Beyond Supply Chain: The Next Battleground for China's Pharmaceutical E-commerce

The pharmaceutical e-commerce sector has seen continuous activity recently, as companies ramp up efforts to strengthen their capabilities.

Since the beginning of this year, VCBeat (WeChat: vcbeat) has reported that Weiming Penguin announced tens of millions in Series A financing; 7lecare laid out its “Internet Healthcare Complex” strategy and secured funding; Yaoshibang completed RMB 110 million in financing; 111.com entered into a strategic partnership with Biostime; and Jianke reached collaborations with multiple pharmaceutical companies and health supplement manufacturers.

Pharmaceutical e-commerce players are actively strengthening their supply chains, expanding medical services, and introducing capital support this year, marking 2026 as a “watershed” year for the industry. Competition for market share and users is set to intensify dramatically. In response to key weaknesses such as restrictions on online sales of prescription drugs, challenges in integrating with medical insurance systems, and insufficient professional services, these companies are seeking breakthroughs through supply chain optimization, internet hospitals, mobile health solutions, and offline pharmacies. This strategy represents both an indirect approach to circumvent regulatory hurdles and an effort to build competitive advantages distinct from traditional offline models.

The Supply Chain Is the Lifeline of Pharmaceutical E-Commerce

Kang Kai, General Manager of Alibaba Health’s Tmall Pharmacy Pavilion, stated in an interview with VCBeat (WeChat ID: vcbeat) that the essence of pharmaceutical e-commerce is still e-commerce. Especially as e-commerce in other sectors has matured, pharmaceutical e-commerce can draw valuable lessons from them in areas such as supply chain management, marketing, operations, and cost control.

A review of the evolution of e-commerce demonstrates that the supply chain is its lifeline. The fundamental shift from early C2C transactions to the currently dominant B2C model lies in changes to the supply chain. In spontaneous C2C transactions, product quality is the most difficult factor to control. However, the internet is best suited for promoting and replicating standardized offerings, which requires a high degree of consistency in the quality and price of transaction objects. This has driven e-commerce products toward greater standardization. Enterprises, rather than individuals, are better positioned to maintain such consistency. Consistency in procurement (or the ability of platforms to verify and certify product attributes) builds the reputation of enterprises or platforms and fosters brand development. Amazon, Alibaba, and JD.com have all followed this development path, and their rich product offerings and standardized transaction processes are equally applicable to pharmaceutical e-commerce.

From the perspective of pharmaceutical e-commerce, the aspect most susceptible to user skepticism is the reliability of drug quality. An effective solution lies in strengthening the supply chain, manifested through diversified “Authentic Product Alliances” and strategic collaboration initiatives. 111.com (Yi Yao Wang) was the first in the industry to pioneer such an “Authentic Product Alliance,” securing endorsements from numerous large-scale pharmaceutical manufacturers, including Dong-E-E-Jiao, Huiren, Baiyunshan and Huangpu Pharmaceutical, among others. Since then, the alliance has continued to expand its membership, covering multiple sectors such as contact lenses and health supplements.

Another key objective for pharmaceutical e-commerce platforms to engage industrial enterprises and strengthen their supply chains is to expand product variety to meet user demand. As retail channels, pharmaceutical e-commerce platforms and offline pharmacies serve the same customer base. However, given the high penetration, extensive coverage, and high chain-store ratio of physical pharmacies, consumers have little incentive to purchase medications online. Moreover, unlike fast-moving consumer goods such as apparel, pharmaceutical purchases involve less need for personalization and autonomous decision-making, leaving limited room for “innovation.” Therefore, the primary competitive advantage for pharmaceutical e-commerce lies in offering a broader range of pharmaceutical products.

Generally, brick-and-mortar pharmacies typically stock between 2,000 and 3,000 SKUs (stock-keeping units, i.e., drug varieties), primarily due to constraints on inventory and management costs. In theory, however, there is no ceiling for SKU expansion in pharmaceutical e-commerce. Data released by several leading pharmaceutical e-commerce platforms indicate that their SKU counts have reached or exceeded 50,000. To a large extent, consumers turn to pharmaceutical e-commerce channels only when they are unable to find specific medications offline—a trend supported by survey data from a consulting firm, which shows that this user segment accounts for a significant proportion.

