China's Third-Party Medical Testing Market Poised for 10-Fold Growth, Inspired by Two Decades of U.S. ICL Evolution

By the end of December 2016, the National Health and Family Planning Commission successively issued the basic standards and management specifications for four categories of independently established medical institutions—medical imaging diagnostic centers, medical laboratories, blood purification institutions, and pathology diagnostic centers—and provided interpretations on issues of public concern.

The successive introduction of relevant policies has led to a sustained increase in capital market attention toward independently established medical institutions, such as clinical laboratories and imaging centers. VCBeat will analyze the current development status of these types of medical institutions in China and examine several benchmark enterprises. In this article, we focus on independent clinical laboratories. What exactly are independently established medical institutions? How significant is their growth potential? Which companies serve as industry benchmarks? And what is the state of development in foreign markets? You will find answers to all these questions within this article.

What Is an Independent Clinical Laboratory?

The concept of Independent Clinical Laboratories (ICLs), as defined by the Medical Administration and Hospital Management Bureau of the National Health and Family Planning Commission, is thatA medical institution with independent legal entity status that performs clinical laboratory testing on specimens derived from the human body for the purpose of providing information relevant to the diagnosis, management, prevention, and treatment of human diseases or health assessment, including clinical hematology and body fluid testing, clinical chemistry testing, clinical immunology testing, clinical microbiology testing, clinical cellular and molecular genetic testing, and clinical pathological examination, and issues test results.

Independent medical laboratories, also known as third-party medical testing institutions, differ from traditional hospital clinical laboratories in thatThis laboratory is a separately established medical institution, an independent legal entity that independently assumes corresponding legal liabilities and has no affiliation with the hospital.Therefore, such healthcare facilities are referred to as Independent Medical Institutions. In this document, the National Health and Family Planning Commission encourages private capital to participate in the establishment of independent medical laboratory institutions and promotes scaled development. Priority in setup approval will be granted to medical testing centers that aim to form chain-based and group-oriented operations.

Three Major Advantages of Independent Clinical Laboratories

The benefits of spinning off hospital clinical laboratories into independent entities are evident. Independent medical laboratories, leveraging economies of scale, offer advantages in efficiency, quality, and cost-effectiveness compared to hospital-based laboratories.

First, independent medical laboratories are more adept at cost control. By assuming the testing workload for an entire region, they achieve economies of scale, which enhances efficiency and reduces costs. Furthermore, their higher testing volume grants them certain bargaining power when dealing with upstream reagent suppliers and diagnostic equipment manufacturers. Another important reason isMajor hospitals can avoid redundant investment in building clinical laboratories, thereby reducing national expenditure on equipment procurement.

Secondly, independent clinical laboratories offer a wider variety of testing items than hospital laboratories due to their larger scale.Hospital laboratories typically offer fewer than 1,000 test items, whereas independent clinical laboratories can provide 1,000–2,000. For instance, KingMed Diagnostics offers more than 2,000 tests, while large independent laboratories in the United States and Japan can perform over 4,000 tests.

Third, independent clinical laboratories tend to procure equipment with higher precision and more advanced performance, while implementing stricter quality control standards.Independent clinical laboratories are mandated to obtain ISO 15189 accreditation, with some also achieving CAP accreditation, thereby offering advantages over hospital-based clinical laboratories in terms of standardized management and quality control.

Independent Medical Laboratory Testing Markets in China and Abroad

Development of the Independent Clinical Laboratory Market in the United States

Independent clinical laboratories in the United States emerged in the 1930s. Due to the large number of private practices, many of these healthcare providers lacked sufficient funds to purchase large-scale equipment for testing their limited sample volumes. Consequently, hospital laboratories began to offer outsourced testing services. Outsourcing became a widely adopted testing model among private practices and small healthcare institutions; however, at that time, it was primarily hospital laboratory departments that provided these outsourced services.

Since the 1960s, independent clinical laboratory testing institutions have emerged. The two major U.S. players, Quest and LabCorp, both originated in the 1960s: Quest’s predecessor, MetPath, was founded in 1967, and LabCorp’s predecessor, National Health Laboratories, was established in 1969.

