From Forced Transformation of Pharmaceutical Representatives to the Fantastic Journey of a Pill

On the 47th day after resigning, Zeng Yi found a new job with unchanged responsibilities: maintaining physician relationships.

Previously, he worked as a pharmaceutical sales representative and is currently employed at a mobile health company. The company provides users with services such as online light consultations, appointment registration, patient triage, and health management. Due to its extensive pool of physician resources and user data, it has attracted the attention of pharmaceutical manufacturers, leading to collaborative partnerships between the two parties. Mobile health companies seek financial gains, while pharmaceutical manufacturers aim to expand their distribution channels.

Thanks to his accumulated pool of physician resources, Zeng Yi’s onboarding was straightforward. In addition to maintaining relationships with physicians, he continued to monitor their prescribing practices. What has changed is the compensation structure: previously, performance-based pay was calculated based on volume, whereas now it is a fixed amount. All things considered, although his previous earnings were higher, they came with greater pressure; the current lower income is still acceptable.

Zeng Yi is the third case identified by VCBeat (WeChat: vcbeat) of a former pharmaceutical sales representative transitioning to an internet healthcare company. After pharmaceutical sales representatives increasingly became synonymous with a “gray ecosystem,” several employees resigned from Zeng Yi’s provincial distribution company. Beyond these individuals, tens of thousands of pharmaceutical sales representatives across China began to leave their traditional systems, although the vast majority remained within the pharmaceutical industry. Unlike those who departed later, Zeng Yi and his colleagues were fortunate enough to avoid that wave of public condemnation.

Pharmaceutical Sales Representatives Endure Growing Pains Amid Transformation

Some of these transitioning pharmaceutical sales representatives have moved to pharmaceutical distribution and logistics companies, while others have joined internet healthcare firms. Their job responsibilities, however, have remained largely unchanged; they continue to play a critical role in the pharmaceutical distribution process. Through their relationship management, medications reach end users from manufacturers via various channels. Their influence targets those who hold decision-making power over medication selection. Whether through volume-based procurement initiatives or relationship maintenance, this remains their primary objective.

Behind the transformation of the pharmaceutical sales representative community, where Zeng Yi belongs, policy pressure serves as the trigger, changes in the diagnosis and treatment system act as the lever, internet healthcare functions as the catalyst, and shifts in drug marketing channels represent the outward manifestation, with each factor building upon the previous one.

Pharmaceutical Individual Agent Information Posted on a Website

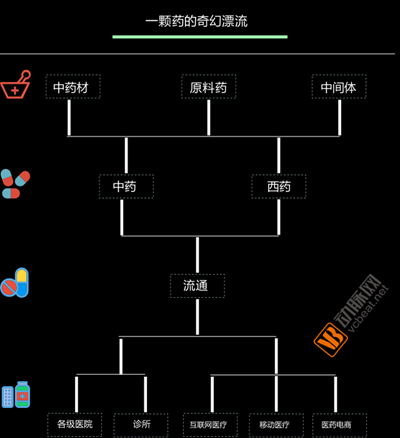

Delving deeper, it all revolves around the core element of “drugs.” What is the magic of pharmaceuticals, and why do they tug at the nerves of every link in the industry chain? Under the theme “The Fantastical Journey of a Pill,” VCBeat (WeChat ID: vcbeat) interviewed stakeholders from pharmaceutical manufacturers, distributors, retail pharmacy chains, e-pharmacy platforms, O2O pharmaceutical services, mobile health companies, and internet hospitals. The aim was to unravel the steps a pill takes from the manufacturer to the patient, and to clarify the roles played by each party along the way.

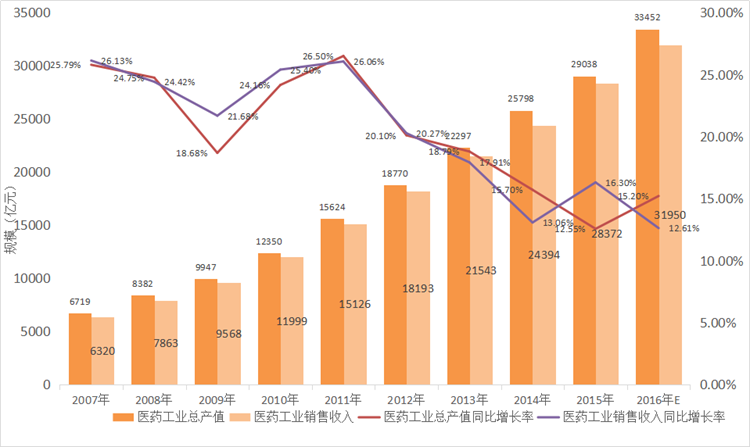

How Much Medication Do We Consume Annually?

