy sector has achieved a compound annual growth rate (CAGR) of 16%, yet the industry remains relatively fragmented. In 2015, the chain pharmacy penetration rate in China stood at 45.7%, with product sales dominated by over-the-counter (OTC) medications and health supplements, while prescription drugs accounted for a relatively small share. Going forward, the industry will build on scale expansion, deepen product line development, and provide integrated services through complementary online and offline channels.

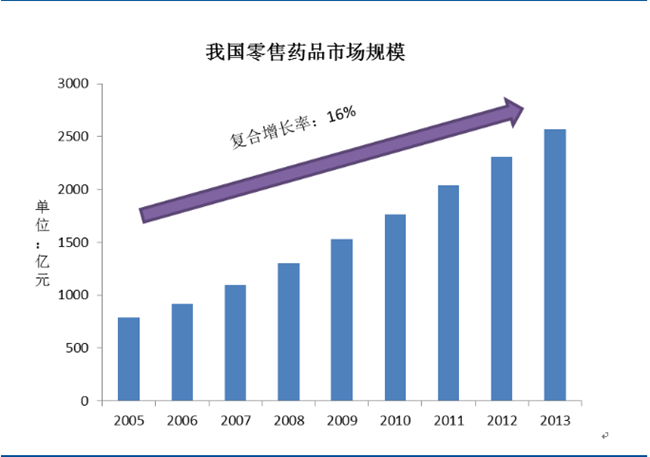

Compared with the current growth rate of less than 5% for retail pharmacies in the United States, the scale of China's retail pharmacy sector grew from RMB 79 billion in 2005 to RMB 257.1 billion in 2013, representing a compound annual growth rate (CAGR) of 16%.

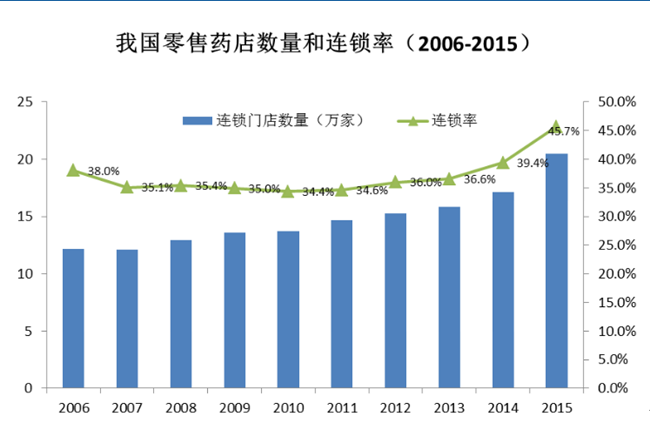

However, China’s pharmacy chain industry remains relatively fragmented, with a low chain penetration rate. By the end of 2013, the total number of retail pharmacies in China reached 432,700, and the industry as a whole was still characterized by numerous, small-scale, scattered, and disordered operations. In 2015, the chain penetration rate for domestic pharmacies stood at 45.7%, representing a 6-percentage-point increase from 2014; nevertheless, this rate remained comparatively low relative to that of developed countries.

Figure 1: The Market Size of China's Retail Pharmaceutical Industry

Source: China Pharmaceutical Retail Development Research Center, Minsheng Securities Research Institute

Figure 2: Number of Retail Pharmacies and Chain Rate in China (2006-2015)

Source: Southern Pharmaceutical Institute, Minsheng Securities Research Institute

(II) Sales Categories Focused on OTCdominated by [non-prescription drugs], with prescription drugs accounting for a relatively low proportion