The supply chain is the lifeline of pharmaceutical e-commerce. First, extensive collaboration with the pharmaceutical industry endorses pharmaceutical e-commerce platforms themselves, building their brand. Second, such broad partnerships help expand the range of products listed, which largely becomes a key reason for users to choose a particular pharmaceutical e-commerce platform.

The Urgent Need for Differentiation in Pharmaceutical E-commerce

The Class C license for pharmaceutical e-commerce was initially available only to chain retail pharmacies as the applying entity, implying that e-commerce originally existed as an adjunct to offline retail. This inherent relationship determined the significant asymmetry between the two, giving rise to the two most burdensome “shackles”—prescription drugs and medical insurance reimbursement.

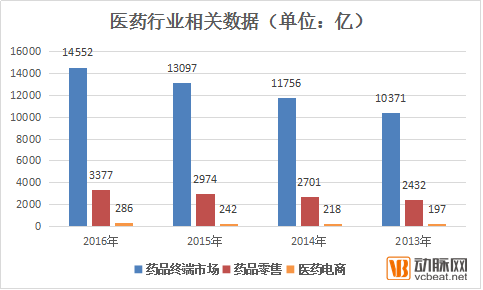

In fact, retail pharmacies that appear to have higher “priority” do not hold an advantage in obtaining prescriptions. Under the healthcare system where hospitals rely on drug sales for revenue, the distribution ratio of pharmaceuticals between hospitals and retail channels is approximately 80:20. Regardless of whether prescription drugs or over-the-counter (OTC) medications yield higher profit margins, offline retail stores are inherently at a disadvantage in terms of volume alone. When it comes to online pharmacies, they further lag behind chain stores in timeliness and professionalism, making the market situation predictable. According to relevant statistics, the total market size of pharmaceutical terminal sales in 2016 was RMB 1.4552 trillion, with retail pharmacy sales revenue reaching RMB 337.7 billion and B2C pharmaceutical e-commerce sales amounting to RMB 28.6 billion. Thus, the share of pharmaceutical e-commerce accounted for less than 10% of the overall pharmaceutical retail market.

Data Note: Compiled from market research and industry reports

Driven by policy initiatives, healthcare reform continues to deepen, and the opening of prescription channels may become the focal point for business expansion in pharmaceutical e-commerce. To address the outflow of prescriptions, three strategic directions are available: offline pharmacies, Direct-to-Patient (DTP) pharmacies, and internet hospitals. The limitation of offline pharmacies lies in their restriction to serving customers based on geographic location; however, with proper informatization, their service scope and customer base can be significantly expanded. A preliminary concept is the integrated “store-warehouse” model, where pharmacies function as regional distribution centers, thereby improving the operational efficiency of individual stores. DTP pharmacies represent a relatively new concept, specializing in the sale of innovative and imported drugs, making them highly suitable for operation via internet-based models. The third direction is internet hospitals. Following President Xi’s endorsement of internet hospitals at the Wuzhen World Internet Conference, this sector has experienced rapid development. As the most common access point, telemedicine effectively connects doctors and patients through video communication equipment in pharmacies, mobile apps, and websites, enabling the issuance of prescriptions. Pharmaceutical e-commerce platforms such as Ali Health, 111.com.cn, Jianke, and Qilekang have all begun to invest heavily in internet hospitals, aiming to enhance their professional service capabilities and secure prescription flows.

Regarding medical insurance, integrating pharmaceutical e-commerce with the national basic medical insurance system may not be realistic in China, given that cross-regional direct settlement has not yet been successfully implemented. However, there are two potential breakthroughs: Pharmacy Benefit Management (PBM) and commercial health insurance. Cost containment within the medical insurance system has always been a focal point of healthcare reform. PBM could provide pharmaceutical e-commerce platforms with room for strategic development. Leveraging their systematic accumulation of drug-related data and pharmaceutical consumption data, as well as their strong relationships with pharmaceutical manufacturers, these platforms can participate in the design of commercial insurance products, serving as key connectors across the upstream and downstream of pharmaceutical consumption.

For industrial enterprises, market assessments are prone to distortion within the “industrial enterprise–distributor–retailer” model. In contrast, the “industrial enterprise–e-commerce” model facilitates easy tracking of consumer data and product flows, enabling the acquisition of market feedback data that offers certain guidance value for production processes; this may well explain why such enterprises are actively embracing e-commerce.