From 1960 to 1980, total U.S. healthcare expenditure grew from $26.9 billion to $247.2 billion, with its share of the nation’s GDP rising from 5.1% to 8.9%. Beginning in the 1980s, in an effort to alleviate the financial burden of healthcare, the U.S. government and commercial health insurers successively revised insurance policies while simultaneously reducing medical subsidies to hospitals. In 1984, the U.S. Congress mandated that laboratory testing services be covered under Medicare Part B (Supplementary Medical Insurance) and instituted periodic reductions in the Medicare budget caps.

Under cost pressures, hospitals began outsourcing laboratory services to independent clinical laboratories with lower operating costs, marking the first phase of rapid growth for these entities. By the late 1980s, their market share had expanded to approximately 20% of the testing market. At that time, private clinics held an equal share of the testing market as independent clinical laboratories, while hospitals accounted for 60% of the market share.

In 1988, the U.S. Congress enacted the Clinical Laboratory Improvement Amendments (CLIA '88), subjecting private clinic laboratories and independent medical laboratories to strict regulation. Clinical laboratories must obtain certification under this act to ensure that the testing services provided by certified laboratories are consistent, accurate, reliable, and timely. The promulgation of this act spurred a second phase of rapid growth for independent medical laboratory institutions, which held advantages in quality and efficiency. By the mid-1990s, the market share of private clinic laboratories had declined to 8%, while the market share of independent medical laboratories expanded significantly to approximately 35% of the testing market, a proportion that has remained stable to the present day.

Meanwhile, large independent clinical laboratory companies began aggressive acquisitions to expand their market share. For example, Quest acquired SmithKline Beecham’s laboratory business for $1.3 billion in August 1999, leading to a significant surge in performance starting that year.

Currently, the independent medical laboratory testing sector in the United States is highly mature, with independent clinical laboratories accounting for approximately 35% of the market. The remaining roughly 60% of testing is conducted in hospital-affiliated laboratories, university laboratories, and other laboratory settings. In Germany and Japan, the market share of independent clinical laboratories exceeds 60% in both countries.

U.S. Market Case Study

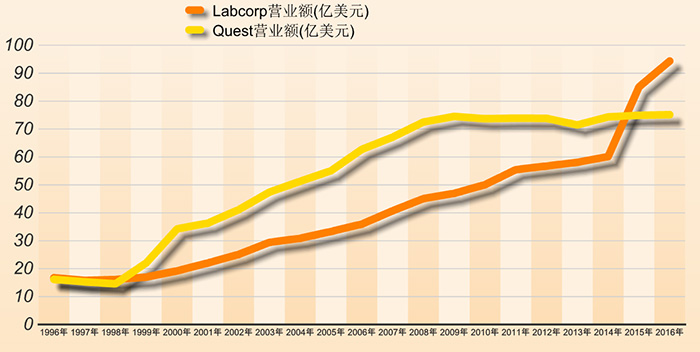

QuestandLabCorpThey are the two largest independent clinical laboratory companies in the United States, collectively accounting for approximately 70% of the U.S. independent clinical laboratory market. VCBeat has compiled and analyzed the key financial data of these two companies over the past two decades, which sufficiently reflects the evolution of the U.S. third-party testing market during this period.

