Comprehensive Analysis of 108 Listed-Company-Sponsored Healthcare Industry Funds with Total Committed Capital of RMB 168.2 Billion

In recent years, within the investment landscape of the big health industry, listed companies have increasingly adopted industrial funds as a vehicle to invest in high-quality projects. This approach enables listed companies to mitigate the impact on the secondary market that direct acquisitions and mergers might cause. The introduction of new technologies and new business lines has proven significant in promoting business expansion and strategic transformation for these companies. Furthermore, collaborative models and leveraged buyouts have alleviated financial pressures on listed companies. Coupled with the influx of private equity (PE) firms and professional asset management institutions, the establishment of industrial funds by listed companies has witnessed an explosive growth trend.

VCBeat (WeChat ID: vcbeat) has compiled data on 108 large-health industry funds initiated by listed companies since 2015, with an estimated total scale of RMB 168.2 billion, aiming to examine the development trajectory of the pharmaceutical industry from the perspectives of industrial investment and mergers and acquisitions.

Section 1: Data Interpretation

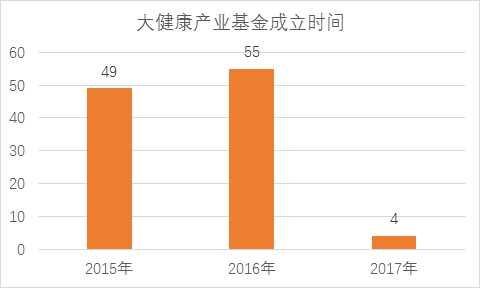

Date of Establishment of the Industrial Fund

In 2015, a total of 49 health industry funds were announced to be established. In 2016, this number further expanded to 55. This year, just two months in, four new health industry funds have already been announced.

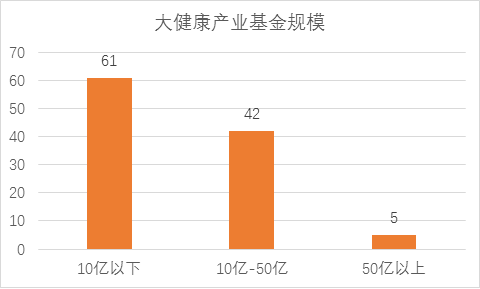

Fund Size

Among the 108 industrial funds included in the statistics, 61 have sizes below RMB 1 billion. Of these, 13 funds have an expected size of RMB 300 million, and 21 funds have a size of RMB 1 billion, accounting for approximately half of the total in this bracket. There are 42 big health industry funds in the RMB 1–5 billion range, while only five funds exceed RMB 5 billion. These include biomedical M&A funds initiated by Nanjing Xinbai, Sanpower Group, Nanjing Yingpeng Asset Management, and Bank of Nanjing; investment funds established by Galaxy Group in areas such as immunotherapy, clinical application platforms for stem cells, and the development of macromolecular drugs and antibody drugs; and the Global M&A Fund for the Big Health Industry, with an expected size of RMB 20 billion, jointly initiated by China CITIC Bank and Sanpower Group on January 20 this year.

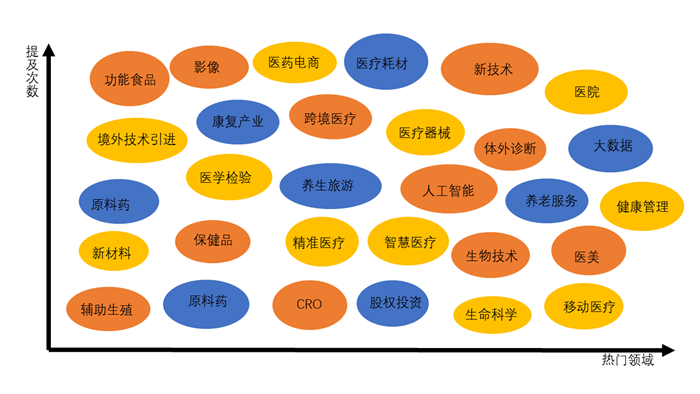

Field

The sectors targeted by industrial funds span from foundational layers, such as new materials and emerging technologies, to end-user services. Based on mention frequency and trending areas, we have created a corresponding coordinate map. The map reveals that hospitals, medical devices, medical consumables, pharmaceutical e-commerce, in vitro diagnostics (IVD), and elderly care services are the focal points of discussion and hot investment areas. Although mobile health, life sciences, and biotechnology are also highly discussed, few companies have actually entered these fields. This is because the optimal investment window for mobile health has passed, with the market landscape largely established; furthermore, immature business models have dampened investor enthusiasm. In the realms of life sciences and biotechnology, despite high interest, fewer companies are being pursued due to the long investment cycles required, which often exceed the typical 5–10 year lifespan of most funds.