Potential Return to Offline Channels in the Future

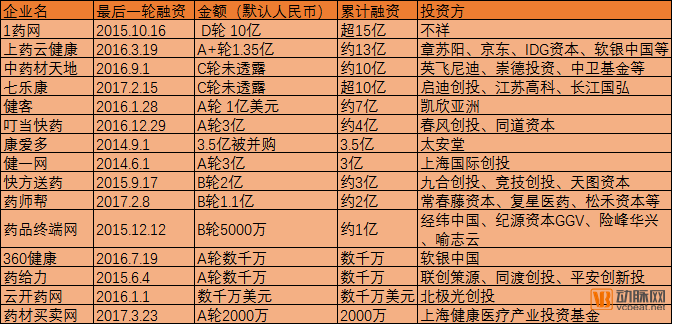

Capital has always been a critical driver in the development of pharmaceutical e-commerce. Currently, few pharmaceutical e-commerce enterprises are profitable; whether they are pure-play pharmaceutical e-commerce firms, platform-based pharmaceutical e-commerce companies, or those controlled by listed corporations, achieving a balance between costs and revenue remains challenging. Against this backdrop, sustained capital infusion can help pharmaceutical e-commerce enterprises strengthen their capabilities and actively break through existing market impasses.

Lu Sheng, a partner at Shengrui Consulting, has long observed the pharmaceutical e-commerce industry and proposed several hypotheses regarding capital’s role in driving its development. He believes that pharmaceutical e-commerce’s penetration into offline channels remains shallow, and that an integrated online-offline business model is more likely to stand out in future market competition.

Lu Sheng explained that the currently thriving pharmaceutical e-commerce companies can be broadly categorized into two camps: those with internet company DNA and those with retail chain DNA. Internet companies emphasize rapid market deployment and expansion of consumer-facing (C-end) users, giving them a marketing advantage. In contrast, retail chains treat their e-commerce operations as a supplement, focusing primarily on offline mergers and acquisitions. For instance, companies like Yixintang and Laobaixing acquire hundreds of stores annually, but their resource allocation to e-commerce is comparatively limited. Only through collaboration between retail chains and internet-driven companies can an integrated online-offline development model generate true “chemical reactions.”

In terms of cooperation models, options may include retail chains introducing internet teams, directly acquiring relevant enterprises, or engaging in deep partnerships to conduct joint operations at the business level.

“In essence, it remains a capital-driven process. Since last year, several pharmaceutical e-commerce platforms have secured massive rounds of financing, with cumulative funding for multiple companies exceeding RMB 1 billion. Without clear profitability to support such valuations, this financing trajectory cannot be sustained, let alone an eventual listing on the capital markets. Embracing the financial strength of retail pharmacy chains is a prudent strategic choice,” said Lu Sheng. He believes that capital infusion into pharmaceutical e-commerce is increasingly leaning toward industry-specific investors. Large retail pharmacy chains, with their robust financial capabilities and ability to effectively integrate these businesses, represent an alternative pathway beyond traditional financing for pharmaceutical e-commerce firms.

Data Note: Compiled from market research and industry reports.

Lu Sheng noted that the development of China’s pharmaceutical e-commerce sector can draw lessons from the United States, with Walgreens serving as a benchmark. As both the largest retail chain and the leading pharmaceutical e-commerce platform in the U.S., Walgreens initially built its foundation in retail. Over the course of its growth, it not only incubated its own e-commerce operations internally but also acquired several pharmaceutical e-commerce companies, ultimately achieving its position as the largest player in the national market.

From an industry-wide perspective, the ratio of online pharmaceutical sales to retail channel sales in the United States is approximately 3:7. In contrast, China’s pharmaceutical e-commerce sector still has substantial room for growth. By effectively integrating the advantages of both online and offline channels, a win-win outcome can be achieved.

“Everyone is talking about ‘New Retail’ now. New Retail refers to the synergy between online and offline channels. The same applies to pharmaceutical retail: traditional chains are actively embracing the internet, while pharmaceutical e-commerce is returning to offline operations, evolving into pharmaceutical New Retail,” summarized Lu Sheng.