China's Pharma M&A Surge: Five-Fold Growth in Five Years, Total Deal Value Reaches RMB 180 Billion

M&A Momentum in China’s Pharmaceutical Industry Is Gaining StrengthDomestic small pharmaceutical companies, hospitals, and chain pharmacies, as well as foreign pharmaceutical firms, new drug R&D institutions, and healthcare organizations, have frequently become targets for mergers and acquisitions (M&A). Factors such as the implementation of the revised Good Manufacturing Practice (GMP) standards, pharmaceutical distribution planning, downstream expansion by pharmaceutical manufacturers, efforts to strengthen in-house R&D capabilities, reforms in drug approval and review processes, medical insurance cost containment and formulary adjustments, and strategies to expand overseas through partnerships have all contributed to the continuous M&A-driven expansion of pharmaceutical enterprises. Under the new competitive landscape, domestic pharmaceutical companies are leveraging their accumulated cash reserves and market capital to integrate resources, sparking a new wave of M&A activity.

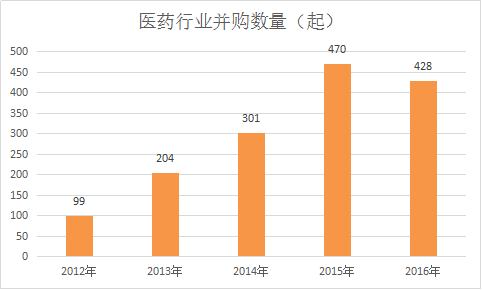

In 2016, the number of M&A deals in China's pharmaceutical industry exceeded 400, with the total transaction value surpassing RMB 180 billion., overseas M&A deals exceeded RMB 20 billion, setting new records for both the number and value of transactions. Looking back, data compiled from announcements by listed companies and research reports from renowned consulting firms show that since 2012, the number and value of mergers and acquisitions in China’s pharmaceutical industry have continued to grow, increasing more than fivefold over five years.

Why Is M&A in the Pharmaceutical Industry So Hot? Who Is Buying, Why Are They Buying, and How Has the M&A Logic Changed? VCBeat (WeChat ID: vcbeat) Provides a Detailed Analysis.

From 32 Billion to 180 Billion

According to announcements from listed companies and relevant research reports from consulting firms compiled by VCBeat, the number of mergers and acquisitions (M&A) in the pharmaceutical industry has shown a continuous upward trend since 2012. By 2015, the number had exceeded 450 deals, before declining last year.

Chart Note: Compiled from public sources and research reports; data completeness and accuracy are not guaranteed, for reference only.

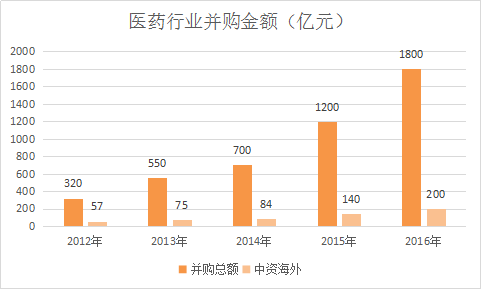

Corresponding to the sustained growth in the number of mergers and acquisitions (M&A), the total transaction value has repeatedly reached new highs. In 2012, the total M&A value in China’s pharmaceutical industry was approximately RMB 32 billion; by 2016, it had exceeded RMB 180 billion, representing a more than fivefold increase over the five-year period.

Chart Note: Compiled from public sources and research reports; data completeness and accuracy are not guaranteed. For reference only.