Data Source: Quest Annual Report

Data Source: LabCorp Annual Report

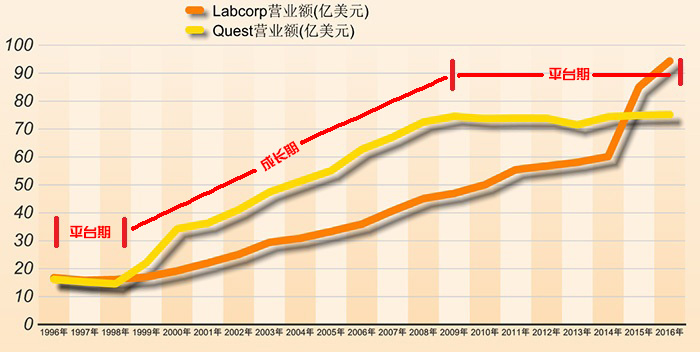

1998–2008: Rapid Growth Driven by Acquisitions

By examining the revenue trends over a 20-year period, we can observe that the true phase of rapid development for both companies occurred between 1998 and 2008. During this decade, their financial metrics exhibited significant growth. Taking Quest as an example, its business revenue declined slowly from 1996 to 1998, then began to grow rapidly starting in 1999, with a compound annual growth rate exceeding 10%, while its gross profit margin increased from 30% to over 40%. LabCorp followed a nearly identical growth trajectory. From 1998 to 2008, both companies embarked on a ten-year journey of sustained rapid performance growth.

Most critical is the change in market capitalization. Between 1998 and 2000, Quest’s market cap surged from $500 million to over $7 billion, while LabCorp’s rose from $450 million to more than $6 billion. As of March 2, 2017, Quest’s total market capitalization stood at $13.398 billion, and LabCorp’s at $14.553 billion. Over the 20-year period, the two companies’ market caps grew by factors of 30 and 41, respectively, with the most rapid growth occurring between 1998 and 2000.

Meanwhile, as both companies grew stronger, they began to engage in extensive mergers and acquisitions. Quest Diagnostics has shown a preference for acquiring laboratory assets, strengthening its service capabilities by purchasing laboratories across various regions of the United States, thereby increasing its market share. The acquisition of SmithKline Beecham’s clinical laboratory business in August 1999 marked the peak of its M&A activities. Subsequently, it acquired other companies related to the testing industry, such as MedPlus, LabOne, HemoCue, Pathway Diagnostics, Hartford HealthCare, and MemorialCare Health System, expanding its business scope beyond clinical laboratory services. In contrast, Labcorp has focused more on acquiring technology companies with new projects to enhance its competitiveness in specialized testing. The most typical example is its acquisition of Covance in 2015.

2008–2016: Inconspicuous Market Growth

Data from the past decade shows that the total revenue growth curves for Quest and LabCorp have been relatively flat.Independent testing laboratories in the United States have long maintained a stable 35% market share in the medical testing market, indicating thatThe U.S. independent clinical laboratory market has matured, leaving limited growth potential for the two dominant players.

LabCorp’s 10-year average growth rate was 10.06%, while Quest’s was 3.13%. In fact, LabCorp’s average growth rate exceeding 10% was driven by a 2014 acquisition that significantly boosted its revenue; excluding the 2015 data, the company’s actual 9-year average growth rate was only 6.94%.

LabCorp has long been the second-largest independent clinical laboratory in the U.S. market. Following its $6.1 billion cash-and-stock acquisition of Covance, the world’s second-largest contract research organization (CRO) for drug development, at the end of 2014, LabCorp saw a significant increase in total revenue in 2015, surpassing Quest.

Based on estimates from the testing market, the U.S. clinical laboratory market was valued at approximately $55 billion in 2014, with the independent clinical laboratory segment—holding a 35% market share—amounting to roughly $19.2 billion. In 2014, prior to the acquisition of Covance, LabCorp reported revenue of $6.012 billion, capturing a 31% share of the independent clinical laboratory market. Quest Diagnostics generated revenue of $7.435 billion, accounting for a 39% share of the same market. Together, these two companies commanded a 70% market share, while the remaining 30% was divided among other small and medium-sized independent laboratories. Undoubtedly, LabCorp and Quest Diagnostics are the two dominant players with decisive influence in the U.S. independent clinical laboratory market.

Other Data Changes

Over the past decade, the gross profit margins of both companies have declined year by year from above 40%. In particular, LabCorp’s data for the first three quarters of 2016 showed a margin of only 33.2%. The acquisition of Covance reduced the company’s overall gross profit margin; however, within the testing segment alone, the gross profit margin remained close to 40%.

In LabCorp’s reported business data, testing services are categorized into routine testing (general testing), genetic diagnostics (specialized testing), and pathological diagnostics. Revenue from routine testing grew from $2.778 billion in 2008 to $3.657 billion by the end of 2014 (CAGR = 4.69%), while genomic and specialized testing experienced relatively faster growth, increasing from $1.478 billion in 2008 to $2.026 billion in 2014 (CAGR = 5.40%).