The overall pharmaceutical industry (including pharmaceuticals, medical devices, health supplements, etc.) remains in a growth phase, although the growth rate has slightly declined, dropping by approximately half compared to the over 20% growth rate seen before 2012. In 2016, the total output value of the pharmaceutical industry reached RMB 3.34 trillion, representing a year-on-year increase of 15.2%; sales revenue of the pharmaceutical industry amounted to RMB 3.2 trillion, marking a 12.61% increase from the previous year.

Chart Note: Compiled from public information and research reports; data completeness and accuracy are not guaranteed. For reference only.

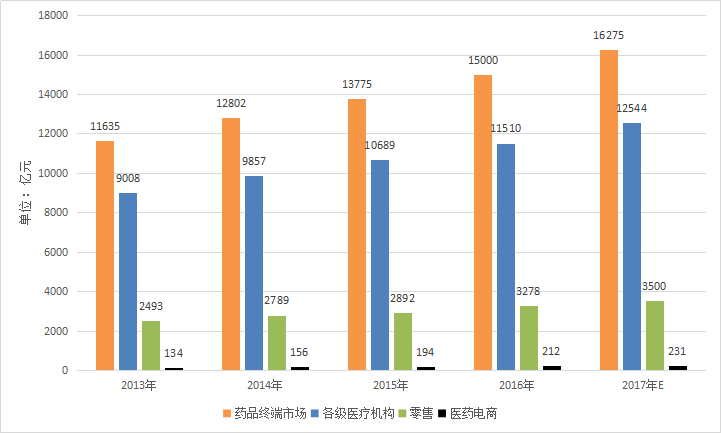

In terms of pharmaceuticals, the market size at the terminal end in 2016 was approximately RMB 1.5 trillion. Among this, drugs sold through medical institutions at various levels accounted for more than 75% of the total market size, amounting to RMB 1.15 trillion; the retail channel accounted for over 21%, with a value of RMB 327.8 billion; other channels and e-commerce platforms held a relatively small share, totaling RMB 21.2 billion.

Chart Note: Compiled from public information and research reports; data completeness and accuracy are not guaranteed. For reference only.

The above data also provides a rough overview of the pharmaceutical distribution channel structure, with medical institutions at all levels and retail channels accounting for approximately 80% and 20% of sales, respectively. As an emerging channel, pharmaceutical e-commerce accounts for less than 2% of the total market size.

Industrial Enterprises: Deepening Offline Presence, Actively Engaging Online

In terms of production capacity, there are over 4,000 pharmaceutical companies in China. The domestic drug registry comprises approximately 180,000 products (excluding expired or revoked approvals), while the imported drug registry includes around 4,700 products. Drug categories encompass chemical drugs, biological products, traditional Chinese medicines (TCM), active pharmaceutical ingredients (APIs), formulation intermediates, pharmaceutical excipients, diagnostic reagents, and combination drug-device products. Currently, more than 160,000 drug products are pending registration approval in China, and nearly 4,000 are undergoing clinical trial applications.

From the perspective of marketing channels, the distributor model and the delivery service provider model are the two mainstream marketing approaches adopted by pharmaceutical companies. The former involves multi-tiered agency distribution, where pharmaceutical manufacturers focus solely on production and the recruitment of regional agents. These regional agents leverage their resources with medical institutions such as hospitals and retail pharmacies to deliver products to end-users. Alternatively, pharmaceutical companies may control the marketing process through their in-house sales teams, employing compliant methods such as academic conferences and professional visits, while relying on delivery service providers for product shipment.

Two simple cases can be cited in this regard. The IPO prospectus of a small pharmaceutical company revealed that its core product portfolio consists of only three drugs, including anti-allergy agents, non-steroidal anti-inflammatory drugs (NSAIDs), and antibiotics (all generics), with annual sales of approximately RMB 200 million. The distributor model accounts for three-quarters of its domestic finished dosage form sales, while the delivery distributor model accounts for one-quarter.