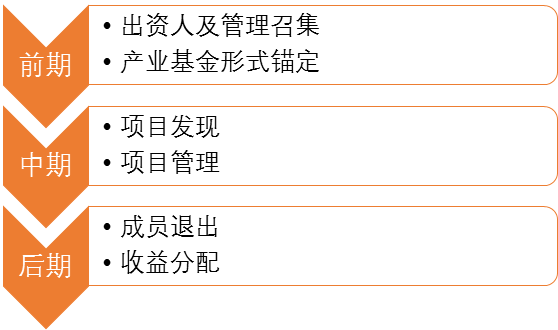

Operational Process of the Big Health Industry Fund

Cooperation Model

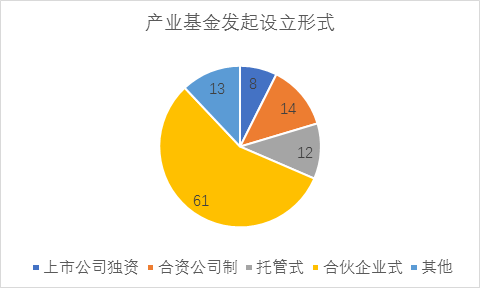

Through an analysis of health and wellness investment funds established and participated in by 108 listed companies, we have identified four models for initiating such funds: wholly owned by a listed company, jointly established by multiple parties, trust-based, and limited partnership. The trust-based and limited partnership models are the most prevalent. These initiation structures exhibit some overlap. Below, we will analyze each model in detail and interpret representative case studies.

Listed Company Sole Proprietorship.This refers to listed companies establishing fund management firms and injecting their own idle funds into the fund pool. Typically, such funds are modest in size, and the projects they invest in are directly related to the core business of the initiating entity.

Joint Venture System.Specifically, professional asset management institutions and listed companies, together with their controlling subsidiaries, jointly contribute capital to establish a joint venture company, which then initiates the fund-raising plan; both the asset management institution and the listed company subscribe for certain quotas.

Managed.Generally, listed companies differ slightly from professional asset management institutions in terms of asset management and investment capabilities. Therefore, some listed companies choose to engage external asset management firms to manage their industrial funds. These asset management institutions earn management fees as compensation, while also having the option to co-invest in certain projects. They may exit these investments at appropriate times, with the listed company providing endorsement, and ultimately receive additional returns in the form of the listed company’s shares, private placements, or other equity instruments.

Partnership Structure.This business model is characterized by the participation of multiple listed companies, asset management firms, banks, and government entities as fund investors. Furthermore, there are structural differences among these investors, including senior, mezzanine, and junior tranches. Typically, listed companies serve as junior partners, assuming higher risks in exchange for potentially higher returns and greater decision-making authority.

There is a large number of partnership-type funds; we have selected the Hubei Zhongzhu Zhongbang Changjiang Medical M&A Investment Fund as our sample case. On December 21 of last year, Zhongzhu Medical issued an announcement stating that it had signed a cooperation agreement with Zhongbang Asset Management and Changjiang Fund to establish an M&A fund. The parties plan to jointly initiate an industrial M&A fund with a total size of RMB 1.8 billion. As a subordinated limited partner, Zhongzhu Medical will contribute RMB 200 million, accounting for 11.10% of the total. In this fund structure, although the listed company, acting as a subordinated partner, does not hold priority rights upon exit, the invested projects align with Zhongzhu Medical’s strategic transformation direction and fit the company’s long-term development path.

By synthesizing the aforementioned cooperation models, the advantages and disadvantages of asset management companies and listed companies jointly initiating and establishing big health industry funds become clearly evident. For asset management companies, leveraging the platform of a listed company facilitates trust endorsement, thereby enabling easier access to capital. For listed companies, asset management companies can provide professional asset management plans and possess mature expertise in project evaluation. Furthermore, the invested projects align with the strategic objectives of the listed company; if mergers and acquisitions or integrations are successfully executed, they can significantly enhance the listed company’s competitiveness.

Section 2: Market Environment and Trend Outlook

The above merely represents the superficial aspects of investments by listed companies and asset management firms in the big health industry. As professional investors, one should possess the ability to look beyond appearances and grasp the essence. The reason why industrial funds are flocking to compete in the big health sector lies in the promising development prospects of the big health and healthcare-related industries, favorable policy incentives, and the need for listed companies with substantial cash reserves to seek viable investment outlets.

In October last year, the State Council issued the “Outline of the ‘Healthy China 2030’ Plan” (hereinafter referred to as the “Plan”), providing systematic guidance and phased objectives for the development of the broader health industry.