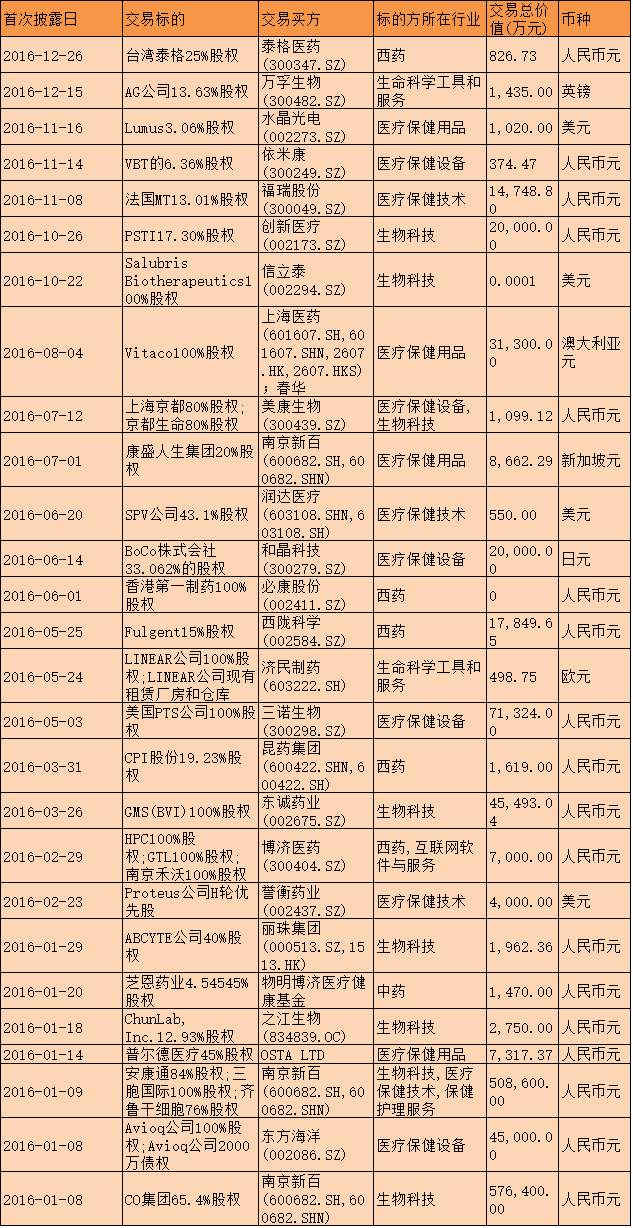

Major M&A Deals in the Pharmaceutical Industry: A Historical Review

Chart Note: Compiled from public information and research reports; data completeness and accuracy are not guaranteed, for reference only.

Policy Pressure Is the Trigger

The primary drivers of investment and M&A in the pharmaceutical industry are most directly spurred by the extension of industrial chain layouts, with back-door listings, asset restructuring, and the introduction of advanced overseas technologies and R&D capabilities also being key priorities.

According to the 2015 Annual Regulatory Statistics Report of the China Food and Drug Administration, as of the end of November 2015, there were a total of 5,065 manufacturers of active pharmaceutical ingredients (APIs) and finished dosage forms in China. Research by Orient Securities indicates that over 70% of pharmaceutical companies in China have annual revenues below RMB 50 million, with nearly 20% operating at a loss.

Based on this, the drive for pharmaceutical companies to increase industry concentration through mergers and acquisitions serves as an endogenous impetus for large-scale capital operations by pharmaceutical and related enterprises.

At the policy level, the new Good Manufacturing Practice (GMP) implemented in 2011 and the Quality and Efficacy Consistency Evaluation Policy for generic drugs implemented in 2016 have strongly driven mergers and acquisitions in the pharmaceutical industry.

The new GMP was implemented in March 2011, emphasizing sterile and purification requirements for the production process, while also requiring enterprises to establish a quality management system. Due to the increased cleanliness levels, the investment in facility construction and equipment will be substantial.

For instance, Yibai Pharmaceutical announced that the first phase of its GMP retrofitting project required an investment of RMB 271 million, with a payback period exceeding four years. For small pharmaceutical companies, such investments often exceed their annual profits, posing significant challenges to their financial strength and financing capabilities. At the time, there were voices suggesting that the new version of GMP would have a “reshuffling effect” on the pharmaceutical industry.

The reshaping effect of the new GMP on the industry has enhanced the competitiveness of large pharmaceutical enterprises, which have raised funds through public stock offerings and margin trading to upgrade their GMP-compliant workshops, while also extending their reach to small pharmaceutical companies with strong growth potential to acquire their drug production approvals.

Another policy with a significant impact on the industry landscape is the “Consistency Evaluation” initiative, which was launched in April last year. The regulation stipulates that generic chemical drugs in oral solid dosage forms listed in the National Essential Medicines List (2012 Edition) and approved for marketing before October 1, 2007, should, in principle, complete the consistency evaluation by the end of 2018.

Among the more than 5,000 manufacturers of active pharmaceutical ingredients (APIs) and finished dosage forms mentioned above, there are approximately 105,000 approval numbers for chemical drug production, the vast majority of which are for generic drugs. The scope of enterprises affected by the consistency evaluation policy and its overall impact far exceed those of any other policy.