The situation at large pharmaceutical companies is slightly different. A marketing professional from a leading domestic listed pharmaceutical company told VCBeat (WeChat ID: vcbeat) that, thanks to its strong R&D capabilities and portfolio of dozens of proprietary formulation products, its marketing efforts have primarily focused on in-house academic promotion, targeting hospital-based channels. Only in recent years has the company begun to explore the OTC and out-of-hospital markets.

Under the influence of a series of policies, including centralized drug procurement bidding, the replacement of business tax with value-added tax (VAT), Document No. 94, the two-invoice system, and Document No. 13, the existing marketing models of pharmaceutical manufacturers have been significantly impacted. For instance, previous practices such as affiliation and invoice passing—which were problematic due to multiple markups on drug prices and tax evasion—have been curbed. Many small-scale distributors have lost their operational basis and are unable to continue their businesses, necessitating that pharmaceutical companies strengthen their capabilities in executing ground-level marketing strategies.

The aforementioned representative from a listed pharmaceutical company also stated that, under the influence of policies such as secondary price negotiations, the separation of prescribing and dispensing, and the outflow of prescriptions, pharmaceutical companies have begun to more actively expand their channels—including the previously neglected out-of-hospital market and the internet healthcare market—in order to safeguard their interests. However, the industry’s shift remains relatively prudent, with efforts made to avoid disrupting the existing landscape of vested interests.

In terms of their attitude toward “going online,” pharmaceutical companies have been relatively proactive, engaging in collaborations with both pharmaceutical e-commerce platforms and internet healthcare providers. Their objectives are twofold: first, to conduct physician education initiatives, and second, to explore digital marketing strategies.

Distribution Enterprises: Transformation Pressures and Integration Trends

There are approximately 13,500 pharmaceutical distribution enterprises in China, most of which are small and medium-sized companies. Together with some virtual companies and natural persons possessing sales channels, they constitute the main entities implementing pharmaceutical distribution. Their business models include three categories: direct hospital sales, distribution and allocation, and fast-wholesale of generic drugs. Under the new series of policies regulating pharmaceutical distribution, all types of business entities are facing significant pain points.

Pain Points for Commercial Distribution Enterprises: Thin Margins, Lack of Professional Academic Promotion Teams, and the Risk of Being Replaced by Third-Party Logistics ProvidersCommercial pharmaceutical distributors face the pain point of razor-thin profit margins. Although they handle a wide range of clinical products, they lack specialized marketing teams to conduct compliant academic promotion, making it difficult to scale up product sales. As a result, pharmaceutical manufacturers are reluctant to collaborate with them on their flagship products, exposing these distributors to the risk of being replaced by third-party logistics (3PL) providers. For instance, SF Express has entered the pharmaceutical distribution sector by establishing pharmaceutical warehouses and cold-chain infrastructure, drawing significant attention from the industry.

The pain points for small and medium-sized distributors in the circulation sector include the lack of distribution qualifications, a significant decline in business, difficulty in obtaining regional sales rights for high-quality products from pharmaceutical manufacturers, insufficient academic marketing capabilities, capital shortages, and immense survival pressure. Furthermore, compliance issues associated with virtual companies and individual operators in the pharmaceutical industry—such as invoice passing and affiliation arrangements—are difficult to resolve, posing a risk of elimination.

A Chongqing-based pharmaceutical company with an integrated wholesale and retail business model told VCBeat that its previous procurement channels included major pharmaceutical distributors such as Jointown Pharmaceutical Group and Chongqing Pharmaceutical Group. The company then leveraged its own business network to supply hospitals and retail pharmacies in districts and counties, earning profits from the price differential. However, following the implementation of new pharmaceutical policies, these large distributors have begun establishing a presence at the grassroots level by deploying dedicated sales personnel. As a result, the group is currently considering whether to exit the pharmaceutical distribution business and focus primarily on retail operations.

This scenario of an integrated wholesale and retail pharmaceutical distribution company is fairly typical for small and medium-sized enterprises (SMEs) in the sector. Their operations are concentrated in three to four neighboring district- and county-level cities, with nearly 100 stores and annual revenue of approximately RMB 200 million. Distribution business accounts for about one-third of total revenue, but its profit margin is significantly lower than that of retail—by a factor of three to four. Therefore, discontinuing the wholesale business would be an acceptable option.

It is an inevitable trend in the consolidation of the pharmaceutical distribution industry for small and medium-sized commercial enterprises to either voluntarily exit the market or seek acquisition by larger companies. According to the 13th Five-Year Plan for Pharmaceutical Distribution, by 2020, China aims to cultivate a group of large-scale pharmaceutical distribution enterprises with nationwide network coverage and a high degree of intensification and informatization, such that the annual sales revenue of the top 100 pharmaceutical wholesalers accounts for more than 90% of the total pharmaceutical wholesale market.