Quest offers a range of services including routine testing, genetic testing, anatomical pathology testing, drug abuse testing, and related services. Quest’s data also show that, as the routine testing market approaches saturation, corporate profitability is primarily driven by high-margin, premium offerings, with the compound growth rate of sales in genetic and tissue diagnostics significantly outpacing that of routine testing.

Development of China's Independent Medical Laboratory Market

Due to systemic factors, independent clinical laboratories in China started relatively late.

In the 1990s, with continuous socioeconomic development and advancements in laboratory testing technologies, the demand for testing services rose steadily and the range of test items expanded. Hospitals, as the sole providers of medical laboratory services, could no longer meet the actual needs of the growing testing and diagnostics sector. Since then, sporadic independent clinical laboratory enterprises have emerged in China.

KingMed Diagnostics, currently the largest independent clinical laboratory in China, originated as a subsidiary laboratory of Guangzhou Medical University and began exploring outsourced medical testing services in 1994. After 2000, independent clinical laboratories such as Daan Gene, Hangzhou Adicon, and Dian Diagnostics were established successively. In 2005, three institutions—Daan Gene, KingMed Diagnostics, and Adicon—launched nationwide chain operation models. Currently, the independent clinical testing services market is dominated by four leading enterprises: Dian Diagnostics, KingMed Diagnostics, Adicon, and Daan Gene, which collectively account for more than 75% of the total market share.

As the service segment of the in vitro diagnostics (IVD) industry chain, the development dynamics of the independent clinical laboratory market are highly susceptible to policy influences. The boom in the U.S. independent clinical laboratory market during the 1980s was driven by changes in health insurance policies, a trend mirrored in China. Although independent clinical laboratories began to emerge after 2005, they lacked corresponding policy support, with the market outpacing regulatory frameworks. It was not until 2009, when the Ministry of Health issued the Basic Standards for Clinical Laboratories (Trial), that clinical laboratories (independent clinical laboratories) were officially added as a category of medical institutions for the first time. This policy established preliminary requirements for capital, personnel, and equipment necessary for setting up such facilities. Effectively serving as an “identity card” for independent clinical laboratories, this policy laid the groundwork for the industry’s rapid growth. After 2009, the number of independent clinical laboratories across China exceeded 200, marking the beginning of a flourishing and diversified industry landscape.

In June 2012, the State Council issued the "Opinions on Pilot Comprehensive Reform of County-Level Public Hospitals," which for the first time proposed to "encourage resource intensification, explore the establishment of inspection and testing centers, promote mutual recognition of inspection and test results among medical institutions, and outsource logistical services." This marked the national government's first explicit endorsement of the outsourcing model for laboratory services.

On October 14, 2013, the State Council issued the “Several Opinions on Promoting the Development of the Health Service Industry.” Provisions such as “intensify openness in the medical services sector; all areas not explicitly prohibited by laws and regulations shall be opened to social capital” were interpreted by the industry as a significant signal that the government encourages the development of private medical institutions, including third-party medical laboratories.

In December 2016, the National Health and Family Planning Commission issued the *Basic Standards for Medical Laboratories (Trial)* and the *Management Specifications for Medical Laboratories (Trial)*, introducing new regulations on policy oversight, scale, and service quality. The policies encourage the chain and group-based development of independent laboratories, which is a significant benefit for companies involved in this sector. In particular, leading enterprises hold advantages in terms of scale, cost, and management capabilities, potentially squeezing the survival space for small and medium-sized testing institutions.

Independent medical laboratories face substantial industry barriers. In addition to obtaining approval from municipal-level or higher health and family planning administrative departments to secure a "Medical Institution Practice License," they must also obtain approvals from environmental protection and public security authorities, implement quality control in accordance with the ISO 15189 standard, and be uniformly incorporated into the local medical quality control system for oversight. Engaging in independent third-party forensic appraisal services further requires approval and supervision by judicial administrative departments.

