An In-Depth Overview of China's Pharmaceutical E-Commerce Landscape: Industry Map and Key Players

Positive developments in the pharmaceutical e-commerce sector continue to emerge, as policy support and favorable guidance for the industry are steadily intensifying.

The origins of pharmaceutical e-commerce can be traced back to the 2005 Interim Provisions on the Approval of Internet Drug Transaction Services. At that time, internet drug transactions referred to the exchange of information and facilitation of transactions via online platforms among pharmaceutical manufacturers, distributors, retailers, and hospitals, as well as the provision of online purchasing channels for individual consumers. Today, the concept of pharmaceutical e-commerce has gradually expanded, giving rise to a series of new drug-centric services, including pharmaceutical marketing, pharmaceutical O2O (online-to-offline), herbal medicine trading, and pharmaceutical care services.

VCBeat (WeChat ID: vcbeat) has compiled a list of active players in the pharmaceutical e-commerce industry, created an industry landscape map, and conducted sample analyses on several representative pharmaceutical e-commerce companies to help you gain a comprehensive understanding of the sector in a single article.

Overview: Market Size Approaches RMB 100 Billion

Let’s begin with an overview of the Internet Drug Transaction Service Qualification Certificate. This certificate is issued by the China Food and Drug Administration (CFDA) to enterprises engaged in online drug transaction services and is categorized into three types: A, B, and C. - **Type A Certificate**: Approved by the national CFDA. Holders operate as third-party drug transaction service platforms, providing information services to pharmaceutical manufacturers, distributors, and medical institutions. They are prohibited from selling drugs directly to individual consumers. - **Type B Certificate**: Approved by local food and drug regulatory authorities. Holders are typically pharmaceutical manufacturers and distribution companies, facilitating online drug transactions with other drug trading enterprises outside their own organizations. - **Type C Certificate**: Also approved by local authorities. Applicants are chain pharmacies, operating as online pharmacies that sell drugs directly to individual consumers.

As of January 2017, there were 41 enterprises holding License A, 195 holding License B, and 598 holding License C. On January 21, the State Council issued an administrative decision to abolish the review requirements for Licenses B and C in pharmaceutical e-commerce, thereby lowering market entry barriers for the sector.

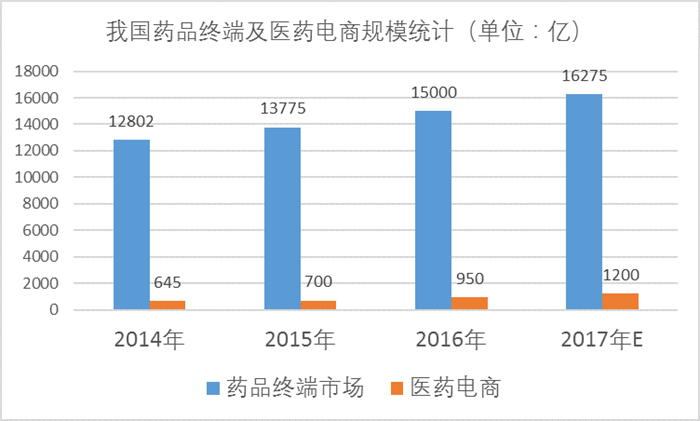

In terms of scale, the share of pharmaceutical e-commerce in the terminal drug market is not high, but its growth rate is very high.

According to data from Zhongkang CMH, pharmaceutical e-commerce has maintained growth for six consecutive years, with the scale of online pharmacies (B2C) alone surpassing RMB 10 billion. In 2015, the overall market size of online pharmacies reached RMB 11 billion, representing a 52.8% increase from 2014. The total category size of online pharmacies is projected to reach RMB 16 billion in 2016, a year-on-year growth of 45.5%.

In the B2B sector, influenced by policies such as "separation of prescribing and dispensing" and the "two-invoice system," pharmaceutical manufacturers and distributors have been actively developing their own e-commerce platforms. However, the pharmaceutical B2B market is still in its early stages, primarily serving chain pharmacies, independent pharmacies, and clinics, and has not yet penetrated the hospital tendering and procurement system. As the "two-invoice system" is further implemented, socialized drug procurement may create growth opportunities for pharmaceutical B2B.

Based on data from Qianzhan Industry Research Institute and related consulting firms, we have compiled the overall market size data for pharmaceutical e-commerce (B2B and B2C), projecting that the total market size will exceed RMB 100 billion after 2017.

Source: VCBeat Research

Industry Scan: Distribution and Retail Are the Main Drivers

Source: VCBeat Editorial Team

We conducted a scan of 40 active enterprises in the pharmaceutical e-commerce industry, categorizing the sector into B2C, B2B (platform), O2O, medicinal materials, and marketing platforms.

As can also be seen from the industry landscape, the pharmaceutical e-commerce sector is currently dominated by online pharmacies. Its business model and profit drivers are relatively clear and have gained recognition from both the market and investors.