This means that the industry must go through an inevitable phase of elimination and consolidation, which will undoubtedly bring about the growing pains of transformation, as seen in the aforementioned integrated wholesale and retail companies.

Retail Enterprises: Enhancing Services and Venturing into Clinical Care

According to statistical data from the China Food and Drug Administration, by the end of 2015, there were 4,981 retail pharmacy chains nationwide, operating 204,000 chain stores, while the number of independent pharmacies stood at 243,000, resulting in a chain store rate of 45.5%. Meanwhile, 13,200 new pharmacies were added that year, representing a 3.04% increase, which was lower than the growth rate of the chain store rate. The faster growth of chain stores compared to the overall addition of new pharmacies indicates that the retail pharmacy sector is undergoing further consolidation.

Where Does the Integrated Vision Lie? The U.S. market may serve as a reference. Taking the U.S. market as an example, the chain affiliation rate of retail pharmacies is approximately 75%, nearly 30 percentage points higher than that in China. Meanwhile, its market concentration is relatively high, with three pharmacy retail giants—CVS, Walgreens, and Rite Aid—accounting for more than 75% of the U.S. pharmaceutical retail market share, operating over 4,000 stores. In contrast, the top ten retail pharmacy chains in China hold a relatively low market share, and their store networks do not yet meet the standard for nationwide coverage.

The consolidation of China’s domestic pharmaceutical retail market is being driven by listed companies and regional leaders. Yixintang, Yifeng Pharmacy, Laobaixing Pharmacy, Guoda Drugstore, and Shuyu Civilian Pharmacy have all raised capital in the secondary market to fund mergers and acquisitions (notably, Yixintang’s annual report data shows that its store count exceeded 4,000 by the end of 2016). Other regional pharmacy leaders, such as Gansu Zhongyou and Shandong Lijian, have also expanded aggressively with the support of industrial capital.

Amidst the fierce competition for market share, pharmacies are also diversifying their service offerings, driven by pharmaceutical policies and shifting consumer demand. Large and medium-sized chain pharmacies, in particular, are focusing not only on expanding their scale but also on evolving their functional models, gradually developing services such as pharmaceutical care, medication delivery, chronic disease management, specialty pharmacy services, and health benefit management.

First is the consultation service. VCBeat (WeChat: vcbeat) previously reported that the Chengdu Municipal Drug Administration launched an electronic prescription pilot program among chain pharmacies across the city. More than 3,000 pharmacies have activated consultation services, and over 1,800 have joined the electronic prescription pilot. These pilot pharmacies will provide consumers with health consultations, electronic prescription issuance, and verification services.

The collaboration between internet healthcare and retail pharmacies also holds significant promise, as exemplified by the “Pharmacy-Clinic-Store Project” led by WeDoctor. By partnering with chain pharmacies to integrate consultations from the Wuzhen Internet Hospital into their stores, WeDoctor has connected more than 12,000 pharmacies, handling an average of 26,000 consultations per day. This demonstrates that pharmacies have adopted a proactive stance toward introducing consultation services, yielding notably effective results.

WeDoctor Wuzhen Internet Hospital Pharmacy Consultation Point

Secondly, it serves as the entry point for health management services. In fact, many companies have already proposed this concept, including Dingdang Kuaiyao, under Renhe Pharmaceutical Group, with its “Smart Pharmacy” initiative, and Haoyaoshi Pharmacy with its “Health Service Point.” Both aim to position physical pharmacies as the gateway and platform for the future broader health industry.

From the perspective of pharmaceutical care services provided by pharmacies, it is only natural to serve as an entry point for health management. By establishing user health records and subsequently engaging in full-cycle health management services, pharmacies can both enhance user stickiness and achieve a functional closed loop.

Recently, some pharmacies have introduced the concept of "new retail" in pharmacy, which integrates offline pharmacies with online applications to provide consumers with experiential and personalized services. Although still in the conceptual stage, this approach has opened up new directions for the business expansion of offline pharmacies.

E-Commerce in Pharmaceuticals: Nascent Yet Facing a Long and Arduous Journey

The origins of pharmaceutical e-commerce can be traced back to the 2005 issuance of the Interim Provisions on the Approval of Internet Drug Transaction Services. At that time, “internet drug transactions” referred to the exchange of information and facilitation of transactions via online platforms among pharmaceutical manufacturers, distributors, retailers, and hospitals, as well as the provision of online purchasing channels for individual consumers.