First, there is a shortage of clinical resources. A senior executive at a listed pharmaceutical company stated that only 200 clinical institutions nationwide are qualified to conduct the relevant trials. With 17,000 essential drug varieties subject to consistency evaluation, completing all assessments would take at least ten years. In terms of cost, consistency evaluation is comparable to compliance with the new Good Manufacturing Practice (GMP) standards. Previously, the cost for consistency evaluation of a single product was around RMB 500,000–600,000. After the standards were raised, the cost increased to over RMB 5 million. Including preliminary basic research expenses, the total cost per product amounts to approximately RMB 8 million. As most pharmaceutical companies have multiple products requiring evaluation, the overall expenditure can reach hundreds of millions of yuan.

With the implementation of the new GMP and the consistency evaluation, the pharmaceutical industry is on the verge of a major reshuffle. It is widely acknowledged within the industry that the number of domestic pharmaceutical companies will be halved, dropping from approximately 5,000 to 2,500, with the market landscape evolving into an 80/20 split between state-owned and private pharmaceutical enterprises.

Based on this, the issue of mergers and acquisitions (M&A) and integration among pharmaceutical companies has been effectively addressed. Small pharmaceutical companies have not disappeared; rather, they have been incorporated into the systems of large pharmaceutical enterprises through mergers, restructurings, and other means. This integration allows them to leverage the capital strength of larger firms to navigate policy transitions, while also gaining access to enhanced competitiveness in areas such as production technologies and drug approval numbers. Among the more than 400 industry M&A transactions identified in 2016, over half involved such “big fish eating small fish” scenarios.

Backdoor Listing, Asset Restructuring, Overseas M&A

Backdoor Listing: A Case Study of Kaiyao Group’s Reverse Merger with Furen PharmaceuticalKaiyao Group is primarily engaged in the research and development, production, and sales of chemical drugs, traditional Chinese medicine (TCM) proprietary medicines, and active pharmaceutical ingredients (APIs). Its main products cover chemical drugs, TCM proprietary medicines, and APIs in various dosage forms. The company holds over 460 drug approval numbers, with nearly 30 varieties included in the National Reimbursement Drug List and more than 150 varieties listed in the National Essential Medicines List.Furen Pharmaceutical Group is a comprehensive conglomerate with pharmaceuticals and alcoholic beverages as its core industries, integrating R&D, production, operations, investment, and management. In late December 2015, Furen Pharmaceutical announced the acquisition of 100% equity interest in Kaiyao Group through a combination of share issuance and cash payment, with the total transaction amounting to RMB 7.85 billion.

The backdoor listing has proven to be a win-win scenario. Following the injection of Kaiyao Group into Furen Pharmaceutical, the combined entity has achieved comprehensive resource integration by leveraging Furen’s robust traditional Chinese medicine (TCM) production capabilities alongside Kaiyao’s chemical drug manufacturing strengths, thereby boosting performance.

In terms of asset restructuring, state-owned enterprises have taken the lead, with the injection of Chongqing Pharmaceutical into Jianfeng Chemical serving as a typical case. Both Chongqing Pharmaceutical and Jianfeng Chemical are subsidiaries of Chongqing Huayi Group. Jianfeng Chemical’s core business is urea production, and it incurred losses in 2014 and 2015, facing delisting pressure. Meanwhile, Chongqing Pharmaceutical had repeatedly planned to enter the capital market. Driven by their common controlling shareholder, Huayi Group, Chongqing Pharmaceutical was fully injected into Jianfeng Chemical last April, with a transaction consideration of RMB 6.698 billion. This round of transactions not only enabled Chongqing Pharmaceutical to achieve a backdoor listing but also preserved Jianfeng Chemical’s shell resource.

In terms of overseas mergers and acquisitions, the intensifying domestic competitive landscape and tightening policy environment are the primary drivers, with large pharmaceutical companies seeking to “borrow a ship to go to sea” by acquiring high-quality foreign targets. From an investment perspective, expectations of RMB depreciation and valuation disparities between domestic and international markets have emboldened pharmaceutical companies to purchase foreign assets. Additionally, the desire to introduce foreign R&D capabilities and advanced technologies is another key factor. Corresponding cases can be found for each of these points: for instance, Fosun Pharma acquired the Indian pharmaceutical company Gland Pharma with the aim of entering the European and American markets; Shanghai Pharmaceuticals acquired Vitaco’s premium health supplement product line to enhance group competitiveness and boost confidence in the secondary market; and Neptunus took control of Provisio, a U.S.-based manufacturer and technology provider of oncology equipment, intending to establish a presence in the oncology treatment sector.

