15 Chinese Real Estate Giants Pivot to Healthcare: Strategic Moves Across Four Key Sectors

In early March 2016, VCBeat compiled a list of approximately 15 real estate developers in China that had entered the healthcare sector and summarized four key observations: 1) All are publicly listed companies with robust cash flows; 2) They actively respond to government initiatives by investing in and constructing hospitals; 3) They are venturing into internet healthcare to gain a first-mover advantage; 4) The return on investment cycle is long, and scaling up will take time. The original article can be found in “How Have Wealthy Real Estate Developers Fared in Their Foray into the Healthcare Sector?》. Following the article’s publication, the editorial team received enthusiastic feedback from readers, prompting the release of a sequel.

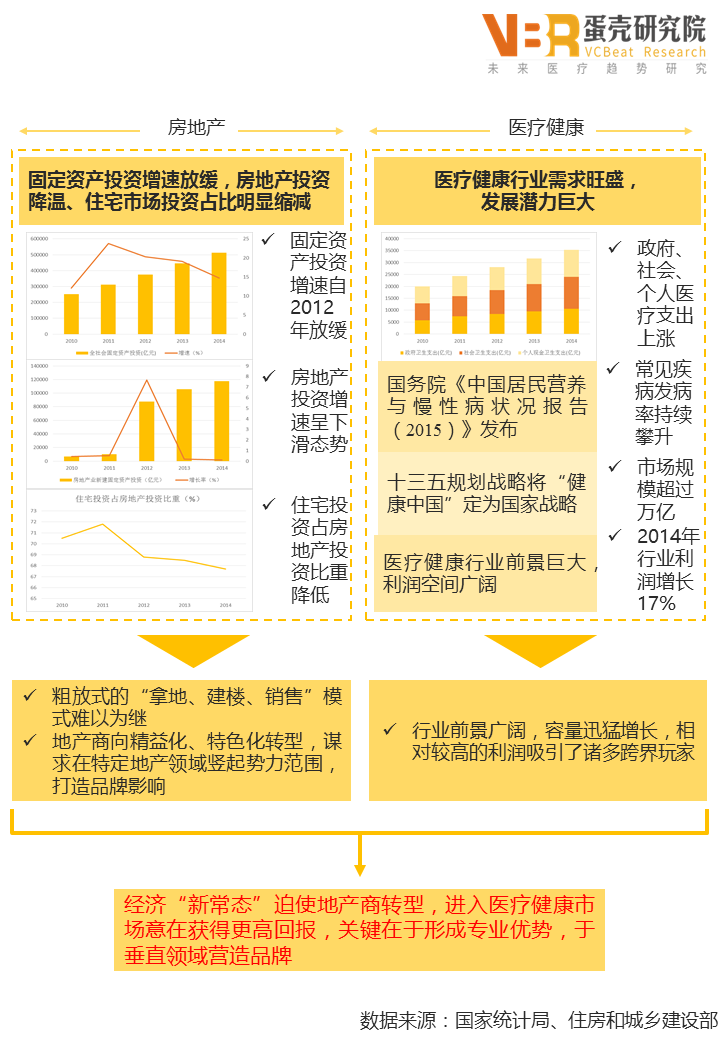

I. Traditional real estate developers face the dilemma of an economic downturn and are adjusting their strategic direction; with a promising outlook for the healthcare industry, investing in medical real estate has become one of the top priorities for these developers.

Although China’s total fixed-asset investment has maintained an overall upward trend, the growth rate has declined since 2012, with investment growth stabilizing. Meanwhile, the growth rate of real estate investment has shown a sharp decline. In terms of the share of residential investment within total real estate development investment, the proportion of residential investment has been gradually decreasing; between 2008 and 2014, this share dropped by 4.5 percentage points. This indicates that the growth rate of residential investment has lagged behind that of overall real estate investment, reflecting a gradual shift of capital from residential construction to other specialized construction sectors.

On the other hand, there is a huge demand for medical and health services in China. As society places increasing emphasis on health alongside rising living standards, domestic demand for healthcare services continues to grow, with medical expenditures increasing year by year. According to the "Report on Nutrition and Chronic Disease Status of Chinese Residents (2015)" issued by the State Council, the prevalence of chronic diseases and cancer has been rising in recent years. Furthermore, due to population aging, changes in dietary structure, physical inactivity, and environmental degradation, the incidence rates of various common diseases have increased and are unlikely to reverse in the short term.

From a policy perspective, the proposal for the 13th Five-Year Plan elevated “Healthy China” to a national strategy, unlocking a trillion-yuan market and positioning the domestic healthcare industry as a new engine of economic growth. In recent years, the central government has introduced various favorable policies to encourage social capital investment in the healthcare sector. Furthermore, the healthcare industry not only boasts promising prospects but also offers substantial profit margins. In 2014, the industry’s total operating revenue reached RMB 684.636 billion, a year-on-year increase of 13.57%, while operating profits amounted to RMB 63.386 billion, up 17.71% year on year. Compared with the squeezed profit margins in the real estate sector, the healthcare industry’s robust profitability and strong growth potential have attracted significant inflows of real estate capital.