To date, the concept of pharmaceutical e-commerce has gradually expanded, giving rise to a series of drug-centric new services such as pharmaceutical marketing, pharmaceutical O2O (online-to-offline), medicinal materials trading, and pharmaceutical care services. However, the sector is currently dominated by online pharmacies, whose business models and profit drivers are relatively clear and have gained recognition from both the market and consumers.

Pharmaceutical E-commerce Landscape

Currently, three major bottlenecks are constraining the development of pharmaceutical e-commerce. First, there are restrictions on the online sale of prescription drugs; in the short term, regulators are unlikely to lift these restrictions due to concerns over medication safety. Second, integration with medical insurance remains a challenge. The primary issue is that China’s medical insurance system is managed at the regional level, while nationwide pooling is still in the planning stage. As a result, pharmaceutical e-commerce platforms cannot facilitate cross-regional medical insurance reimbursement for drug purchases. Third, consumer perception poses a hurdle. Unlike general consumer goods, pharmaceuticals have not yet been fully accepted by the public as an e-commerce category. The market requires further cultivation, and consumer habits will take time to evolve.

VCBeat (WeChat: vcbeat) consulted Xie Fangmin, CEO of Jianke.com, who provided an interpretation from the perspective of an industry insider on how pharmaceutical e-commerce is transforming drug distribution channels.

Xie Fangmin told VCBeat that pharmaceutical companies value the e-commerce channel because it allows them to directly access raw consumer data. Through this information, pharmaceutical companies can identify who is purchasing their medications and determine which product categories perform well in specific regions—insights that are unattainable through traditional distribution channels.

Pharmaceutical companies have also made significant adjustments to adapt to the pharmaceutical e-commerce channel, including modifying dosage forms and specifications to meet the demands of this channel.

Xie Fangmin believes that the collaboration between pharmaceutical companies and online pharmacies is the result of two-way communication. In addition to pharmaceutical companies adapting to distribution channels, online pharmacies themselves must also undertake significant efforts to earn the trust of pharmaceutical manufacturers. This includes meeting hard metrics related to warehousing as well as soft metrics concerning data processing capabilities.

He cited as an example that Jianke and Abbott recently launched the non-invasive glucose meter developed by the latter in China, following extensive communication and standard-setting efforts. To support this launch, Jianke invested millions to renovate its warehouses and upgrade its temperature-controlled storage environment.

Group photo featuring Jianke.com CEO Xie Fangmin, Eric Shroff, Vice President of Abbott’s Asia Pacific Diabetes Care Division, and others

“For pharmaceutical e-commerce, I agree with the assertion that the supply chain is its lifeline. The four major challenges in supply chain management for pharmaceutical e-commerce platforms are product assortment listing, price acquisition, and ensuring timely and stable supply,” said Xie Fangmin.

From the perspective of channel structure, Xie Fangmin believes that pharmaceutical companies’ “entry into the online space” is a slow and gradual process. It is a systematic endeavor involving various aspects, such as channel transformation and adjustment of interest structures. Nevertheless, pharmaceutical companies are increasingly eager to embrace pharmaceutical e-commerce. Through the establishment of the “Authentic Products Alliance,” Jianke has partnered with thousands of well-known pharmaceutical companies, including domestic and international leaders in chemical and traditional Chinese medicines such as Pfizer, Bayer, GlaxoSmithKline, Tongrentang, and Baiyunshan.

Overall, pharmaceutical e-commerce is poised to become a highly significant channel alongside healthcare institutions and out-of-hospital retail. To capitalize on potential growth, pharmaceutical e-commerce companies should strengthen their capabilities in supply chain, technology, and management.

Internet Healthcare: The Pharmaceutical Closed Loop and Stakeholder Interests

Recently, Yinchuan City held a centralized signing ceremony for internet hospitals. Seventeen well-known Chinese internet healthcare companies, including Chunyu Doctor, DXY, and Qilekang, jointly signed agreements with Yinchuan to establish the Yinchuan Smart Internet Hospital Base. This number accounts for nearly half of the total number of internet hospitals nationwide in the previous year, pushing the concept of internet healthcare to its “tipping point.”

Analysys·Ecosystem Map of the Internet Healthcare Market

How is internet-based healthcare, represented by online hospitals, penetrating the pharmaceutical distribution sector? We selected two cases for analysis: WeDoctor and Chunyu Doctor.