Despite high barriers to entry, this industry has become a sector encouraged by the state for development and will gradually enter a phase of rapid growth, with potential competitors increasing over time. If testing agencies lack core competitiveness in technical capabilities, cost control, and quality management, they are highly likely to face market risks in the competitive landscape.

Case Studies of the Chinese Market

KingMed Diagnostics

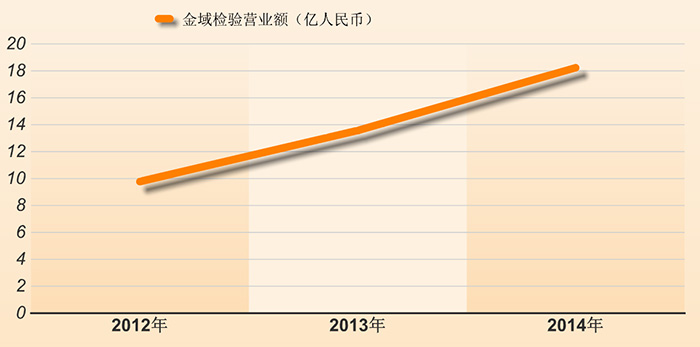

Data source: KingMed Diagnostics' prospectus

KingMed Diagnostics is headquartered in Guangzhou. Its core management team began exploring outsourced medical laboratory services in 1994 and formally established Guangzhou KingMed Medical Laboratory Center Co., Ltd. in 2003. The company currently primarily engages in medical laboratory testing, clinical trials, food hygiene testing, and forensic appraisal. It has established 33 medical laboratory facilities across mainland China and the Hong Kong Special Administrative Region. In 2015, KingMed Diagnostics submitted an initial public offering (IPO) application, disclosing its operational data from 2012 through the first three quarters of 2015 in its prospectus. From 2012 to 2014, driven by the expansion of its sales scale, the company’s operating revenue continued to grow, achieving a compound annual growth rate (CAGR) of 36.61%. Specifically, revenue increased by RMB 379 million in 2013 compared to 2012, representing a growth rate of 38.77%; and by RMB 468 million in 2014 compared to 2013, representing a growth rate of 34.48%.

KingMed Diagnostics’ core business is third-party medical laboratory testing, which accounts for over 95% of its revenue. Biochemistry and chemiluminescence testing represents a relatively traditional segment within KingMed’s medical laboratory services; although it contributes the largest share of revenue, this proportion has been declining year by year, dropping from 28.31% in 2012 to 26.85% in 2015. In contrast, the emerging genomics testing segment has experienced rapid growth, with its share of core business revenue increasing from 16.14% to 20.05%.

Dian Diagnostics

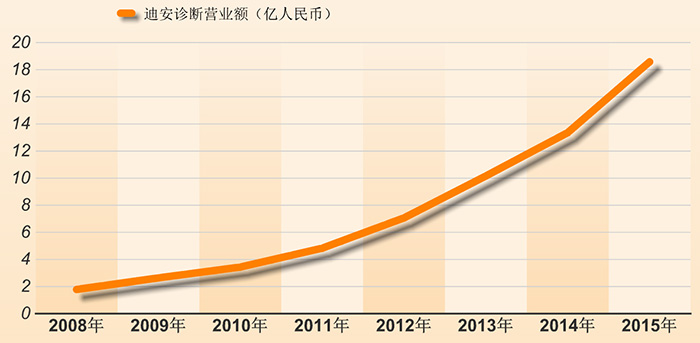

Data Source: Dian Diagnostics Annual Report

Zhejiang Dian Diagnostics Technology Co., Ltd. was established in 2001 as an independent third-party medical diagnostic service provider, with outsourced diagnostic services as its core business. It went public in 2011, becoming the first listed independent clinical laboratory in China. In recent years, Dian Diagnostics has maintained a very high growth rate, averaging 39.9%. A comparison of the latest complete annual reports available for both companies shows that in 2014, Dian Diagnostics reported operating revenue of RMB 1.335 billion, of which RMB 829 million came from its medical testing services. The remaining revenue was generated from its agency business for in vitro diagnostic (IVD) products, including the sale of testing instruments, IVD reagents, and consumables. By contrast, KingMed Diagnostics recorded the highest revenue in the industry at RMB 1.823 billion, accounting for 20% of the entire independent clinical laboratory market.

