Shanghai Pharmaceuticals Reports 2016 Revenue of RMB 120.77 Billion and Holds RMB 12 Billion in Cash, Signaling Potential for Major M&A

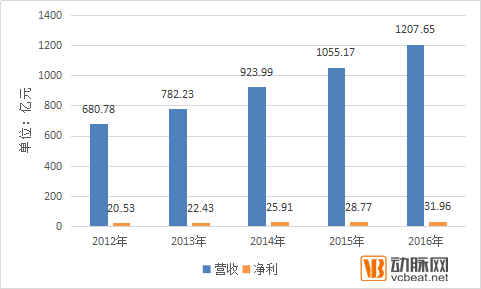

VCBeat (WeChat: vcbeat), March 22 news.Shanghai Pharmaceuticals (601607.SH) released its 2016 annual report today, disclosing revenue of RMB 120.765 billion during the reporting period, a year-on-year increase of 14.45%. Net profit attributable to shareholders of the listed company amounted to RMB 3.196 billion, up 11.10% year on year. Net profit attributable to shareholders of the listed company after deducting non-recurring gains and losses reached RMB 2.926 billion, representing a year-on-year increase of 15.62%. Earnings per share stood at RMB 1.1887, while earnings per share after deducting non-recurring gains and losses were RMB 1.0880.

This marks several consecutive years in which Shanghai Pharmaceuticals has achieved revenue and net profit growth exceeding 10%, maintaining a robust growth trajectory. Notably, the company holds nearly RMB 12 billion in cash and cash equivalents on its balance sheet. In light of earlier rumors regarding its bid to acquire Germany’s Stada Arzneimittel, Shanghai Pharmaceuticals is likely to make significant moves in mergers and acquisitions in 2017.

Shanghai Pharmaceuticals' Historical Performance

Performance Overview

Shanghai Pharmaceuticals’ predecessor was Shanghai No. 4 Pharmaceutical Co., Ltd., which was established in 1993 under the sponsorship of Shanghai Pharmaceutical (Group) Corporation, listed on the Shanghai Stock Exchange in 1994, and renamed Shanghai Pharmaceuticals Co., Ltd. in 1998.

In 2010, the China Securities Regulatory Commission (CSRC) approved Shanghai Pharmaceuticals’ absorption and merger with Shanghai Industrial Pharmaceutical Co., Ltd. and Shanghai Zhongxi Pharmaceutical Company, as well as the issuance of shares to Shanghai Pharmaceutical Group to acquire its pharmaceutical assets. Meanwhile, a private placement was conducted to raise funds from Shanghai Shangshi (Group) Co., Ltd. for the acquisition of pharmaceutical assets held by Shanghai Industrial Holdings Limited (SIHL), thereby completing a major asset restructuring.

As of March 22, 2017, the top five institutional shareholders of Shanghai Pharmaceuticals were HKSCC Nominees Limited, Shanghai Pharmaceutical (Group) Co., Ltd., Shanghai Industrial Holdings Limited, China International Capital Corporation (CICC), and Shanghai Guosheng Group. Together, they held 67.19% of its outstanding A-shares and H-shares. As both Shanghai Pharmaceuticals and Shanghai Industrial Holdings are key operating companies under the supervision of the Shanghai State-owned Assets Supervision and Administration Commission (Shanghai SASAC), the actual controller of Shanghai Pharmaceuticals is the Shanghai SASAC.

As of March 22, Shanghai Pharmaceuticals had 1.923 billion tradable shares and a total share capital of 2.689 billion, with a total market capitalization of RMB 61.845 billion, ranking it among the top ten listed companies in China’s pharmaceutical sector.

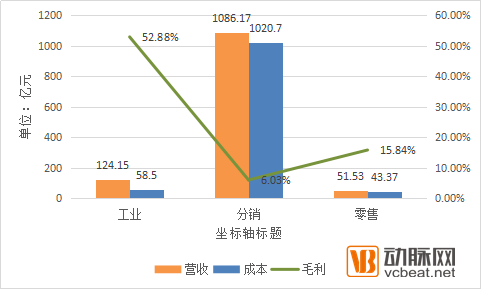

Shanghai Pharmaceuticals is primarily engaged in pharmaceutical manufacturing, distribution, logistics, and retail operations, with pharmaceutical distribution and logistics serving as its main revenue source. According to its 2016 annual report, the company’s pharmaceutical distribution business generated RMB 108.617 billion in revenue during the reporting period, while its pharmaceutical industrial segment recorded operating income of RMB 12.415 billion, and its pharmaceutical retail segment achieved revenue of RMB 5.153 billion.

Revenue and Cost Data by Business Segment

In terms of profit, Shanghai Pharmaceuticals’ industrial segment generated RMB 6.565 billion in profit, its distribution business achieved RMB 6.547 billion, and its retail operations recorded RMB 806 million. The profit from the industrial segment was nearly on par with that from distribution. This contrast is reflected in gross profit margins: the industrial segment’s gross margin stood at 52.88%, while the distribution business registered only 6.03%.