Overall, among the current entrants in the pharmaceutical e-commerce sector, capital from pharmaceutical distribution and retail chain enterprises represents a significant force. Companies such as Jointown Pharmaceutical Group, Laobaixing Pharmacy, Kangze Pharmaceutical, Renhe Pharmaceutical, and Shanghai Pharmaceuticals have established extensive layouts in online pharmacies, pharmaceutical wholesale, and medicinal materials, serving as natural extensions of their offline operations. Other players, including 111.com, Jianke, AliHealth, JD Health, and 360 Health, enjoy high brand recognition among consumer-end (C-end) users. As an emerging concept, medicine delivery O2O (Online-to-Offline) has seen limited participation; particularly following the liquidity crisis experienced by “Yao Geili” last year, industry stakeholders have engaged in deeper reflection on this business model. Currently, KuaiFang SongYao and Dingdang Kuaiyao are the most prominent players in this segment, both having announced that they have achieved basic profitability.

In addition, we have observed several pharmaceutical e-commerce companies with relatively novel business models. These companies integrate drug sales with health management, medical insurance cost control, and smart hardware. However, given their currently limited service population and unclear business models, they are not listed separately.

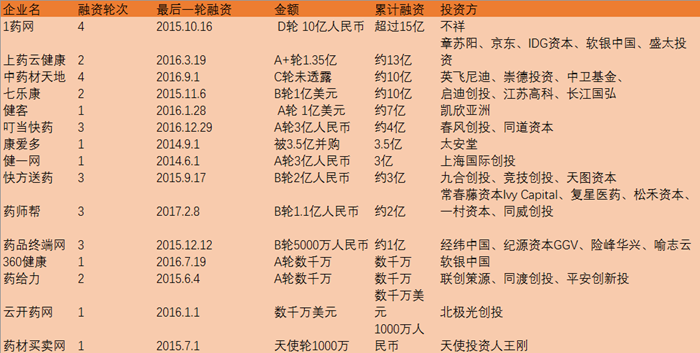

Funding: Over RMB 1.5 Billion

Among companies that have disclosed financing information, 111.com (Yi Yao Wang) currently leads in fundraising, having accumulated over RMB 1.5 billion in financing. A total of four companies have raised more than RMB 1 billion cumulatively: Shanghai Pharmaceuticals Cloud Health, TCMC (Zhong Yao Cai Tian Di), and 7LeKang. On February 15, 2017, 7LeKang announced a new round of financing with participation from multiple investors including Sequoia Capital and JD.com; however, as the specific amount was not disclosed, its ranking remains unchanged.

An overview of all financing information reveals two prominent characteristics. First, financing rounds are concentrated at Series A and beyond; among the 15 startup financing events included in our statistics, 13 occurred at Series A or later stages. This indicates that the pharmaceutical e-commerce sector has entered a mature phase, with the market having consolidated and few new entrants remaining. Second, individual funding amounts are substantial, with nine financing events reaching or exceeding RMB 100 million.

Insights from recent financing events reveal that a key development trend in pharmaceutical e-commerce is diversification and multifunctionality. The era of standalone online pharmacies has reached maturity; future growth hinges on expanding service extensibility, with integration across the entire pharmaceutical industry chain emerging as the strategic direction. This involves combining online and offline operations, integrating marketing with e-commerce strategies, blending professional expertise with guided shopping services, merging pharmaceutical e-commerce with medical hardware, and linking chronic disease management with discounted medications. The depth to which pharmaceutical e-commerce can penetrate mirrors the depth of the physical pharmaceutical industry’s supply chain. Furthermore, since pharmaceutical e-commerce teams are predominantly technology-driven, there is significant potential in integrating e-commerce and internet technologies into traditional pharmaceutical sales. Notable examples include Yaoshibang, where terminal pharmacy drug demand inversely dictates manufacturer distribution, and 360 Hao Yao, which provides supply chain management for chain stores and online pharmacies, along with customer acquisition and fan management for chain pharmacies. The pharmaceutical e-commerce sector has already witnessed diverse business models and product concepts. Due to their deeper digital integration, these entities demonstrate greater acceptance of technology-led industry transformation.

It is foreseeable that few new startups will emerge in the pharmaceutical e-commerce sector, as capital will continue to focus on the aforementioned established players, thereby fostering the emergence of “unicorns” within the industry.

Trend Forecast: Mobile-First, Specialization, O2O

Currently, there are still three major bottlenecks constraining the development of pharmaceutical e-commerce.1. Restrictions on the Online Sale of Prescription Drugs, in the short term, regulators will not lift this restriction due to medication safety concerns.2. Health Insurance Integration, the biggest problem is that China's medical insurance system implements regional pooling management, and national-level pooling is still in the planning stage; therefore, pharmaceutical e-commerce platforms cannot support "cross-regional medication purchases with medical insurance settlement."3. Consumer Awareness, which differs from general consumer goods; the target audience has not yet fully embraced e-commerce as a channel for pharmaceuticals, the market still requires cultivation, and consumer habits need to be gradually fostered.