II. Real estate developers transitioning into the healthcare sector should first prioritize businesses with high synergy, such as medical real estate development and hospital investment—areas characterized by heavy asset intensity and high development margins.

Real estate developers’ investment layout in the healthcare industry is primarily divided into four sectors, including (1) healthcare real estate development, (2) hospital investment and operation, (3) medical devices, pharmaceuticals, and services, and (4) non-clinical services.

Healthcare Real Estate Development: Due to the high synergy with their traditional business, real estate developers entered this sector at an early stage. In traditional healthcare real estate development models, developers were responsible only for the construction phase and exited immediately thereafter. However, in the current wave of transformation, in addition to undertaking early-stage development, real estate developers are also beginning to collaborate with relevant healthcare investment institutions during the mid-stage of projects, signing agreements with healthcare service providers to establish operations on-site, thereby enhancing the healthcare components of their projects. Furthermore, in the later stages, they form joint venture management companies with professional healthcare management groups. This demonstrates a strategy pursued by real estate developers during their transition to deepen their involvement and establish a strong foothold, aiming to achieve greater premium valuation by enhancing their professional expertise.

Hospital Investment and OperationsCapital is gradually shifting from sectors such as dentistry, ophthalmology, and health check-ups to specialized fields including diabetes care, oncology, orthopedics, neurosurgery, proctology, and nephrology, which demand higher levels of medical expertise. Unlike medical real estate development, property developers entering this sector are engaging more deeply in hospital management and operations. Common approaches include acquiring hospital operation and management companies, forming joint ventures to establish operation and management companies, and taking control of hospital operation and management companies. Given the scale of these property developers, current hospital investments are likely just initial forays; their long-term strategy is to build large-scale, chain-based, and branded hospital groups.

Medical Devices, Pharmaceuticals, and Services: It is evident that some regional small-scale real estate developers, whose growth has hit a bottleneck, prefer to enter this sector. First, their small scale makes it difficult to support the substantial capital outlays required for medical real estate development or hospital investment and operation. Even if they do enter the market, given the long payback period associated with medical real estate development, small and medium-sized real estate developers are more prone to liquidity challenges compared to nationwide developers. Avoiding direct competition with industry giants and seeking alternative pathways represents a relatively astute strategic approach; however, due to weak business synergies, whether they can successfully integrate target companies and achieve cross-industry transformation remains to be tested by the market.

Non-Clinical Services: Non-clinical services include hospital logistics services and healthcare supply chain finance, among others. Taking Yihua Health as an example, the company has continuously divested its real estate business over the past few years, completely transforming into the medical health sector. In 2015, Yihua Health acquired Zhongankang, one of the leading providers of non-clinical services for hospitals in China. Its main business includes providing logistical services to hospitals, such as property management, maintenance of medical equipment, medical support services, hospital catering, and distribution. Another example is Huaye Capital, one of whose investment directions involves acquiring accounts receivable from medical institutions and then securitizing these receivable assets.

Among the four points above, (1) and (2) represent the preferred entry pathways for mainstream real estate developers, presenting both opportunities and challenges. Points (3) and (4) are relatively niche; specifically, (3) involves a complete departure from the real estate sector and thus holds limited representative significance. Furthermore, regarding market entry strategies, smaller real estate developers tend to favor mergers and acquisitions (M&A). However, whether they possess comprehensive M&A strategies, conduct thorough due diligence, and ensure effective post-merger integration (such as by establishing dedicated integration departments) remains an intriguing subject for examination.

III. In the United States, healthcare real estate has developed a relatively mature system, whereas China’s investment model for healthcare real estate differs significantly. Data on healthcare real estate investment trusts (REITs) indicate that senior housing and skilled nursing facility models are highly favored by institutional investors in the U.S., while hospital investments are not mainstream—a trend that is exactly the opposite of what is observed in China.

Although factors such as cultural differences and gaps in insurance reimbursement mechanisms have clouded the short-term outlook for capital-intensive investments in China’s senior housing and nursing home sectors, the immense demand driven by an aging society suggests that these segments will likely mirror the U.S. market in the future, accounting for half of the healthcare real estate sector.

Meanwhile, hospital investment has emerged as a new trend among domestic real estate developers in recent years. However, recruiting high-quality physicians, managing hospital operations, and building hospital brands remain long-term challenges. The public-private partnership (PPP) model actively promoted by the government may benefit investors to some extent, but its effectiveness still needs to be validated by the market. In the United States, large hospital institutions typically choose to build their own facilities to meet requirements related to medical processes, compliance, and infrastructure/equipment, while institutional investors are less involved in this sector.