Amazon and Google Are Watching, Apple Is Waiting: The 'Rebels' Eye Control of Healthcare

“The Economist” has recently intensified its focus on the intersection of technology and healthcare, offering bold predictions about technology’s impact on the sector and pinning hopes for medical innovation on tech giants outside the traditional healthcare industry, such as Google, Amazon, and Apple. In fact, IBM and Microsoft—two other major players—have also been aggressively investing in healthcare.As China’s tech-driven healthcare sector continues to grow and strengthen, this article holds considerable reference value. Here,VCBeat (WeChat: vcbeat) has compiled a detailed summary of its discussions and viewpoints.

Tech companies’ years-long efforts to digitally transform healthcare are finally bearing fruit. Traditional healthcare players’ThroneComfortably seated, yet suddenly realizing that its dominant position is about to be lost.

Common sense tells us that the key to saving patients experiencing cardiac arrest lies in racing against time. Amazon’s Alexa voice assistant can recite cardiopulmonary resuscitation (CPR) procedures, which were taught to it by the American Heart Association in partnership with Amazon. As a health assistant, Alexa is also accumulating other healthcare capabilities, including providing companionship for the elderly and answering questions about pediatric disease treatments. In the near future, it may also help physicians perform voice documentation when their hands are occupied or remind patients to take their medications on time.

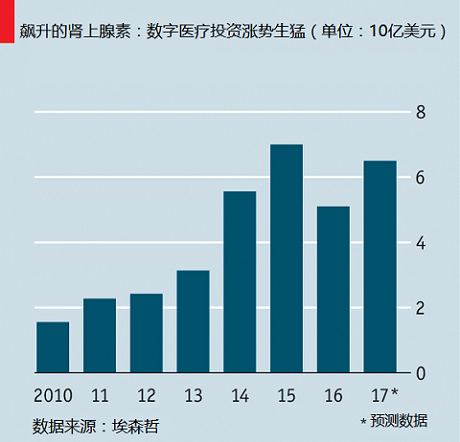

Amazon’s Alexa is merely one attempt within the healthcare industry, a sector with a relatively low level of digitalization. Due to overly stringent regulations and the high costs associated with medical innovation, the tech industry’s forays into healthcare have largely constituted a grand narrative of failure. Nevertheless, unbeknownst to many, the digital transformation of healthcare has begun to accelerate, with investments in this area surging.

A major driver behind the accelerated digitalization of healthcare is the potential for cost savings. As populations age, many countries face mounting pressure from rising healthcare expenditures, a significant portion of which stems from inefficiencies that are entirely avoidable. For the same condition, different treatment approaches can lead to vastly disparate medical costs. In wealthy nations, approximately one-fifth of healthcare spending is wasted on practices such as erroneous or unnecessary treatments. Eliminating these inefficiencies would yield substantial potential benefits.

Consumers have adopted a significantly more open attitude toward digital healthcare compared to previous years. Technologies such as telemedicine, mobile health applications, and analytical methods leveraging digital models for predicting medical outcomes have seen broader adoption. Additionally, automatic diagnostics and wearable sensors are increasingly utilized in monitoring physiological indicators like blood pressure.

# The Landscape Upended: Three Types of Players Vie for Power and Profit

If the digitalization of healthcare is defined as a reform, then there will inevitably be winners and losers. Andy Richards, an observer of digital health, believes that three types of players in the industry are currently vying for control over the “healthcare value chain.”

The first category of players is "Traditional Innovators", namely pharmaceutical companies, hospitals, and medical technology companies, such as GE HealthCare, Siemens, Medtronic, and Philips;The second category is “incumbents”, including health insurers, pharmacy benefit managers (PBMs), and single-payer healthcare systems such as the UK’s National Health Service (NHS);The third category is the “Rebels”, tech giants such as Google, Apple, and Amazon, which are aggressively developing healthcare-related apps, predictive diagnostic systems, and novel medical devices, are gradually profiting from the digital transformation of healthcare.

“Traditional innovators” face the threat that medical records are about to become fully electronic, and new patient information will be obtained from gene sequencing, sensors, and even social networks. Governments and insurers will have a clearer understanding of which treatments are effective and will shift toward outcome-based reimbursement models. This means that products developed by “traditional innovators,” no matter how high-tech, will not be purchased if they fail to deliver satisfactory therapeutic outcomes.