In contrast, developed countries in Europe and the United States not only have more open policies but also higher consumer awareness. Taking the United States as an example, its pharmaceutical e-commerce sector is highly developed with a relatively mature market, where online pharmacies (B2C) account for approximately 30% of the entire retail market, compared to around 5% in China. About 50% of the product categories sold are prescription drugs, whereas China is still in the early stages of development.

Pharmaceutical e-commerce companies have also made proactive attempts to break through the bottlenecks constraining their development. These efforts include obtaining prescription drug sales rights by integrating internet hospitals and electronic prescriptions; enhancing user stickiness by combining services with health management and chronic disease management; and focusing on models such as specialized pharmacies and exclusive drug supply channels. In the future, pharmaceutical e-commerce may grow into a channel comparable in stature to hospitals and retail outlets.

Recent industry developments and key policy highlights indicate that pharmaceutical e-commerce will trend toward mobileization, specialization, and diversification.

One is that mobile transactions have surpassed those on PCs and other channels.In fact, this is also one of the major characteristics of the entire e-commerce sector. According to Nielsen data, mobile transactions accounted for 69.4% of the total e-commerce industry in 2016. Specifically, in the pharmaceutical e-commerce sector, data from 111.com.cn, a company with strong mobile performance, shows that 80% of its customers come from mobile devices, with monthly active users exceeding 1.5 million.

Data released by Analysys Consulting shows that in the pharmaceutical e-commerce market structure of 2015, the PC segment surpassed the mobile segment in the first two quarters, while the mobile segment overtook the PC segment in the last two quarters. On a more granular level, the market share of platform-based mobile channels exceeded that of self-operated mobile channels; in the first three quarters of this year, the market share of platform-based mobile channels remained above 75%, significantly leading self-operated mobile channels.

Second, the level of specialization has been strengthened.Pharmaceutical consumption is characterized by low frequency. While integrating it into a platform app is relatively lightweight, embedding health management and light consultation services into e-commerce platforms could potentially increase the open rate of e-commerce apps. Online pharmacies such as 111.com.cn (Yi Yao Wang), Jianke.com, and Kangaiduo have all launched “medicine + medical care” models. For instance, 111.com.cn’s Yizhen App starts with online consultations and leads to pharmaceutical product recommendations, demonstrating significant traffic conversion effects. Additionally, companies like Yun Kai Ya Mei focus on cultivating their own pharmacists and operating self-owned stores; their professional service teams provide users with advice on drug selection, medication usage, and health management, thereby enhancing service penetration. Across the industry, beyond the aforementioned companies, many other pharmaceutical e-commerce players have indicated they will strengthen their pharmacist and health consultation teams to ensure consistency between online purchasing experiences and offline service quality.

As previously mentioned, pharmaceutical e-commerce has expanded into medical services such as lightweight online consultations and internet hospitals. This trend is expected to deepen in the future, further stimulating more business activities centered around “pharmaceuticals.” Among the companies we have reviewed, some specialize in “flash sales” of drugs, while others provide dedicated services and products for patients with chronic and special diseases. Based on their financing performance, the primary reason these companies have attracted investor interest is their differentiated positioning. Due to the absence of geographical and temporal constraints, pharmaceutical e-commerce platforms can more easily aggregate users with similar medication needs, thereby sustaining their business operations while meeting patient demands.

Third, O2O will receive greater attention.This can be corroborated by the “Several Opinions on Further Improving Drug Production, Circulation, and Use” (hereinafter referred to as the “Opinions”) issued by the State Council on February 9. The “Opinions” point out that it is necessary to guide the standardized development of “Internet + Drug Circulation,” support drug circulation enterprises in strengthening cooperation with internet companies, promote the integrated development of online and offline channels, and cultivate emerging business formats. It also calls for regulating internet retail services provided by retail pharmacies and promoting new delivery models such as “online ordering with in-store pickup” and “online ordering with home delivery.” This has undoubtedly given a strong boost to pharmaceutical O2O, with several pharmaceutical O2O companies telling reporters at the time that the sector might be ushering in its spring.

In fact, many companies had already been deeply engaged in this sector. For instance, Alibaba Health, in collaboration with multiple pharmacies, established the “China Pharmaceutical O2O Pioneer Alliance.” Leveraging mobile internet and data technologies, it integrated the upstream and downstream segments of the healthcare and pharmaceutical services industry. This was directly manifested by users being able to place orders via the Alibaba Health app, with nearby pharmacies delivering the medications, thereby creating an online-to-offline synergy. The sector has also attracted numerous O2O medication delivery companies, including Kuai Fang Song Yao, Ding Dang Kuai Yao, and Song Yao 360. However, their business models differ slightly: Alibaba Health provides order traffic redirection to offline pharmacies, whereas Kuai Fang operates its own self-built pharmacies. The former aims to integrate the entire pharmaceutical industry, while the latter seeks to control the medication purchasing and delivery processes to enhance service quality and customer satisfaction.

In summary, while policy progress may be sluggish, enterprises are already making proactive attempts, driving regulatory advancements through market mechanisms. As a result, the pharmaceutical e-commerce sector is poised to maintain steady and rapid growth.