In addition to the aforementioned “Pharmacy-Clinic-Store” project, WeDoctor has also made strategic moves in the pharmaceutical sector. This is reflected in two sections within its app: “Health Cloud City” and “Online Pharmacy.” Health Cloud City offers over-the-counter (OTC) medications and health supplements, while the Online Pharmacy provides prescription drugs and common medical devices. However, purchasing medications from the Online Pharmacy requires consultation with contracted physicians affiliated with WeDoctor.

Screenshot of the WeDoctor App

According to VCBeat, the pharmaceutical products in the aforementioned two segments are supplied by Jinxiang.com. In 2015, WeDoctor completed its acquisition of a controlling stake in Jinxiang.com, with Lu Zigui, Vice President of WeDoctor, appointed as CEO of Jinxiang.com. Established in 2007, Jinxiang.com is one of the earliest enterprises in China engaged in pharmaceutical e-commerce. According to the revenue data publicly disclosed by WeDoctor Group, its annual revenue is approximately RMB 1 billion, with profit sources including insurance, internet hospitals, and pharmaceuticals.

As a representative of mobile healthcare, Chunyu Doctor entered the pharmaceutical business at an early stage. It has successively established partnerships with Haoyaoshi Online Pharmacy, Dingdang Kuaiyao, and 111.com (Yi Yao Wang), and also collaborates with the pharmaceutical manufacturer AstraZeneca.

Tan Wanneng, Public Relations Director at Chunyu Doctor, stated in an interview with VCBeat that Chunyu Doctor has consistently led the industry in accumulating users and data on both the physician and patient sides. Leveraging its influence among physicians and users, Chunyu Doctor has been actively engaged in educating both groups since 2014, thereby becoming a reliable channel for digital marketing by healthcare industry partners, including pharmaceutical companies.

According to Tan Wanneng, the explicit objectives of the collaboration between AstraZeneca and Chunyu Doctor are threefold: enhancing the efficiency and stickiness of doctor-patient interactions, improving patient adherence, and helping physicians manage patients more effectively. Ultimately, these efforts aim to promote standardized diagnosis and treatment as well as rational medication use for chronic diseases such as cardiovascular conditions.

Spring Rain Doctor and AstraZeneca Signing Ceremony

From the very essence of healthcare, medical services and pharmaceuticals are inextricably linked; wherever there is a demand for medical care, there is inevitably a corresponding demand for pharmaceutical products. Therefore, it is almost inevitable for internet healthcare platforms to venture into pharmaceutical distribution. Entry strategies may include building proprietary systems, as adopted by WeDoctor, or partnering with pharmaceutical manufacturers and e-commerce platforms, as chosen by Chunyu Doctor.

In addition to the “medicine + healthcare” model, the “pharmaceuticals + healthcare” trend is also evident. For instance, 1YaoWang, Jianke, and Qilekang are actively laying out internet hospital services or launching mobile medical businesses. It can be concluded that, regardless of whether it is “medicine + healthcare” or “pharmaceuticals + healthcare,” there are only two fundamental driving forces: first, creating a closed-loop user experience, and second, pursuing economic interests.

Supplementary Text: The Demise of Pharmaceutical Sales Representatives

A Baidu search for the keyword “pharmaceutical sales representative” yields 17.8 million results, with search trends peaking last December and an average of 3,352 daily search queries. The CCTV undercover report on the “kickback scandal” struck a nerve among Chinese citizens concerned about the difficulty and high cost of accessing medical care, leading many to identify pharmaceutical sales representatives as the hidden drivers behind soaring drug prices and briefly channeling public frustration toward the healthcare system.

By February this year, the provisions on the registration and filing of medical representatives in Document No. 13 issued by the China Food and Drug Administration drove searches for the keyword “medical representative” to a new peak.

It is difficult to predict when the next peak for “pharmaceutical representatives” will occur, whether triggered by the introduction of relevant policies or by further revelations of kickback schemes. One thing is certain: the issue of illicit inducements in pharmaceutical sales has drawn the attention of the industry, regulatory authorities, and the general public.

Baidu Index for Medical Representatives

The profession of pharmaceutical sales representative was not pioneered in China. Originally, there were no such roles in the country; it was only in the late 1980s, as joint-venture and foreign-funded pharmaceutical companies gradually established their presence in China, that they introduced pharmaceutical sales representatives as a new concept to the Chinese market.