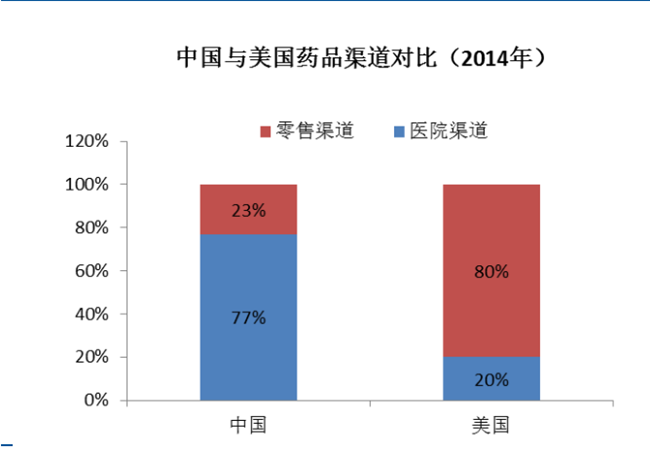

As China has not yet separated prescribing from dispensing, the majority of pharmaceuticals are still sold through hospital channels. In 2015, the domestic terminal market size for pharmaceuticals reached RMB 1,262.8 billion, while the retail pharmaceutical market amounted to only RMB 311.5 billion, accounting for 23% of the total.

Figure 3: Comparison of Pharmaceutical Distribution Channels in China and the United States (2014)

Source: Southern Institute, Minsheng Securities Research Institute

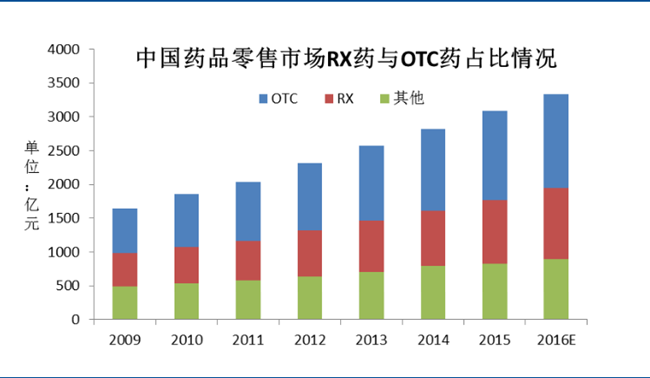

Meanwhile, the product mix in retail pharmacies is still dominated by over-the-counter (OTC) drugs, medical health products, and dietary supplements, with prescription drugs accounting for a relatively small share. In 2015, sales of prescription drugs in retail pharmacies reached RMB 93.9 billion, representing approximately 30% of total sales—a figure that remains significantly lower than CVS’s prescription drug sales proportion of over 70%.

Figure 4: Market Share of Prescription (RX) and Over-the-Counter (OTC) Drugs in China's Pharmaceutical Retail Sector

Source: Research Report on China's Pharmaceutical Retail Industry, Minsheng Securities Research Institute

Currently, retail pharmacies in China have begun experimenting with DTP/DTC services for prescription drugs, similar to specialty pharmacy services in the United States, but the scale remains relatively small. For further details, please refer to our previous industry report, “Insights into the Development of China’s Pharmacies from the Perspective of Diplomat Pharmacy, the Largest Independent Specialty Pharmacy in the United States》. Other value-added services offered by pharmacies include on-site Traditional Chinese Medicine (TCM) consultations and TCM diagnosis and treatment; however, due to the scarcity of TCM practitioners, large-scale promotion and replication remain challenging. As for the Pharmacy Benefit Management (PBM) business, which has reached maturity in the United States, it is still in an exploratory stage in China.

We believe that the current development stage of retail pharmacies in China is similar to that of the United States in the 1980s and 1990s, still in a phase of rapid expansion and market consolidation, leveraging capital for mergers and acquisitions. At the product level, although prescription drugs cannot be sold in large volumes through retail pharmacies in the short term, retail pharmacies can learn from CVS’s approach by focusing on optimizing existing product offerings, enhancing gross profit margins through building their own brands or partnering with specific suppliers. Meanwhile, by integrating online pharmacy platforms with offline stores, they can create a complementary omnichannel ecosystem, providing patients with integrated services.