The Plan outlines the overall objective that, by 2020, China should establish a basic medical and health system with Chinese characteristics covering both urban and rural residents; continuously improve health literacy; develop a sound and efficient health service system; ensure universal access to basic medical and health services as well as basic physical fitness services; basically form a health industry system with rich connotations and a rational structure; and rank among the leading upper-middle-income countries in terms of major health indicators.

By 2030, the institutional framework for promoting health for all will be further improved; development in the health sector will be more coordinated; healthy lifestyles will become widespread; the quality of health services and the level of health security will continue to rise; the health industry will flourish; health equity will be basically achieved; and major health indicators will reach the levels of high-income countries. By 2050, China will be built into a Healthy Nation commensurate with a modern socialist country.

At the industrial level, the primary objective has been to establish a comprehensive and structurally optimized health industry system, cultivate a cohort of large enterprises with strong innovation capabilities and international competitiveness, and position the sector as a pillar of the national economy. Further bolstering industry confidence, the Plan also outlines targets for market scale: the total size of the health industry is projected to exceed RMB 8 trillion by 2020 and surpass RMB 16 trillion by 2030.

Source: Compiled by VCBeat

Pharmaceutical Market Environment

Within the broader health and wellness industry, pharmaceutical-related sectors demonstrate the greatest growth potential. The pharmaceutical industry is a major category encompassing the research and development of chemical drugs, traditional Chinese medicine, and biological products (including gene and cell therapies), as well as medical devices and healthcare services. It holds a significant position in the socio-economic landscape, directly impacting public health and social development. Consequently, it has been frequently highlighted in key policy and economic planning documents, such as the 13th Five-Year Plan, Healthy China 2030, and the Guidelines for the Development Planning of the Pharmaceutical Industry.

From a market performance perspective, the pharmaceutical industry has demonstrated stable overall development trends and maintained a high growth rate over the long term. Data from the National Bureau of Statistics shows that in 2016, the value-added growth rate of the pharmaceutical manufacturing industry was 10.8%, higher than the 6.7% growth rate of the national economy.

From the perspective of the overall national economy, the pharmaceutical industry is a vital component, spanning the entire life cycle and exhibiting weak cyclicality, thereby being less susceptible to economic fluctuations. In the current market environment, three major drivers are fueling the continued development of the pharmaceutical industry: rising household income levels; continuous improvement in reimbursement systems for both basic medical insurance and commercial health insurance; and demographic structural adjustments, characterized by significant demands from an aging population and newborns. Driven by these factors, the pharmaceutical industry has maintained a high growth rate.

According to data from the Southern Institute of Pharmaceutical Economics under the China Food and Drug Administration (CFDA), the output value of the pharmaceutical industry exceeded RMB 1 trillion in 2010 and rose to RMB 2.5798 trillion in 2014, with a compound annual growth rate of 21.19%.

Data Source: CFDA Southern Economic Research Institute

Pharmaceutical-Related Policies

If the big health planning and medical-related policies provide a good direction for listed companies to initiate industrial funds, then financial policies solve the problem of "where does the money come from".

As stated in the 2016 revised "Administrative Measures for Major Asset Restructuring of Listed Companies," "investment institutions such as legally established M&A funds, equity investment funds, venture capital funds, and industrial investment funds are encouraged to participate in the M&A and restructuring of listed companies." This has undoubtedly provided a significant boost to listed companies initiating or participating in industrial funds.

Conclusion

This is the best of times for capital, and also the best of times for entrepreneurship. Publicly listed companies and asset management firms wield substantial capital in their search for high-quality investment opportunities, while startups press forward with the determination to transform industries and change the world. Industrial funds represent just one of the many ways in which these two forces converge. High-quality projects can secure funding, and discerning capital can identify promising ventures; it is precisely this virtuous cycle that drives continuous social progress.

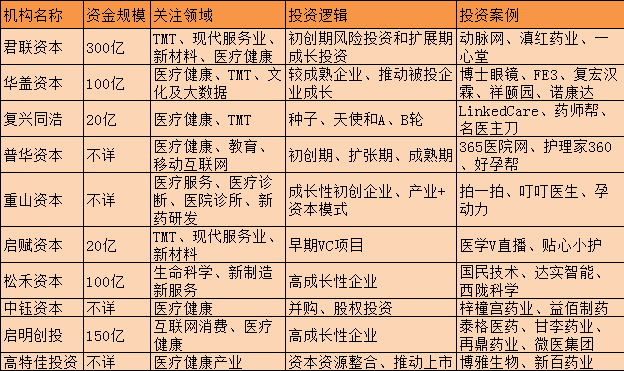

Alongside the capital influx into publicly listed companies, professional asset management firms and investment institutions have been deeply exploring the healthcare and wellness industry. These entities typically focus on startups and early-stage investments in specialized medical fields, playing a pivotal role behind many “unicorns.” We have also compiled relevant data and selected the 10 most renowned investment institutions in the healthcare sector.