In addition to the two companies analyzed above, adding Adicon and Daan Gene, these four companies are currently the top four independent clinical laboratory companies, collectively accounting for approximately 70% of the market share.

Data Comparison of Benchmark Companies in China and the United States

Growth Rate and Market Share

We compare the data of four independent clinical laboratory companies in China and the United States. In terms of growth rate, Quest Diagnostics and LabCorp in the U.S. have recently encountered growth challenges, unless they pursue large-scale acquisitions. However, these two companies are already massive in scale, collectively holding a 70% share of the U.S. market, making it difficult to accelerate growth through mergers and acquisitions within the same industry. For instance, LabCorp’s most recent acquisition was that of the contract research organization (CRO) Covance at the end of 2014, which significantly boosted its revenue but had little relevance to medical testing laboratories.

After reaching approximately 35% market share around the year 2000, the market share of independent clinical laboratories in the United States remained virtually unchanged for more than a decade until 2016, indicating a high level of industry maturity. So, what is the current size of China’s independent clinical laboratory market?

Meanwhile, the two Chinese companies featured in this case study have been experiencing rapid growth in recent years, with their revenue growing at a rate of nearly 40%.

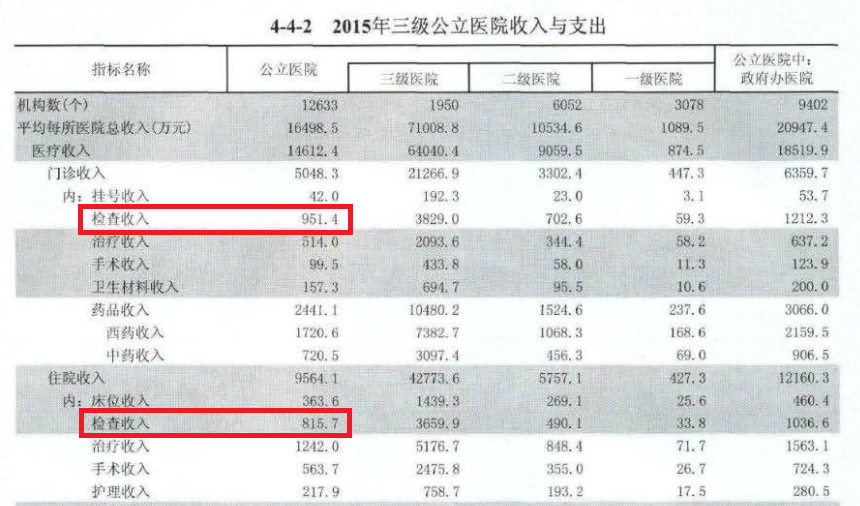

Based on data from the “China Health and Family Planning Statistical Yearbook 2016” released by the National Health and Family Planning Commission, we can estimate the proportion of revenue generated by independent clinical laboratories within China’s overall clinical testing market. There are a total of 12,633 tertiary public hospitals in China. In their medical revenue for 2015, the average outpatient testing revenue per hospital was RMB 9.514 million, and the average inpatient testing revenue was RMB 8.157 million, allowing us to calculate the combined total as follows:The total market size of clinical laboratories in tertiary public hospitals in China is approximately RMB 223.1 billion.Meanwhile, the annual medical revenue of tertiary public hospitals reached RMB 2.1596 trillion, with examination fees accounting for approximately 10.3% of their total medical revenue.