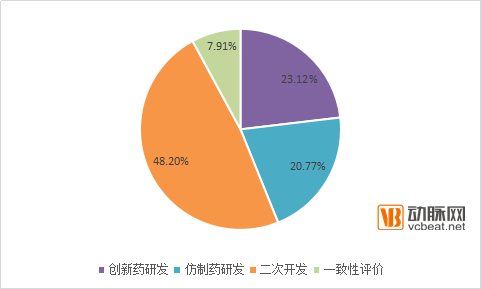

For this reason, Shanghai Pharmaceuticals has also increased its investment in pharmaceutical R&D. The annual report shows that the company’s total R&D expenditure last year amounted to RMB 670 million, accounting for 5.4% of its sales revenue. Of this amount, 23.12% was allocated to innovative drug development, 20.77% to generic drug development, 48.20% to secondary development of existing products, and 7.91% to consistency evaluations of quality and efficacy for generic drugs.

Shanghai Pharma's R&D Investment Composition

In terms of R&D strategy, Shanghai Pharmaceuticals stated that it has continuously optimized its R&D system and established an R&D Management Center, achieving multiple phased results. The company adheres to open collaboration and a combination of imitation and innovation, improves its R&D product pipeline, emphasizes the development of biologics, and strengthens efforts in secondary development of existing products, consistency evaluation of quality and efficacy for generic drugs, dosage form innovation, and internationalization.

As the Group’s “cash cow,” Shanghai Pharmaceuticals also places significant emphasis on the development of its pharmaceutical distribution business. According to the annual report, Shanghai Pharmaceuticals covers 25,000 medical institutions, including 24,000 hospitals (of which 1,322 are Grade III hospitals), 586 centers for disease control and prevention, and 129 hospital-consignee pharmacies. The proportion of pure sales to hospitals accounts for 60.79% of the total.

In the retail sector, Shanghai Pharmaceuticals operates 1,807 chain retail pharmacies, including 1,173 directly operated stores and 40 pharmacies jointly operated with medical institutions. “Shanghai Pharma Cloud Health” is a key focus of Shanghai Pharmaceuticals’ retail strategy, concentrating on prescription drugs to develop prescription purchasing and health services. The company launched the “Yiyao E-Prescription” project, establishing an e-prescription circulation system to collect and deliver outpatient prescriptions. Data shows that by the end of 2016, Shanghai Pharma Cloud Health had added 217,000 new e-prescriptions, a year-on-year increase of 600%, and newly connected with 30 hospitals nationwide, a year-on-year increase of 1,400%. Shanghai Pharmaceuticals stated that the Cloud Health project has laid the foundation for further development of innovative businesses.

Accelerated Expansion Through M&A

Another interesting data point in the annual report is that, according to its balance sheet, Shanghai Pharma’s cash and cash equivalents stood at RMB 11.966 billion as of December 31, 2016, compared with RMB 12.039 billion in the same period of the previous year, thereby maintaining a high level of liquidity.

Last year, Shanghai Pharmaceuticals made significant moves in mergers and acquisitions, officially completing the acquisition of Australia’s Vitaco Group on December 17 for RMB 938 million.

Prior to the release of the annual report, news emerged that Shanghai Pharmaceuticals and CVC Capital Partners (“CVC”) had joined forces to bid for Germany’s STADA Arzneimittel AG (“STADA”). Although Shanghai Pharmaceuticals subsequently issued a clarification announcement stating that it had “not submitted any formal letter of intent to any company, including STADA,” it also noted that it had “recently engaged in preliminary discussions with multiple European and American pharmaceutical companies,” leaving room for further speculation.

With RMB 12 billion in cash reserves, Shanghai Pharmaceuticals will certainly not limit its ambitions to Stada alone. Even if it participates in the bid, external estimates place the transaction value of Stada at merely USD 3.8 billion. Coupled with consortium support and related fundraising efforts, Shanghai Pharmaceuticals retains substantial financial flexibility for acquisitions. Therefore, inorganic expansion may well be its optimal strategic choice.

In fact, from the perspective of the entire pharmaceutical industry, according to statistics from VCBeat, the total amount of overseas mergers and acquisitions by Chinese pharmaceutical companies reached 40 billion last year. Leveraging capital to rapidly open up markets and acquire technology is a strategy that Chinese pharmaceutical companies highly favor. For Shanghai Pharmaceuticals, “borrowing a ship to go to sea” can also enhance its R&D capabilities, market share, and long-term growth momentum in the short term.

Zhou Jun, Chairman of Shanghai Pharmaceuticals, who had been in office for only five months, stated at the “Shanghai State-owned Assets Summit Forum” that Shanghai Pharmaceuticals would introduce new initiatives for internationalization over the next three to five years. “Our aim is to play a role in the future integration of capital markets and industry. We will continuously optimize our asset portfolio through financial investments, mergers and acquisitions, and leverage capital markets. Going forward, we will continue to build our business through mergers and acquisitions,” Zhou said at the time.

With the advancement of policies such as domestic consistency evaluation, the two-invoice system, the replacement of business tax with value-added tax (VAT), and healthcare insurance cost containment, the growth rate of the pharmaceutical market has slowed significantly compared to previous years, which has also become a driving force for Shanghai Pharmaceuticals’ overseas M&A and expansion.

Affected by financial report news, Shanghai Pharmaceuticals closed at 23.00 today, with an increase of 1.59%.