The initial role of medical representatives at foreign pharmaceutical companies was to introduce the efficacy and usage of drugs to physicians from an evidence-based medicine perspective, as well as to provide timely feedback on adverse reactions; sales figures were never used as performance evaluation metrics.

Changes occurred in the mid-1990s, as the number of domestic pharmaceutical companies increased and a large volume of generic drugs entered the market, intensifying competition within the pharmaceutical industry. With similar efficacy and comparable pricing, pharmaceutical representatives began offering gifts, cash envelopes (“hongbao”), and kickbacks to influence physicians’ prescribing decisions in favor of their companies’ products. “How to penetrate hospitals” and “how to maintain relationships” became essential skills for newcomers in the pharmaceutical sales profession.

It can be said that the weak R&D capabilities of domestic pharmaceutical companies, coupled with a sales-oriented approach, have given rise to the gray area within the role of medical representatives—namely, kickback-driven sales.

So-called "kickback-driven sales" refers to the practice whereby pharmaceutical representatives provide illegal cash commissions to hospitals and physicians based on sales performance. Due to the inherent professional characteristics of medicine, drug sales ultimately hinge on physicians’ prescriptions; consequently, competition invariably converges on frontline clinicians (with benefits also extended to individuals involved in tendering, procurement, and prescription data aggregation who can influence drug sales volumes).

It may be more appropriate to describe the relationship between pharmaceutical sales representatives and benefit recipients as “each taking what they need.” On one hand, the public-welfare nature of public medical institutions dictates that they cannot pursue profits excessively; the compensation of doctors and medical staff is disproportionate to their labor input, and pharmaceutical kickbacks serve as an invisible supplement. On the other hand, the low cost of generic drugs enables pharmaceutical companies to cede a portion of the benefits to sales personnel (agents) and doctors in exchange for market share, while simultaneously ensuring the companies’ expected profitability.

So, do pharmaceutical sales representatives drive up drug prices? The answer is yes. At the end of last year, China Central Television (CCTV) exposed the kickback scheme between pharmaceutical sales representatives and physicians, with doctors’ kickbacks accounting for 30% to 40% of drug prices. This is also why pharmaceutical sales representatives have faced intense public backlash; the kickback practices they facilitate have significantly increased healthcare costs and the financial burden on both medical insurance systems and individual patients.

How to Address the Issue of Improper Benefit Transfers by Pharmaceutical Representatives: Where to Begin? The most direct and effective approach is to enforce strict investigations and crackdowns. Several provinces have conducted public trials on pharmaceutical bribery cases, which have served as a deterrent and yielded modest results in curbing kickback-driven sales by pharmaceutical representatives. However, many other provinces remain in a wait-and-see stance.

The pharmaceutical distribution chain is lengthy and involves numerous stakeholders; therefore, simply cracking down on medical representatives is not a sufficient solution to the issue of drug pricing. Policymakers believe that further efforts should be made to dismantle the mechanism of subsidizing healthcare services with drug profits. Adhering to the coordinated reform of medical care, health insurance, and pharmaceuticals, we should comprehensively advance reforms such as abolishing drug markups, adjusting prices for medical services, and encouraging patients to purchase medications from retail pharmacies. We must fulfill government funding responsibilities and accelerate the establishment of a new compensation mechanism for public hospitals. We will promote the separation of prescribing from dispensing. Medical institutions shall prescribe medications by their generic names and proactively provide prescriptions to patients.

Outpatients may freely choose to purchase medications either at medical institutions or at retail pharmacies; medical institutions shall not restrict outpatients from purchasing medications at retail pharmacies with a prescription. Where conditions permit, the separation of outpatient pharmacies from medical institutions may be explored. Efforts should be made to establish interconnectivity and real-time sharing among prescription information from medical institutions, medical insurance settlement data, and pharmaceutical retail consumption records.

Analysis suggests that in a mature healthcare market, originator drugs and surgical instruments indeed require academic promotion and professional support from manufacturers during their clinical adoption. Meanwhile, routine commercial promotion of pharmaceuticals is also part of the responsibilities of medical representatives. However, the legal boundary lies in prohibiting the inducement of physicians’ prescribing behaviors through improper benefits.

In China, the widespread lack of academic foundations among domestic pharmaceutical companies, coupled with inadequate regulatory oversight, has given rise to a pervasive model of kickback-driven sales. Medical representatives have gradually been reduced to intermediaries for bribing physicians and hospital administrators, a system that remains mainstream in the pharmaceutical market to this day.