Marc Sluijs, a digital health investment advisor, stated that the next major question is whether pharmaceutical companies will emerge as the biggest losers in this reform. Increasingly comprehensive data will further transparentize the drug market, revealing which medications are ineffective and which conditions do not require pharmacological intervention at all.

The Disappearance of Traditional Players' Dividends in the Digital Era

Dan Mahony, a partner at investment management firm Polar Capital, believes that diabetes medications are bearing the brunt of the challenges posed to pharmaceutical companies by healthcare digitalization. Evidence indicates that physical exercise can effectively control diabetes and even prevent individuals with prediabetes from developing the disease, prompting the emergence of new healthcare services. For instance, UnitedHealthcare, a major U.S. health insurer, has launched a new program in which specialized coaches help individuals with prediabetes prevent disease progression through exercise.

For insurers, providing customers with wearable devices that encourage them to engage in a bit more daily physical activity is far more cost-effective than covering years of mounting medical expenses. Although people often joke that fitness wearables like Fitbit ultimately end up gathering dust in a drawer, such devices have proven effective in helping individuals increase their activity levels within certain insurer-partnered programs. Data shows that since its launch last year, the location-based mobile game Pokémon Go has prompted players worldwide to walk nearly 9 billion kilometers.

Onduo, a company jointly established last year by Google Capital, Verily, and the French pharmaceutical giant Sanofi, was born against this backdrop. Onduo assists patients with diabetes in adhering to medication regimens and adopting healthier lifestyles, and will subsequently support individuals at risk of diabetes in managing their condition. For Sanofi, Onduo represents a strategic hedging investment; in 2015, Sanofi lost patent protection for its blockbuster injectable diabetes drug, Lantus, and faced declining sales.

This shift in mindset is no easy feat for pharmaceutical companies.Digital Innovation Means Product Sales Will Be More Results-Oriented, if pharmaceutical companies continue to prioritize sales volume over patient-centricity, they will face the risk of being eliminated from the market.

Some large hospitals act as both “incumbents” and “traditional innovators,” and are likewise influenced by the digital health trend. The rise of telemedicine and the emphasis on disease prevention and early diagnosis will lead to a decline in hospital admission rates, particularly within commercialized healthcare systems.The Most Profitable Emergency Department Revenue Will Decline Significantly. The most critically ill patients will receive specialized services; for example, Evolution Health provides care to 2 million severely ill patients across 15 U.S. states. It claims to reduce emergency department visits by 20% and hospitalizations by 40%.

The Explosion of MedTech: Tech Giants to Exert Strong Influence

However, hospitals are also set to receive good news: more machine learning projects can make diagnoses from scanned images and test results. Recently, medical staff at London's Royal Free Hospital began using an app that can analyze medical data in real time. Developed by DeepMind, Google’s artificial intelligence subsidiary, the app is capable of identifying patients at risk of acute kidney failure. The hospital stated that this app has already saved nurses a considerable amount of time.

Medical technology companies providing these conveniences to hospitals have even bolder visions. They claim that healthcare will soon move into the home, with diagnosis and monitoring of conditions such as heart disease, concussion, skin cancer, and ear infections achievable through apps and sensors. Last year, the FDA approved as many as 36 health-related apps and devices.

In some developing countries where medical data regulation is less stringent and accessing hospital care is fraught with difficulties, the growth of digital health technologies has been even more pronounced.For example, in China, the largest venture capital investment in 2016 flowed into its digital health sector, namely Ping An Good Doctor's $500 million financing round.

In the short term, medical apps with location-based features will experience explosive growth, and remote consultation services will expand rapidly. In the long run, tech giants will exert the greatest influence. Amazon and Google are closely monitoring the healthcare industry, while Apple is deciding which healthcare sectors to enter.

Profound changes are now inevitable. Investors are seeking healthcare technology unicorns valued at over $1 billion, while payers are focusing on technologies that can generate substantial cost savings. Ultimately, the biggest winners are patients, who either receive better care through health tech or avoid becoming patients altogether thanks to digital health innovations.

Source: The Economist

Author: Christian Assad-Kottner, interventional cardiologist and professional medtech geek.