Appendix 1: Overview of Active Investment Institutions (Companies) in the Healthcare Sector

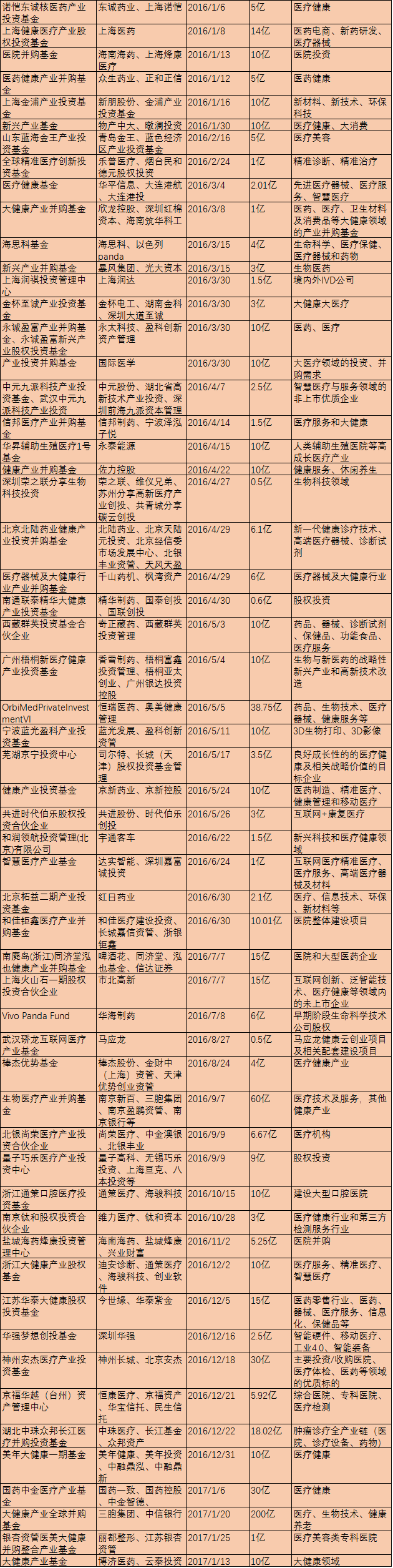

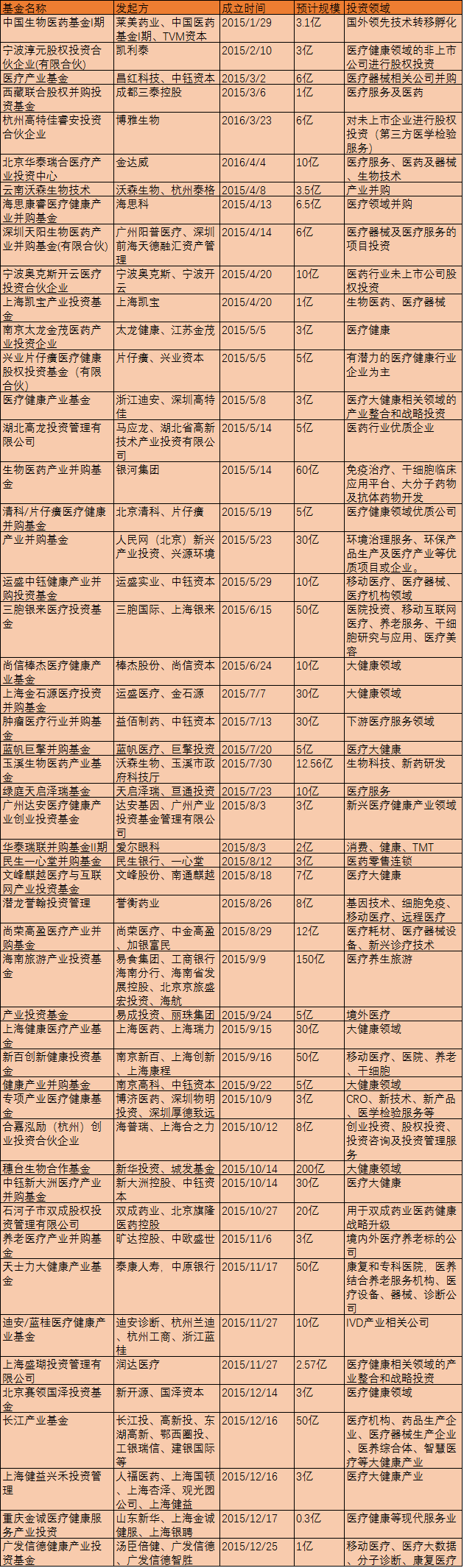

Appendix 2: Data on 108 Health Industry Funds

Overview of Big Health Industry Funds (2016–2017):