Data source: China Health and Family Planning Statistical Yearbook 2016

Data source: "China Health and Family Planning Statistical Yearbook 2016"

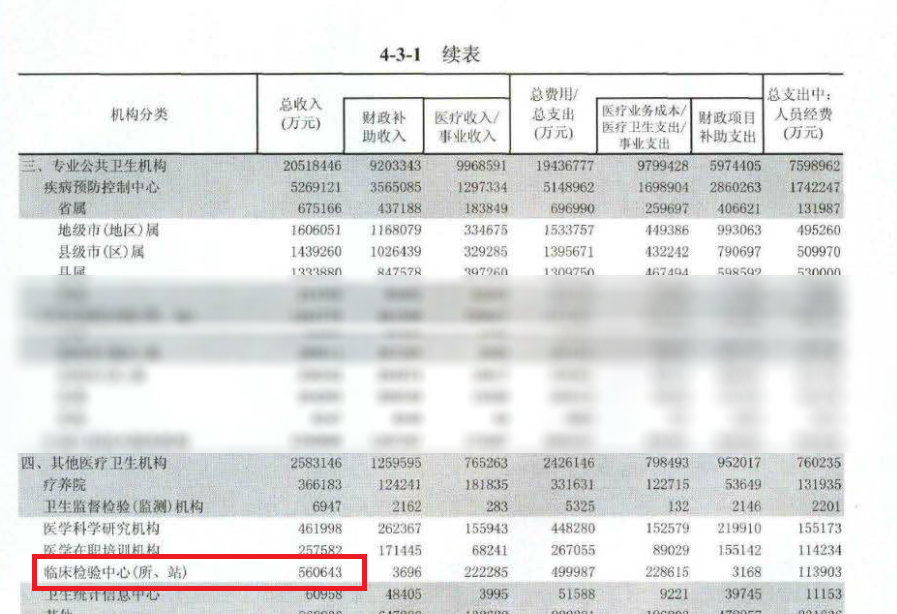

Although the yearbook does not list the total revenue from diagnostic tests for private hospitals and primary healthcare institutions, it can be estimated by multiplying the total revenue of private hospitals (RMB 140.3 billion) by the proportion of diagnostic test fees in medical revenue, which is 10.3%.Examination fees at private hospitals amounted to approximately RMB 14.45 billion.. The total revenue of primary healthcare institutions was RMB 262 billion, with examination fees amounting to approximately RMB 26.989 billion. In 2015, clinical laboratory centers (independent medical testing institutions) generated RMB 5.6 billion in revenue. Summing these four categories, China’s medical testing market totaled approximately RMB 270.1 billion in 2015.

According to the National Health and Family Planning Commission’s Statistical Yearbook, the revenue of independent clinical laboratories (ICLs) was only RMB 5.6 billion, whereas the actual figure is estimated to be around RMB 7–7.5 billion. This market, valued at RMB 270.1 billion, is referred to as the existing market dominated by routine testing, or more specifically, the ICL market space primarily comprising the 1,462 routine test items specified in the “Catalogue of Clinical Laboratory Tests for Medical Institutions.” Novel testing services in the incremental market, such as genomics, are not included in these statistics.

To reach the first peak stage of independent medical laboratories in the United States, which accounted for 20% of the medical testing market share in the late 1980s, China’s independent medical laboratory market still has a huge growth potential of tenfold.

High Gross Margin, but Low Net Profit

The transportation of laboratory specimens requires coordination with logistics systems, subject to constraints such as time sensitivity and cold-chain requirements, thereby necessitating regional consolidation. From an operational management perspective, third-party medical testing is more complex than other centralized industries, making refined process management more challenging. Consequently, once third-party medical testing enterprises achieve scale, they are difficult to surpass in the short term. However, although the gross profit margins of two major domestic testing institutions exceed 35%, approaching 40%—comparable to those of two U.S. companies—their net profit margins remain unsatisfactory.

Taking KingMed Diagnostics as an example, its operating revenues from January to September in 2012, 2013, 2014, and 2015 were RMB 980 million, RMB 1.36 billion, RMB 1.82 billion, and RMB 1.71 billion, respectively, while its net profits were only RMB 51.26 million, RMB 59.94 million, RMB 78.86 million, and RMB 110 million, respectively. Among the 38 subsidiaries and two associate companies under KingMed Diagnostics, 14 subsidiaries and two associate companies reported losses. Independent clinical laboratories belong to the labor-intensive medical services sector, characterized by relatively high fixed costs. During its expansion, the company established numerous new laboratories; however, business volume could not grow rapidly in the short term, resulting in low profit margins.