Kickback-driven sales have alienated physicians’ prescribing behavior, distorted the market’s compensation system, and ultimately exacerbated doctor–patient relations. Campaign-style rectification efforts have failed to make any dent in this system.

In fact, in addition to policy guidance, industrial development has also provided opportunities for the transformation of pharmaceutical sales representatives. VCBeat (WeChat ID: vcbeat) interviewed several cases of such transitions, all of which involved leveraging experience as pharmaceutical sales representatives to enter healthcare-related industries, with notable success.

These include positions at mobile health companies, pharmaceutical e-commerce platforms, health management firms, and offline Traditional Chinese Medicine (TCM) clinics, with some individuals even becoming founding partners.

Meanwhile, there are also calls to retain pharmaceutical sales representatives who engage in academic promotion, serving as a bridge for communication between pharmaceutical companies, hospitals, and physicians, thereby facilitating the better application of new drugs.

Overall, the pharmaceutical industry faces demands for structural adjustment (eliminating non-compliant enterprises through the Generic Drug Consistency Evaluation), regulation of distribution (promoting standardized drug distribution and increasing industry concentration via the Two-Invoice System), and cost control (curbing individual and medical insurance expenditures by abolishing the practice of subsidizing healthcare with drug profits and reducing the proportion of drug costs).

Addressing the issue of pharmaceutical sales representatives is a good entry point, but efforts should not be solely focused on this aspect. A combination of regulation and guidance should be adopted to promote the healthy and sustainable development of pharmaceutical distribution.

Reporter's Notes: Diversified Channels, Significant Integration

The original intent of this article is to explore how pharmaceuticals reach consumers through various channels. In reality, the two most dominant distribution channels remain hospital pharmacies and retail pharmacies. Online pharmaceutical e-commerce may be more suitable for patients with chronic diseases and those requiring long-term medication, as it is often too late to purchase and take medication after the onset of acute conditions like the common cold.

For this reason, some players have entered the O2O medicine delivery market, including Alibaba Health’s “Pioneer Alliance,” as well as Kuai Fang Song Yao, Ding Dang Kuai Yao, and the Hao Yao Shi app. However, their service coverage remains limited, with their service areas largely overlapping with those covered by physical pharmacies (in essence, they are also retail pharmacies).

Looking back, what is the current state of pharmaceutical distribution? What is the mindset of pharmaceutical manufacturers? While these questions have been addressed to some extent, the answers remain somewhat insufficient for the entire drug distribution market. This is because the pharmaceutical industry is a systemic endeavor involving multiple complex issues such as policy compliance, industrial chain division of labor, and divergent stakeholder interests. Any single one of these topics alone could warrant a comprehensive volume.

This addresses the sales aspect, but what about payment? The most intriguing characteristic of pharmaceutical consumption is that the decision-makers, payers, and consumers are often distinct groups: physicians prescribe medications, health insurance (including commercial insurance) covers the costs, and patients use the drugs. Consequently, academic conferences and medical representatives emerged as mechanisms to influence prescribing behavior and drive pharmaceutical sales. While such practices have diminished, new platforms leveraging internet healthcare now command resources spanning hundreds of thousands of physicians. If these platforms can influence physicians’ prescribing authority, could they be considered the largest “medical representatives”?

Ultimately, it boils down to two phrases: “diversified channels and significant integration.” From the end-user’s perspective, diversified channels mean that medicines can be purchased through various platforms, including offline hospitals and pharmacies; online general e-commerce platforms (Tmall, JD.com); specialized pharmaceutical e-commerce platforms (1 Drug Network, Jianke, Haoyaoshi, Qilekang); and internet healthcare platforms (WeDoctor, HaoDaifu Online, Chunyu Doctor), among others.

Integration clearly refers to a single pharmaceutical company becoming increasingly involved in a wider range of pharmaceutical-related businesses, spanning production, distribution, and direct-to-consumer services within the industry chain. Examples include the integration of internet healthcare with pharmaceutical e-commerce, and the convergence of manufacturing enterprises with retail pharmacy chains.

With the addition of insurance, can healthcare, pharmaceuticals, and insurance form a closed loop? Everything is just getting started.

Note: At the interviewee’s request, “Zeng Yi” is a pseudonym, and certain identifying details of other interviewees have also been partially anonymized. Chun Lin from VCBeat also contributed to this article.