In summary, the primary acquirers in pharmaceutical industry M&A include large pharmaceutical companies, cross-industry capital (via reverse mergers), corporate resource restructuring entities, and related industrial investors. The main drivers are acquiring drug manufacturing technologies and regulatory approvals, integrating the industry chain, restructuring resources, making capital investments, and introducing foreign technologies and R&D capabilities.

Pharmaceutical M&A Faces a Turning Point

Although policy and industrial incentives are unlikely to undergo significant changes in the short term, mergers and acquisitions (M&A) in the pharmaceutical industry have begun to reach an inflection point. A notable indicator is that the number of M&A deals in the pharmaceutical sector in 2016 experienced a slight decline compared to 2015, which may signal a shift in the trajectory of M&A activity within the industry.

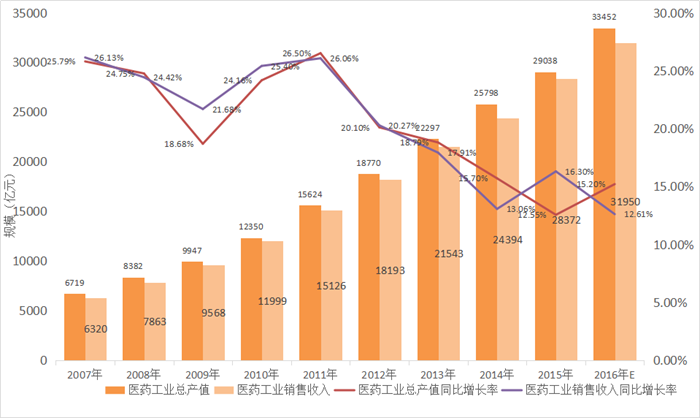

First, it should be pointed out that the pharmaceutical industry is still in a growth phase, but the growth rate has slightly declined, dropping by approximately half compared to the over 20% growth rate seen before 2012.

Chart Note: Compiled from public sources and research reports; data completeness and accuracy are not guaranteed. For reference only.

In the coming years, the pharmaceutical industry will maintain a state of low growth. Reflected at the level of specific corporate behavior, investment and merger and acquisition (M&A) activities will become more prudent. However, the underlying logic of M&A will not change significantly, with three types of targets continuing to lead the trends in pharmaceutical M&A.The first type comprises small pharmaceutical companies with certain market value, including those specializing in traditional Chinese medicine (TCM), chemical drugs, and blood products. M&A activities particularly target exclusive, high-quality TCM varieties.The second type includes healthcare service institutions, such as general hospitals at various levels, specialized hospitals, and chain clinics. Based on previous cases, major players in this field include Fosun, Kangmei, Hainan Haiyao, Tasly, Xinbang, and China Resources Sanjiu. Their pursuit of targets in this sector is expected to continue.The third type encompasses emerging medical fields, including precision medicine, gene technology, and internet-based healthcare. Previous cases indicate that investment amounts in this sector are mostly below RMB 100 million, and a clear value pattern has yet to emerge. Pharmaceutical companies engage in M&A in these areas primarily to enhance their narrative, with minimal short-term impact on financial performance.

Overseas M&A activities also show no discernible pattern. Of the more than 400 M&A deals completed last year, approximately 6% were overseas transactions. The targets were primarily concentrated in areas such as active pharmaceutical ingredients (APIs), generic drugs, medical devices, oncology technologies, genetic testing, radiation therapy, healthcare institutions, and health supplements, largely overlapping with the sectors involved in domestic M&A.

Source: Wind

Notably, the proportion of M&A and investments in emerging technologies is higher abroad than in China, accounting for approximately 40% of total M&A cases. A plausible explanation is that foreign pharmaceutical companies have higher R&D expenditures compared to their Chinese counterparts. Amid the global shift of generic drug manufacturing hubs, Chinese pharmaceutical firms seek to acquire technological reserves through a “money-for-time” strategy, thereby enhancing their capabilities in both original drug development and generic drug production.

Behind the wave of mergers and acquisitions (M&A) in the pharmaceutical industry are policy pressures and the inherent drive for corporate transformation. As growth in the pharmaceutical manufacturing sector stabilizes and industry competition shifts, pharmaceutical M&A has reached a turning point. Nevertheless, the rationale of targeting high-quality assets to enhance pharmaceutical companies’ competitiveness and market control remains valid, suggesting new highlights will emerge in pharmaceutical M&A activities.