Will Hospital Clinical Laboratories Disappear?

Having reviewed the advantages and development history of independent clinical laboratories, we remain optimistic about their future growth potential. However, does this mean that hospital-based clinical laboratories are no longer necessary? Not at all.

Independent clinical laboratories serve as a supplement to the clinical laboratory departments of public hospitals, and their development is constrained by the current state of healthcare in China.However, while China’s vigorous promotion of shifting outpatient services to primary healthcare institutions presents new development opportunities for independent clinical laboratories, a substantial volume of hospital-based laboratory testing will continue to remain within public hospitals over the long term.

Grade A tertiary hospitals shall establish [structures/mechanisms] in accordance with regulations during the accreditation process.Comprehensive Test MenuThere are few laboratory testing projects that need to be outsourced to third-party medical testing companies. The revenue from the laboratory departments of public hospitals accounts for a significant proportion, so public hospitals usually handle projects with stable technology and clear risks on their own. In addition, public hospitals have advantages in sample turnaround time and talent development, which independent medical laboratory institutions cannot surpass for now.Independent clinical laboratories can only undertake testing items that public hospitals are unwilling or unable to perform, including routine tests and genetic tests that are technically complex, yield unstable results, or have low sample volumes.

Independent clinical laboratories also have opportunities in other tiers of hospitals and primary healthcare institutions.For county-level and lower-tier hospitals, establishing a medical testing center of a certain scale not only entails purchasing expensive testing equipment and reagents but also requires cultivating specialized personnel and attracting talent, which is unrealistic.Therefore, independent clinical laboratories will gain faster growth opportunities in the advancement of tiered diagnosis and treatment.

Development Opportunities for Independent Clinical Laboratories

The new healthcare reforms have provided significant development opportunities for independent clinical laboratory services. With the advancement of tiered diagnosis and treatment, national policies encourage the establishment of independent clinical laboratoriesCenter, to achieve regional resource sharing and address the issues of insufficient resources and limited testing capabilities in primary healthcare institutions, by outsourcing certain laboratory tests to testingA third-party provider with a comprehensive service portfolio and reliable quality.

With the strengthening of medical insurance cost containment and in conjunction with reforms to medical service pricing, the state will further reduce examination fees at public hospitals following the elimination of drug price markups.. Driven by cost-control considerations, healthcare institutions are outsourcing a greater number of testing items to independent clinical laboratories that offer economies of scale and lower costs. ThisStrikingly similar to the development opportunities for independent clinical laboratory companies in the United States after the 1980s, driven by healthcare cost containment measures.

In addition to benefiting from the advancement of tiered diagnosis and treatment, the 13th Five-Year Plan placed significant emphasis on precision medicine. The rapid development of next-generation gene sequencing technologyWith the continuous reduction in development and sequencing costs, precision medicine can be rapidly applied across all aspects of biomedicine. Independent medical laboratories providing third-party servicesInstitutions will gain new opportunities from upstream precision drug R&D and downstream personalized medication demands driven by clinical diagnostics.

Under the 13th Five-Year Plan, it was required that by 2020, leading global enterprises in the bio-services industry would be cultivated to drive the development of China’s original drugs, innovative drugs, and therapeutic methods.the launch, to establish a specialized independent third-party service provider offering standardized genetic testing, genetic data interpretation, liquid biopsy, and traditional Chinese medicine testing, thereby cultivatingA specialized service platform for gene therapy, cell therapy, immunotherapy, and other fields that complies with international standards. Therefore, independent clinical laboratories will usher in a new era in geneRapid Growth Opportunities Driven by the Expanded Application of Technology.

Considering the rapid growth of China's overall healthcare market, the increasing outsourcing of laboratory testing services by public hospitals, the advancement of tiered diagnosis and treatment systems, and the widespread adoption of new diagnostic tests, over the next five years,The market size of China's independent clinical laboratory sector may reach RMB 20 billion. Over the next decade, achieving a 20% market share in the independent clinical laboratory market may not be difficult to realize.